DIC Porter's Five Forces Analysis

Don't Miss the Bigger Picture

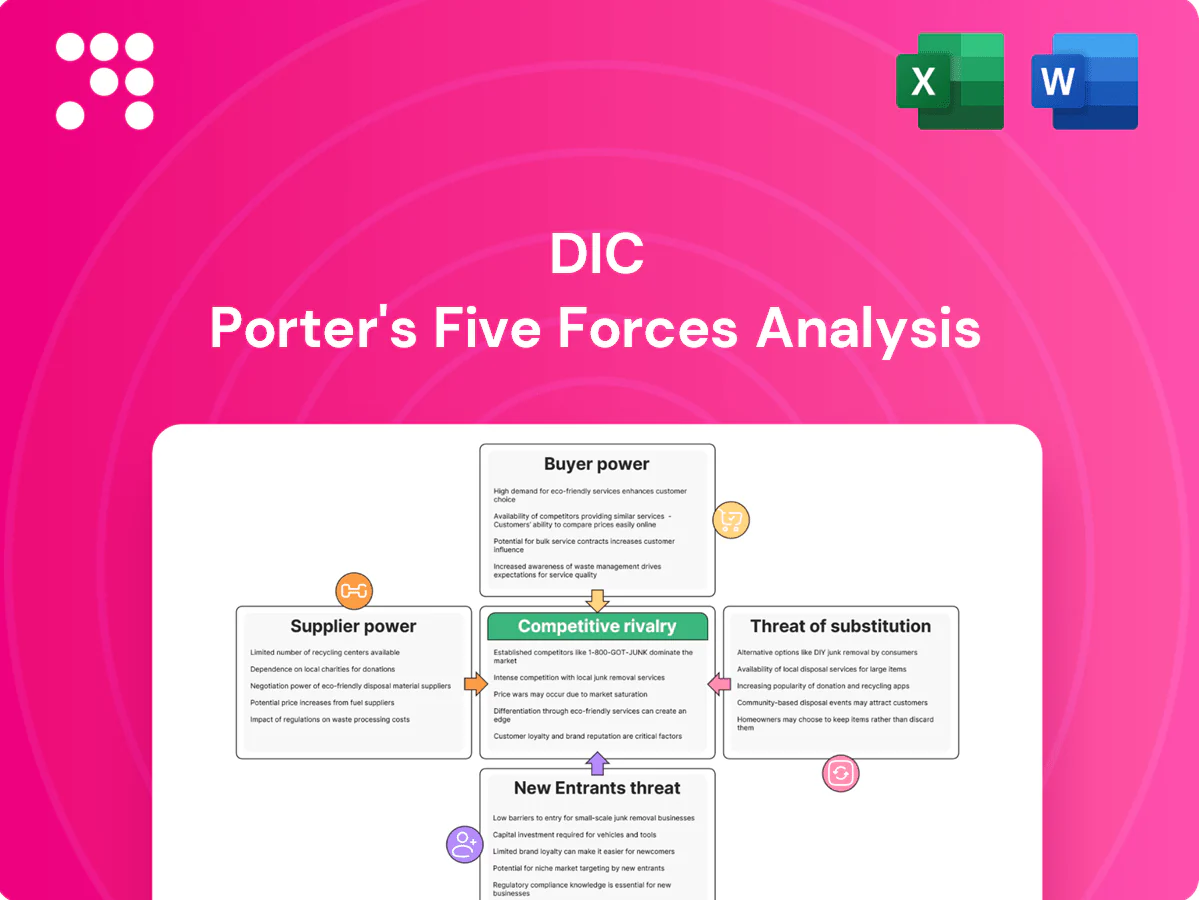

DIC's Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats that shape its margin and strategy. This brief outlines core pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Petrochemical feedstock concentration

Inks, pigments and resins depend on petrochemical derivatives supplied by concentrated majors (BASF, SABIC, Ineos, Sinopec), giving suppliers power to pass through price spikes and set terms. DIC’s scale — consolidated sales around ¥438 billion in FY2023 — moderates bargaining power but exposure to naphtha, solvents, monomers and additives remains material. Volatility in H1 2024 compressed margins before downstream repricing caught up.

