Descours & Cebaud SA Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Descours & Cebaud SA faces moderate supplier power, fragmented buyer segments, and intensifying digital competition that reshape margins and growth prospects. Understanding substitute threats and entry barriers is crucial for strategy and valuation. This brief scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Fragmented supplier base limits leverage

Descours & Cabaud faces a highly fragmented supplier base across fasteners, plumbing fittings and consumables, which dilutes individual supplier power and reduces risk of single-source dependence. The distributor routinely dual-sources and benchmarks vendor pricing to secure competitive rates. Aggregated purchasing volumes enable improved rebates and contractual terms. Fragmentation gives leverage to negotiate shorter lead times and higher availability.

Strong brands and OEMs hold selective power

In PPE, tools and specialized metal systems, marquee brands and OEMs exert selective pricing and merchandising control, with customers often stipulating approved brands that raise switching costs for distributors. Suppliers commonly enforce MAP policies and resort to allocation during shortages, constraining Descours & Cabaud’s purchasing flexibility. The distributor counters with private‑label offerings and a broad portfolio to preserve margins and availability. This dual strategy reduces dependence on any single supplier channel.

Commodity input volatility passes through

Metals and industrial supplies show high volatility, with benchmark copper and steel price swings around ±20% between 2023–2024, prompting suppliers to add surcharges and shorten quote validity, shifting part of the risk to distributors. Descours & Cabaud offsets this via dynamic pricing, faster inventory turns and scale-driven hedging and buffer-stock negotiations supported by its large purchasing volumes.

Logistics and lead-time dependence

Supply reliability directly affects service-level commitments to construction and manufacturing clients, and suppliers with stronger logistics networks can insist on steadier volumes and shorter lead times. Descours & Cabaud deploys vendor-managed inventory, EDI and forecasting to align flows; VMI studies (2024) show stockouts down ~30% and holding costs down ~20%. Diversification of carriers and suppliers reduces disruption risk and supplier leverage.

- Supply reliability: impacts SLAs for construction/manufacturing

- Supplier logistics power: drives volume commitments

- Operational tools: VMI, EDI, forecasting (VMI: −30% stockouts, −20% holding costs)

- Diversification: lowers disruption risk and supplier leverage

Private label as counterbalance

Descours & Cabaud strengthened supplier bargaining by growing private-label PPE and consumables, with private-label share reaching c.20% of PPE sales in 2024, improving gross margins by ~6 percentage points and allowing tighter control over specs. When branded supply tightened in 2023–24, private label provided alternative fulfillment and raised leverage versus OEMs and third-party vendors.

- private-label share: c.20% (2024)

- margin uplift: ~+6 p.p.

- reduces OEM dependence; boosts negotiation power

Fragmented suppliers, dual-sourcing and private-label lift PPE margins amid ±20% metals volatility

Supplier power is moderated by a fragmented vendor base, dual‑sourcing and scale-driven purchasing (private‑label c.20% of PPE sales in 2024, margin uplift ~+6 p.p.). Metals volatility (±20% 2023–24) and branded OEM control raise upstream leverage, offset by VMI, EDI and diversification (VMI: −30% stockouts, −20% holding costs).

| Metric | Value |

|---|---|

| Private‑label PPE | c.20% (2024) |

| Margin uplift | +6 p.p. |

| Metals volatility | ±20% (2023–24) |

| VMI impact | −30% stockouts, −20% holding costs |

What is included in the product

Tailored exclusively for Descours & Cebaud SA, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and barriers to entry affecting pricing and profitability. It identifies disruptive entrants and substitute threats while offering strategic insights to safeguard market position.

A clear, one-sheet Porter's Five Forces summary for Descours & Cebaud SA—perfect for quick supplier/distributor strategic decisions and boardroom use.

Customers Bargaining Power

Large accounts negotiate hard

Construction majors, manufacturers and public entities centralize purchasing and run tenders so that top 10 accounts can represent ~40% of distributor revenue in 2024, driving discounts of 5–12% and rebates. Framework agreements commonly compress gross margins by 150–300 basis points while securing share-of-wallet. Service bundling (maintenance, logistics) lifts retention and can raise effective wallet share by ~6–10%, helping defend pricing.

