Day & Zimmermann Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

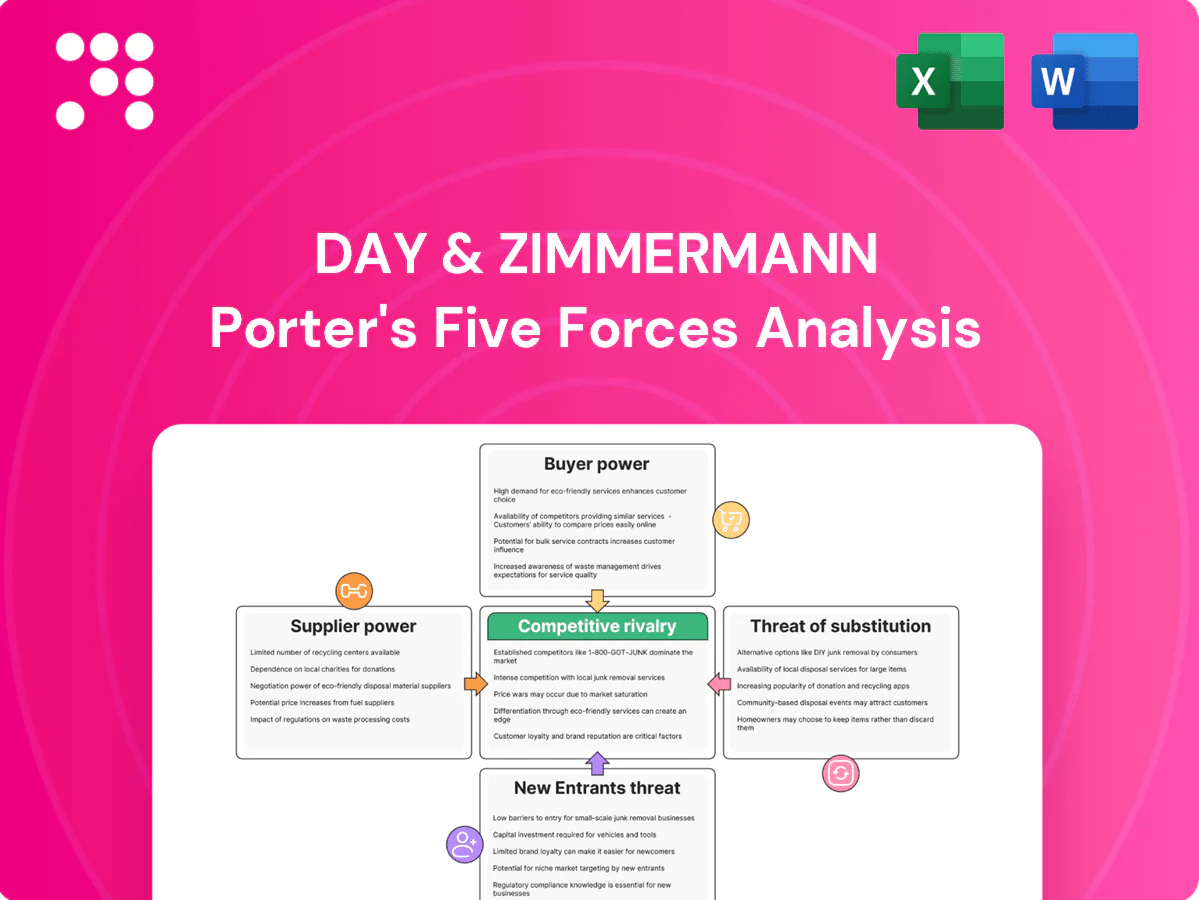

Day & Zimmermann faces complex supplier dynamics, niche buyer demands, moderate entry barriers, tangible substitute risks, and rivalry shaped by contract scale and reputation. This snapshot highlights pressure points but omits force-level ratings and strategic implications. Unlock the full Porter's Five Forces Analysis for a consultant-grade, actionable breakdown to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialized inputs & OEM dependence

Day & Zimmermann depends on specialized materials, components and OEMs for power, industrial and munitions work, exposing it to supplier leverage; as a privately held, multi-billion-dollar company in 2024 it faces elevated switching costs when few qualified OEMs exist. Single-sourced parts can allow suppliers to exert schedule leverage and raise delivery risk. Proactive dual-sourcing and long-term strategic supply agreements reduce this supplier power and mitigate program delays.

