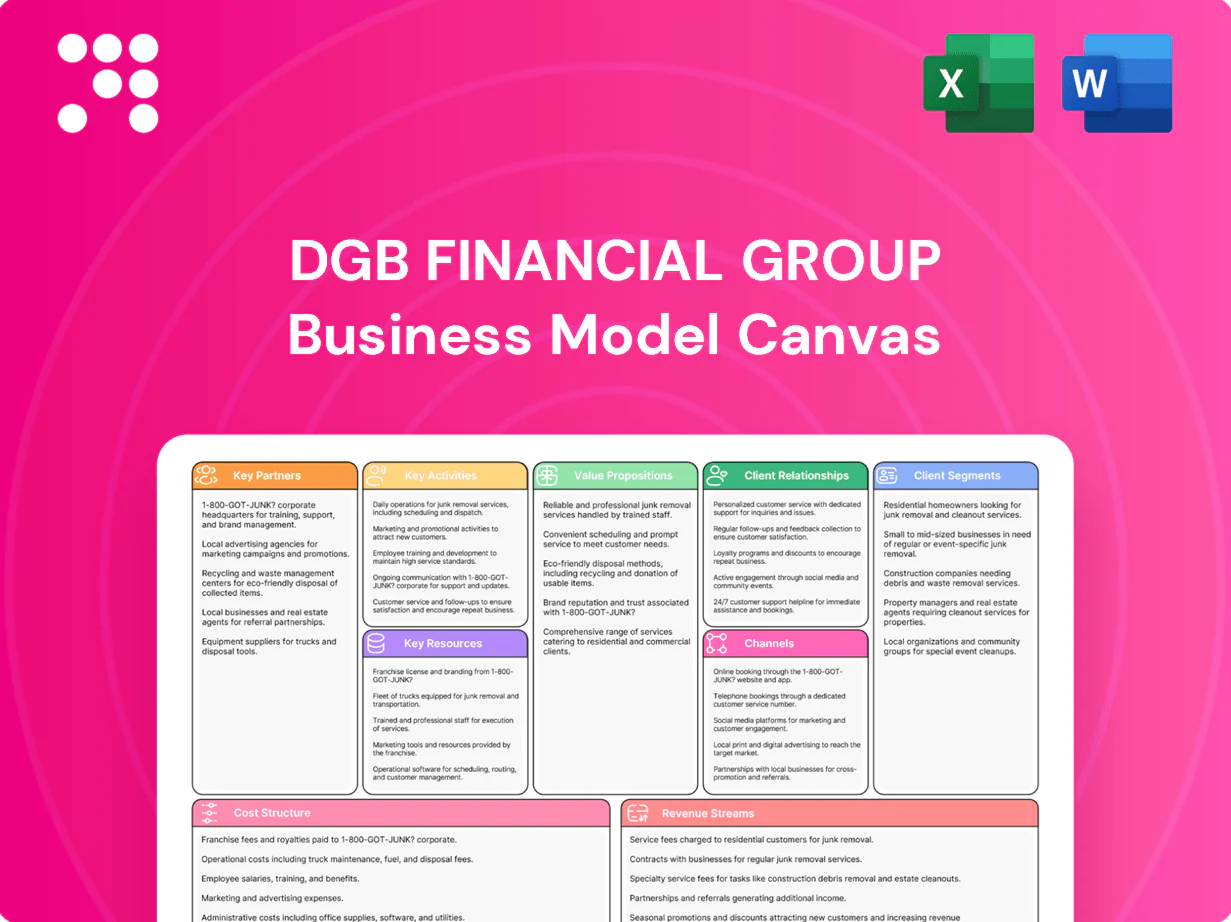

DGB Financial Group Business Model Canvas

Strategic Business Model Canvas: concise value, scale, and defense insights for financial firms

Unlock the strategic blueprint of DGB Financial Group with our concise Business Model Canvas—three to five-sentence insights into how it creates value, scales profitably, and defends market position. Perfect for investors, consultants, and founders seeking actionable analysis; purchase the full, editable Canvas to access detailed building blocks, financial implications, and ready-to-use templates for strategic planning.

