DigiKey Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

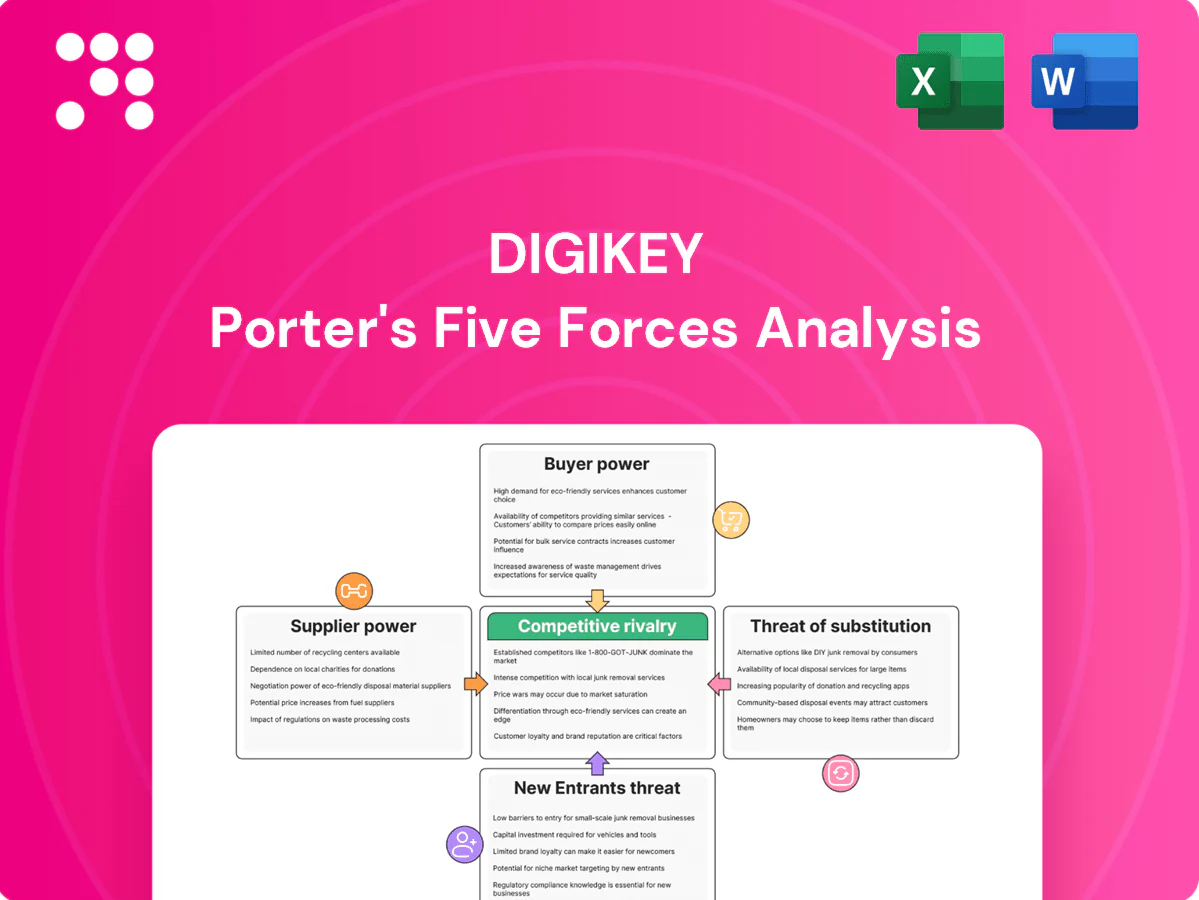

DigiKey’s competitive landscape is shaped by tight supplier relationships, evolving buyer expectations, and constant pressure from digital distributors—this snapshot highlights key tensions and strategic levers. Want the full picture? Unlock the complete Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy decisions.

Suppliers Bargaining Power

Consolidated manufacturer base

Major semiconductor and passives makers concentrate bargaining power, with global semiconductor sales at $556.8 billion in 2023 and TSMC alone holding roughly 56% of the pure‑play foundry market, tightening upstream leverage.

