Dexterra Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

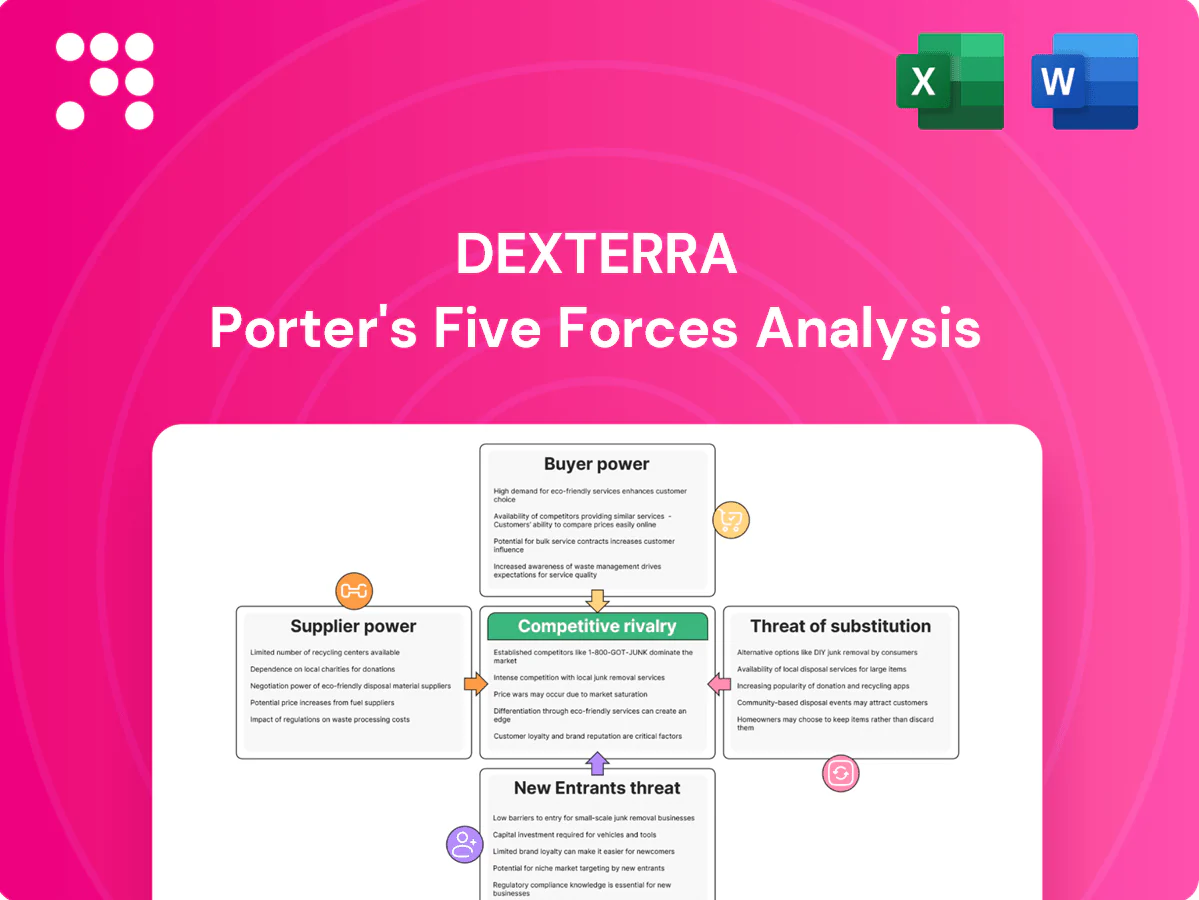

Dexterra's Porter's Five Forces snapshot assesses supplier power, buyer pressure, competitive rivalry, threat of new entrants, and substitute risks to reveal where margins and vulnerabilities lie. It highlights contract-driven revenue strength and regional concentration risks shaping negotiating leverage. This brief preview outlines key dynamics and implications for strategy. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical inputs

Key inputs—steel, lumber, HVAC and generators—and specialty trades are concentrated, with modular components and camp equipment sourced from a handful of qualified vendors, increasing supplier leverage. In tight cycles allocation skews to larger orders, pressuring pricing and lead times. Dexterra mitigates exposure through multi-sourcing and framework agreements to secure capacity and stable terms.

