Diodes Porter's Five Forces Analysis

Don't Miss the Bigger Picture

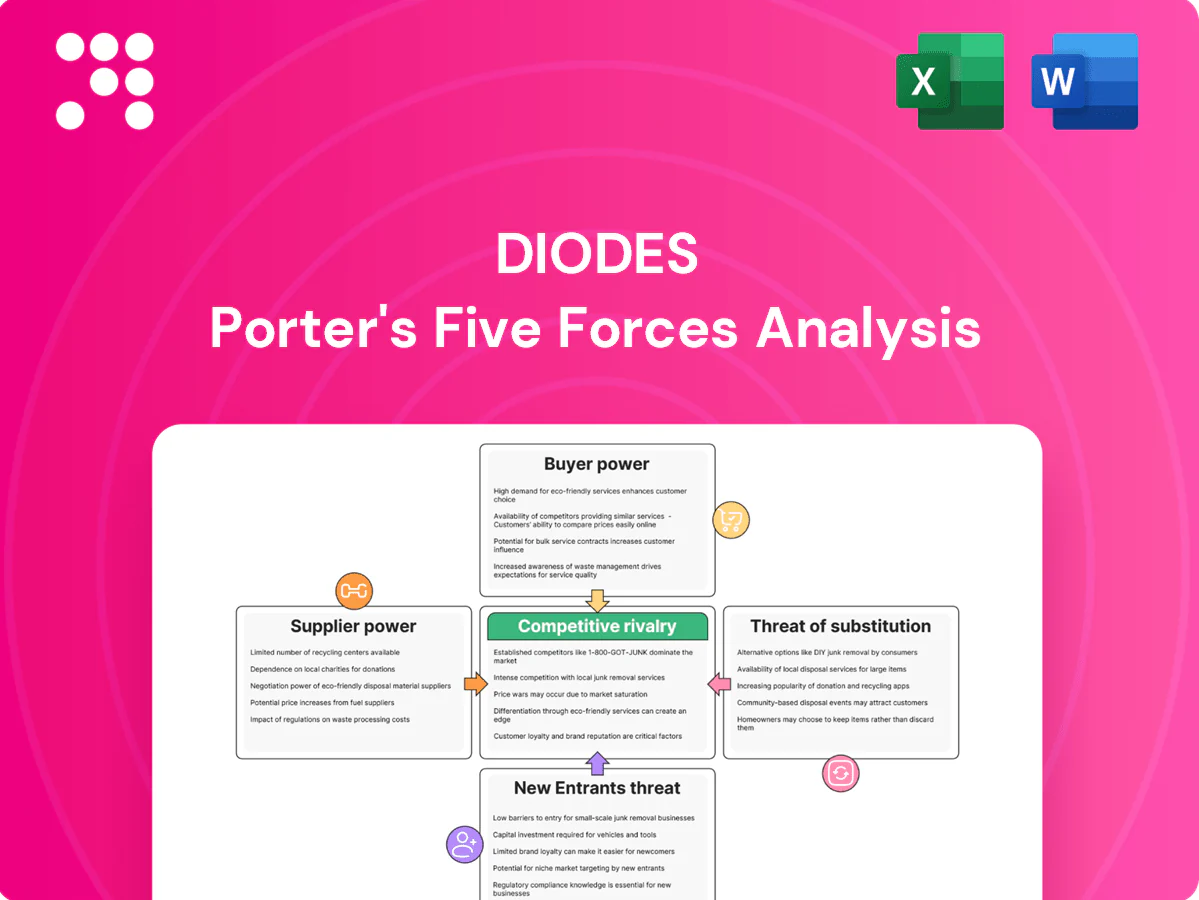

Diodes’s Porter’s Five Forces snapshot highlights moderate supplier power, intense rivalry, and rising substitute and entrant threats from tech shifts that pressure margins; niche product strength offers some defense. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Diodes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundries

Wafer foundries and OSATs remain concentrated—TSMC held over 50% of foundry revenue in 2024 and the top three OSATs captured roughly 60% of OSAT revenue—giving suppliers pricing and allocation leverage. Diodes’ reliance on leading nodes for analog/mixed‑signal and specialty processes heightens exposure. Multi‑sourcing reduces risk but qualification complexity limits feasibility. Long lead times in tight cycles shift power to suppliers.

Specialty materials

Silicon wafers, SiC/GaN substrates and specialty gases/chemicals are supplied by few qualified vendors, so tight upstream supply raises input costs and can constrain Diodes’ output; long‑term agreements mitigate risk but shortages amplify supplier power. Automotive‑grade qualification typically takes 12–24 months, further narrowing approved suppliers and increasing procurement leverage and lead times.

Tooling and EDA lock-in

Semiconductor tools, EDA software and test equipment create high switching frictions—EDA market size was about $13.5 billion in 2024 and major tool vendors maintain deep, proprietary stacks. Vendor-specific ecosystems and IP libraries lock processes and designs, raising practical exit costs. License and maintenance fees can be negotiated but remain sticky, and migration risks (often millions in requalification) keep supplier power elevated.

Capacity cycles

In up-cycles capacity is scarce and suppliers prioritize higher‑margin customers, using allocation policies and expedite fees to raise leverage; industry fab utilization moved from pandemic peaks toward roughly 80% in 2024, easing some pressure. In down‑cycles bargaining power shifts back to buyers as lead times shorten and prices soften. Diodes needs LTAs for security but must embed flexibility clauses to navigate volatility and allocation risk.

