Derby Cycle AG Porter's Five Forces Analysis

From Overview to Strategy Blueprint

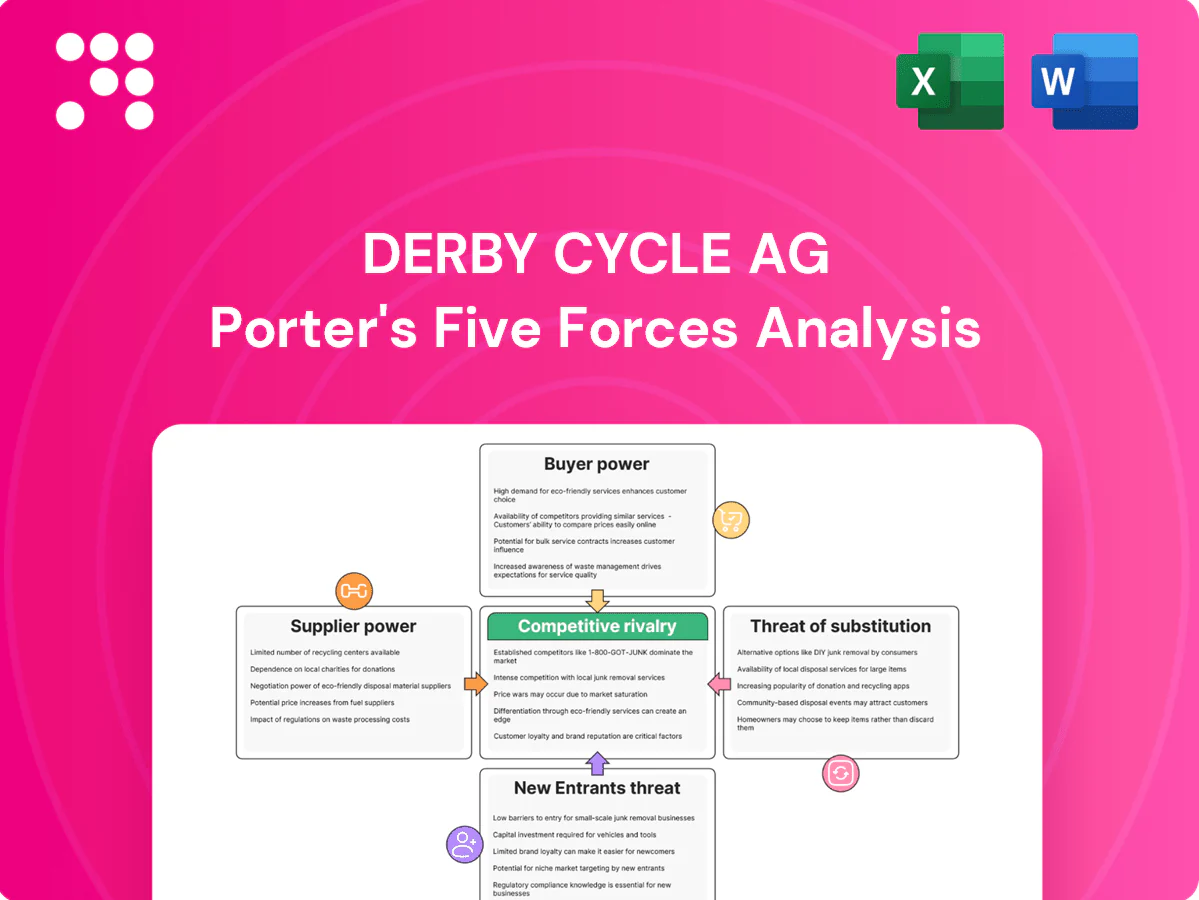

Derby Cycle AG faces intense rivalry from established bike brands and e-commerce entrants, while supplier consolidation and rising component costs press margins; buyers wield moderate power driven by price sensitivity and brand preferences, and substitutes (micromobility) pose growing threat. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Motor and battery dependency

Derby’s e-bikes depend on a concentrated set of premium drive-system suppliers—Bosch, Brose and Shimano—giving suppliers elevated leverage. Limited certified alternatives and complex integration raise tangible switching costs and certification lead times. Allocation constraints in peak seasons often shift commercial terms toward suppliers. Pon Holdings’ 2022 acquisition of Derby partly mitigates this by adding purchasing scale and negotiating clout.

