Dialog Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Dialog Group faces moderate supplier leverage, rising digital competition, and regulatory pressures that together shape its margin and growth outlook. Buyers have increasing choice while substitutes and tech entrants raise long-term threats, making strategic positioning crucial. This brief snapshot hints at risks and opportunities—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights tailored to Dialog Group.

Suppliers Bargaining Power

Specialized equipment OEM dependence

Dialog depends on OEMs for pumps, valves, instrumentation and control systems built to oil and gas standards, and the top 5 OEMs hold roughly 50–60% of the global market (2024), concentrating supply. Limited qualified brands increase switching costs and typical lead times of 20–26 weeks raise delivery risk. OEM after-sales, spares and warranties can drive 10–15% of lifecycle costs, giving OEMs moderate pricing and delivery power.

Skilled labor and niche contractors

EPCC and maintenance demand certified welders, inspectors and process engineers, and in 2024 industry reports showed specialist contractor dayrates can command up to a 20% premium during peak regional project cycles. Dialog reduces exposure through in-house certified teams and long-term contractor panels covering >60% of routine scope. Nonetheless persistent skill scarcity in 2024 sustains supplier leverage for critical niche work.

Technology licensors and process packages

Petrochemical and terminal projects routinely rely on licensors such as Honeywell UOP, Axens and Lummus for process packages, and these licensors dictate design standards, spares lists and performance guarantees.

Licensors often require specific suppliers and warranty-linked spares, constraining Dialog’s procurement flexibility and driving predictable cost premiums.

Mandated vendors and fee structures embed structural supplier power into project economics, raising project CAPEX and operating risk through limited alternatives.

Steel, bulk materials, and logistics

Price volatility in steel, alloys and bulk materials—which moved roughly 20–30% in 2023–2024—can sharply squeeze margins on fixed‑price EPCC contracts; long‑lead items amplify exposure. Port access constraints and heavy‑lift logistics drive schedule risk and can add double‑digit percent cost overruns on select projects. Long‑term procurement frameworks and hedging cut but do not remove exposure, and suppliers keep situational bargaining power in tight markets.

- Price swings 2023–24: ~20–30%

- Fixed‑price EPCC: margin squeeze risk

- Ports/heavy‑lift: schedule + double‑digit cost impact

- Hedging/frameworks: reduce but not eliminate exposure

- Suppliers: retain leverage in tight supply

Land, utilities, and port concessions

Tank terminal economics hinge on scarce waterfront land, jetty rights and utilities supplied largely by government-linked entities and port authorities; concession terms, tariffs and priority connections directly affect margins and throughput; maritime trade moves over 80% of global goods by volume (World Bank), amplifying location-specific supplier power.

- Suppliers: port authorities, state utilities

- Key levers: concessions, tariffs, connection priority

- Impact: high, location-specific bargaining power

OEMs dominate (50–60%), 20–26 week lead times and 20–30% steel volatility risk

Dialog faces concentrated OEM supply (top 5 = 50–60% global, 2024), 20–26 week lead times and 10–15% lifecycle cost dependence on OEM spares. Specialist contractor dayrates hit +20% in peak 2024 cycles; in‑house teams cut exposure but skill scarcity sustains niche supplier leverage. Steel/alloy volatility ~20–30% (2023–24) and port/heavy‑lift constraints add double‑digit cost/schedule risk.

| Metric | 2023–24 |

|---|---|

| Top5 OEM share | 50–60% |

| Lead times | 20–26 weeks |

| Contractor premium | up to 20% |

| Steel volatility | 20–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Dialog Group, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and market-entry barriers to inform pricing, profitability and strategic positioning.

A one-sheet Porter's Five Forces for Dialog Group that turns complexity into clarity—customize pressure levels, swap in your own data, and instantly visualize strategic pressure with a ready-to-copy spider chart for decks or dashboards.