Skilled labor & union dynamics

Highly skilled, certified and often unionized craft labor is critical to Day & Zimmermann’s construction, maintenance and munitions work; tight markets give these suppliers leverage. BLS data show average hourly earnings rose about 4.1% year‑over‑year in 2024, amplifying wage pressure and work‑rule costs that squeeze margins and timelines. Aggressive workforce development and flexible staffing models can reduce supplier leverage by lowering vacancy rates and overtime exposure.

Safety, compliance, and clearance constraints

Regulatory-compliant suppliers with security clearances are scarce for defense and critical infrastructure, giving vendors leverage against Day & Zimmermann; the US DoD FY2024 budget was about $858 billion and there are over 4 million cleared personnel, constraining substitution. Qualification processes and recurring audits limit alternatives, compliance costs are often passed through to buyers, and long-term vetted partnerships lower disruption risk.

Subcontractor capacity and niche expertise

Specialty subcontractors (NDE, specialty welding, explosive handling) are frequently capacity-constrained, with 2024 industry reports noting rate premia of roughly 20–30% during peak outages and turnarounds as competition for certified crews intensifies; schedule sensitivity and high utilization give these suppliers clear bargaining power, while preferred networks and schedule smoothing reduce surge exposure and stabilize costs.

- Supply tightness: certified crew utilization spikes in turnarounds

- Price impact: ~20–30% outage rate premia (2024)

- Mitigation: preferred subcontractor networks, schedule smoothing

Software, tooling, and consumables

Proprietary engineering software, specialized testing tools and critical consumables create strong lock-in; vendors commonly charge recurring license and maintenance fees of ~15–20% of license value and calibration cycles are often annual. Switching risks loss of ISO/AS certifications and breaks data continuity, raising migration costs. Volume deals and adoption of interoperability standards can reduce supplier leverage by ~15–25%.

- 15–20% maintenance fees

- Annual calibration cycles

- ISO 10303/OPC UA mitigate lock-in

- 15–25% potential volume discounts

Cleared-supplier squeeze: DoD $858B, wages 4.1%, outage premia raise costs

Day & Zimmermann faces strong supplier leverage from specialized OEMs, certified craft labor and cleared vendors—US DoD budget $858B (FY2024) and 4.1% avg hourly wage growth (2024) amplify cost and schedule risk. Single-sourced parts, specialty subcontractors (20–30% outage premia) and 15–20% recurring software fees raise switching costs; dual‑sourcing, long‑term contracts and volume discounts (15–25%) mitigate power.

| Metric | 2024 value | Impact |

|---|---|---|

| DoD budget | $858B | drives cleared-supplier scarcity |

| Wage growth | 4.1% YoY | increases labor costs |

| Outage premia | 20–30% | schedule cost pressure |

| Software fees | 15–20% | lock-in cost |

| Volume discount | 15–25% | mitigation |

What is included in the product

Comprehensive Porter's Five Forces analysis for Day & Zimmermann assessing competitive rivalry, buyer and supplier power, barriers to entry, and substitute threats to identify strategic levers that protect margins and highlight disruption risks.

A one-sheet Day & Zimmermann Porter's Five Forces summary that maps supplier, buyer, entrant, substitute and rivalry pressures with customizable scores and an instant radar chart—clean, slide-ready and easy to drop into reports or dashboards.

Customers Bargaining Power

Concentrated government procurement

Defense and federal buyers are few, large, and process-driven; in 2024 the Department of Defense remained the single largest federal contracting entity, concentrating award power. Competitive tendering, LPTA and audit rights pushed many service margins into the low single digits and increased contract scrutiny. Contract vehicles and past performance dominated award dynamics, making compliance excellence essential to retain pricing discipline.

Utility and industrial majors

Large utility and industrial majors buy multi-year, multi-million-dollar projects and recur frequently, enabling them to benchmark vendors and bundle scopes to extract tighter commercial terms. They enforce SLAs and liquidated damages tied to uptime targets — commonly 99.9% — shifting operational and financial risk to the vendor. Vendors that demonstrate superior safety, schedule certainty and lifecycle value reduce customer price pressure and win longer-term awards.