Component brand concentration

Shimano and SRAM dominate drivetrains, brakes and wheels, shaping pricing and availability; Shimano reported roughly 516 billion JPY in revenue in FY2024, underscoring supplier scale. High-end Derby SKUs often specify branded components to meet customer expectations, creating semi-captive bill-of-materials and reducing sourcing flexibility. Dual-sourcing and broader spec flexibility can partially moderate this supplier power.

Frame materials and specialty inputs

Frame materials and specialty inputs exert moderate supplier power for Derby Cycle: 2024 saw aluminum and carbon-fiber supply tightness and carbon premiums keeping composite costs roughly 30% above 2019 levels, while EU industrial power averaged about €0.25/kWh, lifting input costs and margins. Specialized tooling, layup know-how and safety certifications limit quick supplier swaps; long-term contracts and nearshoring are used to smooth volatility.

Logistics and compliance constraints

Logistics and compliance constraints raise supplier bargaining power for Derby Cycle AG: the EU Battery Regulation came into force in 2024 and CE conformity for key components increases supplier-side leverage, while ongoing 2024 freight volatility has amplified delivery risk. Delays in batteries and drivetrain parts ripple through final assembly schedules, and suppliers guaranteeing compliant, on-time delivery command premiums. Integrating planning data with suppliers reduces surprise costs and buffer stock needs.

- EU 2024: Battery Regulation in force — higher compliance bar

- Freight 2024: continued volatility increases delay risk

- Premiums paid to reliable, compliant suppliers

- Shared planning data cuts surprise costs

Group purchasing advantages

Pon.Bike’s aggregated demand secures stronger volume discounts and priority allocations from component suppliers, improving Derby Cycle AG’s purchasing leverage across Kalkhoff, Focus, and Raleigh. Shared vendor scorecards and harmonized specifications standardize quality metrics and amplify negotiation clout with upstream manufacturers. Centralized sourcing reduces fragmentation but does not eliminate supplier concentration risks in key e-bike components.

Concentrated e-bike supply: Shimano ~516 bn JPY, composites +30%

Derby’s e-bike supply is concentrated among Bosch, Brose and Shimano (Shimano ~516 billion JPY revenue FY2024), giving suppliers high leverage. EU Battery Regulation (2024) and freight volatility raise compliance and delivery premiums. Pon’s 2022 integration improves volume discounts but supplier concentration and ~30% higher carbon-composite costs since 2019 keep bargaining power elevated.

| Metric | 2024 | Impact |

|---|---|---|

| Shimano rev | ~516 bn JPY | supplier scale |

| Composite premium | ~+30% vs 2019 | higher input cost |

| Regulation | EU Battery Reg 2024 | compliance premiums |

What is included in the product

Tailored Porter's Five Forces analysis for Derby Cycle AG uncovering competitive drivers, buyer and supplier power, substitutes and disruptive threats, and barriers deterring new entrants; includes industry-backed insights and strategic commentary to inform investor reports, strategy decks, or editable Word presentations.

A concise one-sheet Porter's Five Forces for Derby Cycle AG—quickly pinpoint supplier/buyer power, rival intensity and entrant threats to relieve analysis bottlenecks and speed strategic decisions.

Customers Bargaining Power

Dealer network leverage

Independent bike dealers shape assortment and pricing via floor space allocation and sell-through expectations, pressuring Derby on margins and co-op marketing commitments. Seasonal brand switching by dealers increases negotiation leverage on terms and promotional support. Rising after-sales service expectations drive higher warranty and service costs for Derby. Strong brand recognition for Focus and Kalkhoff helps secure shelf space despite dealer bargaining power.

Price-sensitive consumers

Mid-market buyers for Derby Cycle compare features and prices widely, intensifying discount pressure as the global e‑bike market exceeded USD 40 billion in 2024 and competition widened. Online transparency—with online channels accounting for roughly 20% of bicycle sales in Europe in 2024—heightens cross‑shopping on components and specs. Financing offers and seasonal promos drive conversion, while premium e‑bike buyers, who can pay 20–40% price premiums, show lower elasticity.

