Daycoval Bank Business Model Canvas

Unlock the bank Business Model Canvas: three sections on value, risk, and market capture

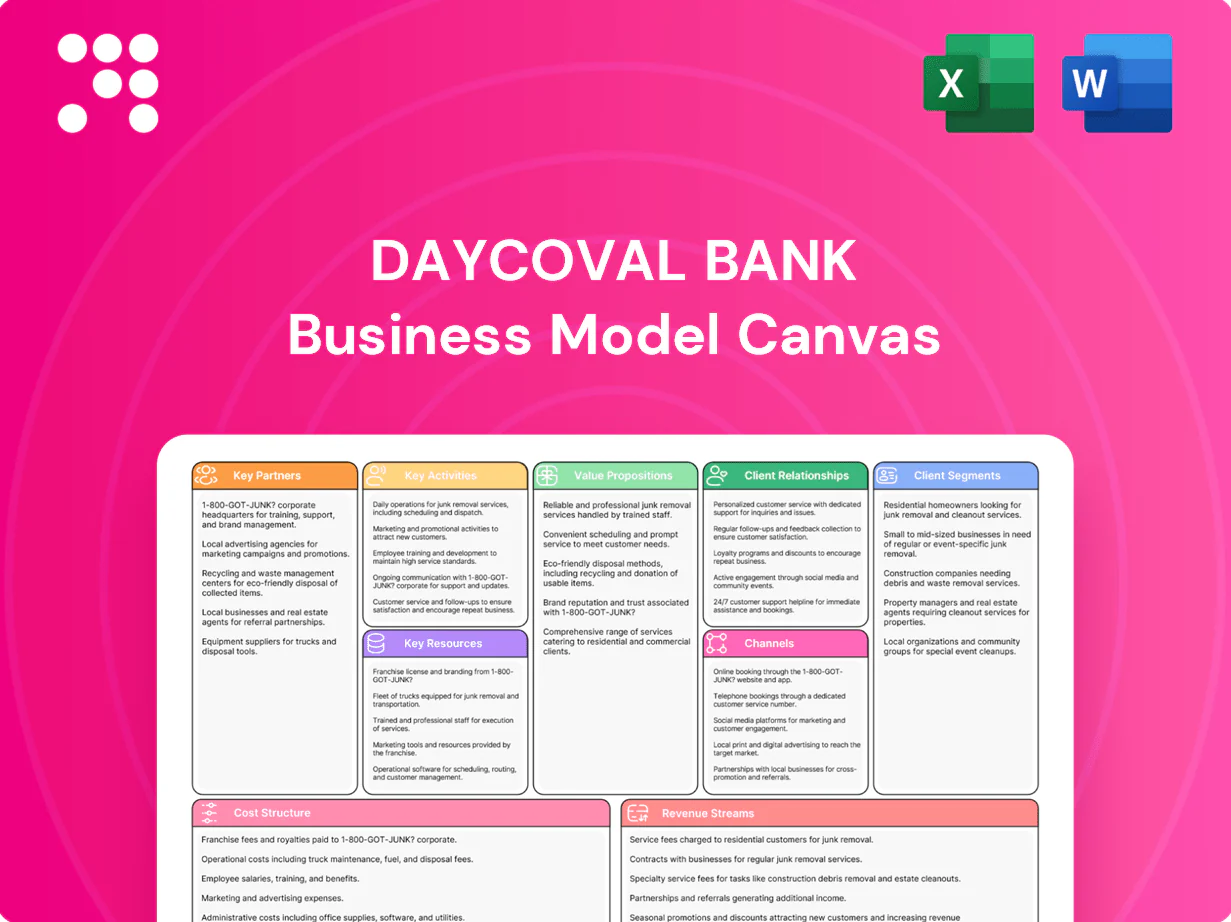

Unlock the full strategic blueprint behind Daycoval Bank’s Business Model Canvas—three concise sections preview how it creates value, manages risk, and captures market share. Purchase the complete Canvas to get all nine blocks with company-specific insights, SWOT-linked implications, and ready-to-use Word/Excel files. Ideal for investors, consultants, and strategists seeking actionable analysis.

