DFIN Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

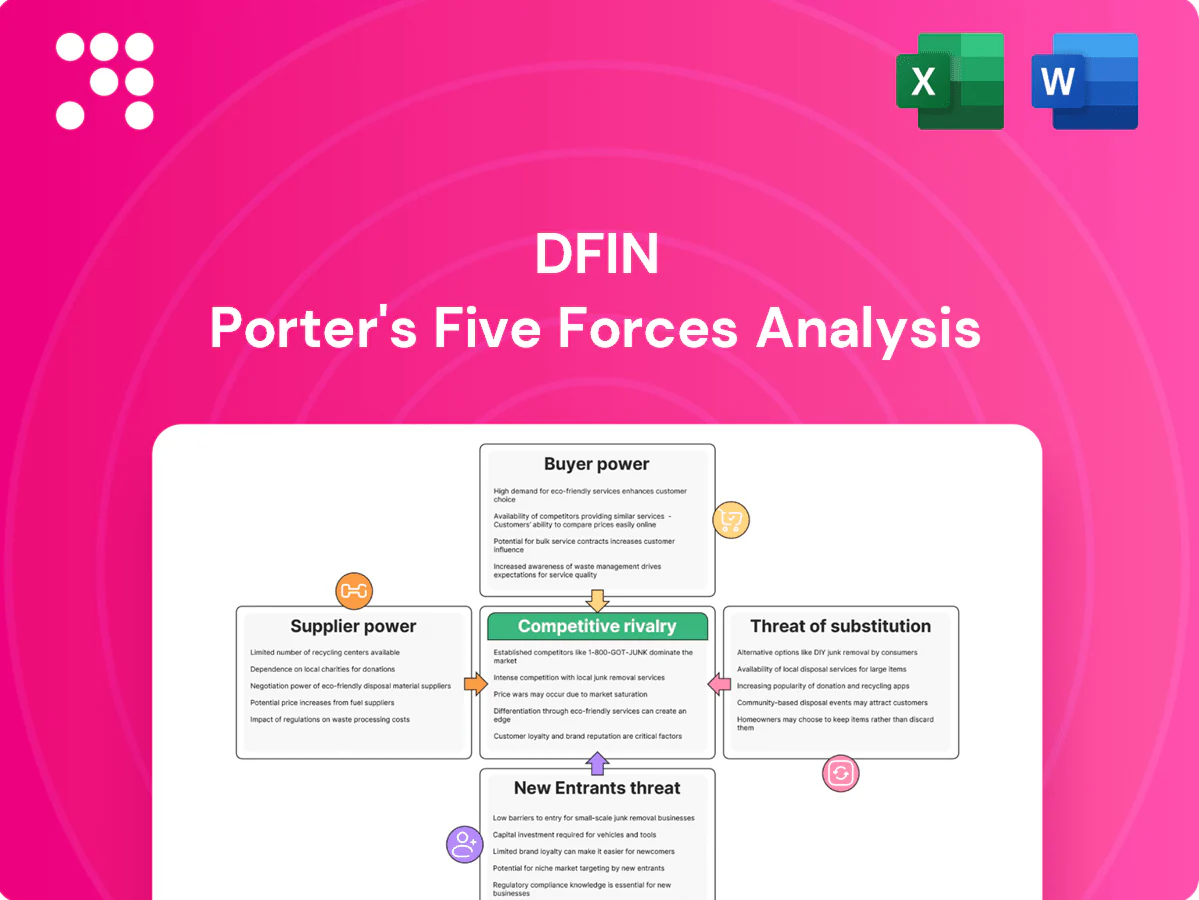

DFIN faces nuanced competitive pressures—from concentrated buyers to evolving substitute technologies—that shape margins and strategic choices; this snapshot highlights key tension points and opportunity areas. For investors and strategists, understanding these forces is critical to positioning and risk management. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to DFIN.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

DFIN relies on major cloud providers for scalable, secure infrastructure; top three hyperscalers (AWS 33%, Azure 23%, GCP 11% in 2024) control ~67% of the market, enabling pricing and contractual leverage. Multi-cloud designs and long-term contracts temper that power, but stringent performance SLAs and SEC/SOX compliance needs materially constrain switching and raise migration costs.

