DCB Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

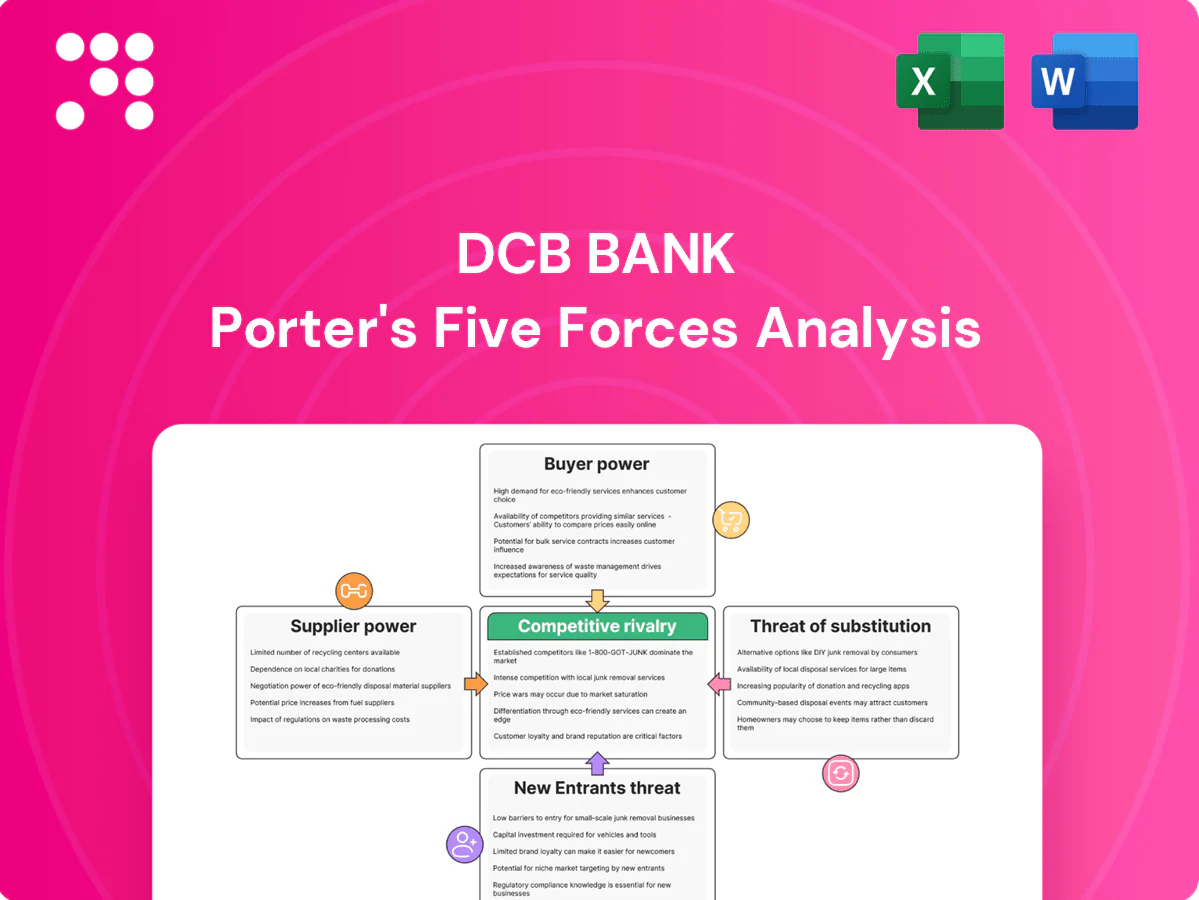

DCB Bank’s Porter's Five Forces snapshot highlights competitive intensity from larger private banks, moderate buyer power from retail and SME segments, restrained supplier influence, and evolving substitute and entry threats. This brief overview teases critical risks and opportunities. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and strategic implications tailored to DCB Bank.