Labor and subcontractor scarcity

Remote Dexterra projects demand certified skilled labor that remains scarce: ManpowerGroup 2024 found 48% of employers reporting talent shortages, elevating subcontractor bargaining power. Subcontractors in remote regions command 10–25% premiums or priority access, while 2024 wage inflation in field services averaged near 5%, plus travel premiums, raising input costs. Long-term labor partnerships and training pipelines cut exposure by stabilizing supply and pricing.

Food, fuel, and utilities volatility

Catering and accommodations for Dexterra depend heavily on food commodities and energy inputs; the FAO Food Price Index averaged about 119 in 2024 and Brent crude averaged roughly $90/bbl, driving cost risk. Price swings pass through unevenly depending on contract clauses, shifting margins to either client or provider. Logistics to remote sites amplifies volatility and supplier power through higher transport and bunkering premiums. Hedging and indexed contracts are used to stabilize margins and cap exposure.

Tech and FM systems dependence

CMMS, IoT sensors and advanced cleaning technologies are concentrated among a few vendors, and with 17.1 billion connected IoT devices in 2024, integration and data lock-in materially raise switching costs. License and maintenance fees (typical SaaS maintenance ~18% ARR) give suppliers pricing leverage, while open standards and modular IT architectures can dilute that power.

- Concentration: limited vendors

- Scale: 17.1B IoT devices (2024)

- Costs: ~18% ARR maintenance

- Mitigation: open standards/modularity

Logistics and last-mile access

Specialized transport and remote-access carriers are limited in many Dexterra markets, giving suppliers leverage; last-mile can represent 40–60% of total delivery cost (2024), while remote-route freight often costs 2–4x urban rates. Weather and seasonal capacity volatility amplify negotiating power and freight surcharges can trim margins rapidly, so long-term carrier contracts and staged inventory mitigate exposure.

Supplier power: 17.1B IoT, labor shortages 48%, Brent ~$90 - pricing & switching costs rise

Supplier concentration across steel, modular components and specialized services gives vendors pricing leverage; key tech suppliers create switching costs (17.1B IoT devices, 18% ARR maintenance). Labor scarcity lifts subcontractor power (ManpowerGroup 2024: 48% report shortages; field wage inflation ~5%). Energy and logistics (FAO index 119; Brent ~$90/bbl; last-mile 40–60%) amplify cost volatility; hedging and long-term contracts mitigate.

| Metric | 2024 Value |

|---|---|

| IoT devices | 17.1B |

| Labor shortages | 48% |

| Brent | $90/bbl |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Dexterra, assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, plus disruptive risks and strategic implications—editable Word, ready for reports.

A clear, one-sheet summary of Dexterra's Porter's Five Forces—ideal for quick strategic decisions, customizable for evolving market data, and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Large enterprise and public buyers

Mining, energy, government, healthcare and education clients buy at scale, often via centralized procurement; OECD data shows public procurement averages about 12% of GDP. Centralized RFPs and formal tendering create strong pricing pressure and require detailed compliance. Buyers routinely demand SLAs, penalties and regular performance reporting. Dexterra competes by emphasizing total value, robust compliance and measurable outcomes.

Multi-year, rebiddable contracts

Multi-year, rebiddable contracts deliver volume stability for Dexterra but frequent rebids enable price resets at renewal, keeping customer leverage high. Incumbency provides operational advantages and smoother transition assurances, yet structured handovers make switching feasible for many clients. Benchmarking and indexation clauses commonly limit escalations to CPI or agreed indices, tightening margin flexibility. Demonstrable performance differentiation drives renewals and pricing power.

Service bundling expectations

Clients increasingly demand integrated FM, accommodations and modular solutions from a single provider; a 2024 industry survey found 58% of corporate buyers prefer bundled services. Bundling shifts volume leverage to buyers, who commonly negotiate package discounts of 10–20% on multi-service contracts. Effective cross-selling can defend margins by expanding scope and raising average contract value by roughly 12% in 2024 cases. High customization and service integration increase client stickiness despite stronger buyer power.