Niche regulatory data providers

Specialized taxonomy, regulatory content, and niche market data are sourced from a limited pool, giving these suppliers disproportionate bargaining power over pricing and access. Scarcity enables leverage on contract terms, while DFIN can mitigate risk through content partnerships and building internal curation capabilities. High accuracy and timeliness requirements, however, constrain substitution and force reliance on trusted providers.

Specialized compliance talent

Subject-matter experts and certified engineers are critical inputs, and tight 2024 labor markets—ManpowerGroup reporting 69% of employers facing talent shortages—drive wage pressure and attrition risk.

DFIN offsets this with training pipelines and global delivery hubs to scale capacity, but project timing and quality still hinge on securing scarce expertise.

Third‑party software and security tools

DFIN integrates entitlement, encryption, and monitoring from select vendors, and 2024 market dynamics—with enterprise security spend exceeding $180B—mean certification alignment (SOC 2, ISO 27001) materially narrows viable suppliers, increasing supplier power via bundled pricing and lock‑in; open standards and modular architecture preserve flexibility and reduce switching costs.

- Certs: SOC 2/ISO 27001

- Risk: bundled pricing, lock‑in

- Mitigation: open standards, modular design

Print and communications vendors

For DFIN, print and logistics partners remain critical for shareholder communications and regulated mailings; U.S. commercial printing revenue was roughly $64 billion in 2024, keeping supplier capacity central to service continuity. Peak filing seasons can push lead times and spot pricing up 10–25%, shifting bargaining power to suppliers. Maintaining multi-vendor rosters and improved demand forecasting mitigates risk, while gradual digital adoption (annual e-delivery growth ~6% in 2024) reduces long-term print dependence.

- Supplier concentration: medium — capacity spikes boost leverage

- Cost sensitivity: high — peak premiums ~10–25%

- Mitigants: multi-vendor rosters, forecasting

- Trend: digital adoption up ~6% in 2024, lowering print reliance

Supplier squeeze: hyperscaler concentration 33%/23%/11%, talent 69%

DFIN faces concentrated supplier power: hyperscalers (AWS 33%/Azure 23%/GCP 11% in 2024) and niche content providers constrain pricing and switching. Talent shortages (ManpowerGroup 69% in 2024) and security certification needs (enterprise security spend >$180B) increase leverage. Print capacity peaks (US commercial printing ~$64B; peak premiums 10–25%) further tilt power to suppliers.

| Metric | 2024 Value |

|---|---|

| Hyperscaler share | AWS 33% / Azure 23% / GCP 11% |

| Security spend | > $180B |

| Talent shortage | 69% |

| US printing rev | $64B |

| E-delivery growth | ~6% |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, substitutes, and entry threats specific to DFIN, combining industry data and strategic commentary to assess pricing power and market defenses; fully editable Word format for investor decks, business plans, or internal strategy.

A concise, one-sheet DFIN Porter's Five Forces tool that visualizes strategic pressure with dynamic spider charts, lets you customize force levels and swap in your own data, requires no macros, and exports clean slides for rapid decision-making.

Customers Bargaining Power

Large enterprise customers

Banks, asset managers and public companies buy at scale and run competitive RFPs, with procurement teams negotiating aggressively; Gartner 2024 finds RFP-driven sourcing often yields 5–15% cost savings. Volume and reference-client value amplify bargaining power, driving deeper discounts on per-user and per-deal pricing. Multi-year contracts frequently trade lower rates for revenue visibility and retention, stabilizing lifetime value despite initial concessions.

High switching costs, but not absolute

Workflow embedding via templates and integrations makes switching from DFIN costly, as customers migrate entrenched processes and automated filings. Data residency requirements and immutable audit trails in 2024 amplify migration complexity and legal risk for clients. Standardized reporting formats permit eventual transition, so DFIN must reinforce stickiness through ecosystem lock-in and superior support.