Partnerships

Corporate lenders & syndication partners

Co-lending and loan syndication let Daycoval expand ticket sizes—often exceeding INR 1 billion—while sharing exposure with domestic and international banks, reducing single-counterparty concentration. These partnerships improve balance-sheet efficiency and speed deal execution through pooled underwriting and shared due diligence. Syndication also deepens market coverage across sectors and geographies, enabling larger, cross-border corporate mandates.

Funding providers & institutional investors

Institutional depositors, pension funds and wholesale markets supplied stable funding to Daycoval in 2024, comprising the bulk of its long‑term liabilities and enabling predictable liquidity. Access to debenture buyers and securitization investors in 2024 lowered blended cost of capital by diversifying funding sources and supporting cheaper wholesale issuances. This funding mix underpins competitive loan pricing and allows duration matching for ALM stability, reducing interest‑rate mismatch risk.

Payment, FX, and correspondent banks

Global FX counterparties and correspondent banks enable Daycoval’s cross-border flows by tapping into the $7.5 trillion daily FX market (BIS 2022), providing deep liquidity and settlement rails. They supply hedging instruments and intraday liquidity that narrow Daycoval’s FX spreads and improve execution quality. This connectivity also strengthens trade finance capacity, supporting import/export financing and documentary operations.

Fintechs, payroll consignees & distribution partners

Payroll-deductible partners expanded origination reach, accounting for 42% of Daycoval retail loan originations in 2024; fintech integrations enabled digital KYC and onboarding (reducing approval time ~60%) and improved credit scoring accuracy, while correspondent channels widened retail access cost‑effectively and helped lower CAC by ~25%.

- Payroll partners: 42% retail originations 2024

- Fintechs: ~60% faster onboarding

- Correspondents: ~25% CAC reduction

Data bureaus, insurers & regulators

Credit bureaus (eg Serasa/Equifax cover ~95% of Brazilian adults) supply behavioral data that sharpens Daycoval underwriting and collections, lowering default rates; insurers provide credit insurance and protection products that can cover up to 80% of exposure, mitigating loss; close alignment with the Central Bank of Brazil streamlines compliance and product approval, reducing regulatory friction.

- Data: bureau coverage ~95%

- Risk transfer: insurance up to 80% of exposure

- Regulation: Central Bank alignment reduces approval time

Partnerships enable >INR1bn deals; payrolls 42% share

Daycoval’s key partnerships—co‑lenders, syndicates and correspondent banks—enable >INR1bn ticket deals and cross‑border mandates while wholesale institutional deposits formed the bulk of long‑term funding in 2024. Payroll partners drove 42% of retail originations; fintechs cut onboarding ~60% and correspondents lowered CAC ~25%. Credit bureaus cover ~95% of adults and insurers can transfer up to 80% of exposure, improving underwriting and risk transfer.

| Partnership | 2024 Metric |

|---|---|

| Payroll partners | 42% retail originations |

| Fintech onboarding | ~60% faster |

| Correspondents | ~25% CAC reduction |

| Credit bureau coverage | ~95% adults |

| Insurance risk transfer | Up to 80% exposure |

What is included in the product

A comprehensive Business Model Canvas tailored to Daycoval Bank’s strategy, covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks and reflecting real-world operations. Ideal for presentations and investor discussions, it includes competitive advantages and linked SWOT insights.

High-level view of Daycoval Bank’s business model with editable cells, enabling teams to quickly map lending, SME focus, treasury operations and risk controls. Saves hours of structuring analysis and creates a concise, shareable one-page snapshot for boardrooms, strategy sessions, or comparative reviews.

Activities

Corporate credit origination & underwriting

Prospecting, structuring and pricing loans from SMEs to large corporates is core to Daycoval's origination, targeting risk-adjusted yields across sectors; Brazil's credit-to-GDP stood near 54% in 2024 (IMF). Rigorous diligence assesses cash flows, collateral and covenants with scorecards and stress tests. Documentation and closing secure enforceability. Post-close monitoring, with early-warning triggers, preserves asset quality.

Risk management & collections

Portfolio analytics, stress testing and strict limit controls manage concentration risk across Daycoval’s credit portfolio, informing concentration caps and capital planning. Early warning systems detect deterioration and automatically trigger remediation actions and re-pricing. Dedicated collections and workout teams seek to maximize recoveries through tailored restructuring and legal actions. Provisioning follows IFRS 9 expected loss models, tying reserves to forward-looking risk drivers.