Switching costs vs multi-sourcing

Project-specific learning curves create tangible switching costs for Day & Zimmermann, but 2024 procurement surveys indicate roughly 60% of large buyers maintain multi-supplier panels, preserving price and capacity leverage. Panel strategies typically cover 50–80% of project spend, keeping suppliers competitive on margins. Strong KPIs and digital integration (ERP and vendor portals) raise stickiness by improving performance visibility, while embedded teams and multi-year programs further lift effective switching costs.

Contract structure and risk transfer

Buyers shape margins through fixed-price, T&M, or EPC contracts with risk-transfer clauses; fixed-price deals concentrate cost risk on Day & Zimmermann while T&M preserves margin but reduces predictability. Performance incentives and penalties—commonly ±2–5 percentage points on contract margins—directly affect cash flow and returns. Milestone payments and retention practices create working capital strain, with industry payment lags often 30–60 days.

- Contract type: fixed-price vs T&M vs EPC

- Incentives/penalties: ±2–5 pp margin impact

- Working capital: milestone timing causes 30–60 day cash strain

- Mitigation: balanced terms + strict change-order governance

Demand cyclicality and budget timing

Demand concentrates around outage seasons (spring and fall), capex cycles and government fiscal calendars — the US federal fiscal year begins October 1 — allowing buyers to time awards and tighten pricing during peak procurement windows. Diversified backlog across services and sectors reduces buyer leverage by smoothing revenue timing. Flexible staffing and a cross-sector project mix stabilize utilization and preserve pricing power.

- Outage seasons: spring/fall

- Government fiscal year: US starts Oct 1

- Backlog diversification reduces volatility

- Flexible staffing smooths utilization

Concentrated federal buyers drive LPTA and crush service margins to low single digits

Defense and federal buyers are few and concentrated (DoD largest in 2024), driving LPTA, audit rights and pushing service margins into low single digits. ~60% large buyers use multi-supplier panels; incentives/penalties ±2–5 pp and payment lags 30–60 days raise buyer leverage.

| Metric | 2024 |

|---|---|

| Multi-supplier panels | ~60% |

| Margin pressure | Low single digits |

Preview the Actual Deliverable

Day & Zimmermann Porter's Five Forces Analysis

This preview shows the exact Day & Zimmermann Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No samples or placeholders—this is the final deliverable. Instant download upon payment.

A Must-Have Tool for Decision-Makers

Day & Zimmermann faces complex supplier dynamics, niche buyer demands, moderate entry barriers, tangible substitute risks, and rivalry shaped by contract scale and reputation. This snapshot highlights pressure points but omits force-level ratings and strategic implications. Unlock the full Porter's Five Forces Analysis for a consultant-grade, actionable breakdown to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialized inputs & OEM dependence

Day & Zimmermann depends on specialized materials, components and OEMs for power, industrial and munitions work, exposing it to supplier leverage; as a privately held, multi-billion-dollar company in 2024 it faces elevated switching costs when few qualified OEMs exist. Single-sourced parts can allow suppliers to exert schedule leverage and raise delivery risk. Proactive dual-sourcing and long-term strategic supply agreements reduce this supplier power and mitigate program delays.

Skilled labor & union dynamics

Highly skilled, certified and often unionized craft labor is critical to Day & Zimmermann’s construction, maintenance and munitions work; tight markets give these suppliers leverage. BLS data show average hourly earnings rose about 4.1% year‑over‑year in 2024, amplifying wage pressure and work‑rule costs that squeeze margins and timelines. Aggressive workforce development and flexible staffing models can reduce supplier leverage by lowering vacancy rates and overtime exposure.

Safety, compliance, and clearance constraints

Regulatory-compliant suppliers with security clearances are scarce for defense and critical infrastructure, giving vendors leverage against Day & Zimmermann; the US DoD FY2024 budget was about $858 billion and there are over 4 million cleared personnel, constraining substitution. Qualification processes and recurring audits limit alternatives, compliance costs are often passed through to buyers, and long-term vetted partnerships lower disruption risk.