Price transparency intensifies

Digital catalogs and marketplaces enable easy cross-vendor comparisons, letting buyers benchmark list and net pricing across SKUs; with over 70% of procurement searches starting online in 2024 this intensifies pricing pressure on Descours & Cabaud to maintain competitive net prices. Any premium must be justified by measurable value-added services such as logistics, technical support or rapid replenishment.

Multi-sourcing reduces lock-in

Professional buyers frequently multi-source to split volumes and sustain pricing pressure; switching costs for standardized MRO items remain low, making price competition intense. Descours & Cabaud offsets this by reinforcing delivery reliability and flexible credit terms that create customer stickiness. Value-added services such as technical support and customized kitting materially raise switching barriers and preserve higher-margin relationships.

Service-level expectations

Next-day delivery, on-site counters and emergency fulfillment are critical for projects and maintenance, giving buyers leverage to demand strict SLA adherence and impose penalties for delays. Penalties and contract clauses amplify buyer bargaining power, while the distributor offsets this by investing in network density and wider inventory to secure uptime. Measured performance data from deliveries and fulfillment drives renewals and upsells.

- Next-day delivery critical

- SLA penalties increase buyer leverage

- Network density & inventory breadth as mitigation

- Performance data fuels renewals/upsells

Specification and compliance demands

Buyers demand certified PPE with CE marking and traceability under Regulation (EU) 2016/425, plus documented quality audits and regulatory compliance, raising service and fulfilment costs for suppliers.

For Descours & Cabaud SA, documented compliance capabilities serve as a differentiator against low-cost rivals, reducing purely price-driven bargaining by proving supply-chain reliability and audit readiness.

- Regulatory anchor: Regulation (EU) 2016/425

- Higher audit/documentation cost pressure

- Compliance strengthens differentiation vs low-cost peers

Top buyers cut 5-12% with 150-300bp margin squeeze; 70% of procurement starts online

Large buyers (top 10 ≈40% revenue) extract 5–12% discounts and 150–300 bp margin compression via framework agreements; 70% of procurement searches start online in 2024, intensifying price benchmarking. Multi-sourcing and low switching costs for MRO increase price pressure; service bundling, next-day delivery and EU 2016/425 compliance raise switching barriers and defend margins.

