DHI Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

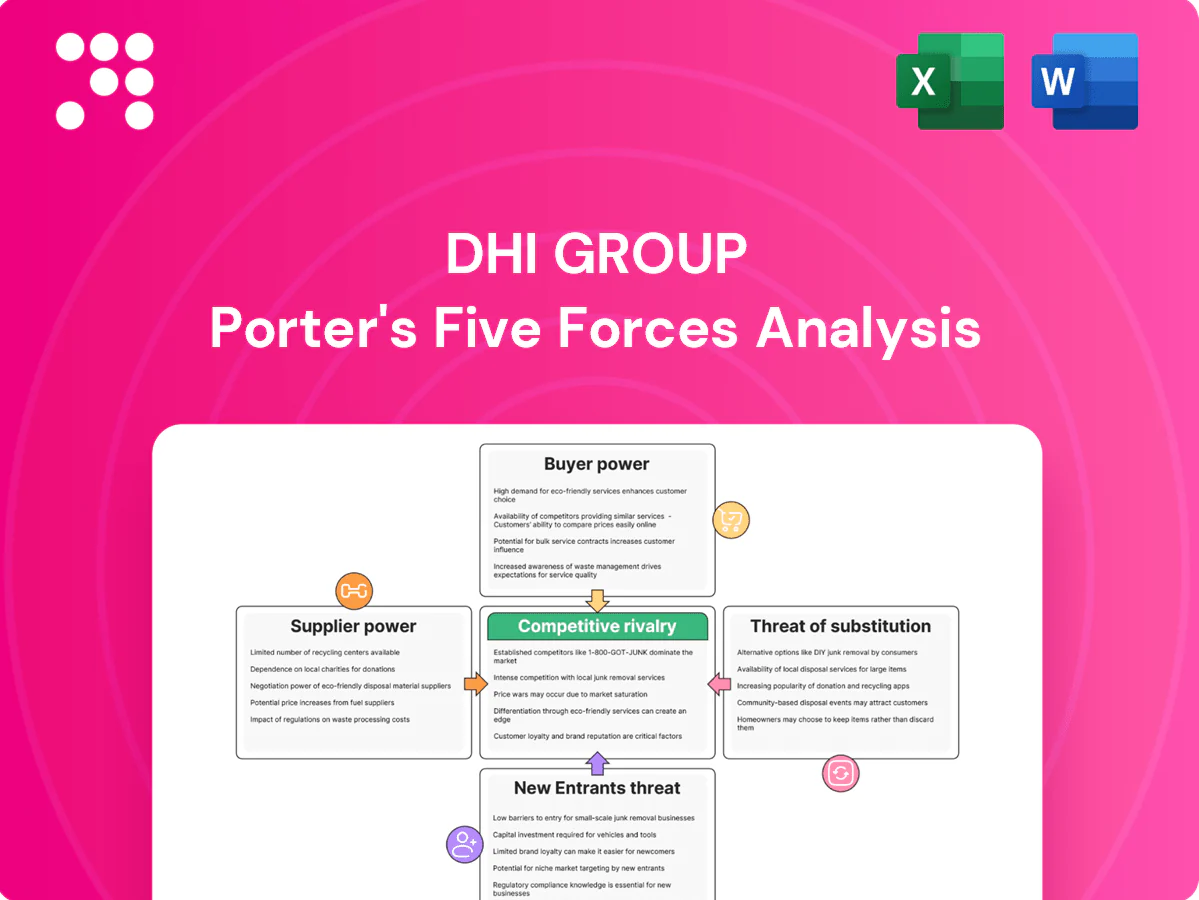

DHI Group faces moderate buyer power and niche supplier relationships, while entrant threats are tempered by brand specialization and data assets. Competitive rivalry is intense among recruitment platforms and substitute job-search tools, putting pressure on margins and innovation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore DHI Group’s strategic risks and market opportunities in detail.

Suppliers Bargaining Power

Concentrated cloud and data vendors

Dependence on a few hyperscale clouds concentrates supplier power—AWS (≈34% global IaaS/PaaS market), Microsoft Azure (≈23%) and Google Cloud (≈11%) in 2024, leaving DHI exposed to pricing and outage risk. Switching infrastructure is costly and risks uptime and search relevance, making rapid migration impractical. Long-term contracts and multi-cloud strategies can reduce leverage. Supplier outages or price moves directly pressure margins and gross margin stability.