Customers Bargaining Power

Concentrated NOC/IOC customer base

Customers are large NOCs/IOCs with professional procurement teams; in 2024 global oil and gas upstream capex was roughly $350bn, concentrating buying power into few large buyers handling multi‑million dollar contracts. Few buyers and big‑ticket projects increase negotiating leverage and competitive tenders drive price pressure. Dialog offsets this through a proven track record and integrated offerings across engineering, procurement and construction, helping protect margins.

Project-based pricing and rebids

In 2024 EPCC work is frequently re-tendered, enabling buyers to benchmark multiple bids and drive down margins; transparent cost breakdowns and liquidated damages provisions shift delivery and price risk to contractors.

Switching costs vs performance history

While switching providers mid-project is risky, at award stage buyers in 2024 can and do swap among qualified firms, keeping initial leverage with purchasers. Dialog’s strong safety, quality and schedule delivery record creates soft lock-in that reduces buyer willingness to change suppliers. Dialog’s lifecycle services—expanded through 2024—incrementally raise switching costs as assets move into operations. Nonetheless award-stage power remains with buyers.

Long-term terminal contracts

Storage customers sign multi-year take-or-pay agreements that lower churn and stabilize revenue streams, with contract tenors commonly spanning several years. Anchor tenants with scale retain bargaining leverage to secure more favorable tariff and volume terms. Cyclical utilization patterns materially affect tenants’ renewal bargaining power, tightening during oversupply and easing when capacity is scarce.

- Multi-year take-or-pay reduces churn

- Anchor tenants secure favorable terms

- Utilization cycles drive renewal leverage

Bundled services and value-add

Bundling EPCC with maintenance and specialist products gives Dialog cross-sell leverage, meeting buyer demand for single-point accountability and faster turnaround, which weakens purely price-driven negotiations; value density from integrated solutions reduces but does not eliminate customer bargaining power.

- Cross-sell: EPCC + maintenance

- Single-point accountability speeds delivery

- Reduces price-only bargaining

- Value density tempers buyer power

Buyers dominate $350bn capex; bundled EPCC + multi-year storage protect margins

Customers are few large NOCs/IOCs; 2024 global upstream capex ~ $350bn concentrates buying power into professional procurement teams, driving competitive tenders and price pressure. Dialog’s EPCC track record and bundled lifecycle services raise switching costs and protect margins, but award-stage leverage remains with buyers. Multi‑year take‑or‑pay storage contracts stabilize revenue while anchor tenants retain negotiation power.