Price transparency and benchmarks

Price transparency in FM and camp services is high, with regional market rates readily available; the global facilities management market was estimated near US$1.2 trillion in 2024, increasing buyer leverage. Clients use third-party benchmarks from IFMA, JLL and CBRE to challenge quotes, while open-book contracting has been shown to compress margins materially. Dexterra offsets pressure via cost engineering and productivity guarantees that protect EBITDA.

- Benchmarks: IFMA/JLL/CBRE

- Market size: ~US$1.2T (2024)

- Open-book: compresses margins

- Mitigants: cost engineering, productivity guarantees

ESG and indigenous participation

Public and resource clients increasingly mandate ESG, safety, and Indigenous engagement; in 2024 these non-price requirements routinely eliminate bidders who lack documented plans and certifications, while differentiating compliant contractors like Dexterra.

Embedding Indigenous partnerships and ESG systems raises switching frictions and recurring compliance costs, shifting negotiations away from pure price toward performance and risk-sharing metrics.

Strong demonstrated compliance in 2024 tempered customer price bargaining by creating measurable value in social license and contract continuity.

- ESG/safety/Indigenous clauses: barrier to entry

- Compliance raises switching costs and retention

- Non-price differentiation reduces pure price bargaining

Buyers drive price pressure: public procurement ~12% GDP, FM market US$1.2T

Buyers exert high leverage via centralized procurement (public procurement ~12% GDP) and transparent FM pricing (global FM ~US$1.2T in 2024), driving strong price pressure. Bundling demand (58% prefer bundled services) yields 10–20% negotiated discounts though cross-sell can raise contract value ~12%. ESG/Indigenous requirements in 2024 increasingly eliminate non-compliant bidders, shifting negotiation toward performance.

| Metric | 2024 Value |

|---|---|

| Public procurement | ~12% GDP |

| Global FM market | ~US$1.2T |

| Buyer bundle preference | 58% |

| Typical bundle discount | 10–20% |

| Cross-sell uplift | ~12% |

Preview the Actual Deliverable

Dexterra Porter's Five Forces Analysis

This preview shows the exact Dexterra Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted and ready to download and use the moment you buy. You’re viewing the final deliverable, identical to the file provided on completion of payment.

Go Beyond the Preview—Access the Full Strategic Report

Dexterra's Porter's Five Forces snapshot assesses supplier power, buyer pressure, competitive rivalry, threat of new entrants, and substitute risks to reveal where margins and vulnerabilities lie. It highlights contract-driven revenue strength and regional concentration risks shaping negotiating leverage. This brief preview outlines key dynamics and implications for strategy. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical inputs

Key inputs—steel, lumber, HVAC and generators—and specialty trades are concentrated, with modular components and camp equipment sourced from a handful of qualified vendors, increasing supplier leverage. In tight cycles allocation skews to larger orders, pressuring pricing and lead times. Dexterra mitigates exposure through multi-sourcing and framework agreements to secure capacity and stable terms.

Labor and subcontractor scarcity

Remote Dexterra projects demand certified skilled labor that remains scarce: ManpowerGroup 2024 found 48% of employers reporting talent shortages, elevating subcontractor bargaining power. Subcontractors in remote regions command 10–25% premiums or priority access, while 2024 wage inflation in field services averaged near 5%, plus travel premiums, raising input costs. Long-term labor partnerships and training pipelines cut exposure by stabilizing supply and pricing.

Food, fuel, and utilities volatility

Catering and accommodations for Dexterra depend heavily on food commodities and energy inputs; the FAO Food Price Index averaged about 119 in 2024 and Brent crude averaged roughly $90/bbl, driving cost risk. Price swings pass through unevenly depending on contract clauses, shifting margins to either client or provider. Logistics to remote sites amplifies volatility and supplier power through higher transport and bunkering premiums. Hedging and indexed contracts are used to stabilize margins and cap exposure.