Partnerships

Local governments and public institutions

Partnerships with Daegu (pop. ~2.4 million) and Gyeongbuk (pop. ~2.6 million) municipal bodies enable payroll, tax collection, and public project financing flows that channel stable fee and deposit volumes to DGB. They strengthen DGB’s role in regional development and expand access to public-sector clients across major city and provincial budgets. Co-branded initiatives deepen trust and help build predictable deposit bases. These ties support ESG and community programs aligned with local development goals.

Fintechs and payment networks

Alliances with fintechs, card schemes and open-banking platforms accelerate DGB’s digital product rollout by enabling API-driven onboarding, payments and lending workflows that cut processing times and friction. Co-development with partners reduces time-to-market and tech costs through shared platforms and cloud-based stacks. These partnerships help capture younger, digital-first customers—over 50% of neobank users were under 35 in 2024—boosting customer acquisition and fee income.

Global correspondent banks

Global correspondent banks enable DGB to support trade finance, remittances and cross-border settlements, boosting international operations and access to FX liquidity; global remittances totaled roughly $630 billion in 2023–24. Structured correspondent partnerships improve pricing and service reliability, reducing settlement times and counterparty risk. This strengthens DGB’s value proposition to exporters and importers by enabling smoother foreign currency flows and market intelligence.

Insurers and asset managers within the group

Intra-group synergies enable bancassurance, funds distribution and holistic wealth offerings; shared data and joint campaigns raised cross-sell rates in 2024, while unified risk governance supports compliant product design, delivering a one-stop financial experience for customers.

- Partners: insurers, asset managers, bancassurance

- Benefit: higher cross-sell, integrated AUM servicing

- Governance: unified risk & compliance

Technology vendors and cybersecurity firms

Core banking, cloud, and AI vendors (supporting platforms after 2024 cloud market ~$620B) underpin DGB Financial Group’s resilience and scalability by enabling real-time processing and elastic capacity.

Cyber partners (cybersecurity spending >$200B in 2024) bolster threat detection, fraud prevention, and regulatory alignment through managed services and analytics.

Joint incident response capabilities reduce downtime, protecting customer trust and operational continuity reflected in lower MTTR and regulatory fines risk.

- core-banking

- cloud-infrastructure

- ai-partners

- cybersecurity

- incident-response

Payroll/tax partnerships stabilize deposits from 5.0M residents

Key partnerships with Daegu (2.4M) and Gyeongbuk (2.6M) secure payroll/tax flows from ~5.0M residents, stabilizing deposits and fee income. Fintech and card alliances speed digital onboarding—>50% of neobank users were under 35 in 2024—boosting acquisition. Cloud/AI and cyber partners (cloud market ~$620B; cybersecurity spend >$200B in 2024) ensure scalable, secure delivery; correspondent banks support remittances (~$630B 2023–24).

| Partner | Role | 2024 Metric |

|---|---|---|

| Daegu/Gyeongbuk | Payroll/tax flows | Population ~5.0M |

| Fintechs/cards | Digital onboarding | >50% users <35 |

| Cloud/AI vendors | Scalability | Cloud market ~$620B |

| Cybersecurity | Threat protection | Spend >$200B |

| Correspondent banks | Trade/remittances | Remittances ~$630B |

What is included in the product

A comprehensive Business Model Canvas for DGB Financial Group aligned to its banking and financial services strategy, covering customer segments, channels, and value propositions across the 9 BMC blocks. Includes narrative insights, competitive advantages, linked SWOT, and a polished format ideal for investor presentations, strategic planning, and validation of growth initiatives.

High-level view of DGB Financial Group’s business model with editable cells, relieving the pain of fragmented strategy by consolidating value propositions, channels, revenue streams and cost structure on a single, shareable page for fast alignment and decision-making.

Activities

Retail and corporate banking operations

Deposits, loans, payments and cash management form DGB’s daily engine of value creation, funding core lending and fee income while supporting liquidity across Daegu and regional branches in 2024. Rigorous credit underwriting and ongoing portfolio monitoring aim to optimize risk-adjusted returns and contain NPLs amid a tightening macro backdrop. SME and mid-market services anchor regional growth, concentrating relationship banking and working-capital solutions. Operational excellence targets improved cost-to-income dynamics through digitization and process standardization.