Suppliers Bargaining Power

Funding mix dependence

DCB Bank depends heavily on retail deposits and CASA (CASA ~46.5% in FY2024) with wholesale borrowings roughly 12% of funding; when system liquidity tightens depositors push rates up and wholesale spreads widen, raising funding costs. Limited pricing power against rate‑sensitive depositors increases supplier leverage. Increasing sticky CASA and granular term deposits can reduce this vulnerability.

Technology and fintech vendors

Core banking, cloud, cybersecurity and payments rails are concentrated among a few large vendors, increasing supplier leverage for DCB Bank. Core replacements are costly and risky, typically requiring 18–36 months and often $10–100m in investment, strengthening vendor bargaining power. Integration with UPI, BBPS and third-party APIs creates coordination dependence on these providers. Multi-vendor strategies and open standards mitigate lock-in risk.

Skilled talent and branch partners

Experienced risk officers, SME relationship managers and data scientists are scarce and mobile, driving wage inflation and retention bonuses that raise input costs—DCB Bank, which operated about 500 branches as of March 2024, faces higher staff cost pressure in growth markets. Business correspondents and rural channel partners can negotiate fees tied to reach and performance, increasing supplier leverage. Building internal talent pipelines and productivity-linked payouts can rebalance bargaining power by lowering reliance on external hires.

Credit bureaus and data providers

Lending at DCB Bank depends on bureau data, eKYC, device intelligence and analytics; three major credit bureaus control over 90% of consumer credit data in India (2024), creating take-it-or-leave-it pricing and SLA-driven 24–72 hr impacts on SME and retail underwriting. Negotiating volume-based contracts (10–30% cost cuts) and building in-house scorecards (reducing bureau pulls 20–40%) curb dependence.

- Concentration: three bureaus >90% (2024)

- SLA impact: 24–72 hr

- Volume discounts: 10–30%

- In-house scorecards reduce pulls 20–40%

Regulatory and payment infrastructure

RBI mandates (minimum CRAR 9% and LCR 100%) and NPCI rails function as quasi-suppliers for DCB Bank by controlling licenses, access and interoperability; NPCI processed over 100 billion UPI transactions in 2024, making access critical. Sudden capital, liquidity or interoperability mandates can spike operating costs, while compliance tech and reporting burdens create indirect supplier power; active participation in industry bodies helps shape timelines and reduce impact.

- RBI: CRAR ≥9%, LCR 100%

- NPCI: >100bn UPI txns (2024)

- Compliance tech adds fixed/recurring costs

- Industry bodies can influence regulation timing

Bank faces supplier leverage: CASA 46.5%, wholesale ~12%, bureaus >90%

DCB Bank faces supplier leverage from funding (CASA ~46.5% in FY2024; wholesale borrowings ~12%), concentrated core/vendor stacks, credit bureaus (>90% market share, 2024) and regulatory/NPCI control (NPCI >100bn UPI txns, 2024; RBI CRAR ≥9%, LCR 100%).

| Metric | 2024 |

|---|---|

| CASA | 46.5% |

| Wholesale funding | ~12% |

| Credit bureaus | >90% |

| UPI txns (NPCI) | >100bn |

What is included in the product

Porter's Five Forces analysis for DCB Bank uncovers competitive pressures, customer and supplier bargaining power, threats from new entrants and substitutes, and intensity of rivalry—highlighting fintech disruption, regulatory barriers, and strategic levers that shape its pricing, margins, and market positioning.

Concise Porter's Five Forces for DCB Bank—one-sheet clarity to spot competitive pressures fast, with customizable scores and a ready-to-use radar chart for instant boardroom-ready insights.

Customers Bargaining Power

Highly price-sensitive depositors

Rate-shopping via aggregators and app comparisons has raised depositor price sensitivity, with NPCI reporting UPI volumes exceeding 100 billion transactions in FY2023-24, easing account mobility. Small shifts of 10–25 basis points in TD or savings rates often trigger visible flows to competitors. CASA balances are somewhat stickier but remain mobile due to instant payments and UPI convenience. Loyalty rewards and bundled services can blunt pure price-driven churn.