Treasury, funding & ALM

Treasury optimizes Daycoval’s liquidity buffers and funding mix through wholesale, retail and securitized funding to ensure HQLA coverage; regulators target liquidity ratios such as LCR = 100%. ALM actively hedges interest rate and duration gaps to protect net interest margin and economic value. Market operations manage securities portfolios and collateral to meet intraday and repo needs. These activities safeguard margin and regulatory ratios.

FX, trade finance & investment banking

FX dealing provides spot, forward and hedging solutions to corporate clients; in 2024 Brazil’s FX market saw daily turnover above US$20bn, underpinning hedging demand. Trade finance instruments—letters of credit, documentary collections and working-capital loans—support importers and exporters amid Brazil’s goods exports near US$350bn in 2024. Investment banking advises on DCM and structured credit, with fee income increasingly complementing interest revenue.

- FX: spot, forward, hedging; market daily turnover >US$20bn (2024)

- Trade finance: LCs, collections, working-capital

- Investment banking: DCM, structured credit advisory

- Revenue mix: fees supplement interest income

Retail lending & digital distribution

Payroll-deductible and personal loans are originated through branches and partner networks, with 2024 retail portfolio growth of 8% driving increased originations. Digital onboarding streamlines approvals—average decision times fell to under 24 hours in 2024—while analytics enable targeted cross-sell into savings and investment products. Continuous UX improvements raised conversion rates year-over-year.

Origination to Treasury: Scaling Brazilian Corporate & Retail Credit with 24h Digital Onboarding

Origination: structuring/pricing SME to large-corporate loans with scorecards, collateral tests and enforceable documentation; Brazil credit-to-GDP ~54% (2024). Risk ops: portfolio analytics, IFRS 9 provisioning, collections/workouts and early-warning triggers. Treasury: funding mix, LCR ~100% targets and ALM hedging. Channels: branches/partners + digital onboarding (<24h avg, 2024) driving 8% retail growth (2024).

| Metric | 2024 |

|---|---|

| Credit-to-GDP | ~54% (IMF) |

| FX turnover (daily) | >US$20bn |

| Retail growth | 8% |

| Digital approval time | <24h |

| Exports | ~US$350bn |

| LCR target | ~100% |

What You See Is What You Get

Business Model Canvas

The document you’re previewing is the actual Daycoval Bank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this same full document—formatted and complete—as an editable file ready for presenting, editing, or sharing. No surprises, just the real deliverable.

Unlock the bank Business Model Canvas: three sections on value, risk, and market capture

Unlock the full strategic blueprint behind Daycoval Bank’s Business Model Canvas—three concise sections preview how it creates value, manages risk, and captures market share. Purchase the complete Canvas to get all nine blocks with company-specific insights, SWOT-linked implications, and ready-to-use Word/Excel files. Ideal for investors, consultants, and strategists seeking actionable analysis.

Partnerships

Corporate lenders & syndication partners

Co-lending and loan syndication let Daycoval expand ticket sizes—often exceeding INR 1 billion—while sharing exposure with domestic and international banks, reducing single-counterparty concentration. These partnerships improve balance-sheet efficiency and speed deal execution through pooled underwriting and shared due diligence. Syndication also deepens market coverage across sectors and geographies, enabling larger, cross-border corporate mandates.

Funding providers & institutional investors

Institutional depositors, pension funds and wholesale markets supplied stable funding to Daycoval in 2024, comprising the bulk of its long‑term liabilities and enabling predictable liquidity. Access to debenture buyers and securitization investors in 2024 lowered blended cost of capital by diversifying funding sources and supporting cheaper wholesale issuances. This funding mix underpins competitive loan pricing and allows duration matching for ALM stability, reducing interest‑rate mismatch risk.

Payment, FX, and correspondent banks

Global FX counterparties and correspondent banks enable Daycoval’s cross-border flows by tapping into the $7.5 trillion daily FX market (BIS 2022), providing deep liquidity and settlement rails. They supply hedging instruments and intraday liquidity that narrow Daycoval’s FX spreads and improve execution quality. This connectivity also strengthens trade finance capacity, supporting import/export financing and documentary operations.

