DBS PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our DBS PESTLE Analysis—three to five expert-level insights into political, economic, social, technological, legal and environmental forces shaping the bank’s future. Ideal for investors and strategists, this ready-to-use report helps you forecast risks and seize opportunities. Purchase the full analysis for the complete, downloadable breakdown and actionable recommendations.

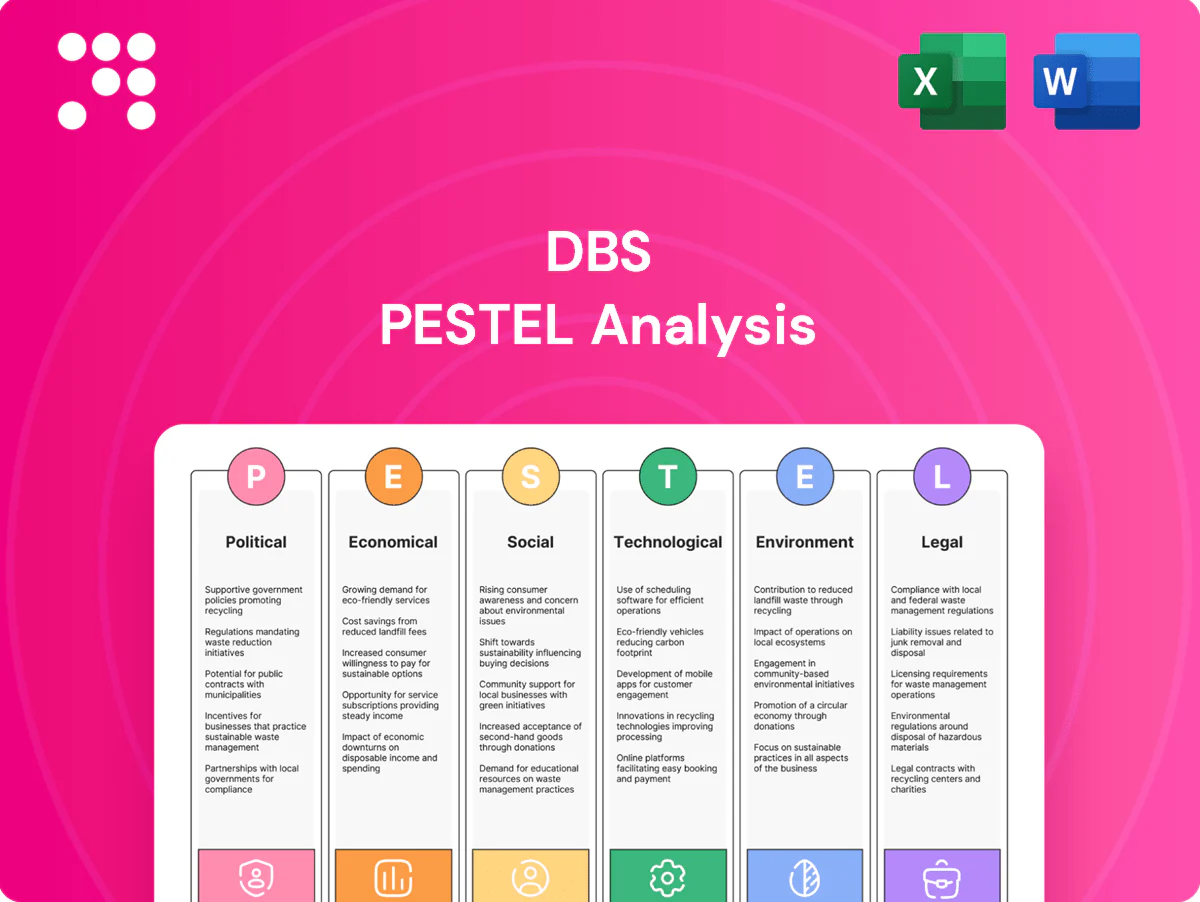

Political factors

Singapore policy stability

DBS benefits from Singapore’s predictable policymaking, pro-business stance and strong public institutions. Consistent monetary and fiscal policies by MAS and the Ministry of Finance support long-term planning and risk management. Government backing of the financial-hub strategy sustains capital flows and talent attraction. Singapore ranked 2nd in the Global Financial Centres Index (2024) and holds AAA ratings from S&P and Fitch, lowering political risk premiums.