Price sensitivity and bundling

Clients increasingly demand bundled savings across reporting, GRC, and communications—58% of enterprise buyers in 2024 favored integrated suites to lower vendor count and costs. Transparent competitor pricing has intensified price pressure, compressing average deal ASPs by mid-single digits. Value-based pricing tied to measurable risk reduction can protect margins, while deeper cross-sell raises perceived total cost of ownership and improves retention.

Regulatory deadlines increase leverage

Hard filing dates such as the SEC 10-K 60-day (accelerated) and 90-day (large accelerated) deadlines put delivery risk squarely on vendors, letting buyers demand penalties or service credits for misses; operational exposure increases customer leverage in SLAs, while consistent on-time performance by DFIN can rebalance negotiations.

- Buyers leverage penalties/service credits

In‑house build alternatives

Larger institutions increasingly evaluate in-house builds with legal and compliance teams as a negotiating lever; 2024 surveys show this is common among enterprise finance buyers. Build options anchor feature and price discussions, but total lifecycle costs, upkeep, and regulatory audits often make buying more cost-effective. DFIN must emphasize faster deployment, stronger assurance, and superior auditability to counter build arguments.

- In‑house as leverage

- Anchors negotiations

- Lifecycle cost disadvantage for build

- DFIN: speed, assurance, auditability

RFPs deliver 5-15% savings as 58% prefer suites; ASPs compress, switching costs rise

Banks, asset managers and public firms wield strong price leverage via RFPs, with Gartner 2024 reporting 5–15% cost savings on RFP-driven sourcing. 58% of enterprise buyers in 2024 prefer integrated suites, increasing bundle demands while transparent competitor pricing compresses ASPs by mid-single digits. Regulatory deadlines (SEC 60/90 days) and penalties boost buyer leverage but DFIN’s on-time record and integrations raise switching costs.

| Metric | 2024 Value |

|---|---|

| RFP savings (Gartner) | 5–15% |

| Prefer integrated suites | 58% |

| ASP compression | mid-single digits |

Full Version Awaits

DFIN Porter's Five Forces Analysis

This preview displays the exact DFIN Porter's Five Forces Analysis you'll receive after purchase—no mockups, no placeholders. The file is fully formatted, professionally written, and ready for immediate download and use. What you see here is the final deliverable, identical to the document delivered upon payment.

A Must-Have Tool for Decision-Makers

DFIN faces nuanced competitive pressures—from concentrated buyers to evolving substitute technologies—that shape margins and strategic choices; this snapshot highlights key tension points and opportunity areas. For investors and strategists, understanding these forces is critical to positioning and risk management. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to DFIN.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

DFIN relies on major cloud providers for scalable, secure infrastructure; top three hyperscalers (AWS 33%, Azure 23%, GCP 11% in 2024) control ~67% of the market, enabling pricing and contractual leverage. Multi-cloud designs and long-term contracts temper that power, but stringent performance SLAs and SEC/SOX compliance needs materially constrain switching and raise migration costs.

Niche regulatory data providers

Specialized taxonomy, regulatory content, and niche market data are sourced from a limited pool, giving these suppliers disproportionate bargaining power over pricing and access. Scarcity enables leverage on contract terms, while DFIN can mitigate risk through content partnerships and building internal curation capabilities. High accuracy and timeliness requirements, however, constrain substitution and force reliance on trusted providers.

Specialized compliance talent

Subject-matter experts and certified engineers are critical inputs, and tight 2024 labor markets—ManpowerGroup reporting 69% of employers facing talent shortages—drive wage pressure and attrition risk.

DFIN offsets this with training pipelines and global delivery hubs to scale capacity, but project timing and quality still hinge on securing scarce expertise.

Third‑party software and security tools

DFIN integrates entitlement, encryption, and monitoring from select vendors, and 2024 market dynamics—with enterprise security spend exceeding $180B—mean certification alignment (SOC 2, ISO 27001) materially narrows viable suppliers, increasing supplier power via bundled pricing and lock‑in; open standards and modular architecture preserve flexibility and reduce switching costs.