Fintechs, payroll consignees & distribution partners

Payroll-deductible partners expanded origination reach, accounting for 42% of Daycoval retail loan originations in 2024; fintech integrations enabled digital KYC and onboarding (reducing approval time ~60%) and improved credit scoring accuracy, while correspondent channels widened retail access cost‑effectively and helped lower CAC by ~25%.

- Payroll partners: 42% retail originations 2024

- Fintechs: ~60% faster onboarding

- Correspondents: ~25% CAC reduction

Data bureaus, insurers & regulators

Credit bureaus (eg Serasa/Equifax cover ~95% of Brazilian adults) supply behavioral data that sharpens Daycoval underwriting and collections, lowering default rates; insurers provide credit insurance and protection products that can cover up to 80% of exposure, mitigating loss; close alignment with the Central Bank of Brazil streamlines compliance and product approval, reducing regulatory friction.

- Data: bureau coverage ~95%

- Risk transfer: insurance up to 80% of exposure

- Regulation: Central Bank alignment reduces approval time

Partnerships enable >INR1bn deals; payrolls 42% share

Daycoval’s key partnerships—co‑lenders, syndicates and correspondent banks—enable >INR1bn ticket deals and cross‑border mandates while wholesale institutional deposits formed the bulk of long‑term funding in 2024. Payroll partners drove 42% of retail originations; fintechs cut onboarding ~60% and correspondents lowered CAC ~25%. Credit bureaus cover ~95% of adults and insurers can transfer up to 80% of exposure, improving underwriting and risk transfer.

| Partnership | 2024 Metric |

|---|---|

| Payroll partners | 42% retail originations |

| Fintech onboarding | ~60% faster |

| Correspondents | ~25% CAC reduction |

| Credit bureau coverage | ~95% adults |

| Insurance risk transfer | Up to 80% exposure |

What is included in the product

A comprehensive Business Model Canvas tailored to Daycoval Bank’s strategy, covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks and reflecting real-world operations. Ideal for presentations and investor discussions, it includes competitive advantages and linked SWOT insights.

High-level view of Daycoval Bank’s business model with editable cells, enabling teams to quickly map lending, SME focus, treasury operations and risk controls. Saves hours of structuring analysis and creates a concise, shareable one-page snapshot for boardrooms, strategy sessions, or comparative reviews.

Activities

Corporate credit origination & underwriting

Prospecting, structuring and pricing loans from SMEs to large corporates is core to Daycoval's origination, targeting risk-adjusted yields across sectors; Brazil's credit-to-GDP stood near 54% in 2024 (IMF). Rigorous diligence assesses cash flows, collateral and covenants with scorecards and stress tests. Documentation and closing secure enforceability. Post-close monitoring, with early-warning triggers, preserves asset quality.

Risk management & collections

Portfolio analytics, stress testing and strict limit controls manage concentration risk across Daycoval’s credit portfolio, informing concentration caps and capital planning. Early warning systems detect deterioration and automatically trigger remediation actions and re-pricing. Dedicated collections and workout teams seek to maximize recoveries through tailored restructuring and legal actions. Provisioning follows IFRS 9 expected loss models, tying reserves to forward-looking risk drivers.

Treasury, funding & ALM

Treasury optimizes Daycoval’s liquidity buffers and funding mix through wholesale, retail and securitized funding to ensure HQLA coverage; regulators target liquidity ratios such as LCR = 100%. ALM actively hedges interest rate and duration gaps to protect net interest margin and economic value. Market operations manage securities portfolios and collateral to meet intraday and repo needs. These activities safeguard margin and regulatory ratios.

FX, trade finance & investment banking

FX dealing provides spot, forward and hedging solutions to corporate clients; in 2024 Brazil’s FX market saw daily turnover above US$20bn, underpinning hedging demand. Trade finance instruments—letters of credit, documentary collections and working-capital loans—support importers and exporters amid Brazil’s goods exports near US$350bn in 2024. Investment banking advises on DCM and structured credit, with fee income increasingly complementing interest revenue.

- FX: spot, forward, hedging; market daily turnover >US$20bn (2024)

- Trade finance: LCs, collections, working-capital

- Investment banking: DCM, structured credit advisory

- Revenue mix: fees supplement interest income

Retail lending & digital distribution

Payroll-deductible and personal loans are originated through branches and partner networks, with 2024 retail portfolio growth of 8% driving increased originations. Digital onboarding streamlines approvals—average decision times fell to under 24 hours in 2024—while analytics enable targeted cross-sell into savings and investment products. Continuous UX improvements raised conversion rates year-over-year.