Regional geopolitics exposure

DBS operates across 18 Asian markets, including ASEAN, Greater China and India, exposing it to US–China tensions and regional flashpoints. Trade restrictions, technology controls or sanctions can disrupt client supply chains and cross-border capital flows. Political instability or elections in these markets may reduce credit demand and stress asset quality. Geographic diversification mitigates single-market shocks but raises coordination complexity.

Cross-border regulatory coordination

DBS operates across 18 markets, requiring alignment with differing central bank priorities and prudential rules that raise compliance burdens and capital-allocation frictions. Regulatory fragmentation increases compliance costs and operational complexity. Passporting and mutual recognition remain uneven in Asia, with ASEAN’s 10 members yet to achieve full harmonization. Strong regulatory relations and local governance sustain licenses and growth.

Government digitalization agendas

Asian governments push digital-economy initiatives, real-time payments and financial inclusion; ASEAN targets a US$1 trillion digital economy by 2030, creating scale for banks. DBS can tap public–private e-payment, digital ID and SME digitization programs to accelerate customer acquisition and data interoperability, but success depends on aligning with national standards and infrastructure timelines.

- e-payments: public–private rails

- digital ID: KYC scale-up

- SME digitization: onboarding

- policy incentives: faster adoption

- alignment: national standards & timelines

Sanctions and foreign policy risks

Singapore bank: AAA, GFCI 2, 18 markets; US-China & OFAC risks

DBS benefits from Singapore’s pro-business policy, AAA ratings (S&P/Fitch) and GFCI rank 2 (2024), supporting low political risk. Operating in 18 Asian markets exposes it to US–China tensions, sanctions and election risks that can hit credit demand. Regulatory fragmentation raises compliance costs; OFAC SDN list >14,000 (2024) increases KYC/AML burdens. ASEAN digital-economy push (US$1tn by 2030) creates growth opportunities.

| Metric | Value |

|---|---|

| Markets | 18 |

| GFCI (2024) | 2 |

| Ratings | AAA (S&P,Fitch) |

| OFAC SDN (2024) | >14,000 |

| ASEAN digital target | US$1tn by 2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact DBS, with data-backed trends and region-specific regulatory context; designed for executives, investors and strategists to identify risks, opportunities and forward-looking scenarios ready for reports or decks.

A concise, visually segmented DBS PESTLE summary that can be dropped into presentations, shared across teams, and annotated for local context—streamlining external risk discussions and speeding strategic planning.

Economic factors

Interest rate cycle sensitivity

DBS net interest margin, around 1.8% in 1H2024, and fee income track global and Asian rate paths, so rapid rate cuts would compress margins sharply while higher-for-longer rates raise non-performing loan risk. Balance sheet hedging and optimizing a CASA-weighted deposit mix reduce repricing shock. Agile product pricing—tiered loan spreads, dynamic deposit pricing—stabilizes returns across cycles.

Regional growth and trade dynamics

ASEAN growth of about 4.5% in 2024 and India’s ~7% FY24 expansion underpin loan demand, wealth flows and transaction banking across DBS’ franchise. China’s slower trajectory—around 4.5% GDP in 2024—reshapes regional exports, commodity cycles and investor sentiment. Trade realignment and supply‑chain shifts drive new trade and project financing needs, while sector selection and country limits mitigate cyclical concentration risks.