Selective authorized distribution agreements and pricing floors give suppliers control over branding, terms and allocations during node shortages.

DigiKey offsets this by offering broad brand coverage and SKU depth but cannot fully neutralize supplier consolidation and allocation cycles.

Line card exclusivity and authorizations

Suppliers control authorizations and line-card exclusivity, shaping territory rights, pricing tiers, and co-marketing access, which directly limits DigiKey’s assortment when marquee lines are withheld.

Losing a key supplier reduces traffic and BOM fulfillment options, while strict MAP, traceability, and compliance rules keep distributors aligned with supplier interests.

DigiKey’s robust compliance programs and demand-generation capabilities help retain authorizations but cannot eliminate supplier gatekeeping.

Design-in dependence

Once engineers design in a vendor part, late switching is costly, reinforcing supplier power and increasing DigiKey’s working capital needs; DigiKey lists over 11 million SKUs (2024) and must maintain alternates. EOL/PCN notices force distributors to manage transitions on supplier timelines, while suppliers can prioritize allocation to strategic accounts, constraining availability. DigiKey invests in cross-reference tools but remains subject to supplier lifecycle decisions.

Pricing and rebate structures

DigiKey faces supplier-controlled levers such as tiered discounts, co-op funds, and back-end rebates; distributors drive volume to hit favorable brackets, which can compress margins. Suppliers often enforce price parity, limiting undercutting and preserving their margin structure. DigiKey’s scale—with sales exceeding $6 billion—secures better headline terms, but variable rebates and back-end adjustments keep final bargaining power largely with suppliers.

- Tiered discounts: supplier-controlled

- Co-op funds/back-end rebates: affect net margins

- Price parity: restricts undercutting

- DigiKey scale: >$6B sales but rebates retain supplier leverage

Logistics and compliance requirements

RoHS (since 2003) and REACH (since 2007) plus 2024 EU digital product passport and tightened country-of-origin/traceability rules push compliance requirements upstream; suppliers control substance declarations and origin data. Suppliers can change packaging MOQs and lead times, shifting working capital needs; DigiKey absorbs inventory and handling costs, embedding supplier-driven compliance spend into its cost base. This structural burden increases supplier bargaining power.

- RoHS/REACH + 2024 DPP: upstream data/control

- Country-of-origin & traceability: documentation enforced

- Packaging MOQs/lead times alter WC; DigiKey bears inventory/handling costs

Supplier consolidation and distribution controls squeeze component distributors’ margins

Supplier consolidation (TSMC ~56% foundry; global semis $556.8B in 2023) and authorized distribution control raise supplier leverage, limiting DigiKey’s assortment despite >11M SKUs (2024) and >$6B sales. MAP, tiered rebates and allocation cycles compress margins and increase working capital via MOQs and compliance costs (RoHS/REACH/DPP). DigiKey’s scale mitigates but does not eliminate supplier gatekeeping.

| Metric | Value |

|---|---|

| Global semiconductor sales (2023) | $556.8B |

| TSMC foundry share | ~56% |

| DigiKey SKUs (2024) | >11M |

| DigiKey sales | >$6B |

What is included in the product

Tailored Porter's Five Forces analysis for DigiKey uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and rivalry, highlighting disruptive threats and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for DigiKey—customizable pressure levels with an instant radar view and clean layout ready to drop into pitch decks or strategic reports.

Customers Bargaining Power

High price transparency

In 2024 engineers and procurement teams can compare prices instantly across Mouser, Arrow, Newark and marketplaces, while RFQs and aggregator sites have largely eliminated information asymmetry. This real-time transparency enables frequent price matching that erodes distributor margins. DigiKey offsets pressure with superior in-stock availability, rapid fulfillment and service SLAs. These operational advantages help protect revenue per order despite tighter pricing.

Low switching costs

Low switching costs are amplified as checkout friction is minimal and competitors offer similar fast-shipping catalogs; Digi-Key’s catalog exceeds 12 million SKUs (2024) so buyers quickly compare prices and availability. Procurement platforms routinely integrate multiple distributors for dual-sourcing, letting OEMs split BOMs to chase spot availability and reduce vendor dependence. To maintain stickiness Digi-Key must keep parametric search accuracy, robust APIs and 99.9% uptime-level reliability.