Specialty intermediates scarcity

Certain pigment intermediates, specialty monomers and additives have few qualified producers across China, India and Europe, raising switching costs and qualification lead times. Limited qualified alternatives let niche intermediate suppliers exert pricing and delivery leverage during tightness or regulatory shifts. DIC uses dual-sourcing and long-term partnerships to mitigate risk, yet supply bottlenecks persisted in 2024. Persistent single-supplier nodes continue to threaten margins and production timing.

Energy and logistics volatility

Energy price swings (Brent averaged about USD 86/bbl in 2024) and freight disruptions directly ripple through chemical input costs, with suppliers increasingly invoking fuel surcharges or shorter quote validity to shift volatility risk to buyers.

For globally shipped materials, port congestion and geopolitics amplified supplier power, even as container rates in 2024 remained roughly 60–70% below 2021 peaks; DIC’s regional production footprint mitigates but does not fully offset systemic shocks.

Backward integration and tolling

Backward integration and tolling: DIC’s resin production and tight alignment with Sun Chemical in 2024 reduce dependence on spot purchases, and strategic tolling contracts and in‑house formulations blunt supplier leverage on key feedstocks; full upstream integration across all intermediates remains impractical, leaving exposure in specialty chemistries.

- In‑house resin capacity: lowers procurement volume

- Tolling: stabilizes input costs

- Partial integration: residual risk in specialty inputs

ESG and compliance constraints

REACH currently covers over 21,000 registered substances and the US EPA TSCA Inventory lists about 86,000 chemicals (EPA, 2024), while tightening regulatory and customer ESG demands shrink the pool of compliant suppliers, raising supplier leverage and approval timelines that can take months to years. Switching to greener inputs often needs requalification and R&D, and DIC’s sustainability push aids negotiations but approvals still limit options.

- Regulatory scope: REACH >21,000, TSCA ~86,000 (EPA 2024)

- Fewer compliant suppliers → higher leverage & longer approvals

- Substitution requires R&D/reevaluation; DIC sustainability mitigates but does not eliminate constraints

Suppliers' pricing power, energy swings and logistics squeeze margins; ¥438bn

Suppliers of petrochemical feedstocks and niche pigment intermediates exert material bargaining power, with DIC’s ¥438 billion FY2023 scale mitigating but not removing exposure. Energy swings (Brent ~USD86/bbl in 2024) and logistics volatility compressed margins in H1 2024. Dual‑sourcing, in‑house resins and tolling reduce risk, yet single‑supplier nodes and regulatory compliance (REACH >21,000; TSCA ~86,000) sustain supplier leverage.

| Metric | Value |

|---|---|

| DIC sales FY2023 | ¥438 bn |

| Brent avg 2024 | USD 86/bbl |

| Container rates vs 2021 | 60–70% lower |

| REACH/TSCA (2024) | >21,000 / ~86,000 |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for DIC, uncovering competitive drivers, supplier and buyer power, and entry and substitute threats that shape pricing and profitability. Identifies disruptive forces and market dynamics that deter entrants, with strategic commentary suitable for investor presentations, internal strategy decks, and editable reports.

A single-sheet DIC Porter's Five Forces summary that clarifies competitive pressures for rapid decision-making; customizable pressure sliders, instant spider chart visualization, and a clean, copy-ready layout let teams model scenarios and integrate results without complex tools.

Customers Bargaining Power

Concentrated global buyers

Concentrated buyers — large packaging converters, FMCG brands, printers, electronics and auto OEMs — wield scale and procurement sophistication, driving hard negotiations on price, service and sustainability. The global packaging market was about 1.1 trillion USD in 2024, concentrating leverage among top customers. Multi-year supply agreements commonly embed indexation and rebate structures, forcing margin pressure. DIC must defend value through superior performance, reliability and regulatory compliance.