FX volatility and capital flows

Currency swings directly hit DBS treasury income, trading P&L and borrower repayment capacity, with the US dollar index having peaked at 114.78 in Sep 2022 highlighting severe conversion shock. Strong USD cycles tighten regional liquidity and elevate dollar funding costs, compressing NIMs. Client hedging demand deepens wallet share but raises market risk management needs. Stable funding and diversified currency mix reduce vulnerability.

Credit cycle and asset quality

SME and consumer credit at DBS remain sensitive to employment (Singapore unemployment ~2.1% in 2024), inflation (CPI ~3.6% in 2024) and property-price moves (private home prices +6.7% in 2024); prudent underwriting and dynamic provisioning—DBS reported NPLs around 1.1% in 2024—help absorb shocks. Sectoral stress in real estate and export-oriented segments can lift NPLs; early-warning analytics and restructuring preserve recoveries.

- Employment risk: unemployment ~2.1% (2024)

- Inflation: CPI ~3.6% (2024)

- Property: private home prices +6.7% (2024)

- DBS NPLs ~1.1% (2024); dynamic provisioning and analytics mitigate losses

Property markets and wealth effects

Real estate trends drive mortgage growth, collateral values and wealth-management flows; URA data showed private residential prices eased about 2% in 2024, which tempered mortgage originations and fee income as cooling measures reduced lending appetite.

- Mortgage growth: weaker amid cooling measures and price -2% (URA 2024)

- Wealth effects: stronger markets lift AUM and bancassurance fees

- Diversification: DBS presence across SEA, HK and China smooths property cycles

Singapore bank: AAA, GFCI 2, 18 markets; US-China & OFAC risks

DBS NIM ~1.8% (1H2024) and fee income follow rate paths so rapid cuts compress margins while higher rates raise credit risk. ASEAN GDP ~4.5% (2024), India ~7% (FY24) support loan and trade; China ~4.5% (2024) slows export demand. SGD CPI ~3.6% and unemployment ~2.1% (2024) shape consumer credit and mortgage trends.

| Metric | Value (2024) |

|---|---|

| NIM | 1.8% (1H) |

| ASEAN GDP | 4.5% |

| India GDP | ~7% |

| China GDP | 4.5% |

| SGD CPI | 3.6% |

| Unemployment | 2.1% |

| Private home prices (URA) | -2% |

| NPLs (DBS) | 1.1% |

What You See Is What You Get

DBS PESTLE Analysis

The preview shown here is the exact DBS PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are the final file with no placeholders or teasers. After checkout you’ll be able to download this same professionally structured document instantly.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our DBS PESTLE Analysis—three to five expert-level insights into political, economic, social, technological, legal and environmental forces shaping the bank’s future. Ideal for investors and strategists, this ready-to-use report helps you forecast risks and seize opportunities. Purchase the full analysis for the complete, downloadable breakdown and actionable recommendations.

Political factors

Singapore policy stability

DBS benefits from Singapore’s predictable policymaking, pro-business stance and strong public institutions. Consistent monetary and fiscal policies by MAS and the Ministry of Finance support long-term planning and risk management. Government backing of the financial-hub strategy sustains capital flows and talent attraction. Singapore ranked 2nd in the Global Financial Centres Index (2024) and holds AAA ratings from S&P and Fitch, lowering political risk premiums.

Regional geopolitics exposure

DBS operates across 18 Asian markets, including ASEAN, Greater China and India, exposing it to US–China tensions and regional flashpoints. Trade restrictions, technology controls or sanctions can disrupt client supply chains and cross-border capital flows. Political instability or elections in these markets may reduce credit demand and stress asset quality. Geographic diversification mitigates single-market shocks but raises coordination complexity.

Cross-border regulatory coordination

DBS operates across 18 markets, requiring alignment with differing central bank priorities and prudential rules that raise compliance burdens and capital-allocation frictions. Regulatory fragmentation increases compliance costs and operational complexity. Passporting and mutual recognition remain uneven in Asia, with ASEAN’s 10 members yet to achieve full harmonization. Strong regulatory relations and local governance sustain licenses and growth.