Low switching costs

Customers can readily switch among established brands offering similar specs, keeping bargaining power high; Derby Cycle AG reported 2023 revenue of about €634 million, underscoring a competitive market. Warranty, dealer service networks and OTA software updates create mild stickiness but not full lock-in. D2C rivals—whose share rose toward 15% of e-bike sales in 2024—lower barriers with home delivery and trial programs. Superior ride quality and distinctive design remain the main levers to raise perceived switching costs.

Demand for after-sales support

E-bike buyers demand reliable service, on-board diagnostics and battery protection; EU consumer rules mandate a minimum 2-year guarantee which raises service expectations. Dealers push Derby Cycle for technician training, diagnostic tools and fast parts flow, squeezing margins; bundled service plans can lower churn but raise per-unit costs. Robust service KPIs (response time, first-time fix rate) can flip buyer power into loyalty.

- Service expectation: EU 2-year guarantee

- Dealer demands: training, tools, fast parts

- Trade-off: bundled plans reduce churn vs higher cost

- KPI focus: response time, first-time fix

Institutional and fleet buyers

Institutional and fleet buyers such as leasing firms, corporate fleets, and public procurement exert strong price and SLA pressure on Derby Cycle AG, leveraging larger order sizes to secure volume concessions and tighter terms. They increasingly demand customization and data integration for fleet telematics and maintenance, raising production complexity. Winning multi-year framework agreements stabilizes volumes but typically compresses margins and increases service obligations.

- High negotiation leverage

- Volume discounts expected

- Customization and data integration required

- Frameworks stabilize volumes, reduce margins

Dealers squeeze margins despite €634m; online 20% and D2C 15%

Dealers and institutional buyers exert strong price and service leverage, squeezing margins despite Derby Cycle AG 2023 revenue ~€634m. Online transparency (≈20% EU sales 2024) and D2C (≈15% e-bike share 2024) increase cross‑shopping; premium buyers pay 20–40% more, reducing elasticity. EU 2‑year guarantee and fleet SLAs raise service costs but bundled plans and strong KPIs can improve retention.

| Metric | 2023/2024 |

|---|---|

| Revenue (Derby Cycle) | ~€634m (2023) |

| Global e‑bike market | >$40bn (2024) |

| Online EU sales | ~20% (2024) |

| D2C e‑bike share | ~15% (2024) |

What You See Is What You Get

Derby Cycle AG Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Derby Cycle AG you'll receive immediately after purchase—no surprises, no placeholders. The document is complete, professionally formatted and ready to download the moment you buy. Use it as-is for strategic decisions, valuation inputs, or competitor assessment.

From Overview to Strategy Blueprint

Derby Cycle AG faces intense rivalry from established bike brands and e-commerce entrants, while supplier consolidation and rising component costs press margins; buyers wield moderate power driven by price sensitivity and brand preferences, and substitutes (micromobility) pose growing threat. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Motor and battery dependency

Derby’s e-bikes depend on a concentrated set of premium drive-system suppliers—Bosch, Brose and Shimano—giving suppliers elevated leverage. Limited certified alternatives and complex integration raise tangible switching costs and certification lead times. Allocation constraints in peak seasons often shift commercial terms toward suppliers. Pon Holdings’ 2022 acquisition of Derby partly mitigates this by adding purchasing scale and negotiating clout.

Component brand concentration

Shimano and SRAM dominate drivetrains, brakes and wheels, shaping pricing and availability; Shimano reported roughly 516 billion JPY in revenue in FY2024, underscoring supplier scale. High-end Derby SKUs often specify branded components to meet customer expectations, creating semi-captive bill-of-materials and reducing sourcing flexibility. Dual-sourcing and broader spec flexibility can partially moderate this supplier power.

Frame materials and specialty inputs

Frame materials and specialty inputs exert moderate supplier power for Derby Cycle: 2024 saw aluminum and carbon-fiber supply tightness and carbon premiums keeping composite costs roughly 30% above 2019 levels, while EU industrial power averaged about €0.25/kWh, lifting input costs and margins. Specialized tooling, layup know-how and safety certifications limit quick supplier swaps; long-term contracts and nearshoring are used to smooth volatility.

Logistics and compliance constraints

Logistics and compliance constraints raise supplier bargaining power for Derby Cycle AG: the EU Battery Regulation came into force in 2024 and CE conformity for key components increases supplier-side leverage, while ongoing 2024 freight volatility has amplified delivery risk. Delays in batteries and drivetrain parts ripple through final assembly schedules, and suppliers guaranteeing compliant, on-time delivery command premiums. Integrating planning data with suppliers reduces surprise costs and buffer stock needs.