Traffic acquisition and ad platforms

Performance marketing channels and app stores effectively gate access to candidate and employer audiences, with Google commanding about 92% of global search and Android ~71% device share (StatCounter 2024). Algorithm changes or pricing hikes by these platforms can raise DHI’s customer acquisition costs and margins. Heavy SEO reliance leaves DHI exposed to frequent Google core updates. Diversifying paid channels and building owned communities reduces this supplier concentration risk.

Specialized verification and compliance services

For security-cleared roles third-party screening and verification vendors are highly specialized and fewer in number, servicing an estimated cleared population of about 2.6 million in the U.S. in 2024, which limits substitutability and grants suppliers measurable bargaining power. Deep technical and systems integration with talent platforms raises switching costs and operational risk. Long-term volume commitments and strategic partnerships are common levers DHI can use to negotiate better terms. Strong compliance regimes (FISMA, DoD JPAS legacy constraints) further constrain buyer options.

Software tooling and AI models

Third-party search, matching, analytics and AI model providers such as OpenAI, Anthropic and Google materially influence DHI product quality and cost; 2024 supplier terms and quota limits shaped integration choices. Rapid pricing and usage-policy shifts among major model vendors in 2024 altered unit economics, while proprietary model development cuts dependence but requires CAPEX and engineering spend. Hybrid build-buy approaches dilute supplier leverage and preserve flexibility.

- Third-party dominance: OpenAI, Anthropic, Google

- 2024 vendor policy shifts impact unit economics

- Proprietary models reduce reliance but raise CAPEX

- Hybrid build-buy lowers supplier bargaining power

Payment processors and fraud tools

Payments, billing, and anti-fraud vendors are largely standardized but still extract meaningful take rates; card processing fees commonly range from 1.5%–3.5% plus $0.20–$0.30 per transaction, and many fraud tools charge percentage or SaaS fees. Chargeback rules and compliance mandates (PCI, PSD2/3-style requirements) create non-negotiable liabilities for merchants. Multi-processor routing provides redundancy and pricing flexibility, so supplier power is moderate due to available alternatives.

- processing-fees: 1.5%–3.5% + $0.20–$0.30 per tx

- chargebacks/compliance: non-negotiable liability

- routing: enables cost arbitration and redundancy

Cloud, search and AI vendor concentration threatens platform margins, uptime and CAC volatility

DHI faces concentrated cloud supplier risk (AWS ≈34%, Azure ≈23%, Google ≈11% IaaS/PaaS 2024), costly switching and outage exposure. Search/app gatekeepers (Google ~92% search, Android ~71% share 2024) raise CAC volatility. AI/model vendors (OpenAI, Anthropic, Google) and niche security screens further constrain bargaining without CAPEX for proprietary builds.

| Supplier | Key stat (2024) |

|---|---|

| Cloud | AWS34%/Azure23%/GCP11% |

| Search/App | Google92%/Android71% |

| Payments | 1.5%–3.5% + $0.20–$0.30 |

What is included in the product

Tailored Porter’s Five Forces analysis for DHI Group uncovers key drivers of competition, buyer and supplier power, and market entry risks specific to its niche recruiting platforms. It identifies substitutes, disruptive threats, and industry dynamics that shape pricing, profitability, and strategic positioning for investors and management.

A concise one-sheet Porter's Five Forces for DHI Group that instantly highlights competitive pressure and talent-market risks, ready to drop into decks for rapid decisions. Customize force levels or swap data to model scenarios—no macros, just clear visuals to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Employers and recruiters can multi-home

Corporate TA teams routinely multi-home across job boards, agencies and LinkedIn (930 million members in 2024), expanding switching options and driving sharper price sensitivity and tougher negotiation on enterprise contracts. Superior candidate quality and niche reach reduce discount pressure by delivering higher fill rates and time-to-hire improvements. Demonstrable ROI metrics—cost-per-hire and quality-of-hire—are decisive for retention.

Large enterprise buyers negotiate hard

Large enterprise buyers demand volume discounts, custom SLAs and integrations, using churn risk to press pricing and product-roadmap concessions; Gartner reported global IT spending at about $4.8 trillion in 2024, keeping enterprise buying power high. Multi-year contracts (commonly 3–5 years) stabilize revenue but often reduce margin via upfront discounts and committed services. Land-and-expand models require explicit KPIs and renewal-linked performance metrics to retain leverage.