| Metric | 2024 Data |

|---|---|

| Top-10 share | ≈40% |

| Discounts | 5–12% |

| Margin compression | 150–300 bp |

| Online searches | 70% |

Preview the Actual Deliverable

Descours & Cebaud SA Porter's Five Forces Analysis

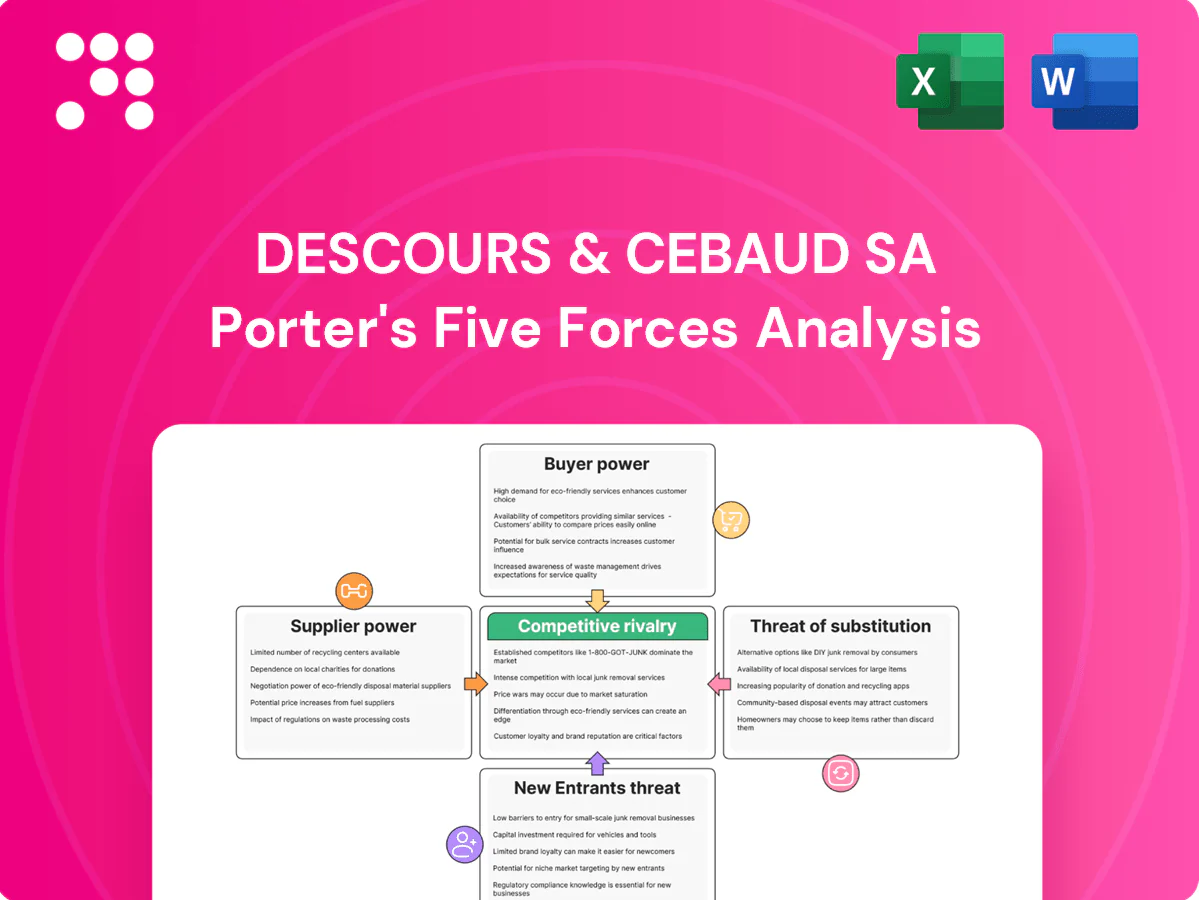

The Descours & Cebaud SA Porter’s Five Forces analysis assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and regulatory factors shaping margins and strategic options. It highlights key levers for defensible positioning, procurement risks, and growth barriers with actionable implications for management and investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Go Beyond the Preview—Access the Full Strategic Report

Descours & Cebaud SA faces moderate supplier power, fragmented buyer segments, and intensifying digital competition that reshape margins and growth prospects. Understanding substitute threats and entry barriers is crucial for strategy and valuation. This brief scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Fragmented supplier base limits leverage

Descours & Cabaud faces a highly fragmented supplier base across fasteners, plumbing fittings and consumables, which dilutes individual supplier power and reduces risk of single-source dependence. The distributor routinely dual-sources and benchmarks vendor pricing to secure competitive rates. Aggregated purchasing volumes enable improved rebates and contractual terms. Fragmentation gives leverage to negotiate shorter lead times and higher availability.

Strong brands and OEMs hold selective power

In PPE, tools and specialized metal systems, marquee brands and OEMs exert selective pricing and merchandising control, with customers often stipulating approved brands that raise switching costs for distributors. Suppliers commonly enforce MAP policies and resort to allocation during shortages, constraining Descours & Cabaud’s purchasing flexibility. The distributor counters with private‑label offerings and a broad portfolio to preserve margins and availability. This dual strategy reduces dependence on any single supplier channel.

Commodity input volatility passes through

Metals and industrial supplies show high volatility, with benchmark copper and steel price swings around ±20% between 2023–2024, prompting suppliers to add surcharges and shorten quote validity, shifting part of the risk to distributors. Descours & Cabaud offsets this via dynamic pricing, faster inventory turns and scale-driven hedging and buffer-stock negotiations supported by its large purchasing volumes.