SME clients negotiate terms

Creditworthy SME clients can strongly negotiate loan rates, collateral, covenants and fees, leveraging that MSMEs contribute about 30% of India’s GDP and drive significant bank business. Competing offers from banks and a large NBFC sector provide credible alternatives, compressing margins. Relationship depth and speed of sanction materially influence outcomes, while sectoral expertise and cash-flow lending allow DCB to command premium pricing.

Low switching costs in digital era

Low switching costs driven by UPI, account portability and paperless onboarding cut friction—UPI now handles tens of billions of transactions annually and onboarding can be completed in minutes. Payments, deposits and basic loans are commoditized in user experience, increasing buyer leverage to demand better pricing and service. Differentiation via superior service quality and narrow niche propositions is essential for DCB Bank to defend margins.

Wealth and affluent segment choice

Affluent clients compare advisory quality, product shelf and fees closely, driven by transparency in mutual funds (AMFI MF AUM ₹47.8 lakh crore as of Mar 2024) and insurance performance reporting, increasing fee sensitivity and wallet dilution from multi-banking relationships; goal-based advisory and open-architecture offerings help retain value.

- Advisory quality: high

- Fee sensitivity: rising

- Multi-banking: dilutes share

- Retention: goal-based + open-architecture

Rural customers with agent influence

Rural and semi-urban clients often follow local influencers and BC agents, reducing individual bargaining but allowing collective preferences to sway product uptake; with India’s BC network >1 million outlets in 2024 and ~64% population rural, service reach and trust beat marginal price cuts for banks like DCB.

Rate swings drive deposit shifts; advisory fees and rural BCs hold customers

Customers increasingly price-sensitive: UPI >100bn txns FY2023-24, 10–25bps rate moves shift deposits; CASA sticky but mobile. SMEs (~30% of GDP) negotiate rates, NBFCs compress margins; DCB’s speed/expertise can preserve spreads. Affluent clients chase advisory/fees (AMFI AUM ₹47.8 lakh crore Mar 2024). Rural trust/BC (>1mn outlets, ~64% rural) sustains stickiness.

| Metric | Value (2024) |

|---|---|

| UPI txns | >100bn FY2023-24 |

| MF AUM | ₹47.8 lakh crore Mar 2024 |

| SME GDP share | ~30% |

| BC outlets | >1,000,000 |

Preview Before You Purchase

DCB Bank Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for DCB Bank you’ll receive after purchase—no placeholders or excerpts. It contains the full competitive assessment, strategic implications, and concise insights ready for immediate download and use. What you see is the final, professionally formatted deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

DCB Bank’s Porter's Five Forces snapshot highlights competitive intensity from larger private banks, moderate buyer power from retail and SME segments, restrained supplier influence, and evolving substitute and entry threats. This brief overview teases critical risks and opportunities. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and strategic implications tailored to DCB Bank.

Suppliers Bargaining Power

Funding mix dependence

DCB Bank depends heavily on retail deposits and CASA (CASA ~46.5% in FY2024) with wholesale borrowings roughly 12% of funding; when system liquidity tightens depositors push rates up and wholesale spreads widen, raising funding costs. Limited pricing power against rate‑sensitive depositors increases supplier leverage. Increasing sticky CASA and granular term deposits can reduce this vulnerability.

Technology and fintech vendors

Core banking, cloud, cybersecurity and payments rails are concentrated among a few large vendors, increasing supplier leverage for DCB Bank. Core replacements are costly and risky, typically requiring 18–36 months and often $10–100m in investment, strengthening vendor bargaining power. Integration with UPI, BBPS and third-party APIs creates coordination dependence on these providers. Multi-vendor strategies and open standards mitigate lock-in risk.

Skilled talent and branch partners

Experienced risk officers, SME relationship managers and data scientists are scarce and mobile, driving wage inflation and retention bonuses that raise input costs—DCB Bank, which operated about 500 branches as of March 2024, faces higher staff cost pressure in growth markets. Business correspondents and rural channel partners can negotiate fees tied to reach and performance, increasing supplier leverage. Building internal talent pipelines and productivity-linked payouts can rebalance bargaining power by lowering reliance on external hires.