Government digitalization agendas

Asian governments push digital-economy initiatives, real-time payments and financial inclusion; ASEAN targets a US$1 trillion digital economy by 2030, creating scale for banks. DBS can tap public–private e-payment, digital ID and SME digitization programs to accelerate customer acquisition and data interoperability, but success depends on aligning with national standards and infrastructure timelines.

- e-payments: public–private rails

- digital ID: KYC scale-up

- SME digitization: onboarding

- policy incentives: faster adoption

- alignment: national standards & timelines

Sanctions and foreign policy risks

Singapore bank: AAA, GFCI 2, 18 markets; US-China & OFAC risks

DBS benefits from Singapore’s pro-business policy, AAA ratings (S&P/Fitch) and GFCI rank 2 (2024), supporting low political risk. Operating in 18 Asian markets exposes it to US–China tensions, sanctions and election risks that can hit credit demand. Regulatory fragmentation raises compliance costs; OFAC SDN list >14,000 (2024) increases KYC/AML burdens. ASEAN digital-economy push (US$1tn by 2030) creates growth opportunities.

| Metric | Value |

|---|---|

| Markets | 18 |

| GFCI (2024) | 2 |

| Ratings | AAA (S&P,Fitch) |

| OFAC SDN (2024) | >14,000 |

| ASEAN digital target | US$1tn by 2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact DBS, with data-backed trends and region-specific regulatory context; designed for executives, investors and strategists to identify risks, opportunities and forward-looking scenarios ready for reports or decks.

A concise, visually segmented DBS PESTLE summary that can be dropped into presentations, shared across teams, and annotated for local context—streamlining external risk discussions and speeding strategic planning.

Economic factors

Interest rate cycle sensitivity

DBS net interest margin, around 1.8% in 1H2024, and fee income track global and Asian rate paths, so rapid rate cuts would compress margins sharply while higher-for-longer rates raise non-performing loan risk. Balance sheet hedging and optimizing a CASA-weighted deposit mix reduce repricing shock. Agile product pricing—tiered loan spreads, dynamic deposit pricing—stabilizes returns across cycles.

Regional growth and trade dynamics

ASEAN growth of about 4.5% in 2024 and India’s ~7% FY24 expansion underpin loan demand, wealth flows and transaction banking across DBS’ franchise. China’s slower trajectory—around 4.5% GDP in 2024—reshapes regional exports, commodity cycles and investor sentiment. Trade realignment and supply‑chain shifts drive new trade and project financing needs, while sector selection and country limits mitigate cyclical concentration risks.

FX volatility and capital flows

Currency swings directly hit DBS treasury income, trading P&L and borrower repayment capacity, with the US dollar index having peaked at 114.78 in Sep 2022 highlighting severe conversion shock. Strong USD cycles tighten regional liquidity and elevate dollar funding costs, compressing NIMs. Client hedging demand deepens wallet share but raises market risk management needs. Stable funding and diversified currency mix reduce vulnerability.

Credit cycle and asset quality

SME and consumer credit at DBS remain sensitive to employment (Singapore unemployment ~2.1% in 2024), inflation (CPI ~3.6% in 2024) and property-price moves (private home prices +6.7% in 2024); prudent underwriting and dynamic provisioning—DBS reported NPLs around 1.1% in 2024—help absorb shocks. Sectoral stress in real estate and export-oriented segments can lift NPLs; early-warning analytics and restructuring preserve recoveries.

- Employment risk: unemployment ~2.1% (2024)

- Inflation: CPI ~3.6% (2024)

- Property: private home prices +6.7% (2024)

- DBS NPLs ~1.1% (2024); dynamic provisioning and analytics mitigate losses

Property markets and wealth effects

Real estate trends drive mortgage growth, collateral values and wealth-management flows; URA data showed private residential prices eased about 2% in 2024, which tempered mortgage originations and fee income as cooling measures reduced lending appetite.