Logistics and lead-time dependence

Supply reliability directly affects service-level commitments to construction and manufacturing clients, and suppliers with stronger logistics networks can insist on steadier volumes and shorter lead times. Descours & Cabaud deploys vendor-managed inventory, EDI and forecasting to align flows; VMI studies (2024) show stockouts down ~30% and holding costs down ~20%. Diversification of carriers and suppliers reduces disruption risk and supplier leverage.

- Supply reliability: impacts SLAs for construction/manufacturing

- Supplier logistics power: drives volume commitments

- Operational tools: VMI, EDI, forecasting (VMI: −30% stockouts, −20% holding costs)

- Diversification: lowers disruption risk and supplier leverage

Private label as counterbalance

Descours & Cabaud strengthened supplier bargaining by growing private-label PPE and consumables, with private-label share reaching c.20% of PPE sales in 2024, improving gross margins by ~6 percentage points and allowing tighter control over specs. When branded supply tightened in 2023–24, private label provided alternative fulfillment and raised leverage versus OEMs and third-party vendors.

- private-label share: c.20% (2024)

- margin uplift: ~+6 p.p.

- reduces OEM dependence; boosts negotiation power

Fragmented suppliers, dual-sourcing and private-label lift PPE margins amid ±20% metals volatility

Supplier power is moderated by a fragmented vendor base, dual‑sourcing and scale-driven purchasing (private‑label c.20% of PPE sales in 2024, margin uplift ~+6 p.p.). Metals volatility (±20% 2023–24) and branded OEM control raise upstream leverage, offset by VMI, EDI and diversification (VMI: −30% stockouts, −20% holding costs).

| Metric | Value |

|---|---|

| Private‑label PPE | c.20% (2024) |

| Margin uplift | +6 p.p. |

| Metals volatility | ±20% (2023–24) |

| VMI impact | −30% stockouts, −20% holding costs |

What is included in the product

Tailored exclusively for Descours & Cebaud SA, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and barriers to entry affecting pricing and profitability. It identifies disruptive entrants and substitute threats while offering strategic insights to safeguard market position.

A clear, one-sheet Porter's Five Forces summary for Descours & Cebaud SA—perfect for quick supplier/distributor strategic decisions and boardroom use.

Customers Bargaining Power

Large accounts negotiate hard

Construction majors, manufacturers and public entities centralize purchasing and run tenders so that top 10 accounts can represent ~40% of distributor revenue in 2024, driving discounts of 5–12% and rebates. Framework agreements commonly compress gross margins by 150–300 basis points while securing share-of-wallet. Service bundling (maintenance, logistics) lifts retention and can raise effective wallet share by ~6–10%, helping defend pricing.

Price transparency intensifies

Digital catalogs and marketplaces enable easy cross-vendor comparisons, letting buyers benchmark list and net pricing across SKUs; with over 70% of procurement searches starting online in 2024 this intensifies pricing pressure on Descours & Cabaud to maintain competitive net prices. Any premium must be justified by measurable value-added services such as logistics, technical support or rapid replenishment.

Multi-sourcing reduces lock-in

Professional buyers frequently multi-source to split volumes and sustain pricing pressure; switching costs for standardized MRO items remain low, making price competition intense. Descours & Cabaud offsets this by reinforcing delivery reliability and flexible credit terms that create customer stickiness. Value-added services such as technical support and customized kitting materially raise switching barriers and preserve higher-margin relationships.

Service-level expectations

Next-day delivery, on-site counters and emergency fulfillment are critical for projects and maintenance, giving buyers leverage to demand strict SLA adherence and impose penalties for delays. Penalties and contract clauses amplify buyer bargaining power, while the distributor offsets this by investing in network density and wider inventory to secure uptime. Measured performance data from deliveries and fulfillment drives renewals and upsells.

- Next-day delivery critical

- SLA penalties increase buyer leverage

- Network density & inventory breadth as mitigation

- Performance data fuels renewals/upsells

Specification and compliance demands

Buyers demand certified PPE with CE marking and traceability under Regulation (EU) 2016/425, plus documented quality audits and regulatory compliance, raising service and fulfilment costs for suppliers.

For Descours & Cabaud SA, documented compliance capabilities serve as a differentiator against low-cost rivals, reducing purely price-driven bargaining by proving supply-chain reliability and audit readiness.