Credit bureaus and data providers

Lending at DCB Bank depends on bureau data, eKYC, device intelligence and analytics; three major credit bureaus control over 90% of consumer credit data in India (2024), creating take-it-or-leave-it pricing and SLA-driven 24–72 hr impacts on SME and retail underwriting. Negotiating volume-based contracts (10–30% cost cuts) and building in-house scorecards (reducing bureau pulls 20–40%) curb dependence.

- Concentration: three bureaus >90% (2024)

- SLA impact: 24–72 hr

- Volume discounts: 10–30%

- In-house scorecards reduce pulls 20–40%

Regulatory and payment infrastructure

RBI mandates (minimum CRAR 9% and LCR 100%) and NPCI rails function as quasi-suppliers for DCB Bank by controlling licenses, access and interoperability; NPCI processed over 100 billion UPI transactions in 2024, making access critical. Sudden capital, liquidity or interoperability mandates can spike operating costs, while compliance tech and reporting burdens create indirect supplier power; active participation in industry bodies helps shape timelines and reduce impact.

- RBI: CRAR ≥9%, LCR 100%

- NPCI: >100bn UPI txns (2024)

- Compliance tech adds fixed/recurring costs

- Industry bodies can influence regulation timing

Bank faces supplier leverage: CASA 46.5%, wholesale ~12%, bureaus >90%

DCB Bank faces supplier leverage from funding (CASA ~46.5% in FY2024; wholesale borrowings ~12%), concentrated core/vendor stacks, credit bureaus (>90% market share, 2024) and regulatory/NPCI control (NPCI >100bn UPI txns, 2024; RBI CRAR ≥9%, LCR 100%).

| Metric | 2024 |

|---|---|

| CASA | 46.5% |

| Wholesale funding | ~12% |

| Credit bureaus | >90% |

| UPI txns (NPCI) | >100bn |

What is included in the product

Porter's Five Forces analysis for DCB Bank uncovers competitive pressures, customer and supplier bargaining power, threats from new entrants and substitutes, and intensity of rivalry—highlighting fintech disruption, regulatory barriers, and strategic levers that shape its pricing, margins, and market positioning.

Concise Porter's Five Forces for DCB Bank—one-sheet clarity to spot competitive pressures fast, with customizable scores and a ready-to-use radar chart for instant boardroom-ready insights.

Customers Bargaining Power

Highly price-sensitive depositors

Rate-shopping via aggregators and app comparisons has raised depositor price sensitivity, with NPCI reporting UPI volumes exceeding 100 billion transactions in FY2023-24, easing account mobility. Small shifts of 10–25 basis points in TD or savings rates often trigger visible flows to competitors. CASA balances are somewhat stickier but remain mobile due to instant payments and UPI convenience. Loyalty rewards and bundled services can blunt pure price-driven churn.

SME clients negotiate terms

Creditworthy SME clients can strongly negotiate loan rates, collateral, covenants and fees, leveraging that MSMEs contribute about 30% of India’s GDP and drive significant bank business. Competing offers from banks and a large NBFC sector provide credible alternatives, compressing margins. Relationship depth and speed of sanction materially influence outcomes, while sectoral expertise and cash-flow lending allow DCB to command premium pricing.

Low switching costs in digital era

Low switching costs driven by UPI, account portability and paperless onboarding cut friction—UPI now handles tens of billions of transactions annually and onboarding can be completed in minutes. Payments, deposits and basic loans are commoditized in user experience, increasing buyer leverage to demand better pricing and service. Differentiation via superior service quality and narrow niche propositions is essential for DCB Bank to defend margins.

Wealth and affluent segment choice

Affluent clients compare advisory quality, product shelf and fees closely, driven by transparency in mutual funds (AMFI MF AUM ₹47.8 lakh crore as of Mar 2024) and insurance performance reporting, increasing fee sensitivity and wallet dilution from multi-banking relationships; goal-based advisory and open-architecture offerings help retain value.

- Advisory quality: high

- Fee sensitivity: rising

- Multi-banking: dilutes share

- Retention: goal-based + open-architecture

Rural customers with agent influence

Rural and semi-urban clients often follow local influencers and BC agents, reducing individual bargaining but allowing collective preferences to sway product uptake; with India’s BC network >1 million outlets in 2024 and ~64% population rural, service reach and trust beat marginal price cuts for banks like DCB.