- EU 2024: Battery Regulation in force — higher compliance bar

- Freight 2024: continued volatility increases delay risk

- Premiums paid to reliable, compliant suppliers

- Shared planning data cuts surprise costs

Group purchasing advantages

Pon.Bike’s aggregated demand secures stronger volume discounts and priority allocations from component suppliers, improving Derby Cycle AG’s purchasing leverage across Kalkhoff, Focus, and Raleigh. Shared vendor scorecards and harmonized specifications standardize quality metrics and amplify negotiation clout with upstream manufacturers. Centralized sourcing reduces fragmentation but does not eliminate supplier concentration risks in key e-bike components.

Concentrated e-bike supply: Shimano ~516 bn JPY, composites +30%

Derby’s e-bike supply is concentrated among Bosch, Brose and Shimano (Shimano ~516 billion JPY revenue FY2024), giving suppliers high leverage. EU Battery Regulation (2024) and freight volatility raise compliance and delivery premiums. Pon’s 2022 integration improves volume discounts but supplier concentration and ~30% higher carbon-composite costs since 2019 keep bargaining power elevated.

| Metric | 2024 | Impact |

|---|---|---|

| Shimano rev | ~516 bn JPY | supplier scale |

| Composite premium | ~+30% vs 2019 | higher input cost |

| Regulation | EU Battery Reg 2024 | compliance premiums |

What is included in the product

Tailored Porter's Five Forces analysis for Derby Cycle AG uncovering competitive drivers, buyer and supplier power, substitutes and disruptive threats, and barriers deterring new entrants; includes industry-backed insights and strategic commentary to inform investor reports, strategy decks, or editable Word presentations.

A concise one-sheet Porter's Five Forces for Derby Cycle AG—quickly pinpoint supplier/buyer power, rival intensity and entrant threats to relieve analysis bottlenecks and speed strategic decisions.

Customers Bargaining Power

Dealer network leverage

Independent bike dealers shape assortment and pricing via floor space allocation and sell-through expectations, pressuring Derby on margins and co-op marketing commitments. Seasonal brand switching by dealers increases negotiation leverage on terms and promotional support. Rising after-sales service expectations drive higher warranty and service costs for Derby. Strong brand recognition for Focus and Kalkhoff helps secure shelf space despite dealer bargaining power.

Price-sensitive consumers

Mid-market buyers for Derby Cycle compare features and prices widely, intensifying discount pressure as the global e‑bike market exceeded USD 40 billion in 2024 and competition widened. Online transparency—with online channels accounting for roughly 20% of bicycle sales in Europe in 2024—heightens cross‑shopping on components and specs. Financing offers and seasonal promos drive conversion, while premium e‑bike buyers, who can pay 20–40% price premiums, show lower elasticity.

Low switching costs

Customers can readily switch among established brands offering similar specs, keeping bargaining power high; Derby Cycle AG reported 2023 revenue of about €634 million, underscoring a competitive market. Warranty, dealer service networks and OTA software updates create mild stickiness but not full lock-in. D2C rivals—whose share rose toward 15% of e-bike sales in 2024—lower barriers with home delivery and trial programs. Superior ride quality and distinctive design remain the main levers to raise perceived switching costs.

Demand for after-sales support

E-bike buyers demand reliable service, on-board diagnostics and battery protection; EU consumer rules mandate a minimum 2-year guarantee which raises service expectations. Dealers push Derby Cycle for technician training, diagnostic tools and fast parts flow, squeezing margins; bundled service plans can lower churn but raise per-unit costs. Robust service KPIs (response time, first-time fix rate) can flip buyer power into loyalty.

- Service expectation: EU 2-year guarantee

- Dealer demands: training, tools, fast parts

- Trade-off: bundled plans reduce churn vs higher cost

- KPI focus: response time, first-time fix

Institutional and fleet buyers

Institutional and fleet buyers such as leasing firms, corporate fleets, and public procurement exert strong price and SLA pressure on Derby Cycle AG, leveraging larger order sizes to secure volume concessions and tighter terms. They increasingly demand customization and data integration for fleet telematics and maintenance, raising production complexity. Winning multi-year framework agreements stabilizes volumes but typically compresses margins and increases service obligations.