Securities brokerage and investment banking

Securities brokerage executes equities, bonds and derivatives for individual and institutional clients, while investment banking handles underwriting, M&A advisory and structured financing mandates. Dedicated research teams support client decisions and originate products across markets. Fee income from brokerage and IB activities diversifies revenue beyond net interest margins.

Asset management and wealth advisory

Mutual funds, discretionary mandates and retirement products are tailored to conservative, balanced and aggressive risk profiles, supporting DGB’s AUM-driven growth (AUM +4.1% in 2024). Financial planning and tax-efficient strategies deepen client relationships and cut after-tax drag on returns. Model portfolios leverage proprietary research and risk tools to standardize outcomes and scale advice. Cross-selling across banking and insurance lifts client lifetime value and retention.

Insurance distribution and underwriting

Bancassurance and group policies expand DGB Financial Group’s protection mix, leveraging branch and digital channels to increase penetration. Underwriting discipline and efficient claims management preserve profitability through risk selection and expense control. Data-driven pricing and telematics-enhanced models improve loss ratios while integrated purchase-to-service journeys reduce friction and lift persistency.

- Bancassurance expansion

- Underwriting & claims

- Data-driven pricing

- Integrated customer journeys

Digital transformation and risk/compliance

Digital transformation at DGB in 2024 prioritizes mobile-first experiences, AI-driven credit models and automation to elevate service while cybersecurity, AML/KYC and regulatory reporting maintain compliance; data governance and analytics enable personalized offers and continuous improvement supports domestic and overseas expansion.

- mobile-first

- AI credit models

- automation

- cybersecurity

- AML/KYC

- regulatory reporting

- data governance

- continuous improvement

SME digitization, diversified fees and liquidity drive growth; AUM +4.1%

Deposits, loans, payments and cash management fund lending and liquidity for regional branches, with SME relationship banking and digitization driving efficiency. Brokerage, IB and AUM products diversify fees; AUM +4.1% in 2024. Bancassurance, underwriting discipline and AI credit models support risk-adjusted growth.

| Metric | 2024 |

|---|---|

| AUM growth | +4.1% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual DGB Financial Group Business Model Canvas, not a mockup. When you purchase, you'll receive this exact file with all sections included, formatted and ready to edit in Word and Excel. No placeholders or hidden content—what you see is what you'll download and use immediately.

Strategic Business Model Canvas: concise value, scale, and defense insights for financial firms

Unlock the strategic blueprint of DGB Financial Group with our concise Business Model Canvas—three to five-sentence insights into how it creates value, scales profitably, and defends market position. Perfect for investors, consultants, and founders seeking actionable analysis; purchase the full, editable Canvas to access detailed building blocks, financial implications, and ready-to-use templates for strategic planning.

Partnerships

Local governments and public institutions

Partnerships with Daegu (pop. ~2.4 million) and Gyeongbuk (pop. ~2.6 million) municipal bodies enable payroll, tax collection, and public project financing flows that channel stable fee and deposit volumes to DGB. They strengthen DGB’s role in regional development and expand access to public-sector clients across major city and provincial budgets. Co-branded initiatives deepen trust and help build predictable deposit bases. These ties support ESG and community programs aligned with local development goals.

Fintechs and payment networks

Alliances with fintechs, card schemes and open-banking platforms accelerate DGB’s digital product rollout by enabling API-driven onboarding, payments and lending workflows that cut processing times and friction. Co-development with partners reduces time-to-market and tech costs through shared platforms and cloud-based stacks. These partnerships help capture younger, digital-first customers—over 50% of neobank users were under 35 in 2024—boosting customer acquisition and fee income.

Global correspondent banks

Global correspondent banks enable DGB to support trade finance, remittances and cross-border settlements, boosting international operations and access to FX liquidity; global remittances totaled roughly $630 billion in 2023–24. Structured correspondent partnerships improve pricing and service reliability, reducing settlement times and counterparty risk. This strengthens DGB’s value proposition to exporters and importers by enabling smoother foreign currency flows and market intelligence.