- Mortgage growth: weaker amid cooling measures and price -2% (URA 2024)

- Wealth effects: stronger markets lift AUM and bancassurance fees

- Diversification: DBS presence across SEA, HK and China smooths property cycles

Singapore bank: AAA, GFCI 2, 18 markets; US-China & OFAC risks

DBS NIM ~1.8% (1H2024) and fee income follow rate paths so rapid cuts compress margins while higher rates raise credit risk. ASEAN GDP ~4.5% (2024), India ~7% (FY24) support loan and trade; China ~4.5% (2024) slows export demand. SGD CPI ~3.6% and unemployment ~2.1% (2024) shape consumer credit and mortgage trends.

| Metric | Value (2024) |

|---|---|

| NIM | 1.8% (1H) |

| ASEAN GDP | 4.5% |

| India GDP | ~7% |

| China GDP | 4.5% |

| SGD CPI | 3.6% |

| Unemployment | 2.1% |

| Private home prices (URA) | -2% |

| NPLs (DBS) | 1.1% |

What You See Is What You Get

DBS PESTLE Analysis

The preview shown here is the exact DBS PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are the final file with no placeholders or teasers. After checkout you’ll be able to download this same professionally structured document instantly.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our DBS PESTLE Analysis—three to five expert-level insights into political, economic, social, technological, legal and environmental forces shaping the bank’s future. Ideal for investors and strategists, this ready-to-use report helps you forecast risks and seize opportunities. Purchase the full analysis for the complete, downloadable breakdown and actionable recommendations.

Political factors

Singapore policy stability

DBS benefits from Singapore’s predictable policymaking, pro-business stance and strong public institutions. Consistent monetary and fiscal policies by MAS and the Ministry of Finance support long-term planning and risk management. Government backing of the financial-hub strategy sustains capital flows and talent attraction. Singapore ranked 2nd in the Global Financial Centres Index (2024) and holds AAA ratings from S&P and Fitch, lowering political risk premiums.

Regional geopolitics exposure

DBS operates across 18 Asian markets, including ASEAN, Greater China and India, exposing it to US–China tensions and regional flashpoints. Trade restrictions, technology controls or sanctions can disrupt client supply chains and cross-border capital flows. Political instability or elections in these markets may reduce credit demand and stress asset quality. Geographic diversification mitigates single-market shocks but raises coordination complexity.

Cross-border regulatory coordination

DBS operates across 18 markets, requiring alignment with differing central bank priorities and prudential rules that raise compliance burdens and capital-allocation frictions. Regulatory fragmentation increases compliance costs and operational complexity. Passporting and mutual recognition remain uneven in Asia, with ASEAN’s 10 members yet to achieve full harmonization. Strong regulatory relations and local governance sustain licenses and growth.

Government digitalization agendas

Asian governments push digital-economy initiatives, real-time payments and financial inclusion; ASEAN targets a US$1 trillion digital economy by 2030, creating scale for banks. DBS can tap public–private e-payment, digital ID and SME digitization programs to accelerate customer acquisition and data interoperability, but success depends on aligning with national standards and infrastructure timelines.

- e-payments: public–private rails

- digital ID: KYC scale-up

- SME digitization: onboarding

- policy incentives: faster adoption

- alignment: national standards & timelines

Sanctions and foreign policy risks

Singapore bank: AAA, GFCI 2, 18 markets; US-China & OFAC risks

DBS benefits from Singapore’s pro-business policy, AAA ratings (S&P/Fitch) and GFCI rank 2 (2024), supporting low political risk. Operating in 18 Asian markets exposes it to US–China tensions, sanctions and election risks that can hit credit demand. Regulatory fragmentation raises compliance costs; OFAC SDN list >14,000 (2024) increases KYC/AML burdens. ASEAN digital-economy push (US$1tn by 2030) creates growth opportunities.

| Metric | Value |

|---|---|

| Markets | 18 |

| GFCI (2024) | 2 |

| Ratings | AAA (S&P,Fitch) |

| OFAC SDN (2024) | >14,000 |

| ASEAN digital target | US$1tn by 2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact DBS, with data-backed trends and region-specific regulatory context; designed for executives, investors and strategists to identify risks, opportunities and forward-looking scenarios ready for reports or decks.