Fragmented but professional demand

Many DigiKey customers buy small prototype quantities, limiting individual bargaining power, while larger OEM/EMS buyers place production orders and extract better terms. Urgent design cycles and downtime needs raise willingness to pay for rush buys, reducing price sensitivity. As of 2024 DigiKey lists over 12 million SKUs and reported annual sales exceeding $6 billion, supporting tiered pricing and instant availability to serve both segments.

BOM-level leverage

On full BOMs buyers solicit competitive quotes and substitutions, using approved alternates and multi-sourcing to lower reliance on any single distributor; DigiKey’s BOM tools and cross-reference features are designed to capture the full basket and increase win rates amid 2024 supply normalization. Line-item cherry-picking by buyers—prioritizing price on high-volume SKUs—keeps customer bargaining power meaningful despite basket capture efforts.

- Buyers: leverage full-BOM quotes and alternates

- Multi-sourcing: reduces single-distributor dependence

- DigiKey tools: BOM import, cross-refs, basket capture

- Risk: line-item cherry-picking sustains buyer power

Service expectations

Customers demand same-day ship, precise inventory visibility and frictionless returns; a 2024 industry survey found 78% of electronics buyers consider delivery speed a critical supplier criterion, and any lapse drives rapid churn to rivals. Buyers also expect free technical support and documentation, raising DigiKey’s cost-to-serve and strengthening buyer leverage.

- Same-day/next-day expectation — 78%

- Free tech support/documentation — required

- High service intensity → higher cost-to-serve and buyer power

Scale vs buyer power: 12M+ SKUs, $6B sales vs 78% same/next-day demand

Customers have strong price leverage from instant comparison and low switching costs; 78% expect same/next-day delivery. DigiKey’s scale—12M+ SKUs and >$6B sales (2024)—provides inventory resilience and tiered pricing to blunt concessions. Multi-sourcing and BOM cherry-picking keep buyer power high despite DigiKey’s BOM tools and fast fulfillment.

| Metric | Value |

|---|---|

| SKUs | 12M+ |

| Revenue (2024) | >$6B |

| Delivery criticality | 78% |

What You See Is What You Get

DigiKey Porter's Five Forces Analysis

This preview shows the exact DigiKey Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable, identical to what will be available to you instantly.

Go Beyond the Preview—Access the Full Strategic Report

DigiKey’s competitive landscape is shaped by tight supplier relationships, evolving buyer expectations, and constant pressure from digital distributors—this snapshot highlights key tensions and strategic levers. Want the full picture? Unlock the complete Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy decisions.

Suppliers Bargaining Power

Consolidated manufacturer base

Major semiconductor and passives makers concentrate bargaining power, with global semiconductor sales at $556.8 billion in 2023 and TSMC alone holding roughly 56% of the pure‑play foundry market, tightening upstream leverage.

Selective authorized distribution agreements and pricing floors give suppliers control over branding, terms and allocations during node shortages.

DigiKey offsets this by offering broad brand coverage and SKU depth but cannot fully neutralize supplier consolidation and allocation cycles.

Line card exclusivity and authorizations

Suppliers control authorizations and line-card exclusivity, shaping territory rights, pricing tiers, and co-marketing access, which directly limits DigiKey’s assortment when marquee lines are withheld.

Losing a key supplier reduces traffic and BOM fulfillment options, while strict MAP, traceability, and compliance rules keep distributors aligned with supplier interests.

DigiKey’s robust compliance programs and demand-generation capabilities help retain authorizations but cannot eliminate supplier gatekeeping.

Design-in dependence

Once engineers design in a vendor part, late switching is costly, reinforcing supplier power and increasing DigiKey’s working capital needs; DigiKey lists over 11 million SKUs (2024) and must maintain alternates. EOL/PCN notices force distributors to manage transitions on supplier timelines, while suppliers can prioritize allocation to strategic accounts, constraining availability. DigiKey invests in cross-reference tools but remains subject to supplier lifecycle decisions.