- Regulatory anchor: Regulation (EU) 2016/425

- Higher audit/documentation cost pressure

- Compliance strengthens differentiation vs low-cost peers

Top buyers cut 5-12% with 150-300bp margin squeeze; 70% of procurement starts online

Large buyers (top 10 ≈40% revenue) extract 5–12% discounts and 150–300 bp margin compression via framework agreements; 70% of procurement searches start online in 2024, intensifying price benchmarking. Multi-sourcing and low switching costs for MRO increase price pressure; service bundling, next-day delivery and EU 2016/425 compliance raise switching barriers and defend margins.

| Metric | 2024 Data |

|---|---|

| Top-10 share | ≈40% |

| Discounts | 5–12% |

| Margin compression | 150–300 bp |

| Online searches | 70% |

Preview the Actual Deliverable

Descours & Cebaud SA Porter's Five Forces Analysis

The Descours & Cebaud SA Porter’s Five Forces analysis assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and regulatory factors shaping margins and strategic options. It highlights key levers for defensible positioning, procurement risks, and growth barriers with actionable implications for management and investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Description

Go Beyond the Preview—Access the Full Strategic Report

Descours & Cebaud SA faces moderate supplier power, fragmented buyer segments, and intensifying digital competition that reshape margins and growth prospects. Understanding substitute threats and entry barriers is crucial for strategy and valuation. This brief scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Fragmented supplier base limits leverage

Descours & Cabaud faces a highly fragmented supplier base across fasteners, plumbing fittings and consumables, which dilutes individual supplier power and reduces risk of single-source dependence. The distributor routinely dual-sources and benchmarks vendor pricing to secure competitive rates. Aggregated purchasing volumes enable improved rebates and contractual terms. Fragmentation gives leverage to negotiate shorter lead times and higher availability.

Strong brands and OEMs hold selective power

In PPE, tools and specialized metal systems, marquee brands and OEMs exert selective pricing and merchandising control, with customers often stipulating approved brands that raise switching costs for distributors. Suppliers commonly enforce MAP policies and resort to allocation during shortages, constraining Descours & Cabaud’s purchasing flexibility. The distributor counters with private‑label offerings and a broad portfolio to preserve margins and availability. This dual strategy reduces dependence on any single supplier channel.

Commodity input volatility passes through

Metals and industrial supplies show high volatility, with benchmark copper and steel price swings around ±20% between 2023–2024, prompting suppliers to add surcharges and shorten quote validity, shifting part of the risk to distributors. Descours & Cabaud offsets this via dynamic pricing, faster inventory turns and scale-driven hedging and buffer-stock negotiations supported by its large purchasing volumes.

Logistics and lead-time dependence

Supply reliability directly affects service-level commitments to construction and manufacturing clients, and suppliers with stronger logistics networks can insist on steadier volumes and shorter lead times. Descours & Cabaud deploys vendor-managed inventory, EDI and forecasting to align flows; VMI studies (2024) show stockouts down ~30% and holding costs down ~20%. Diversification of carriers and suppliers reduces disruption risk and supplier leverage.

- Supply reliability: impacts SLAs for construction/manufacturing

- Supplier logistics power: drives volume commitments

- Operational tools: VMI, EDI, forecasting (VMI: −30% stockouts, −20% holding costs)

- Diversification: lowers disruption risk and supplier leverage

Private label as counterbalance

Descours & Cabaud strengthened supplier bargaining by growing private-label PPE and consumables, with private-label share reaching c.20% of PPE sales in 2024, improving gross margins by ~6 percentage points and allowing tighter control over specs. When branded supply tightened in 2023–24, private label provided alternative fulfillment and raised leverage versus OEMs and third-party vendors.

- private-label share: c.20% (2024)

- margin uplift: ~+6 p.p.