- Certs: SOC 2/ISO 27001

- Risk: bundled pricing, lock‑in

- Mitigation: open standards, modular design

Print and communications vendors

For DFIN, print and logistics partners remain critical for shareholder communications and regulated mailings; U.S. commercial printing revenue was roughly $64 billion in 2024, keeping supplier capacity central to service continuity. Peak filing seasons can push lead times and spot pricing up 10–25%, shifting bargaining power to suppliers. Maintaining multi-vendor rosters and improved demand forecasting mitigates risk, while gradual digital adoption (annual e-delivery growth ~6% in 2024) reduces long-term print dependence.

- Supplier concentration: medium — capacity spikes boost leverage

- Cost sensitivity: high — peak premiums ~10–25%

- Mitigants: multi-vendor rosters, forecasting

- Trend: digital adoption up ~6% in 2024, lowering print reliance

Supplier squeeze: hyperscaler concentration 33%/23%/11%, talent 69%

DFIN faces concentrated supplier power: hyperscalers (AWS 33%/Azure 23%/GCP 11% in 2024) and niche content providers constrain pricing and switching. Talent shortages (ManpowerGroup 69% in 2024) and security certification needs (enterprise security spend >$180B) increase leverage. Print capacity peaks (US commercial printing ~$64B; peak premiums 10–25%) further tilt power to suppliers.

| Metric | 2024 Value |

|---|---|

| Hyperscaler share | AWS 33% / Azure 23% / GCP 11% |

| Security spend | > $180B |

| Talent shortage | 69% |

| US printing rev | $64B |

| E-delivery growth | ~6% |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, substitutes, and entry threats specific to DFIN, combining industry data and strategic commentary to assess pricing power and market defenses; fully editable Word format for investor decks, business plans, or internal strategy.

A concise, one-sheet DFIN Porter's Five Forces tool that visualizes strategic pressure with dynamic spider charts, lets you customize force levels and swap in your own data, requires no macros, and exports clean slides for rapid decision-making.

Customers Bargaining Power

Large enterprise customers

Banks, asset managers and public companies buy at scale and run competitive RFPs, with procurement teams negotiating aggressively; Gartner 2024 finds RFP-driven sourcing often yields 5–15% cost savings. Volume and reference-client value amplify bargaining power, driving deeper discounts on per-user and per-deal pricing. Multi-year contracts frequently trade lower rates for revenue visibility and retention, stabilizing lifetime value despite initial concessions.

High switching costs, but not absolute

Workflow embedding via templates and integrations makes switching from DFIN costly, as customers migrate entrenched processes and automated filings. Data residency requirements and immutable audit trails in 2024 amplify migration complexity and legal risk for clients. Standardized reporting formats permit eventual transition, so DFIN must reinforce stickiness through ecosystem lock-in and superior support.

Price sensitivity and bundling

Clients increasingly demand bundled savings across reporting, GRC, and communications—58% of enterprise buyers in 2024 favored integrated suites to lower vendor count and costs. Transparent competitor pricing has intensified price pressure, compressing average deal ASPs by mid-single digits. Value-based pricing tied to measurable risk reduction can protect margins, while deeper cross-sell raises perceived total cost of ownership and improves retention.

Regulatory deadlines increase leverage

Hard filing dates such as the SEC 10-K 60-day (accelerated) and 90-day (large accelerated) deadlines put delivery risk squarely on vendors, letting buyers demand penalties or service credits for misses; operational exposure increases customer leverage in SLAs, while consistent on-time performance by DFIN can rebalance negotiations.

- Buyers leverage penalties/service credits

In‑house build alternatives

Larger institutions increasingly evaluate in-house builds with legal and compliance teams as a negotiating lever; 2024 surveys show this is common among enterprise finance buyers. Build options anchor feature and price discussions, but total lifecycle costs, upkeep, and regulatory audits often make buying more cost-effective. DFIN must emphasize faster deployment, stronger assurance, and superior auditability to counter build arguments.