A concise, visually segmented DBS PESTLE summary that can be dropped into presentations, shared across teams, and annotated for local context—streamlining external risk discussions and speeding strategic planning.

Economic factors

Interest rate cycle sensitivity

DBS net interest margin, around 1.8% in 1H2024, and fee income track global and Asian rate paths, so rapid rate cuts would compress margins sharply while higher-for-longer rates raise non-performing loan risk. Balance sheet hedging and optimizing a CASA-weighted deposit mix reduce repricing shock. Agile product pricing—tiered loan spreads, dynamic deposit pricing—stabilizes returns across cycles.

Regional growth and trade dynamics

ASEAN growth of about 4.5% in 2024 and India’s ~7% FY24 expansion underpin loan demand, wealth flows and transaction banking across DBS’ franchise. China’s slower trajectory—around 4.5% GDP in 2024—reshapes regional exports, commodity cycles and investor sentiment. Trade realignment and supply‑chain shifts drive new trade and project financing needs, while sector selection and country limits mitigate cyclical concentration risks.

FX volatility and capital flows

Currency swings directly hit DBS treasury income, trading P&L and borrower repayment capacity, with the US dollar index having peaked at 114.78 in Sep 2022 highlighting severe conversion shock. Strong USD cycles tighten regional liquidity and elevate dollar funding costs, compressing NIMs. Client hedging demand deepens wallet share but raises market risk management needs. Stable funding and diversified currency mix reduce vulnerability.

Credit cycle and asset quality

SME and consumer credit at DBS remain sensitive to employment (Singapore unemployment ~2.1% in 2024), inflation (CPI ~3.6% in 2024) and property-price moves (private home prices +6.7% in 2024); prudent underwriting and dynamic provisioning—DBS reported NPLs around 1.1% in 2024—help absorb shocks. Sectoral stress in real estate and export-oriented segments can lift NPLs; early-warning analytics and restructuring preserve recoveries.

- Employment risk: unemployment ~2.1% (2024)

- Inflation: CPI ~3.6% (2024)

- Property: private home prices +6.7% (2024)

- DBS NPLs ~1.1% (2024); dynamic provisioning and analytics mitigate losses

Property markets and wealth effects

Real estate trends drive mortgage growth, collateral values and wealth-management flows; URA data showed private residential prices eased about 2% in 2024, which tempered mortgage originations and fee income as cooling measures reduced lending appetite.

- Mortgage growth: weaker amid cooling measures and price -2% (URA 2024)

- Wealth effects: stronger markets lift AUM and bancassurance fees

- Diversification: DBS presence across SEA, HK and China smooths property cycles

Singapore bank: AAA, GFCI 2, 18 markets; US-China & OFAC risks

DBS NIM ~1.8% (1H2024) and fee income follow rate paths so rapid cuts compress margins while higher rates raise credit risk. ASEAN GDP ~4.5% (2024), India ~7% (FY24) support loan and trade; China ~4.5% (2024) slows export demand. SGD CPI ~3.6% and unemployment ~2.1% (2024) shape consumer credit and mortgage trends.

| Metric | Value (2024) |

|---|---|

| NIM | 1.8% (1H) |

| ASEAN GDP | 4.5% |

| India GDP | ~7% |

| China GDP | 4.5% |

| SGD CPI | 3.6% |

| Unemployment | 2.1% |

| Private home prices (URA) | -2% |

| NPLs (DBS) | 1.1% |

What You See Is What You Get

DBS PESTLE Analysis

The preview shown here is the exact DBS PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are the final file with no placeholders or teasers. After checkout you’ll be able to download this same professionally structured document instantly.