Pricing and rebate structures

DigiKey faces supplier-controlled levers such as tiered discounts, co-op funds, and back-end rebates; distributors drive volume to hit favorable brackets, which can compress margins. Suppliers often enforce price parity, limiting undercutting and preserving their margin structure. DigiKey’s scale—with sales exceeding $6 billion—secures better headline terms, but variable rebates and back-end adjustments keep final bargaining power largely with suppliers.

- Tiered discounts: supplier-controlled

- Co-op funds/back-end rebates: affect net margins

- Price parity: restricts undercutting

- DigiKey scale: >$6B sales but rebates retain supplier leverage

Logistics and compliance requirements

RoHS (since 2003) and REACH (since 2007) plus 2024 EU digital product passport and tightened country-of-origin/traceability rules push compliance requirements upstream; suppliers control substance declarations and origin data. Suppliers can change packaging MOQs and lead times, shifting working capital needs; DigiKey absorbs inventory and handling costs, embedding supplier-driven compliance spend into its cost base. This structural burden increases supplier bargaining power.

- RoHS/REACH + 2024 DPP: upstream data/control

- Country-of-origin & traceability: documentation enforced

- Packaging MOQs/lead times alter WC; DigiKey bears inventory/handling costs

Supplier consolidation and distribution controls squeeze component distributors’ margins

Supplier consolidation (TSMC ~56% foundry; global semis $556.8B in 2023) and authorized distribution control raise supplier leverage, limiting DigiKey’s assortment despite >11M SKUs (2024) and >$6B sales. MAP, tiered rebates and allocation cycles compress margins and increase working capital via MOQs and compliance costs (RoHS/REACH/DPP). DigiKey’s scale mitigates but does not eliminate supplier gatekeeping.

| Metric | Value |

|---|---|

| Global semiconductor sales (2023) | $556.8B |

| TSMC foundry share | ~56% |

| DigiKey SKUs (2024) | >11M |

| DigiKey sales | >$6B |

What is included in the product

Tailored Porter's Five Forces analysis for DigiKey uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and rivalry, highlighting disruptive threats and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for DigiKey—customizable pressure levels with an instant radar view and clean layout ready to drop into pitch decks or strategic reports.

Customers Bargaining Power

High price transparency

In 2024 engineers and procurement teams can compare prices instantly across Mouser, Arrow, Newark and marketplaces, while RFQs and aggregator sites have largely eliminated information asymmetry. This real-time transparency enables frequent price matching that erodes distributor margins. DigiKey offsets pressure with superior in-stock availability, rapid fulfillment and service SLAs. These operational advantages help protect revenue per order despite tighter pricing.

Low switching costs

Low switching costs are amplified as checkout friction is minimal and competitors offer similar fast-shipping catalogs; Digi-Key’s catalog exceeds 12 million SKUs (2024) so buyers quickly compare prices and availability. Procurement platforms routinely integrate multiple distributors for dual-sourcing, letting OEMs split BOMs to chase spot availability and reduce vendor dependence. To maintain stickiness Digi-Key must keep parametric search accuracy, robust APIs and 99.9% uptime-level reliability.

Fragmented but professional demand

Many DigiKey customers buy small prototype quantities, limiting individual bargaining power, while larger OEM/EMS buyers place production orders and extract better terms. Urgent design cycles and downtime needs raise willingness to pay for rush buys, reducing price sensitivity. As of 2024 DigiKey lists over 12 million SKUs and reported annual sales exceeding $6 billion, supporting tiered pricing and instant availability to serve both segments.

BOM-level leverage

On full BOMs buyers solicit competitive quotes and substitutions, using approved alternates and multi-sourcing to lower reliance on any single distributor; DigiKey’s BOM tools and cross-reference features are designed to capture the full basket and increase win rates amid 2024 supply normalization. Line-item cherry-picking by buyers—prioritizing price on high-volume SKUs—keeps customer bargaining power meaningful despite basket capture efforts.