| Metric | 2024 value | Impact |

|---|---|---|

| Global upstream capex | $350bn | Concentrated buyer power |

| Storage contracts | Multi‑year | Revenue stability, anchor leverage |

Preview the Actual Deliverable

Dialog Group Porter's Five Forces Analysis

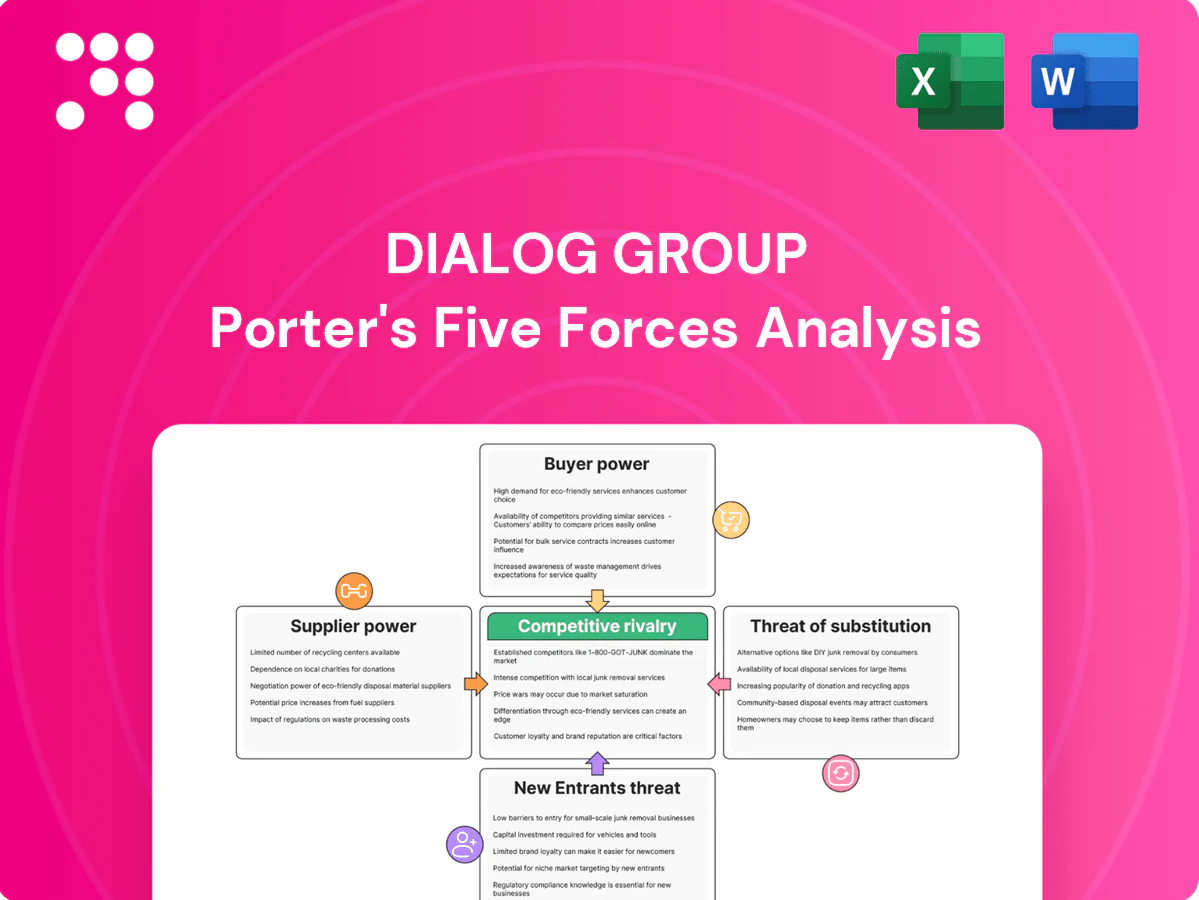

This preview shows the exact Porter's Five Forces analysis of Dialog Group you'll receive after purchase—no placeholders or mockups. It evaluates industry rivalry, threat of entry, buyer and supplier power, and substitute pressures with concise, actionable insights. The document is professionally formatted and ready for immediate download and use.

A Must-Have Tool for Decision-Makers

Dialog Group faces moderate supplier leverage, rising digital competition, and regulatory pressures that together shape its margin and growth outlook. Buyers have increasing choice while substitutes and tech entrants raise long-term threats, making strategic positioning crucial. This brief snapshot hints at risks and opportunities—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights tailored to Dialog Group.

Suppliers Bargaining Power

Specialized equipment OEM dependence

Dialog depends on OEMs for pumps, valves, instrumentation and control systems built to oil and gas standards, and the top 5 OEMs hold roughly 50–60% of the global market (2024), concentrating supply. Limited qualified brands increase switching costs and typical lead times of 20–26 weeks raise delivery risk. OEM after-sales, spares and warranties can drive 10–15% of lifecycle costs, giving OEMs moderate pricing and delivery power.

Skilled labor and niche contractors

EPCC and maintenance demand certified welders, inspectors and process engineers, and in 2024 industry reports showed specialist contractor dayrates can command up to a 20% premium during peak regional project cycles. Dialog reduces exposure through in-house certified teams and long-term contractor panels covering >60% of routine scope. Nonetheless persistent skill scarcity in 2024 sustains supplier leverage for critical niche work.

Technology licensors and process packages

Petrochemical and terminal projects routinely rely on licensors such as Honeywell UOP, Axens and Lummus for process packages, and these licensors dictate design standards, spares lists and performance guarantees.

Licensors often require specific suppliers and warranty-linked spares, constraining Dialog’s procurement flexibility and driving predictable cost premiums.