SMBs are price sensitive and churn-prone

SMBs, which comprise 99.9% of US firms per the SBA, operate with tight budgets and episodic hiring cycles, making them highly price sensitive and churn-prone. They switch platforms rapidly when ROI is delayed, so self-serve packaging and transparent pricing increase comparability and accelerate selection. For DHI Group, maintaining low CAC and delivering quick time-to-value are essential to retain these customers.

Candidates exert indirect power via engagement

Candidates exert indirect power via engagement: job seekers rarely pay on DHI platforms but their participation drives liquidity, and poor UX or irrelevant matches push them to substitutes, eroding employer value; LinkedIn reached about 930 million members in 2024, underscoring candidate mobility. Brand trust, community features, and content keep talent engaged, while high-quality candidate density weakens employer bargaining power.

- job_seekers_free

- liquidity_drivers

- ux_churn_risk

- brand_trust_engagement

- candidate_density_weakens_employers

Data-driven procurement expectations

Buyers increasingly demand attribution, benchmarking, and pay-for-performance models, making opaque analytics a direct driver of discounting and reduced willingness to pay list prices; providing real-time dashboards and outcome guarantees neutralizes this leverage and preserves margins. Contracts now routinely embed performance clauses and KPIs, shifting negotiations from price to measurable outcomes.

- Attribution demands: buyers require clear ROI mapping

- Benchmarking: comparison data drives negotiation

- Pay-for-performance: ties fees to outcomes

- Dashboards/outcome guarantees: mitigate buyer power

- Performance clauses: becoming standard in contracts

Multi-homed buyers and candidate power squeeze pricing; UX-driven churn erodes employer leverage

Buyers multi-home across boards and LinkedIn (930 million members in 2024), raising switching options and price pressure. Large enterprises wield leverage via volume discounts and custom SLAs amid ~$4.8T global IT spend (2024), while US SMBs (99.9% of firms) are highly price sensitive. Candidates drive liquidity; poor UX increases churn and weakens employer purchasing power.

| Metric | 2024 Value |

|---|---|

| LinkedIn members | 930 million |

| Global IT spend | $4.8 trillion |

| US SMB share | 99.9% |

| Typical contract length | 3–5 years |

Preview the Actual Deliverable

DHI Group Porter's Five Forces Analysis

This preview shows the exact DHI Group Porter’s Five Forces analysis you'll receive—no placeholders or mockups. Once you purchase, you’ll get immediate access to this same fully formatted, professionally written document. It’s complete, ready for download and use in your decision-making or reports.

Go Beyond the Preview—Access the Full Strategic Report

DHI Group faces moderate buyer power and niche supplier relationships, while entrant threats are tempered by brand specialization and data assets. Competitive rivalry is intense among recruitment platforms and substitute job-search tools, putting pressure on margins and innovation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore DHI Group’s strategic risks and market opportunities in detail.

Suppliers Bargaining Power

Concentrated cloud and data vendors

Dependence on a few hyperscale clouds concentrates supplier power—AWS (≈34% global IaaS/PaaS market), Microsoft Azure (≈23%) and Google Cloud (≈11%) in 2024, leaving DHI exposed to pricing and outage risk. Switching infrastructure is costly and risks uptime and search relevance, making rapid migration impractical. Long-term contracts and multi-cloud strategies can reduce leverage. Supplier outages or price moves directly pressure margins and gross margin stability.

Traffic acquisition and ad platforms

Performance marketing channels and app stores effectively gate access to candidate and employer audiences, with Google commanding about 92% of global search and Android ~71% device share (StatCounter 2024). Algorithm changes or pricing hikes by these platforms can raise DHI’s customer acquisition costs and margins. Heavy SEO reliance leaves DHI exposed to frequent Google core updates. Diversifying paid channels and building owned communities reduces this supplier concentration risk.

Specialized verification and compliance services

For security-cleared roles third-party screening and verification vendors are highly specialized and fewer in number, servicing an estimated cleared population of about 2.6 million in the U.S. in 2024, which limits substitutability and grants suppliers measurable bargaining power. Deep technical and systems integration with talent platforms raises switching costs and operational risk. Long-term volume commitments and strategic partnerships are common levers DHI can use to negotiate better terms. Strong compliance regimes (FISMA, DoD JPAS legacy constraints) further constrain buyer options.

Software tooling and AI models

Third-party search, matching, analytics and AI model providers such as OpenAI, Anthropic and Google materially influence DHI product quality and cost; 2024 supplier terms and quota limits shaped integration choices. Rapid pricing and usage-policy shifts among major model vendors in 2024 altered unit economics, while proprietary model development cuts dependence but requires CAPEX and engineering spend. Hybrid build-buy approaches dilute supplier leverage and preserve flexibility.