Moderate switching costs

Product reformulation and print-line requalification create meaningful switching frictions for buyers, slowing moves despite commoditization; global printing inks market was about US$29 billion in 2024, where dual-sourcing remains common. For commoditized inks and resins buyers often dual-source to pressure pricing, limiting supplier margins. In high-spec electronics and automotive coatings, lengthy validation and qualification reduce buyer flexibility and favor DIC where application engineering is critical.

Price sensitivity in commoditized SKUs

Standard solvent-borne inks and general-purpose resins face intense price comparisons; 2024 industry reports show frequent tenders and spot buys dominate procurement cycles. Elasticity is higher in these commoditized segments, causing margin compression during oversupply cycles reported across 2024. Buyers leverage volume and specification parity to push prices down. Value-add technical service and application support can partially de-commoditize offers and preserve premium pricing.

Performance and compliance demands

Brand owners demand low-VOC, low-odor, food-contact safe and recyclable-friendly formulations, narrowing acceptable suppliers and reducing buyer leverage. Where DIC’s advanced, differentiated formulations meet these specs, willingness to pay improves and documentation/audit support further defend pricing. Global paints and coatings market was $171.6 billion in 2023 (Statista).

- Low-VOC

- Food-contact safe

- Recyclable-friendly

- Documentation/audits defend pricing

Global service and reliability

Multinationals prize global availability, consistent quality and short lead times; suppliers that guarantee continuity command stronger pricing and longer contracts, while any service failure rapidly restores buyer leverage. DIC’s global network and Sun Chemical footprint covered 60+ countries in 2024, reinforcing its negotiating position, though on-time delivery and continuity remain critical to retain that power.

- Global reach: 60+ countries (2024)

- Key strengths: continuity, quality, lead times

- Primary risk: service failures shift leverage to buyers

Buyers squeeze ink margins; global packaging USD1.1T strengthens leverage

Concentrated, sophisticated buyers (packaging converters, FMCG, OEMs) exert strong price/service pressure; global packaging market ~USD1.1T (2024) and printing inks ~USD29B (2024) concentrate leverage. Dual-sourcing in commoditized inks drives margin compression, while long validation in electronics/auto raises switching costs favoring DIC. DIC’s 60+ country footprint (2024) and advanced formulations (low-VOC, food-safe) partially defend pricing.

Preview the Actual Deliverable

DIC Porter's Five Forces Analysis

This preview shows the exact DIC Porter's Five Forces analysis you'll receive after purchase; it is the fully formatted, final document with no placeholders. The file available for download immediately upon payment is identical to what you see here and ready for use in reports or presentations. No mockups, no edits required.

Don't Miss the Bigger Picture

DIC's Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats that shape its margin and strategy. This brief outlines core pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Petrochemical feedstock concentration

Inks, pigments and resins depend on petrochemical derivatives supplied by concentrated majors (BASF, SABIC, Ineos, Sinopec), giving suppliers power to pass through price spikes and set terms. DIC’s scale — consolidated sales around ¥438 billion in FY2023 — moderates bargaining power but exposure to naphtha, solvents, monomers and additives remains material. Volatility in H1 2024 compressed margins before downstream repricing caught up.

Specialty intermediates scarcity

Certain pigment intermediates, specialty monomers and additives have few qualified producers across China, India and Europe, raising switching costs and qualification lead times. Limited qualified alternatives let niche intermediate suppliers exert pricing and delivery leverage during tightness or regulatory shifts. DIC uses dual-sourcing and long-term partnerships to mitigate risk, yet supply bottlenecks persisted in 2024. Persistent single-supplier nodes continue to threaten margins and production timing.

Energy and logistics volatility

Energy price swings (Brent averaged about USD 86/bbl in 2024) and freight disruptions directly ripple through chemical input costs, with suppliers increasingly invoking fuel surcharges or shorter quote validity to shift volatility risk to buyers.

For globally shipped materials, port congestion and geopolitics amplified supplier power, even as container rates in 2024 remained roughly 60–70% below 2021 peaks; DIC’s regional production footprint mitigates but does not fully offset systemic shocks.

Backward integration and tolling

Backward integration and tolling: DIC’s resin production and tight alignment with Sun Chemical in 2024 reduce dependence on spot purchases, and strategic tolling contracts and in‑house formulations blunt supplier leverage on key feedstocks; full upstream integration across all intermediates remains impractical, leaving exposure in specialty chemistries.