Mandated vendors and fee structures embed structural supplier power into project economics, raising project CAPEX and operating risk through limited alternatives.

Steel, bulk materials, and logistics

Price volatility in steel, alloys and bulk materials—which moved roughly 20–30% in 2023–2024—can sharply squeeze margins on fixed‑price EPCC contracts; long‑lead items amplify exposure. Port access constraints and heavy‑lift logistics drive schedule risk and can add double‑digit percent cost overruns on select projects. Long‑term procurement frameworks and hedging cut but do not remove exposure, and suppliers keep situational bargaining power in tight markets.

- Price swings 2023–24: ~20–30%

- Fixed‑price EPCC: margin squeeze risk

- Ports/heavy‑lift: schedule + double‑digit cost impact

- Hedging/frameworks: reduce but not eliminate exposure

- Suppliers: retain leverage in tight supply

Land, utilities, and port concessions

Tank terminal economics hinge on scarce waterfront land, jetty rights and utilities supplied largely by government-linked entities and port authorities; concession terms, tariffs and priority connections directly affect margins and throughput; maritime trade moves over 80% of global goods by volume (World Bank), amplifying location-specific supplier power.

- Suppliers: port authorities, state utilities

- Key levers: concessions, tariffs, connection priority

- Impact: high, location-specific bargaining power

OEMs dominate (50–60%), 20–26 week lead times and 20–30% steel volatility risk

Dialog faces concentrated OEM supply (top 5 = 50–60% global, 2024), 20–26 week lead times and 10–15% lifecycle cost dependence on OEM spares. Specialist contractor dayrates hit +20% in peak 2024 cycles; in‑house teams cut exposure but skill scarcity sustains niche supplier leverage. Steel/alloy volatility ~20–30% (2023–24) and port/heavy‑lift constraints add double‑digit cost/schedule risk.

| Metric | 2023–24 |

|---|---|

| Top5 OEM share | 50–60% |

| Lead times | 20–26 weeks |

| Contractor premium | up to 20% |

| Steel volatility | 20–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Dialog Group, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and market-entry barriers to inform pricing, profitability and strategic positioning.

A one-sheet Porter's Five Forces for Dialog Group that turns complexity into clarity—customize pressure levels, swap in your own data, and instantly visualize strategic pressure with a ready-to-copy spider chart for decks or dashboards.

Customers Bargaining Power

Concentrated NOC/IOC customer base

Customers are large NOCs/IOCs with professional procurement teams; in 2024 global oil and gas upstream capex was roughly $350bn, concentrating buying power into few large buyers handling multi‑million dollar contracts. Few buyers and big‑ticket projects increase negotiating leverage and competitive tenders drive price pressure. Dialog offsets this through a proven track record and integrated offerings across engineering, procurement and construction, helping protect margins.

Project-based pricing and rebids

In 2024 EPCC work is frequently re-tendered, enabling buyers to benchmark multiple bids and drive down margins; transparent cost breakdowns and liquidated damages provisions shift delivery and price risk to contractors.

Switching costs vs performance history

While switching providers mid-project is risky, at award stage buyers in 2024 can and do swap among qualified firms, keeping initial leverage with purchasers. Dialog’s strong safety, quality and schedule delivery record creates soft lock-in that reduces buyer willingness to change suppliers. Dialog’s lifecycle services—expanded through 2024—incrementally raise switching costs as assets move into operations. Nonetheless award-stage power remains with buyers.

Long-term terminal contracts

Storage customers sign multi-year take-or-pay agreements that lower churn and stabilize revenue streams, with contract tenors commonly spanning several years. Anchor tenants with scale retain bargaining leverage to secure more favorable tariff and volume terms. Cyclical utilization patterns materially affect tenants’ renewal bargaining power, tightening during oversupply and easing when capacity is scarce.

- Multi-year take-or-pay reduces churn

- Anchor tenants secure favorable terms

- Utilization cycles drive renewal leverage

Bundled services and value-add

Bundling EPCC with maintenance and specialist products gives Dialog cross-sell leverage, meeting buyer demand for single-point accountability and faster turnaround, which weakens purely price-driven negotiations; value density from integrated solutions reduces but does not eliminate customer bargaining power.