- In‑house as leverage

- Anchors negotiations

- Lifecycle cost disadvantage for build

- DFIN: speed, assurance, auditability

RFPs deliver 5-15% savings as 58% prefer suites; ASPs compress, switching costs rise

Banks, asset managers and public firms wield strong price leverage via RFPs, with Gartner 2024 reporting 5–15% cost savings on RFP-driven sourcing. 58% of enterprise buyers in 2024 prefer integrated suites, increasing bundle demands while transparent competitor pricing compresses ASPs by mid-single digits. Regulatory deadlines (SEC 60/90 days) and penalties boost buyer leverage but DFIN’s on-time record and integrations raise switching costs.

| Metric | 2024 Value |

|---|---|

| RFP savings (Gartner) | 5–15% |

| Prefer integrated suites | 58% |

| ASP compression | mid-single digits |

Full Version Awaits

DFIN Porter's Five Forces Analysis

This preview displays the exact DFIN Porter's Five Forces Analysis you'll receive after purchase—no mockups, no placeholders. The file is fully formatted, professionally written, and ready for immediate download and use. What you see here is the final deliverable, identical to the document delivered upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

DFIN faces nuanced competitive pressures—from concentrated buyers to evolving substitute technologies—that shape margins and strategic choices; this snapshot highlights key tension points and opportunity areas. For investors and strategists, understanding these forces is critical to positioning and risk management. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to DFIN.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

DFIN relies on major cloud providers for scalable, secure infrastructure; top three hyperscalers (AWS 33%, Azure 23%, GCP 11% in 2024) control ~67% of the market, enabling pricing and contractual leverage. Multi-cloud designs and long-term contracts temper that power, but stringent performance SLAs and SEC/SOX compliance needs materially constrain switching and raise migration costs.

Niche regulatory data providers

Specialized taxonomy, regulatory content, and niche market data are sourced from a limited pool, giving these suppliers disproportionate bargaining power over pricing and access. Scarcity enables leverage on contract terms, while DFIN can mitigate risk through content partnerships and building internal curation capabilities. High accuracy and timeliness requirements, however, constrain substitution and force reliance on trusted providers.

Specialized compliance talent

Subject-matter experts and certified engineers are critical inputs, and tight 2024 labor markets—ManpowerGroup reporting 69% of employers facing talent shortages—drive wage pressure and attrition risk.

DFIN offsets this with training pipelines and global delivery hubs to scale capacity, but project timing and quality still hinge on securing scarce expertise.

Third‑party software and security tools

DFIN integrates entitlement, encryption, and monitoring from select vendors, and 2024 market dynamics—with enterprise security spend exceeding $180B—mean certification alignment (SOC 2, ISO 27001) materially narrows viable suppliers, increasing supplier power via bundled pricing and lock‑in; open standards and modular architecture preserve flexibility and reduce switching costs.

- Certs: SOC 2/ISO 27001

- Risk: bundled pricing, lock‑in

- Mitigation: open standards, modular design

Print and communications vendors

For DFIN, print and logistics partners remain critical for shareholder communications and regulated mailings; U.S. commercial printing revenue was roughly $64 billion in 2024, keeping supplier capacity central to service continuity. Peak filing seasons can push lead times and spot pricing up 10–25%, shifting bargaining power to suppliers. Maintaining multi-vendor rosters and improved demand forecasting mitigates risk, while gradual digital adoption (annual e-delivery growth ~6% in 2024) reduces long-term print dependence.