- reduces OEM dependence; boosts negotiation power

Fragmented suppliers, dual-sourcing and private-label lift PPE margins amid ±20% metals volatility

Supplier power is moderated by a fragmented vendor base, dual‑sourcing and scale-driven purchasing (private‑label c.20% of PPE sales in 2024, margin uplift ~+6 p.p.). Metals volatility (±20% 2023–24) and branded OEM control raise upstream leverage, offset by VMI, EDI and diversification (VMI: −30% stockouts, −20% holding costs).

| Metric | Value |

|---|---|

| Private‑label PPE | c.20% (2024) |

| Margin uplift | +6 p.p. |

| Metals volatility | ±20% (2023–24) |

| VMI impact | −30% stockouts, −20% holding costs |

What is included in the product

Tailored exclusively for Descours & Cebaud SA, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and barriers to entry affecting pricing and profitability. It identifies disruptive entrants and substitute threats while offering strategic insights to safeguard market position.

A clear, one-sheet Porter's Five Forces summary for Descours & Cebaud SA—perfect for quick supplier/distributor strategic decisions and boardroom use.

Customers Bargaining Power

Large accounts negotiate hard

Construction majors, manufacturers and public entities centralize purchasing and run tenders so that top 10 accounts can represent ~40% of distributor revenue in 2024, driving discounts of 5–12% and rebates. Framework agreements commonly compress gross margins by 150–300 basis points while securing share-of-wallet. Service bundling (maintenance, logistics) lifts retention and can raise effective wallet share by ~6–10%, helping defend pricing.

Price transparency intensifies

Digital catalogs and marketplaces enable easy cross-vendor comparisons, letting buyers benchmark list and net pricing across SKUs; with over 70% of procurement searches starting online in 2024 this intensifies pricing pressure on Descours & Cabaud to maintain competitive net prices. Any premium must be justified by measurable value-added services such as logistics, technical support or rapid replenishment.

Multi-sourcing reduces lock-in

Professional buyers frequently multi-source to split volumes and sustain pricing pressure; switching costs for standardized MRO items remain low, making price competition intense. Descours & Cabaud offsets this by reinforcing delivery reliability and flexible credit terms that create customer stickiness. Value-added services such as technical support and customized kitting materially raise switching barriers and preserve higher-margin relationships.

Service-level expectations

Next-day delivery, on-site counters and emergency fulfillment are critical for projects and maintenance, giving buyers leverage to demand strict SLA adherence and impose penalties for delays. Penalties and contract clauses amplify buyer bargaining power, while the distributor offsets this by investing in network density and wider inventory to secure uptime. Measured performance data from deliveries and fulfillment drives renewals and upsells.

- Next-day delivery critical

- SLA penalties increase buyer leverage

- Network density & inventory breadth as mitigation

- Performance data fuels renewals/upsells

Specification and compliance demands

Buyers demand certified PPE with CE marking and traceability under Regulation (EU) 2016/425, plus documented quality audits and regulatory compliance, raising service and fulfilment costs for suppliers.

For Descours & Cabaud SA, documented compliance capabilities serve as a differentiator against low-cost rivals, reducing purely price-driven bargaining by proving supply-chain reliability and audit readiness.

- Regulatory anchor: Regulation (EU) 2016/425

- Higher audit/documentation cost pressure

- Compliance strengthens differentiation vs low-cost peers

Top buyers cut 5-12% with 150-300bp margin squeeze; 70% of procurement starts online

Large buyers (top 10 ≈40% revenue) extract 5–12% discounts and 150–300 bp margin compression via framework agreements; 70% of procurement searches start online in 2024, intensifying price benchmarking. Multi-sourcing and low switching costs for MRO increase price pressure; service bundling, next-day delivery and EU 2016/425 compliance raise switching barriers and defend margins.

| Metric | 2024 Data |

|---|---|

| Top-10 share | ≈40% |

| Discounts | 5–12% |

| Margin compression | 150–300 bp |

| Online searches | 70% |

Preview the Actual Deliverable

Descours & Cebaud SA Porter's Five Forces Analysis

The Descours & Cebaud SA Porter’s Five Forces analysis assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and regulatory factors shaping margins and strategic options. It highlights key levers for defensible positioning, procurement risks, and growth barriers with actionable implications for management and investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.