Tech and FM systems dependence

CMMS, IoT sensors and advanced cleaning technologies are concentrated among a few vendors, and with 17.1 billion connected IoT devices in 2024, integration and data lock-in materially raise switching costs. License and maintenance fees (typical SaaS maintenance ~18% ARR) give suppliers pricing leverage, while open standards and modular IT architectures can dilute that power.

- Concentration: limited vendors

- Scale: 17.1B IoT devices (2024)

- Costs: ~18% ARR maintenance

- Mitigation: open standards/modularity

Logistics and last-mile access

Specialized transport and remote-access carriers are limited in many Dexterra markets, giving suppliers leverage; last-mile can represent 40–60% of total delivery cost (2024), while remote-route freight often costs 2–4x urban rates. Weather and seasonal capacity volatility amplify negotiating power and freight surcharges can trim margins rapidly, so long-term carrier contracts and staged inventory mitigate exposure.

Supplier power: 17.1B IoT, labor shortages 48%, Brent ~$90 - pricing & switching costs rise

Supplier concentration across steel, modular components and specialized services gives vendors pricing leverage; key tech suppliers create switching costs (17.1B IoT devices, 18% ARR maintenance). Labor scarcity lifts subcontractor power (ManpowerGroup 2024: 48% report shortages; field wage inflation ~5%). Energy and logistics (FAO index 119; Brent ~$90/bbl; last-mile 40–60%) amplify cost volatility; hedging and long-term contracts mitigate.

| Metric | 2024 Value |

|---|---|

| IoT devices | 17.1B |

| Labor shortages | 48% |

| Brent | $90/bbl |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Dexterra, assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, plus disruptive risks and strategic implications—editable Word, ready for reports.

A clear, one-sheet summary of Dexterra's Porter's Five Forces—ideal for quick strategic decisions, customizable for evolving market data, and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Large enterprise and public buyers

Mining, energy, government, healthcare and education clients buy at scale, often via centralized procurement; OECD data shows public procurement averages about 12% of GDP. Centralized RFPs and formal tendering create strong pricing pressure and require detailed compliance. Buyers routinely demand SLAs, penalties and regular performance reporting. Dexterra competes by emphasizing total value, robust compliance and measurable outcomes.

Multi-year, rebiddable contracts

Multi-year, rebiddable contracts deliver volume stability for Dexterra but frequent rebids enable price resets at renewal, keeping customer leverage high. Incumbency provides operational advantages and smoother transition assurances, yet structured handovers make switching feasible for many clients. Benchmarking and indexation clauses commonly limit escalations to CPI or agreed indices, tightening margin flexibility. Demonstrable performance differentiation drives renewals and pricing power.

Service bundling expectations

Clients increasingly demand integrated FM, accommodations and modular solutions from a single provider; a 2024 industry survey found 58% of corporate buyers prefer bundled services. Bundling shifts volume leverage to buyers, who commonly negotiate package discounts of 10–20% on multi-service contracts. Effective cross-selling can defend margins by expanding scope and raising average contract value by roughly 12% in 2024 cases. High customization and service integration increase client stickiness despite stronger buyer power.

Price transparency and benchmarks

Price transparency in FM and camp services is high, with regional market rates readily available; the global facilities management market was estimated near US$1.2 trillion in 2024, increasing buyer leverage. Clients use third-party benchmarks from IFMA, JLL and CBRE to challenge quotes, while open-book contracting has been shown to compress margins materially. Dexterra offsets pressure via cost engineering and productivity guarantees that protect EBITDA.

- Benchmarks: IFMA/JLL/CBRE

- Market size: ~US$1.2T (2024)

- Open-book: compresses margins

- Mitigants: cost engineering, productivity guarantees

ESG and indigenous participation

Public and resource clients increasingly mandate ESG, safety, and Indigenous engagement; in 2024 these non-price requirements routinely eliminate bidders who lack documented plans and certifications, while differentiating compliant contractors like Dexterra.

Embedding Indigenous partnerships and ESG systems raises switching frictions and recurring compliance costs, shifting negotiations away from pure price toward performance and risk-sharing metrics.