- Third-party dominance: OpenAI, Anthropic, Google

- 2024 vendor policy shifts impact unit economics

- Proprietary models reduce reliance but raise CAPEX

- Hybrid build-buy lowers supplier bargaining power

Payment processors and fraud tools

Payments, billing, and anti-fraud vendors are largely standardized but still extract meaningful take rates; card processing fees commonly range from 1.5%–3.5% plus $0.20–$0.30 per transaction, and many fraud tools charge percentage or SaaS fees. Chargeback rules and compliance mandates (PCI, PSD2/3-style requirements) create non-negotiable liabilities for merchants. Multi-processor routing provides redundancy and pricing flexibility, so supplier power is moderate due to available alternatives.

- processing-fees: 1.5%–3.5% + $0.20–$0.30 per tx

- chargebacks/compliance: non-negotiable liability

- routing: enables cost arbitration and redundancy

Cloud, search and AI vendor concentration threatens platform margins, uptime and CAC volatility

DHI faces concentrated cloud supplier risk (AWS ≈34%, Azure ≈23%, Google ≈11% IaaS/PaaS 2024), costly switching and outage exposure. Search/app gatekeepers (Google ~92% search, Android ~71% share 2024) raise CAC volatility. AI/model vendors (OpenAI, Anthropic, Google) and niche security screens further constrain bargaining without CAPEX for proprietary builds.

| Supplier | Key stat (2024) |

|---|---|

| Cloud | AWS34%/Azure23%/GCP11% |

| Search/App | Google92%/Android71% |

| Payments | 1.5%–3.5% + $0.20–$0.30 |

What is included in the product

Tailored Porter’s Five Forces analysis for DHI Group uncovers key drivers of competition, buyer and supplier power, and market entry risks specific to its niche recruiting platforms. It identifies substitutes, disruptive threats, and industry dynamics that shape pricing, profitability, and strategic positioning for investors and management.

A concise one-sheet Porter's Five Forces for DHI Group that instantly highlights competitive pressure and talent-market risks, ready to drop into decks for rapid decisions. Customize force levels or swap data to model scenarios—no macros, just clear visuals to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Employers and recruiters can multi-home

Corporate TA teams routinely multi-home across job boards, agencies and LinkedIn (930 million members in 2024), expanding switching options and driving sharper price sensitivity and tougher negotiation on enterprise contracts. Superior candidate quality and niche reach reduce discount pressure by delivering higher fill rates and time-to-hire improvements. Demonstrable ROI metrics—cost-per-hire and quality-of-hire—are decisive for retention.

Large enterprise buyers negotiate hard

Large enterprise buyers demand volume discounts, custom SLAs and integrations, using churn risk to press pricing and product-roadmap concessions; Gartner reported global IT spending at about $4.8 trillion in 2024, keeping enterprise buying power high. Multi-year contracts (commonly 3–5 years) stabilize revenue but often reduce margin via upfront discounts and committed services. Land-and-expand models require explicit KPIs and renewal-linked performance metrics to retain leverage.

SMBs are price sensitive and churn-prone

SMBs, which comprise 99.9% of US firms per the SBA, operate with tight budgets and episodic hiring cycles, making them highly price sensitive and churn-prone. They switch platforms rapidly when ROI is delayed, so self-serve packaging and transparent pricing increase comparability and accelerate selection. For DHI Group, maintaining low CAC and delivering quick time-to-value are essential to retain these customers.

Candidates exert indirect power via engagement

Candidates exert indirect power via engagement: job seekers rarely pay on DHI platforms but their participation drives liquidity, and poor UX or irrelevant matches push them to substitutes, eroding employer value; LinkedIn reached about 930 million members in 2024, underscoring candidate mobility. Brand trust, community features, and content keep talent engaged, while high-quality candidate density weakens employer bargaining power.

- job_seekers_free

- liquidity_drivers

- ux_churn_risk

- brand_trust_engagement

- candidate_density_weakens_employers

Data-driven procurement expectations

Buyers increasingly demand attribution, benchmarking, and pay-for-performance models, making opaque analytics a direct driver of discounting and reduced willingness to pay list prices; providing real-time dashboards and outcome guarantees neutralizes this leverage and preserves margins. Contracts now routinely embed performance clauses and KPIs, shifting negotiations from price to measurable outcomes.