- High negotiation leverage

- Volume discounts expected

- Customization and data integration required

- Frameworks stabilize volumes, reduce margins

Dealers squeeze margins despite €634m; online 20% and D2C 15%

Dealers and institutional buyers exert strong price and service leverage, squeezing margins despite Derby Cycle AG 2023 revenue ~€634m. Online transparency (≈20% EU sales 2024) and D2C (≈15% e-bike share 2024) increase cross‑shopping; premium buyers pay 20–40% more, reducing elasticity. EU 2‑year guarantee and fleet SLAs raise service costs but bundled plans and strong KPIs can improve retention.

| Metric | 2023/2024 |

|---|---|

| Revenue (Derby Cycle) | ~€634m (2023) |

| Global e‑bike market | >$40bn (2024) |

| Online EU sales | ~20% (2024) |

| D2C e‑bike share | ~15% (2024) |

What You See Is What You Get

Derby Cycle AG Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Derby Cycle AG you'll receive immediately after purchase—no surprises, no placeholders. The document is complete, professionally formatted and ready to download the moment you buy. Use it as-is for strategic decisions, valuation inputs, or competitor assessment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Derby Cycle AG faces intense rivalry from established bike brands and e-commerce entrants, while supplier consolidation and rising component costs press margins; buyers wield moderate power driven by price sensitivity and brand preferences, and substitutes (micromobility) pose growing threat. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Motor and battery dependency

Derby’s e-bikes depend on a concentrated set of premium drive-system suppliers—Bosch, Brose and Shimano—giving suppliers elevated leverage. Limited certified alternatives and complex integration raise tangible switching costs and certification lead times. Allocation constraints in peak seasons often shift commercial terms toward suppliers. Pon Holdings’ 2022 acquisition of Derby partly mitigates this by adding purchasing scale and negotiating clout.

Component brand concentration

Shimano and SRAM dominate drivetrains, brakes and wheels, shaping pricing and availability; Shimano reported roughly 516 billion JPY in revenue in FY2024, underscoring supplier scale. High-end Derby SKUs often specify branded components to meet customer expectations, creating semi-captive bill-of-materials and reducing sourcing flexibility. Dual-sourcing and broader spec flexibility can partially moderate this supplier power.

Frame materials and specialty inputs

Frame materials and specialty inputs exert moderate supplier power for Derby Cycle: 2024 saw aluminum and carbon-fiber supply tightness and carbon premiums keeping composite costs roughly 30% above 2019 levels, while EU industrial power averaged about €0.25/kWh, lifting input costs and margins. Specialized tooling, layup know-how and safety certifications limit quick supplier swaps; long-term contracts and nearshoring are used to smooth volatility.

Logistics and compliance constraints

Logistics and compliance constraints raise supplier bargaining power for Derby Cycle AG: the EU Battery Regulation came into force in 2024 and CE conformity for key components increases supplier-side leverage, while ongoing 2024 freight volatility has amplified delivery risk. Delays in batteries and drivetrain parts ripple through final assembly schedules, and suppliers guaranteeing compliant, on-time delivery command premiums. Integrating planning data with suppliers reduces surprise costs and buffer stock needs.

- EU 2024: Battery Regulation in force — higher compliance bar

- Freight 2024: continued volatility increases delay risk

- Premiums paid to reliable, compliant suppliers

- Shared planning data cuts surprise costs

Group purchasing advantages

Pon.Bike’s aggregated demand secures stronger volume discounts and priority allocations from component suppliers, improving Derby Cycle AG’s purchasing leverage across Kalkhoff, Focus, and Raleigh. Shared vendor scorecards and harmonized specifications standardize quality metrics and amplify negotiation clout with upstream manufacturers. Centralized sourcing reduces fragmentation but does not eliminate supplier concentration risks in key e-bike components.