Origination to Treasury: Scaling Brazilian Corporate & Retail Credit with 24h Digital Onboarding

Origination: structuring/pricing SME to large-corporate loans with scorecards, collateral tests and enforceable documentation; Brazil credit-to-GDP ~54% (2024). Risk ops: portfolio analytics, IFRS 9 provisioning, collections/workouts and early-warning triggers. Treasury: funding mix, LCR ~100% targets and ALM hedging. Channels: branches/partners + digital onboarding (<24h avg, 2024) driving 8% retail growth (2024).

| Metric | 2024 |

|---|---|

| Credit-to-GDP | ~54% (IMF) |

| FX turnover (daily) | >US$20bn |

| Retail growth | 8% |

| Digital approval time | <24h |

| Exports | ~US$350bn |

| LCR target | ~100% |

What You See Is What You Get

Business Model Canvas

The document you’re previewing is the actual Daycoval Bank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this same full document—formatted and complete—as an editable file ready for presenting, editing, or sharing. No surprises, just the real deliverable.

Description

Unlock the bank Business Model Canvas: three sections on value, risk, and market capture

Unlock the full strategic blueprint behind Daycoval Bank’s Business Model Canvas—three concise sections preview how it creates value, manages risk, and captures market share. Purchase the complete Canvas to get all nine blocks with company-specific insights, SWOT-linked implications, and ready-to-use Word/Excel files. Ideal for investors, consultants, and strategists seeking actionable analysis.

Partnerships

Corporate lenders & syndication partners

Co-lending and loan syndication let Daycoval expand ticket sizes—often exceeding INR 1 billion—while sharing exposure with domestic and international banks, reducing single-counterparty concentration. These partnerships improve balance-sheet efficiency and speed deal execution through pooled underwriting and shared due diligence. Syndication also deepens market coverage across sectors and geographies, enabling larger, cross-border corporate mandates.

Funding providers & institutional investors

Institutional depositors, pension funds and wholesale markets supplied stable funding to Daycoval in 2024, comprising the bulk of its long‑term liabilities and enabling predictable liquidity. Access to debenture buyers and securitization investors in 2024 lowered blended cost of capital by diversifying funding sources and supporting cheaper wholesale issuances. This funding mix underpins competitive loan pricing and allows duration matching for ALM stability, reducing interest‑rate mismatch risk.

Payment, FX, and correspondent banks

Global FX counterparties and correspondent banks enable Daycoval’s cross-border flows by tapping into the $7.5 trillion daily FX market (BIS 2022), providing deep liquidity and settlement rails. They supply hedging instruments and intraday liquidity that narrow Daycoval’s FX spreads and improve execution quality. This connectivity also strengthens trade finance capacity, supporting import/export financing and documentary operations.

Fintechs, payroll consignees & distribution partners

Payroll-deductible partners expanded origination reach, accounting for 42% of Daycoval retail loan originations in 2024; fintech integrations enabled digital KYC and onboarding (reducing approval time ~60%) and improved credit scoring accuracy, while correspondent channels widened retail access cost‑effectively and helped lower CAC by ~25%.

- Payroll partners: 42% retail originations 2024

- Fintechs: ~60% faster onboarding

- Correspondents: ~25% CAC reduction

Data bureaus, insurers & regulators

Credit bureaus (eg Serasa/Equifax cover ~95% of Brazilian adults) supply behavioral data that sharpens Daycoval underwriting and collections, lowering default rates; insurers provide credit insurance and protection products that can cover up to 80% of exposure, mitigating loss; close alignment with the Central Bank of Brazil streamlines compliance and product approval, reducing regulatory friction.