- Attribution demands: buyers require clear ROI mapping

- Benchmarking: comparison data drives negotiation

- Pay-for-performance: ties fees to outcomes

- Dashboards/outcome guarantees: mitigate buyer power

- Performance clauses: becoming standard in contracts

Multi-homed buyers and candidate power squeeze pricing; UX-driven churn erodes employer leverage

Buyers multi-home across boards and LinkedIn (930 million members in 2024), raising switching options and price pressure. Large enterprises wield leverage via volume discounts and custom SLAs amid ~$4.8T global IT spend (2024), while US SMBs (99.9% of firms) are highly price sensitive. Candidates drive liquidity; poor UX increases churn and weakens employer purchasing power.

| Metric | 2024 Value |

|---|---|

| LinkedIn members | 930 million |

| Global IT spend | $4.8 trillion |

| US SMB share | 99.9% |

| Typical contract length | 3–5 years |

Preview the Actual Deliverable

DHI Group Porter's Five Forces Analysis

This preview shows the exact DHI Group Porter’s Five Forces analysis you'll receive—no placeholders or mockups. Once you purchase, you’ll get immediate access to this same fully formatted, professionally written document. It’s complete, ready for download and use in your decision-making or reports.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

DHI Group faces moderate buyer power and niche supplier relationships, while entrant threats are tempered by brand specialization and data assets. Competitive rivalry is intense among recruitment platforms and substitute job-search tools, putting pressure on margins and innovation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore DHI Group’s strategic risks and market opportunities in detail.

Suppliers Bargaining Power

Concentrated cloud and data vendors

Dependence on a few hyperscale clouds concentrates supplier power—AWS (≈34% global IaaS/PaaS market), Microsoft Azure (≈23%) and Google Cloud (≈11%) in 2024, leaving DHI exposed to pricing and outage risk. Switching infrastructure is costly and risks uptime and search relevance, making rapid migration impractical. Long-term contracts and multi-cloud strategies can reduce leverage. Supplier outages or price moves directly pressure margins and gross margin stability.

Traffic acquisition and ad platforms

Performance marketing channels and app stores effectively gate access to candidate and employer audiences, with Google commanding about 92% of global search and Android ~71% device share (StatCounter 2024). Algorithm changes or pricing hikes by these platforms can raise DHI’s customer acquisition costs and margins. Heavy SEO reliance leaves DHI exposed to frequent Google core updates. Diversifying paid channels and building owned communities reduces this supplier concentration risk.

Specialized verification and compliance services

For security-cleared roles third-party screening and verification vendors are highly specialized and fewer in number, servicing an estimated cleared population of about 2.6 million in the U.S. in 2024, which limits substitutability and grants suppliers measurable bargaining power. Deep technical and systems integration with talent platforms raises switching costs and operational risk. Long-term volume commitments and strategic partnerships are common levers DHI can use to negotiate better terms. Strong compliance regimes (FISMA, DoD JPAS legacy constraints) further constrain buyer options.

Software tooling and AI models

Third-party search, matching, analytics and AI model providers such as OpenAI, Anthropic and Google materially influence DHI product quality and cost; 2024 supplier terms and quota limits shaped integration choices. Rapid pricing and usage-policy shifts among major model vendors in 2024 altered unit economics, while proprietary model development cuts dependence but requires CAPEX and engineering spend. Hybrid build-buy approaches dilute supplier leverage and preserve flexibility.

- Third-party dominance: OpenAI, Anthropic, Google

- 2024 vendor policy shifts impact unit economics

- Proprietary models reduce reliance but raise CAPEX

- Hybrid build-buy lowers supplier bargaining power

Payment processors and fraud tools

Payments, billing, and anti-fraud vendors are largely standardized but still extract meaningful take rates; card processing fees commonly range from 1.5%–3.5% plus $0.20–$0.30 per transaction, and many fraud tools charge percentage or SaaS fees. Chargeback rules and compliance mandates (PCI, PSD2/3-style requirements) create non-negotiable liabilities for merchants. Multi-processor routing provides redundancy and pricing flexibility, so supplier power is moderate due to available alternatives.