Rate swings drive deposit shifts; advisory fees and rural BCs hold customers

Customers increasingly price-sensitive: UPI >100bn txns FY2023-24, 10–25bps rate moves shift deposits; CASA sticky but mobile. SMEs (~30% of GDP) negotiate rates, NBFCs compress margins; DCB’s speed/expertise can preserve spreads. Affluent clients chase advisory/fees (AMFI AUM ₹47.8 lakh crore Mar 2024). Rural trust/BC (>1mn outlets, ~64% rural) sustains stickiness.

| Metric | Value (2024) |

|---|---|

| UPI txns | >100bn FY2023-24 |

| MF AUM | ₹47.8 lakh crore Mar 2024 |

| SME GDP share | ~30% |

| BC outlets | >1,000,000 |

Preview Before You Purchase

DCB Bank Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for DCB Bank you’ll receive after purchase—no placeholders or excerpts. It contains the full competitive assessment, strategic implications, and concise insights ready for immediate download and use. What you see is the final, professionally formatted deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

DCB Bank’s Porter's Five Forces snapshot highlights competitive intensity from larger private banks, moderate buyer power from retail and SME segments, restrained supplier influence, and evolving substitute and entry threats. This brief overview teases critical risks and opportunities. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and strategic implications tailored to DCB Bank.

Suppliers Bargaining Power

Funding mix dependence

DCB Bank depends heavily on retail deposits and CASA (CASA ~46.5% in FY2024) with wholesale borrowings roughly 12% of funding; when system liquidity tightens depositors push rates up and wholesale spreads widen, raising funding costs. Limited pricing power against rate‑sensitive depositors increases supplier leverage. Increasing sticky CASA and granular term deposits can reduce this vulnerability.

Technology and fintech vendors

Core banking, cloud, cybersecurity and payments rails are concentrated among a few large vendors, increasing supplier leverage for DCB Bank. Core replacements are costly and risky, typically requiring 18–36 months and often $10–100m in investment, strengthening vendor bargaining power. Integration with UPI, BBPS and third-party APIs creates coordination dependence on these providers. Multi-vendor strategies and open standards mitigate lock-in risk.

Skilled talent and branch partners

Experienced risk officers, SME relationship managers and data scientists are scarce and mobile, driving wage inflation and retention bonuses that raise input costs—DCB Bank, which operated about 500 branches as of March 2024, faces higher staff cost pressure in growth markets. Business correspondents and rural channel partners can negotiate fees tied to reach and performance, increasing supplier leverage. Building internal talent pipelines and productivity-linked payouts can rebalance bargaining power by lowering reliance on external hires.

Credit bureaus and data providers

Lending at DCB Bank depends on bureau data, eKYC, device intelligence and analytics; three major credit bureaus control over 90% of consumer credit data in India (2024), creating take-it-or-leave-it pricing and SLA-driven 24–72 hr impacts on SME and retail underwriting. Negotiating volume-based contracts (10–30% cost cuts) and building in-house scorecards (reducing bureau pulls 20–40%) curb dependence.

- Concentration: three bureaus >90% (2024)

- SLA impact: 24–72 hr

- Volume discounts: 10–30%

- In-house scorecards reduce pulls 20–40%

Regulatory and payment infrastructure

RBI mandates (minimum CRAR 9% and LCR 100%) and NPCI rails function as quasi-suppliers for DCB Bank by controlling licenses, access and interoperability; NPCI processed over 100 billion UPI transactions in 2024, making access critical. Sudden capital, liquidity or interoperability mandates can spike operating costs, while compliance tech and reporting burdens create indirect supplier power; active participation in industry bodies helps shape timelines and reduce impact.