- In‑house resin capacity: lowers procurement volume

- Tolling: stabilizes input costs

- Partial integration: residual risk in specialty inputs

ESG and compliance constraints

REACH currently covers over 21,000 registered substances and the US EPA TSCA Inventory lists about 86,000 chemicals (EPA, 2024), while tightening regulatory and customer ESG demands shrink the pool of compliant suppliers, raising supplier leverage and approval timelines that can take months to years. Switching to greener inputs often needs requalification and R&D, and DIC’s sustainability push aids negotiations but approvals still limit options.

- Regulatory scope: REACH >21,000, TSCA ~86,000 (EPA 2024)

- Fewer compliant suppliers → higher leverage & longer approvals

- Substitution requires R&D/reevaluation; DIC sustainability mitigates but does not eliminate constraints

Suppliers' pricing power, energy swings and logistics squeeze margins; ¥438bn

Suppliers of petrochemical feedstocks and niche pigment intermediates exert material bargaining power, with DIC’s ¥438 billion FY2023 scale mitigating but not removing exposure. Energy swings (Brent ~USD86/bbl in 2024) and logistics volatility compressed margins in H1 2024. Dual‑sourcing, in‑house resins and tolling reduce risk, yet single‑supplier nodes and regulatory compliance (REACH >21,000; TSCA ~86,000) sustain supplier leverage.

| Metric | Value |

|---|---|

| DIC sales FY2023 | ¥438 bn |

| Brent avg 2024 | USD 86/bbl |

| Container rates vs 2021 | 60–70% lower |

| REACH/TSCA (2024) | >21,000 / ~86,000 |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for DIC, uncovering competitive drivers, supplier and buyer power, and entry and substitute threats that shape pricing and profitability. Identifies disruptive forces and market dynamics that deter entrants, with strategic commentary suitable for investor presentations, internal strategy decks, and editable reports.

A single-sheet DIC Porter's Five Forces summary that clarifies competitive pressures for rapid decision-making; customizable pressure sliders, instant spider chart visualization, and a clean, copy-ready layout let teams model scenarios and integrate results without complex tools.

Customers Bargaining Power

Concentrated global buyers

Concentrated buyers — large packaging converters, FMCG brands, printers, electronics and auto OEMs — wield scale and procurement sophistication, driving hard negotiations on price, service and sustainability. The global packaging market was about 1.1 trillion USD in 2024, concentrating leverage among top customers. Multi-year supply agreements commonly embed indexation and rebate structures, forcing margin pressure. DIC must defend value through superior performance, reliability and regulatory compliance.

Moderate switching costs

Product reformulation and print-line requalification create meaningful switching frictions for buyers, slowing moves despite commoditization; global printing inks market was about US$29 billion in 2024, where dual-sourcing remains common. For commoditized inks and resins buyers often dual-source to pressure pricing, limiting supplier margins. In high-spec electronics and automotive coatings, lengthy validation and qualification reduce buyer flexibility and favor DIC where application engineering is critical.

Price sensitivity in commoditized SKUs

Standard solvent-borne inks and general-purpose resins face intense price comparisons; 2024 industry reports show frequent tenders and spot buys dominate procurement cycles. Elasticity is higher in these commoditized segments, causing margin compression during oversupply cycles reported across 2024. Buyers leverage volume and specification parity to push prices down. Value-add technical service and application support can partially de-commoditize offers and preserve premium pricing.

Performance and compliance demands

Brand owners demand low-VOC, low-odor, food-contact safe and recyclable-friendly formulations, narrowing acceptable suppliers and reducing buyer leverage. Where DIC’s advanced, differentiated formulations meet these specs, willingness to pay improves and documentation/audit support further defend pricing. Global paints and coatings market was $171.6 billion in 2023 (Statista).