Strong demonstrated compliance in 2024 tempered customer price bargaining by creating measurable value in social license and contract continuity.

- ESG/safety/Indigenous clauses: barrier to entry

- Compliance raises switching costs and retention

- Non-price differentiation reduces pure price bargaining

Buyers drive price pressure: public procurement ~12% GDP, FM market US$1.2T

Buyers exert high leverage via centralized procurement (public procurement ~12% GDP) and transparent FM pricing (global FM ~US$1.2T in 2024), driving strong price pressure. Bundling demand (58% prefer bundled services) yields 10–20% negotiated discounts though cross-sell can raise contract value ~12%. ESG/Indigenous requirements in 2024 increasingly eliminate non-compliant bidders, shifting negotiation toward performance.

| Metric | 2024 Value |

|---|---|

| Public procurement | ~12% GDP |

| Global FM market | ~US$1.2T |

| Buyer bundle preference | 58% |

| Typical bundle discount | 10–20% |

| Cross-sell uplift | ~12% |

Preview the Actual Deliverable

Dexterra Porter's Five Forces Analysis

This preview shows the exact Dexterra Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted and ready to download and use the moment you buy. You’re viewing the final deliverable, identical to the file provided on completion of payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Dexterra's Porter's Five Forces snapshot assesses supplier power, buyer pressure, competitive rivalry, threat of new entrants, and substitute risks to reveal where margins and vulnerabilities lie. It highlights contract-driven revenue strength and regional concentration risks shaping negotiating leverage. This brief preview outlines key dynamics and implications for strategy. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical inputs

Key inputs—steel, lumber, HVAC and generators—and specialty trades are concentrated, with modular components and camp equipment sourced from a handful of qualified vendors, increasing supplier leverage. In tight cycles allocation skews to larger orders, pressuring pricing and lead times. Dexterra mitigates exposure through multi-sourcing and framework agreements to secure capacity and stable terms.

Labor and subcontractor scarcity

Remote Dexterra projects demand certified skilled labor that remains scarce: ManpowerGroup 2024 found 48% of employers reporting talent shortages, elevating subcontractor bargaining power. Subcontractors in remote regions command 10–25% premiums or priority access, while 2024 wage inflation in field services averaged near 5%, plus travel premiums, raising input costs. Long-term labor partnerships and training pipelines cut exposure by stabilizing supply and pricing.

Food, fuel, and utilities volatility

Catering and accommodations for Dexterra depend heavily on food commodities and energy inputs; the FAO Food Price Index averaged about 119 in 2024 and Brent crude averaged roughly $90/bbl, driving cost risk. Price swings pass through unevenly depending on contract clauses, shifting margins to either client or provider. Logistics to remote sites amplifies volatility and supplier power through higher transport and bunkering premiums. Hedging and indexed contracts are used to stabilize margins and cap exposure.

Tech and FM systems dependence

CMMS, IoT sensors and advanced cleaning technologies are concentrated among a few vendors, and with 17.1 billion connected IoT devices in 2024, integration and data lock-in materially raise switching costs. License and maintenance fees (typical SaaS maintenance ~18% ARR) give suppliers pricing leverage, while open standards and modular IT architectures can dilute that power.

- Concentration: limited vendors

- Scale: 17.1B IoT devices (2024)

- Costs: ~18% ARR maintenance

- Mitigation: open standards/modularity

Logistics and last-mile access

Specialized transport and remote-access carriers are limited in many Dexterra markets, giving suppliers leverage; last-mile can represent 40–60% of total delivery cost (2024), while remote-route freight often costs 2–4x urban rates. Weather and seasonal capacity volatility amplify negotiating power and freight surcharges can trim margins rapidly, so long-term carrier contracts and staged inventory mitigate exposure.