Insurers and asset managers within the group

Intra-group synergies enable bancassurance, funds distribution and holistic wealth offerings; shared data and joint campaigns raised cross-sell rates in 2024, while unified risk governance supports compliant product design, delivering a one-stop financial experience for customers.

- Partners: insurers, asset managers, bancassurance

- Benefit: higher cross-sell, integrated AUM servicing

- Governance: unified risk & compliance

Technology vendors and cybersecurity firms

Core banking, cloud, and AI vendors (supporting platforms after 2024 cloud market ~$620B) underpin DGB Financial Group’s resilience and scalability by enabling real-time processing and elastic capacity.

Cyber partners (cybersecurity spending >$200B in 2024) bolster threat detection, fraud prevention, and regulatory alignment through managed services and analytics.

Joint incident response capabilities reduce downtime, protecting customer trust and operational continuity reflected in lower MTTR and regulatory fines risk.

- core-banking

- cloud-infrastructure

- ai-partners

- cybersecurity

- incident-response

Payroll/tax partnerships stabilize deposits from 5.0M residents

Key partnerships with Daegu (2.4M) and Gyeongbuk (2.6M) secure payroll/tax flows from ~5.0M residents, stabilizing deposits and fee income. Fintech and card alliances speed digital onboarding—>50% of neobank users were under 35 in 2024—boosting acquisition. Cloud/AI and cyber partners (cloud market ~$620B; cybersecurity spend >$200B in 2024) ensure scalable, secure delivery; correspondent banks support remittances (~$630B 2023–24).

| Partner | Role | 2024 Metric |

|---|---|---|

| Daegu/Gyeongbuk | Payroll/tax flows | Population ~5.0M |

| Fintechs/cards | Digital onboarding | >50% users <35 |

| Cloud/AI vendors | Scalability | Cloud market ~$620B |

| Cybersecurity | Threat protection | Spend >$200B |

| Correspondent banks | Trade/remittances | Remittances ~$630B |

What is included in the product

A comprehensive Business Model Canvas for DGB Financial Group aligned to its banking and financial services strategy, covering customer segments, channels, and value propositions across the 9 BMC blocks. Includes narrative insights, competitive advantages, linked SWOT, and a polished format ideal for investor presentations, strategic planning, and validation of growth initiatives.

High-level view of DGB Financial Group’s business model with editable cells, relieving the pain of fragmented strategy by consolidating value propositions, channels, revenue streams and cost structure on a single, shareable page for fast alignment and decision-making.

Activities

Retail and corporate banking operations

Deposits, loans, payments and cash management form DGB’s daily engine of value creation, funding core lending and fee income while supporting liquidity across Daegu and regional branches in 2024. Rigorous credit underwriting and ongoing portfolio monitoring aim to optimize risk-adjusted returns and contain NPLs amid a tightening macro backdrop. SME and mid-market services anchor regional growth, concentrating relationship banking and working-capital solutions. Operational excellence targets improved cost-to-income dynamics through digitization and process standardization.

Securities brokerage and investment banking

Securities brokerage executes equities, bonds and derivatives for individual and institutional clients, while investment banking handles underwriting, M&A advisory and structured financing mandates. Dedicated research teams support client decisions and originate products across markets. Fee income from brokerage and IB activities diversifies revenue beyond net interest margins.

Asset management and wealth advisory

Mutual funds, discretionary mandates and retirement products are tailored to conservative, balanced and aggressive risk profiles, supporting DGB’s AUM-driven growth (AUM +4.1% in 2024). Financial planning and tax-efficient strategies deepen client relationships and cut after-tax drag on returns. Model portfolios leverage proprietary research and risk tools to standardize outcomes and scale advice. Cross-selling across banking and insurance lifts client lifetime value and retention.

Insurance distribution and underwriting

Bancassurance and group policies expand DGB Financial Group’s protection mix, leveraging branch and digital channels to increase penetration. Underwriting discipline and efficient claims management preserve profitability through risk selection and expense control. Data-driven pricing and telematics-enhanced models improve loss ratios while integrated purchase-to-service journeys reduce friction and lift persistency.