Subcontractor capacity and niche expertise

Specialty subcontractors (NDE, specialty welding, explosive handling) are frequently capacity-constrained, with 2024 industry reports noting rate premia of roughly 20–30% during peak outages and turnarounds as competition for certified crews intensifies; schedule sensitivity and high utilization give these suppliers clear bargaining power, while preferred networks and schedule smoothing reduce surge exposure and stabilize costs.

- Supply tightness: certified crew utilization spikes in turnarounds

- Price impact: ~20–30% outage rate premia (2024)

- Mitigation: preferred subcontractor networks, schedule smoothing

Software, tooling, and consumables

Proprietary engineering software, specialized testing tools and critical consumables create strong lock-in; vendors commonly charge recurring license and maintenance fees of ~15–20% of license value and calibration cycles are often annual. Switching risks loss of ISO/AS certifications and breaks data continuity, raising migration costs. Volume deals and adoption of interoperability standards can reduce supplier leverage by ~15–25%.

- 15–20% maintenance fees

- Annual calibration cycles

- ISO 10303/OPC UA mitigate lock-in

- 15–25% potential volume discounts

Cleared-supplier squeeze: DoD $858B, wages 4.1%, outage premia raise costs

Day & Zimmermann faces strong supplier leverage from specialized OEMs, certified craft labor and cleared vendors—US DoD budget $858B (FY2024) and 4.1% avg hourly wage growth (2024) amplify cost and schedule risk. Single-sourced parts, specialty subcontractors (20–30% outage premia) and 15–20% recurring software fees raise switching costs; dual‑sourcing, long‑term contracts and volume discounts (15–25%) mitigate power.

| Metric | 2024 value | Impact |

|---|---|---|

| DoD budget | $858B | drives cleared-supplier scarcity |

| Wage growth | 4.1% YoY | increases labor costs |

| Outage premia | 20–30% | schedule cost pressure |

| Software fees | 15–20% | lock-in cost |

| Volume discount | 15–25% | mitigation |

What is included in the product

Comprehensive Porter's Five Forces analysis for Day & Zimmermann assessing competitive rivalry, buyer and supplier power, barriers to entry, and substitute threats to identify strategic levers that protect margins and highlight disruption risks.

A one-sheet Day & Zimmermann Porter's Five Forces summary that maps supplier, buyer, entrant, substitute and rivalry pressures with customizable scores and an instant radar chart—clean, slide-ready and easy to drop into reports or dashboards.

Customers Bargaining Power

Concentrated government procurement

Defense and federal buyers are few, large, and process-driven; in 2024 the Department of Defense remained the single largest federal contracting entity, concentrating award power. Competitive tendering, LPTA and audit rights pushed many service margins into the low single digits and increased contract scrutiny. Contract vehicles and past performance dominated award dynamics, making compliance excellence essential to retain pricing discipline.

Utility and industrial majors

Large utility and industrial majors buy multi-year, multi-million-dollar projects and recur frequently, enabling them to benchmark vendors and bundle scopes to extract tighter commercial terms. They enforce SLAs and liquidated damages tied to uptime targets — commonly 99.9% — shifting operational and financial risk to the vendor. Vendors that demonstrate superior safety, schedule certainty and lifecycle value reduce customer price pressure and win longer-term awards.

Switching costs vs multi-sourcing

Project-specific learning curves create tangible switching costs for Day & Zimmermann, but 2024 procurement surveys indicate roughly 60% of large buyers maintain multi-supplier panels, preserving price and capacity leverage. Panel strategies typically cover 50–80% of project spend, keeping suppliers competitive on margins. Strong KPIs and digital integration (ERP and vendor portals) raise stickiness by improving performance visibility, while embedded teams and multi-year programs further lift effective switching costs.

Contract structure and risk transfer

Buyers shape margins through fixed-price, T&M, or EPC contracts with risk-transfer clauses; fixed-price deals concentrate cost risk on Day & Zimmermann while T&M preserves margin but reduces predictability. Performance incentives and penalties—commonly ±2–5 percentage points on contract margins—directly affect cash flow and returns. Milestone payments and retention practices create working capital strain, with industry payment lags often 30–60 days.