- Buyers: leverage full-BOM quotes and alternates

- Multi-sourcing: reduces single-distributor dependence

- DigiKey tools: BOM import, cross-refs, basket capture

- Risk: line-item cherry-picking sustains buyer power

Service expectations

Customers demand same-day ship, precise inventory visibility and frictionless returns; a 2024 industry survey found 78% of electronics buyers consider delivery speed a critical supplier criterion, and any lapse drives rapid churn to rivals. Buyers also expect free technical support and documentation, raising DigiKey’s cost-to-serve and strengthening buyer leverage.

- Same-day/next-day expectation — 78%

- Free tech support/documentation — required

- High service intensity → higher cost-to-serve and buyer power

Scale vs buyer power: 12M+ SKUs, $6B sales vs 78% same/next-day demand

Customers have strong price leverage from instant comparison and low switching costs; 78% expect same/next-day delivery. DigiKey’s scale—12M+ SKUs and >$6B sales (2024)—provides inventory resilience and tiered pricing to blunt concessions. Multi-sourcing and BOM cherry-picking keep buyer power high despite DigiKey’s BOM tools and fast fulfillment.

| Metric | Value |

|---|---|

| SKUs | 12M+ |

| Revenue (2024) | >$6B |

| Delivery criticality | 78% |

What You See Is What You Get

DigiKey Porter's Five Forces Analysis

This preview shows the exact DigiKey Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable, identical to what will be available to you instantly.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

DigiKey’s competitive landscape is shaped by tight supplier relationships, evolving buyer expectations, and constant pressure from digital distributors—this snapshot highlights key tensions and strategic levers. Want the full picture? Unlock the complete Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy decisions.

Suppliers Bargaining Power

Consolidated manufacturer base

Major semiconductor and passives makers concentrate bargaining power, with global semiconductor sales at $556.8 billion in 2023 and TSMC alone holding roughly 56% of the pure‑play foundry market, tightening upstream leverage.

Selective authorized distribution agreements and pricing floors give suppliers control over branding, terms and allocations during node shortages.

DigiKey offsets this by offering broad brand coverage and SKU depth but cannot fully neutralize supplier consolidation and allocation cycles.

Line card exclusivity and authorizations

Suppliers control authorizations and line-card exclusivity, shaping territory rights, pricing tiers, and co-marketing access, which directly limits DigiKey’s assortment when marquee lines are withheld.

Losing a key supplier reduces traffic and BOM fulfillment options, while strict MAP, traceability, and compliance rules keep distributors aligned with supplier interests.

DigiKey’s robust compliance programs and demand-generation capabilities help retain authorizations but cannot eliminate supplier gatekeeping.

Design-in dependence

Once engineers design in a vendor part, late switching is costly, reinforcing supplier power and increasing DigiKey’s working capital needs; DigiKey lists over 11 million SKUs (2024) and must maintain alternates. EOL/PCN notices force distributors to manage transitions on supplier timelines, while suppliers can prioritize allocation to strategic accounts, constraining availability. DigiKey invests in cross-reference tools but remains subject to supplier lifecycle decisions.

Pricing and rebate structures

DigiKey faces supplier-controlled levers such as tiered discounts, co-op funds, and back-end rebates; distributors drive volume to hit favorable brackets, which can compress margins. Suppliers often enforce price parity, limiting undercutting and preserving their margin structure. DigiKey’s scale—with sales exceeding $6 billion—secures better headline terms, but variable rebates and back-end adjustments keep final bargaining power largely with suppliers.

- Tiered discounts: supplier-controlled

- Co-op funds/back-end rebates: affect net margins

- Price parity: restricts undercutting

- DigiKey scale: >$6B sales but rebates retain supplier leverage

Logistics and compliance requirements

RoHS (since 2003) and REACH (since 2007) plus 2024 EU digital product passport and tightened country-of-origin/traceability rules push compliance requirements upstream; suppliers control substance declarations and origin data. Suppliers can change packaging MOQs and lead times, shifting working capital needs; DigiKey absorbs inventory and handling costs, embedding supplier-driven compliance spend into its cost base. This structural burden increases supplier bargaining power.