- Bancassurance expansion

- Underwriting & claims

- Data-driven pricing

- Integrated customer journeys

Digital transformation and risk/compliance

Digital transformation at DGB in 2024 prioritizes mobile-first experiences, AI-driven credit models and automation to elevate service while cybersecurity, AML/KYC and regulatory reporting maintain compliance; data governance and analytics enable personalized offers and continuous improvement supports domestic and overseas expansion.

- mobile-first

- AI credit models

- automation

- cybersecurity

- AML/KYC

- regulatory reporting

- data governance

- continuous improvement

SME digitization, diversified fees and liquidity drive growth; AUM +4.1%

Deposits, loans, payments and cash management fund lending and liquidity for regional branches, with SME relationship banking and digitization driving efficiency. Brokerage, IB and AUM products diversify fees; AUM +4.1% in 2024. Bancassurance, underwriting discipline and AI credit models support risk-adjusted growth.

| Metric | 2024 |

|---|---|

| AUM growth | +4.1% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual DGB Financial Group Business Model Canvas, not a mockup. When you purchase, you'll receive this exact file with all sections included, formatted and ready to edit in Word and Excel. No placeholders or hidden content—what you see is what you'll download and use immediately.

Description

Strategic Business Model Canvas: concise value, scale, and defense insights for financial firms

Unlock the strategic blueprint of DGB Financial Group with our concise Business Model Canvas—three to five-sentence insights into how it creates value, scales profitably, and defends market position. Perfect for investors, consultants, and founders seeking actionable analysis; purchase the full, editable Canvas to access detailed building blocks, financial implications, and ready-to-use templates for strategic planning.

Partnerships

Local governments and public institutions

Partnerships with Daegu (pop. ~2.4 million) and Gyeongbuk (pop. ~2.6 million) municipal bodies enable payroll, tax collection, and public project financing flows that channel stable fee and deposit volumes to DGB. They strengthen DGB’s role in regional development and expand access to public-sector clients across major city and provincial budgets. Co-branded initiatives deepen trust and help build predictable deposit bases. These ties support ESG and community programs aligned with local development goals.

Fintechs and payment networks

Alliances with fintechs, card schemes and open-banking platforms accelerate DGB’s digital product rollout by enabling API-driven onboarding, payments and lending workflows that cut processing times and friction. Co-development with partners reduces time-to-market and tech costs through shared platforms and cloud-based stacks. These partnerships help capture younger, digital-first customers—over 50% of neobank users were under 35 in 2024—boosting customer acquisition and fee income.

Global correspondent banks

Global correspondent banks enable DGB to support trade finance, remittances and cross-border settlements, boosting international operations and access to FX liquidity; global remittances totaled roughly $630 billion in 2023–24. Structured correspondent partnerships improve pricing and service reliability, reducing settlement times and counterparty risk. This strengthens DGB’s value proposition to exporters and importers by enabling smoother foreign currency flows and market intelligence.

Insurers and asset managers within the group

Intra-group synergies enable bancassurance, funds distribution and holistic wealth offerings; shared data and joint campaigns raised cross-sell rates in 2024, while unified risk governance supports compliant product design, delivering a one-stop financial experience for customers.

- Partners: insurers, asset managers, bancassurance

- Benefit: higher cross-sell, integrated AUM servicing

- Governance: unified risk & compliance

Technology vendors and cybersecurity firms

Core banking, cloud, and AI vendors (supporting platforms after 2024 cloud market ~$620B) underpin DGB Financial Group’s resilience and scalability by enabling real-time processing and elastic capacity.

Cyber partners (cybersecurity spending >$200B in 2024) bolster threat detection, fraud prevention, and regulatory alignment through managed services and analytics.

Joint incident response capabilities reduce downtime, protecting customer trust and operational continuity reflected in lower MTTR and regulatory fines risk.