- Contract type: fixed-price vs T&M vs EPC

- Incentives/penalties: ±2–5 pp margin impact

- Working capital: milestone timing causes 30–60 day cash strain

- Mitigation: balanced terms + strict change-order governance

Demand cyclicality and budget timing

Demand concentrates around outage seasons (spring and fall), capex cycles and government fiscal calendars — the US federal fiscal year begins October 1 — allowing buyers to time awards and tighten pricing during peak procurement windows. Diversified backlog across services and sectors reduces buyer leverage by smoothing revenue timing. Flexible staffing and a cross-sector project mix stabilize utilization and preserve pricing power.

- Outage seasons: spring/fall

- Government fiscal year: US starts Oct 1

- Backlog diversification reduces volatility

- Flexible staffing smooths utilization

Concentrated federal buyers drive LPTA and crush service margins to low single digits

Defense and federal buyers are few and concentrated (DoD largest in 2024), driving LPTA, audit rights and pushing service margins into low single digits. ~60% large buyers use multi-supplier panels; incentives/penalties ±2–5 pp and payment lags 30–60 days raise buyer leverage.

| Metric | 2024 |

|---|---|

| Multi-supplier panels | ~60% |

| Margin pressure | Low single digits |

Preview the Actual Deliverable

Day & Zimmermann Porter's Five Forces Analysis

This preview shows the exact Day & Zimmermann Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No samples or placeholders—this is the final deliverable. Instant download upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Day & Zimmermann faces complex supplier dynamics, niche buyer demands, moderate entry barriers, tangible substitute risks, and rivalry shaped by contract scale and reputation. This snapshot highlights pressure points but omits force-level ratings and strategic implications. Unlock the full Porter's Five Forces Analysis for a consultant-grade, actionable breakdown to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialized inputs & OEM dependence

Day & Zimmermann depends on specialized materials, components and OEMs for power, industrial and munitions work, exposing it to supplier leverage; as a privately held, multi-billion-dollar company in 2024 it faces elevated switching costs when few qualified OEMs exist. Single-sourced parts can allow suppliers to exert schedule leverage and raise delivery risk. Proactive dual-sourcing and long-term strategic supply agreements reduce this supplier power and mitigate program delays.

Skilled labor & union dynamics

Highly skilled, certified and often unionized craft labor is critical to Day & Zimmermann’s construction, maintenance and munitions work; tight markets give these suppliers leverage. BLS data show average hourly earnings rose about 4.1% year‑over‑year in 2024, amplifying wage pressure and work‑rule costs that squeeze margins and timelines. Aggressive workforce development and flexible staffing models can reduce supplier leverage by lowering vacancy rates and overtime exposure.

Safety, compliance, and clearance constraints

Regulatory-compliant suppliers with security clearances are scarce for defense and critical infrastructure, giving vendors leverage against Day & Zimmermann; the US DoD FY2024 budget was about $858 billion and there are over 4 million cleared personnel, constraining substitution. Qualification processes and recurring audits limit alternatives, compliance costs are often passed through to buyers, and long-term vetted partnerships lower disruption risk.

Subcontractor capacity and niche expertise

Specialty subcontractors (NDE, specialty welding, explosive handling) are frequently capacity-constrained, with 2024 industry reports noting rate premia of roughly 20–30% during peak outages and turnarounds as competition for certified crews intensifies; schedule sensitivity and high utilization give these suppliers clear bargaining power, while preferred networks and schedule smoothing reduce surge exposure and stabilize costs.

- Supply tightness: certified crew utilization spikes in turnarounds

- Price impact: ~20–30% outage rate premia (2024)

- Mitigation: preferred subcontractor networks, schedule smoothing

Software, tooling, and consumables

Proprietary engineering software, specialized testing tools and critical consumables create strong lock-in; vendors commonly charge recurring license and maintenance fees of ~15–20% of license value and calibration cycles are often annual. Switching risks loss of ISO/AS certifications and breaks data continuity, raising migration costs. Volume deals and adoption of interoperability standards can reduce supplier leverage by ~15–25%.