- Low-VOC

- Food-contact safe

- Recyclable-friendly

- Documentation/audits defend pricing

Global service and reliability

Multinationals prize global availability, consistent quality and short lead times; suppliers that guarantee continuity command stronger pricing and longer contracts, while any service failure rapidly restores buyer leverage. DIC’s global network and Sun Chemical footprint covered 60+ countries in 2024, reinforcing its negotiating position, though on-time delivery and continuity remain critical to retain that power.

- Global reach: 60+ countries (2024)

- Key strengths: continuity, quality, lead times

- Primary risk: service failures shift leverage to buyers

Buyers squeeze ink margins; global packaging USD1.1T strengthens leverage

Concentrated, sophisticated buyers (packaging converters, FMCG, OEMs) exert strong price/service pressure; global packaging market ~USD1.1T (2024) and printing inks ~USD29B (2024) concentrate leverage. Dual-sourcing in commoditized inks drives margin compression, while long validation in electronics/auto raises switching costs favoring DIC. DIC’s 60+ country footprint (2024) and advanced formulations (low-VOC, food-safe) partially defend pricing.

Preview the Actual Deliverable

DIC Porter's Five Forces Analysis

This preview shows the exact DIC Porter's Five Forces analysis you'll receive after purchase; it is the fully formatted, final document with no placeholders. The file available for download immediately upon payment is identical to what you see here and ready for use in reports or presentations. No mockups, no edits required.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

DIC's Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats that shape its margin and strategy. This brief outlines core pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Petrochemical feedstock concentration

Inks, pigments and resins depend on petrochemical derivatives supplied by concentrated majors (BASF, SABIC, Ineos, Sinopec), giving suppliers power to pass through price spikes and set terms. DIC’s scale — consolidated sales around ¥438 billion in FY2023 — moderates bargaining power but exposure to naphtha, solvents, monomers and additives remains material. Volatility in H1 2024 compressed margins before downstream repricing caught up.

Specialty intermediates scarcity

Certain pigment intermediates, specialty monomers and additives have few qualified producers across China, India and Europe, raising switching costs and qualification lead times. Limited qualified alternatives let niche intermediate suppliers exert pricing and delivery leverage during tightness or regulatory shifts. DIC uses dual-sourcing and long-term partnerships to mitigate risk, yet supply bottlenecks persisted in 2024. Persistent single-supplier nodes continue to threaten margins and production timing.

Energy and logistics volatility

Energy price swings (Brent averaged about USD 86/bbl in 2024) and freight disruptions directly ripple through chemical input costs, with suppliers increasingly invoking fuel surcharges or shorter quote validity to shift volatility risk to buyers.

For globally shipped materials, port congestion and geopolitics amplified supplier power, even as container rates in 2024 remained roughly 60–70% below 2021 peaks; DIC’s regional production footprint mitigates but does not fully offset systemic shocks.

Backward integration and tolling

Backward integration and tolling: DIC’s resin production and tight alignment with Sun Chemical in 2024 reduce dependence on spot purchases, and strategic tolling contracts and in‑house formulations blunt supplier leverage on key feedstocks; full upstream integration across all intermediates remains impractical, leaving exposure in specialty chemistries.

- In‑house resin capacity: lowers procurement volume

- Tolling: stabilizes input costs

- Partial integration: residual risk in specialty inputs

ESG and compliance constraints

REACH currently covers over 21,000 registered substances and the US EPA TSCA Inventory lists about 86,000 chemicals (EPA, 2024), while tightening regulatory and customer ESG demands shrink the pool of compliant suppliers, raising supplier leverage and approval timelines that can take months to years. Switching to greener inputs often needs requalification and R&D, and DIC’s sustainability push aids negotiations but approvals still limit options.