- Supplier concentration: medium — capacity spikes boost leverage

- Cost sensitivity: high — peak premiums ~10–25%

- Mitigants: multi-vendor rosters, forecasting

- Trend: digital adoption up ~6% in 2024, lowering print reliance

Supplier squeeze: hyperscaler concentration 33%/23%/11%, talent 69%

DFIN faces concentrated supplier power: hyperscalers (AWS 33%/Azure 23%/GCP 11% in 2024) and niche content providers constrain pricing and switching. Talent shortages (ManpowerGroup 69% in 2024) and security certification needs (enterprise security spend >$180B) increase leverage. Print capacity peaks (US commercial printing ~$64B; peak premiums 10–25%) further tilt power to suppliers.

| Metric | 2024 Value |

|---|---|

| Hyperscaler share | AWS 33% / Azure 23% / GCP 11% |

| Security spend | > $180B |

| Talent shortage | 69% |

| US printing rev | $64B |

| E-delivery growth | ~6% |

What is included in the product

Uncovers competitive drivers, buyer and supplier power, substitutes, and entry threats specific to DFIN, combining industry data and strategic commentary to assess pricing power and market defenses; fully editable Word format for investor decks, business plans, or internal strategy.

A concise, one-sheet DFIN Porter's Five Forces tool that visualizes strategic pressure with dynamic spider charts, lets you customize force levels and swap in your own data, requires no macros, and exports clean slides for rapid decision-making.

Customers Bargaining Power

Large enterprise customers

Banks, asset managers and public companies buy at scale and run competitive RFPs, with procurement teams negotiating aggressively; Gartner 2024 finds RFP-driven sourcing often yields 5–15% cost savings. Volume and reference-client value amplify bargaining power, driving deeper discounts on per-user and per-deal pricing. Multi-year contracts frequently trade lower rates for revenue visibility and retention, stabilizing lifetime value despite initial concessions.

High switching costs, but not absolute

Workflow embedding via templates and integrations makes switching from DFIN costly, as customers migrate entrenched processes and automated filings. Data residency requirements and immutable audit trails in 2024 amplify migration complexity and legal risk for clients. Standardized reporting formats permit eventual transition, so DFIN must reinforce stickiness through ecosystem lock-in and superior support.

Price sensitivity and bundling

Clients increasingly demand bundled savings across reporting, GRC, and communications—58% of enterprise buyers in 2024 favored integrated suites to lower vendor count and costs. Transparent competitor pricing has intensified price pressure, compressing average deal ASPs by mid-single digits. Value-based pricing tied to measurable risk reduction can protect margins, while deeper cross-sell raises perceived total cost of ownership and improves retention.

Regulatory deadlines increase leverage

Hard filing dates such as the SEC 10-K 60-day (accelerated) and 90-day (large accelerated) deadlines put delivery risk squarely on vendors, letting buyers demand penalties or service credits for misses; operational exposure increases customer leverage in SLAs, while consistent on-time performance by DFIN can rebalance negotiations.

- Buyers leverage penalties/service credits

In‑house build alternatives

Larger institutions increasingly evaluate in-house builds with legal and compliance teams as a negotiating lever; 2024 surveys show this is common among enterprise finance buyers. Build options anchor feature and price discussions, but total lifecycle costs, upkeep, and regulatory audits often make buying more cost-effective. DFIN must emphasize faster deployment, stronger assurance, and superior auditability to counter build arguments.

- In‑house as leverage

- Anchors negotiations

- Lifecycle cost disadvantage for build

- DFIN: speed, assurance, auditability

RFPs deliver 5-15% savings as 58% prefer suites; ASPs compress, switching costs rise

Banks, asset managers and public firms wield strong price leverage via RFPs, with Gartner 2024 reporting 5–15% cost savings on RFP-driven sourcing. 58% of enterprise buyers in 2024 prefer integrated suites, increasing bundle demands while transparent competitor pricing compresses ASPs by mid-single digits. Regulatory deadlines (SEC 60/90 days) and penalties boost buyer leverage but DFIN’s on-time record and integrations raise switching costs.

| Metric | 2024 Value |

|---|---|

| RFP savings (Gartner) | 5–15% |

| Prefer integrated suites | 58% |

| ASP compression | mid-single digits |

Full Version Awaits

DFIN Porter's Five Forces Analysis

This preview displays the exact DFIN Porter's Five Forces Analysis you'll receive after purchase—no mockups, no placeholders. The file is fully formatted, professionally written, and ready for immediate download and use. What you see here is the final deliverable, identical to the document delivered upon payment.