- 15–20% maintenance fees

- Annual calibration cycles

- ISO 10303/OPC UA mitigate lock-in

- 15–25% potential volume discounts

Cleared-supplier squeeze: DoD $858B, wages 4.1%, outage premia raise costs

Day & Zimmermann faces strong supplier leverage from specialized OEMs, certified craft labor and cleared vendors—US DoD budget $858B (FY2024) and 4.1% avg hourly wage growth (2024) amplify cost and schedule risk. Single-sourced parts, specialty subcontractors (20–30% outage premia) and 15–20% recurring software fees raise switching costs; dual‑sourcing, long‑term contracts and volume discounts (15–25%) mitigate power.

| Metric | 2024 value | Impact |

|---|---|---|

| DoD budget | $858B | drives cleared-supplier scarcity |

| Wage growth | 4.1% YoY | increases labor costs |

| Outage premia | 20–30% | schedule cost pressure |

| Software fees | 15–20% | lock-in cost |

| Volume discount | 15–25% | mitigation |

What is included in the product

Comprehensive Porter's Five Forces analysis for Day & Zimmermann assessing competitive rivalry, buyer and supplier power, barriers to entry, and substitute threats to identify strategic levers that protect margins and highlight disruption risks.

A one-sheet Day & Zimmermann Porter's Five Forces summary that maps supplier, buyer, entrant, substitute and rivalry pressures with customizable scores and an instant radar chart—clean, slide-ready and easy to drop into reports or dashboards.

Customers Bargaining Power

Concentrated government procurement

Defense and federal buyers are few, large, and process-driven; in 2024 the Department of Defense remained the single largest federal contracting entity, concentrating award power. Competitive tendering, LPTA and audit rights pushed many service margins into the low single digits and increased contract scrutiny. Contract vehicles and past performance dominated award dynamics, making compliance excellence essential to retain pricing discipline.

Utility and industrial majors

Large utility and industrial majors buy multi-year, multi-million-dollar projects and recur frequently, enabling them to benchmark vendors and bundle scopes to extract tighter commercial terms. They enforce SLAs and liquidated damages tied to uptime targets — commonly 99.9% — shifting operational and financial risk to the vendor. Vendors that demonstrate superior safety, schedule certainty and lifecycle value reduce customer price pressure and win longer-term awards.

Switching costs vs multi-sourcing

Project-specific learning curves create tangible switching costs for Day & Zimmermann, but 2024 procurement surveys indicate roughly 60% of large buyers maintain multi-supplier panels, preserving price and capacity leverage. Panel strategies typically cover 50–80% of project spend, keeping suppliers competitive on margins. Strong KPIs and digital integration (ERP and vendor portals) raise stickiness by improving performance visibility, while embedded teams and multi-year programs further lift effective switching costs.

Contract structure and risk transfer

Buyers shape margins through fixed-price, T&M, or EPC contracts with risk-transfer clauses; fixed-price deals concentrate cost risk on Day & Zimmermann while T&M preserves margin but reduces predictability. Performance incentives and penalties—commonly ±2–5 percentage points on contract margins—directly affect cash flow and returns. Milestone payments and retention practices create working capital strain, with industry payment lags often 30–60 days.

- Contract type: fixed-price vs T&M vs EPC

- Incentives/penalties: ±2–5 pp margin impact

- Working capital: milestone timing causes 30–60 day cash strain

- Mitigation: balanced terms + strict change-order governance

Demand cyclicality and budget timing

Demand concentrates around outage seasons (spring and fall), capex cycles and government fiscal calendars — the US federal fiscal year begins October 1 — allowing buyers to time awards and tighten pricing during peak procurement windows. Diversified backlog across services and sectors reduces buyer leverage by smoothing revenue timing. Flexible staffing and a cross-sector project mix stabilize utilization and preserve pricing power.

- Outage seasons: spring/fall

- Government fiscal year: US starts Oct 1

- Backlog diversification reduces volatility

- Flexible staffing smooths utilization

Concentrated federal buyers drive LPTA and crush service margins to low single digits

Defense and federal buyers are few and concentrated (DoD largest in 2024), driving LPTA, audit rights and pushing service margins into low single digits. ~60% large buyers use multi-supplier panels; incentives/penalties ±2–5 pp and payment lags 30–60 days raise buyer leverage.

| Metric | 2024 |

|---|---|

| Multi-supplier panels | ~60% |

| Margin pressure | Low single digits |

Preview the Actual Deliverable

Day & Zimmermann Porter's Five Forces Analysis

This preview shows the exact Day & Zimmermann Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No samples or placeholders—this is the final deliverable. Instant download upon payment.