- RBI: CRAR ≥9%, LCR 100%

- NPCI: >100bn UPI txns (2024)

- Compliance tech adds fixed/recurring costs

- Industry bodies can influence regulation timing

Bank faces supplier leverage: CASA 46.5%, wholesale ~12%, bureaus >90%

DCB Bank faces supplier leverage from funding (CASA ~46.5% in FY2024; wholesale borrowings ~12%), concentrated core/vendor stacks, credit bureaus (>90% market share, 2024) and regulatory/NPCI control (NPCI >100bn UPI txns, 2024; RBI CRAR ≥9%, LCR 100%).

| Metric | 2024 |

|---|---|

| CASA | 46.5% |

| Wholesale funding | ~12% |

| Credit bureaus | >90% |

| UPI txns (NPCI) | >100bn |

What is included in the product

Porter's Five Forces analysis for DCB Bank uncovers competitive pressures, customer and supplier bargaining power, threats from new entrants and substitutes, and intensity of rivalry—highlighting fintech disruption, regulatory barriers, and strategic levers that shape its pricing, margins, and market positioning.

Concise Porter's Five Forces for DCB Bank—one-sheet clarity to spot competitive pressures fast, with customizable scores and a ready-to-use radar chart for instant boardroom-ready insights.

Customers Bargaining Power

Highly price-sensitive depositors

Rate-shopping via aggregators and app comparisons has raised depositor price sensitivity, with NPCI reporting UPI volumes exceeding 100 billion transactions in FY2023-24, easing account mobility. Small shifts of 10–25 basis points in TD or savings rates often trigger visible flows to competitors. CASA balances are somewhat stickier but remain mobile due to instant payments and UPI convenience. Loyalty rewards and bundled services can blunt pure price-driven churn.

SME clients negotiate terms

Creditworthy SME clients can strongly negotiate loan rates, collateral, covenants and fees, leveraging that MSMEs contribute about 30% of India’s GDP and drive significant bank business. Competing offers from banks and a large NBFC sector provide credible alternatives, compressing margins. Relationship depth and speed of sanction materially influence outcomes, while sectoral expertise and cash-flow lending allow DCB to command premium pricing.

Low switching costs in digital era

Low switching costs driven by UPI, account portability and paperless onboarding cut friction—UPI now handles tens of billions of transactions annually and onboarding can be completed in minutes. Payments, deposits and basic loans are commoditized in user experience, increasing buyer leverage to demand better pricing and service. Differentiation via superior service quality and narrow niche propositions is essential for DCB Bank to defend margins.

Wealth and affluent segment choice

Affluent clients compare advisory quality, product shelf and fees closely, driven by transparency in mutual funds (AMFI MF AUM ₹47.8 lakh crore as of Mar 2024) and insurance performance reporting, increasing fee sensitivity and wallet dilution from multi-banking relationships; goal-based advisory and open-architecture offerings help retain value.

- Advisory quality: high

- Fee sensitivity: rising

- Multi-banking: dilutes share

- Retention: goal-based + open-architecture

Rural customers with agent influence

Rural and semi-urban clients often follow local influencers and BC agents, reducing individual bargaining but allowing collective preferences to sway product uptake; with India’s BC network >1 million outlets in 2024 and ~64% population rural, service reach and trust beat marginal price cuts for banks like DCB.

Rate swings drive deposit shifts; advisory fees and rural BCs hold customers

Customers increasingly price-sensitive: UPI >100bn txns FY2023-24, 10–25bps rate moves shift deposits; CASA sticky but mobile. SMEs (~30% of GDP) negotiate rates, NBFCs compress margins; DCB’s speed/expertise can preserve spreads. Affluent clients chase advisory/fees (AMFI AUM ₹47.8 lakh crore Mar 2024). Rural trust/BC (>1mn outlets, ~64% rural) sustains stickiness.

| Metric | Value (2024) |

|---|---|

| UPI txns | >100bn FY2023-24 |

| MF AUM | ₹47.8 lakh crore Mar 2024 |

| SME GDP share | ~30% |

| BC outlets | >1,000,000 |

Preview Before You Purchase

DCB Bank Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for DCB Bank you’ll receive after purchase—no placeholders or excerpts. It contains the full competitive assessment, strategic implications, and concise insights ready for immediate download and use. What you see is the final, professionally formatted deliverable.