- Regulatory scope: REACH >21,000, TSCA ~86,000 (EPA 2024)

- Fewer compliant suppliers → higher leverage & longer approvals

- Substitution requires R&D/reevaluation; DIC sustainability mitigates but does not eliminate constraints

Suppliers' pricing power, energy swings and logistics squeeze margins; ¥438bn

Suppliers of petrochemical feedstocks and niche pigment intermediates exert material bargaining power, with DIC’s ¥438 billion FY2023 scale mitigating but not removing exposure. Energy swings (Brent ~USD86/bbl in 2024) and logistics volatility compressed margins in H1 2024. Dual‑sourcing, in‑house resins and tolling reduce risk, yet single‑supplier nodes and regulatory compliance (REACH >21,000; TSCA ~86,000) sustain supplier leverage.

| Metric | Value |

|---|---|

| DIC sales FY2023 | ¥438 bn |

| Brent avg 2024 | USD 86/bbl |

| Container rates vs 2021 | 60–70% lower |

| REACH/TSCA (2024) | >21,000 / ~86,000 |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored exclusively for DIC, uncovering competitive drivers, supplier and buyer power, and entry and substitute threats that shape pricing and profitability. Identifies disruptive forces and market dynamics that deter entrants, with strategic commentary suitable for investor presentations, internal strategy decks, and editable reports.

A single-sheet DIC Porter's Five Forces summary that clarifies competitive pressures for rapid decision-making; customizable pressure sliders, instant spider chart visualization, and a clean, copy-ready layout let teams model scenarios and integrate results without complex tools.

Customers Bargaining Power

Concentrated global buyers

Concentrated buyers — large packaging converters, FMCG brands, printers, electronics and auto OEMs — wield scale and procurement sophistication, driving hard negotiations on price, service and sustainability. The global packaging market was about 1.1 trillion USD in 2024, concentrating leverage among top customers. Multi-year supply agreements commonly embed indexation and rebate structures, forcing margin pressure. DIC must defend value through superior performance, reliability and regulatory compliance.

Moderate switching costs

Product reformulation and print-line requalification create meaningful switching frictions for buyers, slowing moves despite commoditization; global printing inks market was about US$29 billion in 2024, where dual-sourcing remains common. For commoditized inks and resins buyers often dual-source to pressure pricing, limiting supplier margins. In high-spec electronics and automotive coatings, lengthy validation and qualification reduce buyer flexibility and favor DIC where application engineering is critical.

Price sensitivity in commoditized SKUs

Standard solvent-borne inks and general-purpose resins face intense price comparisons; 2024 industry reports show frequent tenders and spot buys dominate procurement cycles. Elasticity is higher in these commoditized segments, causing margin compression during oversupply cycles reported across 2024. Buyers leverage volume and specification parity to push prices down. Value-add technical service and application support can partially de-commoditize offers and preserve premium pricing.

Performance and compliance demands

Brand owners demand low-VOC, low-odor, food-contact safe and recyclable-friendly formulations, narrowing acceptable suppliers and reducing buyer leverage. Where DIC’s advanced, differentiated formulations meet these specs, willingness to pay improves and documentation/audit support further defend pricing. Global paints and coatings market was $171.6 billion in 2023 (Statista).

- Low-VOC

- Food-contact safe

- Recyclable-friendly

- Documentation/audits defend pricing

Global service and reliability

Multinationals prize global availability, consistent quality and short lead times; suppliers that guarantee continuity command stronger pricing and longer contracts, while any service failure rapidly restores buyer leverage. DIC’s global network and Sun Chemical footprint covered 60+ countries in 2024, reinforcing its negotiating position, though on-time delivery and continuity remain critical to retain that power.

- Global reach: 60+ countries (2024)

- Key strengths: continuity, quality, lead times

- Primary risk: service failures shift leverage to buyers

Buyers squeeze ink margins; global packaging USD1.1T strengthens leverage

Concentrated, sophisticated buyers (packaging converters, FMCG, OEMs) exert strong price/service pressure; global packaging market ~USD1.1T (2024) and printing inks ~USD29B (2024) concentrate leverage. Dual-sourcing in commoditized inks drives margin compression, while long validation in electronics/auto raises switching costs favoring DIC. DIC’s 60+ country footprint (2024) and advanced formulations (low-VOC, food-safe) partially defend pricing.

Preview the Actual Deliverable

DIC Porter's Five Forces Analysis

This preview shows the exact DIC Porter's Five Forces analysis you'll receive after purchase; it is the fully formatted, final document with no placeholders. The file available for download immediately upon payment is identical to what you see here and ready for use in reports or presentations. No mockups, no edits required.