Concentrated e-bike supply: Shimano ~516 bn JPY, composites +30%

Derby’s e-bike supply is concentrated among Bosch, Brose and Shimano (Shimano ~516 billion JPY revenue FY2024), giving suppliers high leverage. EU Battery Regulation (2024) and freight volatility raise compliance and delivery premiums. Pon’s 2022 integration improves volume discounts but supplier concentration and ~30% higher carbon-composite costs since 2019 keep bargaining power elevated.

| Metric | 2024 | Impact |

|---|---|---|

| Shimano rev | ~516 bn JPY | supplier scale |

| Composite premium | ~+30% vs 2019 | higher input cost |

| Regulation | EU Battery Reg 2024 | compliance premiums |

What is included in the product

Tailored Porter's Five Forces analysis for Derby Cycle AG uncovering competitive drivers, buyer and supplier power, substitutes and disruptive threats, and barriers deterring new entrants; includes industry-backed insights and strategic commentary to inform investor reports, strategy decks, or editable Word presentations.

A concise one-sheet Porter's Five Forces for Derby Cycle AG—quickly pinpoint supplier/buyer power, rival intensity and entrant threats to relieve analysis bottlenecks and speed strategic decisions.

Customers Bargaining Power

Dealer network leverage

Independent bike dealers shape assortment and pricing via floor space allocation and sell-through expectations, pressuring Derby on margins and co-op marketing commitments. Seasonal brand switching by dealers increases negotiation leverage on terms and promotional support. Rising after-sales service expectations drive higher warranty and service costs for Derby. Strong brand recognition for Focus and Kalkhoff helps secure shelf space despite dealer bargaining power.

Price-sensitive consumers

Mid-market buyers for Derby Cycle compare features and prices widely, intensifying discount pressure as the global e‑bike market exceeded USD 40 billion in 2024 and competition widened. Online transparency—with online channels accounting for roughly 20% of bicycle sales in Europe in 2024—heightens cross‑shopping on components and specs. Financing offers and seasonal promos drive conversion, while premium e‑bike buyers, who can pay 20–40% price premiums, show lower elasticity.

Low switching costs

Customers can readily switch among established brands offering similar specs, keeping bargaining power high; Derby Cycle AG reported 2023 revenue of about €634 million, underscoring a competitive market. Warranty, dealer service networks and OTA software updates create mild stickiness but not full lock-in. D2C rivals—whose share rose toward 15% of e-bike sales in 2024—lower barriers with home delivery and trial programs. Superior ride quality and distinctive design remain the main levers to raise perceived switching costs.

Demand for after-sales support

E-bike buyers demand reliable service, on-board diagnostics and battery protection; EU consumer rules mandate a minimum 2-year guarantee which raises service expectations. Dealers push Derby Cycle for technician training, diagnostic tools and fast parts flow, squeezing margins; bundled service plans can lower churn but raise per-unit costs. Robust service KPIs (response time, first-time fix rate) can flip buyer power into loyalty.

- Service expectation: EU 2-year guarantee

- Dealer demands: training, tools, fast parts

- Trade-off: bundled plans reduce churn vs higher cost

- KPI focus: response time, first-time fix

Institutional and fleet buyers

Institutional and fleet buyers such as leasing firms, corporate fleets, and public procurement exert strong price and SLA pressure on Derby Cycle AG, leveraging larger order sizes to secure volume concessions and tighter terms. They increasingly demand customization and data integration for fleet telematics and maintenance, raising production complexity. Winning multi-year framework agreements stabilizes volumes but typically compresses margins and increases service obligations.

- High negotiation leverage

- Volume discounts expected

- Customization and data integration required

- Frameworks stabilize volumes, reduce margins

Dealers squeeze margins despite €634m; online 20% and D2C 15%

Dealers and institutional buyers exert strong price and service leverage, squeezing margins despite Derby Cycle AG 2023 revenue ~€634m. Online transparency (≈20% EU sales 2024) and D2C (≈15% e-bike share 2024) increase cross‑shopping; premium buyers pay 20–40% more, reducing elasticity. EU 2‑year guarantee and fleet SLAs raise service costs but bundled plans and strong KPIs can improve retention.

| Metric | 2023/2024 |

|---|---|

| Revenue (Derby Cycle) | ~€634m (2023) |

| Global e‑bike market | >$40bn (2024) |

| Online EU sales | ~20% (2024) |

| D2C e‑bike share | ~15% (2024) |

What You See Is What You Get

Derby Cycle AG Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Derby Cycle AG you'll receive immediately after purchase—no surprises, no placeholders. The document is complete, professionally formatted and ready to download the moment you buy. Use it as-is for strategic decisions, valuation inputs, or competitor assessment.