- Cross-sell: EPCC + maintenance

- Single-point accountability speeds delivery

- Reduces price-only bargaining

- Value density tempers buyer power

Buyers dominate $350bn capex; bundled EPCC + multi-year storage protect margins

Customers are few large NOCs/IOCs; 2024 global upstream capex ~ $350bn concentrates buying power into professional procurement teams, driving competitive tenders and price pressure. Dialog’s EPCC track record and bundled lifecycle services raise switching costs and protect margins, but award-stage leverage remains with buyers. Multi‑year take‑or‑pay storage contracts stabilize revenue while anchor tenants retain negotiation power.

| Metric | 2024 value | Impact |

|---|---|---|

| Global upstream capex | $350bn | Concentrated buyer power |

| Storage contracts | Multi‑year | Revenue stability, anchor leverage |

Preview the Actual Deliverable

Dialog Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Dialog Group you'll receive after purchase—no placeholders or mockups. It evaluates industry rivalry, threat of entry, buyer and supplier power, and substitute pressures with concise, actionable insights. The document is professionally formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Dialog Group faces moderate supplier leverage, rising digital competition, and regulatory pressures that together shape its margin and growth outlook. Buyers have increasing choice while substitutes and tech entrants raise long-term threats, making strategic positioning crucial. This brief snapshot hints at risks and opportunities—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights tailored to Dialog Group.

Suppliers Bargaining Power

Specialized equipment OEM dependence

Dialog depends on OEMs for pumps, valves, instrumentation and control systems built to oil and gas standards, and the top 5 OEMs hold roughly 50–60% of the global market (2024), concentrating supply. Limited qualified brands increase switching costs and typical lead times of 20–26 weeks raise delivery risk. OEM after-sales, spares and warranties can drive 10–15% of lifecycle costs, giving OEMs moderate pricing and delivery power.

Skilled labor and niche contractors

EPCC and maintenance demand certified welders, inspectors and process engineers, and in 2024 industry reports showed specialist contractor dayrates can command up to a 20% premium during peak regional project cycles. Dialog reduces exposure through in-house certified teams and long-term contractor panels covering >60% of routine scope. Nonetheless persistent skill scarcity in 2024 sustains supplier leverage for critical niche work.

Technology licensors and process packages

Petrochemical and terminal projects routinely rely on licensors such as Honeywell UOP, Axens and Lummus for process packages, and these licensors dictate design standards, spares lists and performance guarantees.

Licensors often require specific suppliers and warranty-linked spares, constraining Dialog’s procurement flexibility and driving predictable cost premiums.

Mandated vendors and fee structures embed structural supplier power into project economics, raising project CAPEX and operating risk through limited alternatives.

Steel, bulk materials, and logistics

Price volatility in steel, alloys and bulk materials—which moved roughly 20–30% in 2023–2024—can sharply squeeze margins on fixed‑price EPCC contracts; long‑lead items amplify exposure. Port access constraints and heavy‑lift logistics drive schedule risk and can add double‑digit percent cost overruns on select projects. Long‑term procurement frameworks and hedging cut but do not remove exposure, and suppliers keep situational bargaining power in tight markets.

- Price swings 2023–24: ~20–30%

- Fixed‑price EPCC: margin squeeze risk

- Ports/heavy‑lift: schedule + double‑digit cost impact

- Hedging/frameworks: reduce but not eliminate exposure

- Suppliers: retain leverage in tight supply

Land, utilities, and port concessions

Tank terminal economics hinge on scarce waterfront land, jetty rights and utilities supplied largely by government-linked entities and port authorities; concession terms, tariffs and priority connections directly affect margins and throughput; maritime trade moves over 80% of global goods by volume (World Bank), amplifying location-specific supplier power.