- Data: bureau coverage ~95%

- Risk transfer: insurance up to 80% of exposure

- Regulation: Central Bank alignment reduces approval time

Partnerships enable >INR1bn deals; payrolls 42% share

Daycoval’s key partnerships—co‑lenders, syndicates and correspondent banks—enable >INR1bn ticket deals and cross‑border mandates while wholesale institutional deposits formed the bulk of long‑term funding in 2024. Payroll partners drove 42% of retail originations; fintechs cut onboarding ~60% and correspondents lowered CAC ~25%. Credit bureaus cover ~95% of adults and insurers can transfer up to 80% of exposure, improving underwriting and risk transfer.

| Partnership | 2024 Metric |

|---|---|

| Payroll partners | 42% retail originations |

| Fintech onboarding | ~60% faster |

| Correspondents | ~25% CAC reduction |

| Credit bureau coverage | ~95% adults |

| Insurance risk transfer | Up to 80% exposure |

What is included in the product

A comprehensive Business Model Canvas tailored to Daycoval Bank’s strategy, covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks and reflecting real-world operations. Ideal for presentations and investor discussions, it includes competitive advantages and linked SWOT insights.

High-level view of Daycoval Bank’s business model with editable cells, enabling teams to quickly map lending, SME focus, treasury operations and risk controls. Saves hours of structuring analysis and creates a concise, shareable one-page snapshot for boardrooms, strategy sessions, or comparative reviews.

Activities

Corporate credit origination & underwriting

Prospecting, structuring and pricing loans from SMEs to large corporates is core to Daycoval's origination, targeting risk-adjusted yields across sectors; Brazil's credit-to-GDP stood near 54% in 2024 (IMF). Rigorous diligence assesses cash flows, collateral and covenants with scorecards and stress tests. Documentation and closing secure enforceability. Post-close monitoring, with early-warning triggers, preserves asset quality.

Risk management & collections

Portfolio analytics, stress testing and strict limit controls manage concentration risk across Daycoval’s credit portfolio, informing concentration caps and capital planning. Early warning systems detect deterioration and automatically trigger remediation actions and re-pricing. Dedicated collections and workout teams seek to maximize recoveries through tailored restructuring and legal actions. Provisioning follows IFRS 9 expected loss models, tying reserves to forward-looking risk drivers.

Treasury, funding & ALM

Treasury optimizes Daycoval’s liquidity buffers and funding mix through wholesale, retail and securitized funding to ensure HQLA coverage; regulators target liquidity ratios such as LCR = 100%. ALM actively hedges interest rate and duration gaps to protect net interest margin and economic value. Market operations manage securities portfolios and collateral to meet intraday and repo needs. These activities safeguard margin and regulatory ratios.

FX, trade finance & investment banking

FX dealing provides spot, forward and hedging solutions to corporate clients; in 2024 Brazil’s FX market saw daily turnover above US$20bn, underpinning hedging demand. Trade finance instruments—letters of credit, documentary collections and working-capital loans—support importers and exporters amid Brazil’s goods exports near US$350bn in 2024. Investment banking advises on DCM and structured credit, with fee income increasingly complementing interest revenue.

- FX: spot, forward, hedging; market daily turnover >US$20bn (2024)

- Trade finance: LCs, collections, working-capital

- Investment banking: DCM, structured credit advisory

- Revenue mix: fees supplement interest income

Retail lending & digital distribution

Payroll-deductible and personal loans are originated through branches and partner networks, with 2024 retail portfolio growth of 8% driving increased originations. Digital onboarding streamlines approvals—average decision times fell to under 24 hours in 2024—while analytics enable targeted cross-sell into savings and investment products. Continuous UX improvements raised conversion rates year-over-year.

Origination to Treasury: Scaling Brazilian Corporate & Retail Credit with 24h Digital Onboarding

Origination: structuring/pricing SME to large-corporate loans with scorecards, collateral tests and enforceable documentation; Brazil credit-to-GDP ~54% (2024). Risk ops: portfolio analytics, IFRS 9 provisioning, collections/workouts and early-warning triggers. Treasury: funding mix, LCR ~100% targets and ALM hedging. Channels: branches/partners + digital onboarding (<24h avg, 2024) driving 8% retail growth (2024).

| Metric | 2024 |

|---|---|

| Credit-to-GDP | ~54% (IMF) |

| FX turnover (daily) | >US$20bn |

| Retail growth | 8% |

| Digital approval time | <24h |

| Exports | ~US$350bn |

| LCR target | ~100% |

What You See Is What You Get

Business Model Canvas

The document you’re previewing is the actual Daycoval Bank Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this same full document—formatted and complete—as an editable file ready for presenting, editing, or sharing. No surprises, just the real deliverable.