- processing-fees: 1.5%–3.5% + $0.20–$0.30 per tx

- chargebacks/compliance: non-negotiable liability

- routing: enables cost arbitration and redundancy

Cloud, search and AI vendor concentration threatens platform margins, uptime and CAC volatility

DHI faces concentrated cloud supplier risk (AWS ≈34%, Azure ≈23%, Google ≈11% IaaS/PaaS 2024), costly switching and outage exposure. Search/app gatekeepers (Google ~92% search, Android ~71% share 2024) raise CAC volatility. AI/model vendors (OpenAI, Anthropic, Google) and niche security screens further constrain bargaining without CAPEX for proprietary builds.

| Supplier | Key stat (2024) |

|---|---|

| Cloud | AWS34%/Azure23%/GCP11% |

| Search/App | Google92%/Android71% |

| Payments | 1.5%–3.5% + $0.20–$0.30 |

What is included in the product

Tailored Porter’s Five Forces analysis for DHI Group uncovers key drivers of competition, buyer and supplier power, and market entry risks specific to its niche recruiting platforms. It identifies substitutes, disruptive threats, and industry dynamics that shape pricing, profitability, and strategic positioning for investors and management.

A concise one-sheet Porter's Five Forces for DHI Group that instantly highlights competitive pressure and talent-market risks, ready to drop into decks for rapid decisions. Customize force levels or swap data to model scenarios—no macros, just clear visuals to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Employers and recruiters can multi-home

Corporate TA teams routinely multi-home across job boards, agencies and LinkedIn (930 million members in 2024), expanding switching options and driving sharper price sensitivity and tougher negotiation on enterprise contracts. Superior candidate quality and niche reach reduce discount pressure by delivering higher fill rates and time-to-hire improvements. Demonstrable ROI metrics—cost-per-hire and quality-of-hire—are decisive for retention.

Large enterprise buyers negotiate hard

Large enterprise buyers demand volume discounts, custom SLAs and integrations, using churn risk to press pricing and product-roadmap concessions; Gartner reported global IT spending at about $4.8 trillion in 2024, keeping enterprise buying power high. Multi-year contracts (commonly 3–5 years) stabilize revenue but often reduce margin via upfront discounts and committed services. Land-and-expand models require explicit KPIs and renewal-linked performance metrics to retain leverage.

SMBs are price sensitive and churn-prone

SMBs, which comprise 99.9% of US firms per the SBA, operate with tight budgets and episodic hiring cycles, making them highly price sensitive and churn-prone. They switch platforms rapidly when ROI is delayed, so self-serve packaging and transparent pricing increase comparability and accelerate selection. For DHI Group, maintaining low CAC and delivering quick time-to-value are essential to retain these customers.

Candidates exert indirect power via engagement

Candidates exert indirect power via engagement: job seekers rarely pay on DHI platforms but their participation drives liquidity, and poor UX or irrelevant matches push them to substitutes, eroding employer value; LinkedIn reached about 930 million members in 2024, underscoring candidate mobility. Brand trust, community features, and content keep talent engaged, while high-quality candidate density weakens employer bargaining power.

- job_seekers_free

- liquidity_drivers

- ux_churn_risk

- brand_trust_engagement

- candidate_density_weakens_employers

Data-driven procurement expectations

Buyers increasingly demand attribution, benchmarking, and pay-for-performance models, making opaque analytics a direct driver of discounting and reduced willingness to pay list prices; providing real-time dashboards and outcome guarantees neutralizes this leverage and preserves margins. Contracts now routinely embed performance clauses and KPIs, shifting negotiations from price to measurable outcomes.

- Attribution demands: buyers require clear ROI mapping

- Benchmarking: comparison data drives negotiation

- Pay-for-performance: ties fees to outcomes

- Dashboards/outcome guarantees: mitigate buyer power

- Performance clauses: becoming standard in contracts

Multi-homed buyers and candidate power squeeze pricing; UX-driven churn erodes employer leverage

Buyers multi-home across boards and LinkedIn (930 million members in 2024), raising switching options and price pressure. Large enterprises wield leverage via volume discounts and custom SLAs amid ~$4.8T global IT spend (2024), while US SMBs (99.9% of firms) are highly price sensitive. Candidates drive liquidity; poor UX increases churn and weakens employer purchasing power.

| Metric | 2024 Value |

|---|---|

| LinkedIn members | 930 million |

| Global IT spend | $4.8 trillion |

| US SMB share | 99.9% |

| Typical contract length | 3–5 years |

Preview the Actual Deliverable

DHI Group Porter's Five Forces Analysis

This preview shows the exact DHI Group Porter’s Five Forces analysis you'll receive—no placeholders or mockups. Once you purchase, you’ll get immediate access to this same fully formatted, professionally written document. It’s complete, ready for download and use in your decision-making or reports.