- Suppliers: port authorities, state utilities

- Key levers: concessions, tariffs, connection priority

- Impact: high, location-specific bargaining power

OEMs dominate (50–60%), 20–26 week lead times and 20–30% steel volatility risk

Dialog faces concentrated OEM supply (top 5 = 50–60% global, 2024), 20–26 week lead times and 10–15% lifecycle cost dependence on OEM spares. Specialist contractor dayrates hit +20% in peak 2024 cycles; in‑house teams cut exposure but skill scarcity sustains niche supplier leverage. Steel/alloy volatility ~20–30% (2023–24) and port/heavy‑lift constraints add double‑digit cost/schedule risk.

| Metric | 2023–24 |

|---|---|

| Top5 OEM share | 50–60% |

| Lead times | 20–26 weeks |

| Contractor premium | up to 20% |

| Steel volatility | 20–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Dialog Group, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and market-entry barriers to inform pricing, profitability and strategic positioning.

A one-sheet Porter's Five Forces for Dialog Group that turns complexity into clarity—customize pressure levels, swap in your own data, and instantly visualize strategic pressure with a ready-to-copy spider chart for decks or dashboards.

Customers Bargaining Power

Concentrated NOC/IOC customer base

Customers are large NOCs/IOCs with professional procurement teams; in 2024 global oil and gas upstream capex was roughly $350bn, concentrating buying power into few large buyers handling multi‑million dollar contracts. Few buyers and big‑ticket projects increase negotiating leverage and competitive tenders drive price pressure. Dialog offsets this through a proven track record and integrated offerings across engineering, procurement and construction, helping protect margins.

Project-based pricing and rebids

In 2024 EPCC work is frequently re-tendered, enabling buyers to benchmark multiple bids and drive down margins; transparent cost breakdowns and liquidated damages provisions shift delivery and price risk to contractors.

Switching costs vs performance history

While switching providers mid-project is risky, at award stage buyers in 2024 can and do swap among qualified firms, keeping initial leverage with purchasers. Dialog’s strong safety, quality and schedule delivery record creates soft lock-in that reduces buyer willingness to change suppliers. Dialog’s lifecycle services—expanded through 2024—incrementally raise switching costs as assets move into operations. Nonetheless award-stage power remains with buyers.

Long-term terminal contracts

Storage customers sign multi-year take-or-pay agreements that lower churn and stabilize revenue streams, with contract tenors commonly spanning several years. Anchor tenants with scale retain bargaining leverage to secure more favorable tariff and volume terms. Cyclical utilization patterns materially affect tenants’ renewal bargaining power, tightening during oversupply and easing when capacity is scarce.

- Multi-year take-or-pay reduces churn

- Anchor tenants secure favorable terms

- Utilization cycles drive renewal leverage

Bundled services and value-add

Bundling EPCC with maintenance and specialist products gives Dialog cross-sell leverage, meeting buyer demand for single-point accountability and faster turnaround, which weakens purely price-driven negotiations; value density from integrated solutions reduces but does not eliminate customer bargaining power.

- Cross-sell: EPCC + maintenance

- Single-point accountability speeds delivery

- Reduces price-only bargaining

- Value density tempers buyer power

Buyers dominate $350bn capex; bundled EPCC + multi-year storage protect margins

Customers are few large NOCs/IOCs; 2024 global upstream capex ~ $350bn concentrates buying power into professional procurement teams, driving competitive tenders and price pressure. Dialog’s EPCC track record and bundled lifecycle services raise switching costs and protect margins, but award-stage leverage remains with buyers. Multi‑year take‑or‑pay storage contracts stabilize revenue while anchor tenants retain negotiation power.

| Metric | 2024 value | Impact |

|---|---|---|

| Global upstream capex | $350bn | Concentrated buyer power |

| Storage contracts | Multi‑year | Revenue stability, anchor leverage |

Preview the Actual Deliverable

Dialog Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Dialog Group you'll receive after purchase—no placeholders or mockups. It evaluates industry rivalry, threat of entry, buyer and supplier power, and substitute pressures with concise, actionable insights. The document is professionally formatted and ready for immediate download and use.