Supplier power: 17.1B IoT, labor shortages 48%, Brent ~$90 - pricing & switching costs rise

Supplier concentration across steel, modular components and specialized services gives vendors pricing leverage; key tech suppliers create switching costs (17.1B IoT devices, 18% ARR maintenance). Labor scarcity lifts subcontractor power (ManpowerGroup 2024: 48% report shortages; field wage inflation ~5%). Energy and logistics (FAO index 119; Brent ~$90/bbl; last-mile 40–60%) amplify cost volatility; hedging and long-term contracts mitigate.

| Metric | 2024 Value |

|---|---|

| IoT devices | 17.1B |

| Labor shortages | 48% |

| Brent | $90/bbl |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Dexterra, assessing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, plus disruptive risks and strategic implications—editable Word, ready for reports.

A clear, one-sheet summary of Dexterra's Porter's Five Forces—ideal for quick strategic decisions, customizable for evolving market data, and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Large enterprise and public buyers

Mining, energy, government, healthcare and education clients buy at scale, often via centralized procurement; OECD data shows public procurement averages about 12% of GDP. Centralized RFPs and formal tendering create strong pricing pressure and require detailed compliance. Buyers routinely demand SLAs, penalties and regular performance reporting. Dexterra competes by emphasizing total value, robust compliance and measurable outcomes.

Multi-year, rebiddable contracts

Multi-year, rebiddable contracts deliver volume stability for Dexterra but frequent rebids enable price resets at renewal, keeping customer leverage high. Incumbency provides operational advantages and smoother transition assurances, yet structured handovers make switching feasible for many clients. Benchmarking and indexation clauses commonly limit escalations to CPI or agreed indices, tightening margin flexibility. Demonstrable performance differentiation drives renewals and pricing power.

Service bundling expectations

Clients increasingly demand integrated FM, accommodations and modular solutions from a single provider; a 2024 industry survey found 58% of corporate buyers prefer bundled services. Bundling shifts volume leverage to buyers, who commonly negotiate package discounts of 10–20% on multi-service contracts. Effective cross-selling can defend margins by expanding scope and raising average contract value by roughly 12% in 2024 cases. High customization and service integration increase client stickiness despite stronger buyer power.

Price transparency and benchmarks

Price transparency in FM and camp services is high, with regional market rates readily available; the global facilities management market was estimated near US$1.2 trillion in 2024, increasing buyer leverage. Clients use third-party benchmarks from IFMA, JLL and CBRE to challenge quotes, while open-book contracting has been shown to compress margins materially. Dexterra offsets pressure via cost engineering and productivity guarantees that protect EBITDA.

- Benchmarks: IFMA/JLL/CBRE

- Market size: ~US$1.2T (2024)

- Open-book: compresses margins

- Mitigants: cost engineering, productivity guarantees

ESG and indigenous participation

Public and resource clients increasingly mandate ESG, safety, and Indigenous engagement; in 2024 these non-price requirements routinely eliminate bidders who lack documented plans and certifications, while differentiating compliant contractors like Dexterra.

Embedding Indigenous partnerships and ESG systems raises switching frictions and recurring compliance costs, shifting negotiations away from pure price toward performance and risk-sharing metrics.

Strong demonstrated compliance in 2024 tempered customer price bargaining by creating measurable value in social license and contract continuity.

- ESG/safety/Indigenous clauses: barrier to entry

- Compliance raises switching costs and retention

- Non-price differentiation reduces pure price bargaining

Buyers drive price pressure: public procurement ~12% GDP, FM market US$1.2T

Buyers exert high leverage via centralized procurement (public procurement ~12% GDP) and transparent FM pricing (global FM ~US$1.2T in 2024), driving strong price pressure. Bundling demand (58% prefer bundled services) yields 10–20% negotiated discounts though cross-sell can raise contract value ~12%. ESG/Indigenous requirements in 2024 increasingly eliminate non-compliant bidders, shifting negotiation toward performance.

| Metric | 2024 Value |

|---|---|

| Public procurement | ~12% GDP |

| Global FM market | ~US$1.2T |

| Buyer bundle preference | 58% |

| Typical bundle discount | 10–20% |

| Cross-sell uplift | ~12% |

Preview the Actual Deliverable

Dexterra Porter's Five Forces Analysis

This preview shows the exact Dexterra Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted and ready to download and use the moment you buy. You’re viewing the final deliverable, identical to the file provided on completion of payment.