- RoHS/REACH + 2024 DPP: upstream data/control

- Country-of-origin & traceability: documentation enforced

- Packaging MOQs/lead times alter WC; DigiKey bears inventory/handling costs

Supplier consolidation and distribution controls squeeze component distributors’ margins

Supplier consolidation (TSMC ~56% foundry; global semis $556.8B in 2023) and authorized distribution control raise supplier leverage, limiting DigiKey’s assortment despite >11M SKUs (2024) and >$6B sales. MAP, tiered rebates and allocation cycles compress margins and increase working capital via MOQs and compliance costs (RoHS/REACH/DPP). DigiKey’s scale mitigates but does not eliminate supplier gatekeeping.

| Metric | Value |

|---|---|

| Global semiconductor sales (2023) | $556.8B |

| TSMC foundry share | ~56% |

| DigiKey SKUs (2024) | >11M |

| DigiKey sales | >$6B |

What is included in the product

Tailored Porter's Five Forces analysis for DigiKey uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and rivalry, highlighting disruptive threats and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for DigiKey—customizable pressure levels with an instant radar view and clean layout ready to drop into pitch decks or strategic reports.

Customers Bargaining Power

High price transparency

In 2024 engineers and procurement teams can compare prices instantly across Mouser, Arrow, Newark and marketplaces, while RFQs and aggregator sites have largely eliminated information asymmetry. This real-time transparency enables frequent price matching that erodes distributor margins. DigiKey offsets pressure with superior in-stock availability, rapid fulfillment and service SLAs. These operational advantages help protect revenue per order despite tighter pricing.

Low switching costs

Low switching costs are amplified as checkout friction is minimal and competitors offer similar fast-shipping catalogs; Digi-Key’s catalog exceeds 12 million SKUs (2024) so buyers quickly compare prices and availability. Procurement platforms routinely integrate multiple distributors for dual-sourcing, letting OEMs split BOMs to chase spot availability and reduce vendor dependence. To maintain stickiness Digi-Key must keep parametric search accuracy, robust APIs and 99.9% uptime-level reliability.

Fragmented but professional demand

Many DigiKey customers buy small prototype quantities, limiting individual bargaining power, while larger OEM/EMS buyers place production orders and extract better terms. Urgent design cycles and downtime needs raise willingness to pay for rush buys, reducing price sensitivity. As of 2024 DigiKey lists over 12 million SKUs and reported annual sales exceeding $6 billion, supporting tiered pricing and instant availability to serve both segments.

BOM-level leverage

On full BOMs buyers solicit competitive quotes and substitutions, using approved alternates and multi-sourcing to lower reliance on any single distributor; DigiKey’s BOM tools and cross-reference features are designed to capture the full basket and increase win rates amid 2024 supply normalization. Line-item cherry-picking by buyers—prioritizing price on high-volume SKUs—keeps customer bargaining power meaningful despite basket capture efforts.

- Buyers: leverage full-BOM quotes and alternates

- Multi-sourcing: reduces single-distributor dependence

- DigiKey tools: BOM import, cross-refs, basket capture

- Risk: line-item cherry-picking sustains buyer power

Service expectations

Customers demand same-day ship, precise inventory visibility and frictionless returns; a 2024 industry survey found 78% of electronics buyers consider delivery speed a critical supplier criterion, and any lapse drives rapid churn to rivals. Buyers also expect free technical support and documentation, raising DigiKey’s cost-to-serve and strengthening buyer leverage.

- Same-day/next-day expectation — 78%

- Free tech support/documentation — required

- High service intensity → higher cost-to-serve and buyer power

Scale vs buyer power: 12M+ SKUs, $6B sales vs 78% same/next-day demand

Customers have strong price leverage from instant comparison and low switching costs; 78% expect same/next-day delivery. DigiKey’s scale—12M+ SKUs and >$6B sales (2024)—provides inventory resilience and tiered pricing to blunt concessions. Multi-sourcing and BOM cherry-picking keep buyer power high despite DigiKey’s BOM tools and fast fulfillment.

| Metric | Value |

|---|---|

| SKUs | 12M+ |

| Revenue (2024) | >$6B |

| Delivery criticality | 78% |

What You See Is What You Get

DigiKey Porter's Five Forces Analysis

This preview shows the exact DigiKey Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable, identical to what will be available to you instantly.