- core-banking

- cloud-infrastructure

- ai-partners

- cybersecurity

- incident-response

Payroll/tax partnerships stabilize deposits from 5.0M residents

Key partnerships with Daegu (2.4M) and Gyeongbuk (2.6M) secure payroll/tax flows from ~5.0M residents, stabilizing deposits and fee income. Fintech and card alliances speed digital onboarding—>50% of neobank users were under 35 in 2024—boosting acquisition. Cloud/AI and cyber partners (cloud market ~$620B; cybersecurity spend >$200B in 2024) ensure scalable, secure delivery; correspondent banks support remittances (~$630B 2023–24).

| Partner | Role | 2024 Metric |

|---|---|---|

| Daegu/Gyeongbuk | Payroll/tax flows | Population ~5.0M |

| Fintechs/cards | Digital onboarding | >50% users <35 |

| Cloud/AI vendors | Scalability | Cloud market ~$620B |

| Cybersecurity | Threat protection | Spend >$200B |

| Correspondent banks | Trade/remittances | Remittances ~$630B |

What is included in the product

A comprehensive Business Model Canvas for DGB Financial Group aligned to its banking and financial services strategy, covering customer segments, channels, and value propositions across the 9 BMC blocks. Includes narrative insights, competitive advantages, linked SWOT, and a polished format ideal for investor presentations, strategic planning, and validation of growth initiatives.

High-level view of DGB Financial Group’s business model with editable cells, relieving the pain of fragmented strategy by consolidating value propositions, channels, revenue streams and cost structure on a single, shareable page for fast alignment and decision-making.

Activities

Retail and corporate banking operations

Deposits, loans, payments and cash management form DGB’s daily engine of value creation, funding core lending and fee income while supporting liquidity across Daegu and regional branches in 2024. Rigorous credit underwriting and ongoing portfolio monitoring aim to optimize risk-adjusted returns and contain NPLs amid a tightening macro backdrop. SME and mid-market services anchor regional growth, concentrating relationship banking and working-capital solutions. Operational excellence targets improved cost-to-income dynamics through digitization and process standardization.

Securities brokerage and investment banking

Securities brokerage executes equities, bonds and derivatives for individual and institutional clients, while investment banking handles underwriting, M&A advisory and structured financing mandates. Dedicated research teams support client decisions and originate products across markets. Fee income from brokerage and IB activities diversifies revenue beyond net interest margins.

Asset management and wealth advisory

Mutual funds, discretionary mandates and retirement products are tailored to conservative, balanced and aggressive risk profiles, supporting DGB’s AUM-driven growth (AUM +4.1% in 2024). Financial planning and tax-efficient strategies deepen client relationships and cut after-tax drag on returns. Model portfolios leverage proprietary research and risk tools to standardize outcomes and scale advice. Cross-selling across banking and insurance lifts client lifetime value and retention.

Insurance distribution and underwriting

Bancassurance and group policies expand DGB Financial Group’s protection mix, leveraging branch and digital channels to increase penetration. Underwriting discipline and efficient claims management preserve profitability through risk selection and expense control. Data-driven pricing and telematics-enhanced models improve loss ratios while integrated purchase-to-service journeys reduce friction and lift persistency.

- Bancassurance expansion

- Underwriting & claims

- Data-driven pricing

- Integrated customer journeys

Digital transformation and risk/compliance

Digital transformation at DGB in 2024 prioritizes mobile-first experiences, AI-driven credit models and automation to elevate service while cybersecurity, AML/KYC and regulatory reporting maintain compliance; data governance and analytics enable personalized offers and continuous improvement supports domestic and overseas expansion.

- mobile-first

- AI credit models

- automation

- cybersecurity

- AML/KYC

- regulatory reporting

- data governance

- continuous improvement

SME digitization, diversified fees and liquidity drive growth; AUM +4.1%

Deposits, loans, payments and cash management fund lending and liquidity for regional branches, with SME relationship banking and digitization driving efficiency. Brokerage, IB and AUM products diversify fees; AUM +4.1% in 2024. Bancassurance, underwriting discipline and AI credit models support risk-adjusted growth.

| Metric | 2024 |

|---|---|

| AUM growth | +4.1% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual DGB Financial Group Business Model Canvas, not a mockup. When you purchase, you'll receive this exact file with all sections included, formatted and ready to edit in Word and Excel. No placeholders or hidden content—what you see is what you'll download and use immediately.