- Up-cycle: supplier leverage via allocation, expedite fees

- 2024: fab utilization ~80%, easing supplier scarcity

- Down-cycle: buyer leverage returns with shorter lead times

- Diodes: balance LTAs with flexibility clauses

Geo-logistics exposure

Global supply chains face mounting geopolitical, export-control and logistics risks that heighten supplier leverage; Asia accounts for over 75% of global semiconductor manufacturing capacity and TSMC held roughly 54% of the global foundry market in 2024. Regional concentration in Asia raises disruption potential; diversification and buffer inventory mitigate but cannot eliminate shocks. During disruptions suppliers often pass through higher input and freight costs, reinforcing their bargaining power.

- Asia concentration: >75% of fab capacity (2024)

- TSMC foundry share: ~54% (2024)

- Mitigants: diversification, buffer inventory — not full protection

Foundry ~54%, top-3 OSATs ~60% concentrate supply; Asia >75% capacity

Suppliers exert elevated power: TSMC ~54% foundry share and top‑3 OSATs ~60% (2024) concentrate upstream; Asia >75% of fab capacity. EDA market ~$13.5B (2024) and proprietary tools raise switching costs; wafer/SiC/GaN vendors are few. Fab utilization ~80% (2024) tightens allocation in up‑cycles; automotive qual takes 12–24 months, limiting multi‑sourcing.

| Metric | 2024 value |

|---|---|

| TSMC foundry share | ~54% |

| Top‑3 OSAT share | ~60% |

| EDA market | $13.5B |

| Fab capacity in Asia | >75% |

| Fab utilization | ~80% |

What is included in the product

Concise Porter's Five Forces analysis of Diodes, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry-specific disruptors; evaluates how these forces shape pricing, margins, and strategic positioning within the semiconductor component market.

One-sheet Porter's Five Forces for Diodes—instantly highlights supplier, buyer, rivalry, entrant and substitute pressures to speed strategic decisions; customizable pressure levels and a spider chart make evolving market threats and opportunities clear at a glance.

Customers Bargaining Power

Concentrated OEMs/distributors

Large OEMs, Tier-1s and major distributors aggregate demand—Diodes faces concentrated buying power with the top 5 customers/distributors accounting for roughly 40% of revenue in 2024, enabling sustained price pressure and tighter payment and service terms.

Preferred-vendor status increasingly requires volume rebates, fill-rate and on-time delivery metrics tied to quarterly performance; noncompliance can trigger financial penalties or loss of status.

Losing a top account can cut quarterly volumes by double-digit percentages and materially dent margins and working-capital needs.

Price transparency

Discrete and standard analog parts are highly commoditized with visible market pricing; in 2024 electronic marketplaces listed over 30 million SKUs, enabling instant price comparison. Cross-referencing and parametric search increase buyers’ ability to compare and switch, intensifying churn. RFQs routinely force competitive bidding across multiple vendors, putting ASPs under pressure absent strong product or supply-chain differentiation.

Qualification stickiness

Product qualifications, particularly automotive and industrial, raise switching costs through 12–36 month PPAP/AEC cycles and mandated dual-sourcing by many OEMs, slowing vendor changes. Second-sourcing remains common, preserving buyer leverage despite qualification barriers. Multi-year lifecycles of 5–15 years mean design-in wins can lock demand if supplier performance and support remain strong.

Demand cyclicality

End-market cyclicality drives inventory corrections and order pushouts, with customers renegotiating terms when volumes swing over 20% year-over-year; VMI/consignment programs and flexible LTAs absorb variability, while forecast accuracy (variance >15%) becomes a key negotiation lever for Diodes and its buyers.

- Volume swings >20%

- Forecast variance >15%

- VMI/consignment as leverage

- Flexible LTAs used to reprice

Value-added solutions

Application-specific, high-reliability, and power-efficiency parts from Diodes reduce direct comparability across suppliers, limiting buyer leverage; strong FAE support and extensive reference designs further lower customer bargaining power by speeding integration and reducing design risk. A broader product portfolio simplifies procurement and enables bundle pricing, while performance and reliability often outweigh lowest-price bidding in critical systems.

- Application-specific parts reduce commoditization

- FAE support and reference designs cut buyer switching costs

- Broad portfolio enables bundled procurement

- Reliability/performance can trump price in critical applications

Top-5 hold ≈ 40%; 30M+ SKUs pressure prices

Top 5 customers/distributors ≈40% of revenue in 2024, concentrating buying power and pressuring price, payment and service terms.

30M+ SKUs on electronic marketplaces in 2024 plus RFQ sourcing keep ASPs under pressure, though 12–36 month automotive/industrial qualifications and dual-sourcing slow switching.

Volume swings >20% and forecast variance >15% make VMI/consignment and flexible LTAs key buyer levers; application-specific parts, FAE support and bundled offers can preserve premium pricing.

| Metric | 2024 Value | Implication |

|---|---|---|

| Top-5 revenue | ≈40% | High buyer leverage |

| Market SKUs | 30M+ | Price transparency |

| Forecast variance | >15% | Negotiation leverage |

Full Version Awaits

Diodes Porter's Five Forces Analysis

This preview presents the Diodes Porter's Five Forces Analysis exactly as delivered upon purchase—no placeholders or samples. The full, professionally formatted document you see here is ready for immediate download and use the moment you complete your order. What’s shown is the actual file you’ll receive. No surprises, just the finished analysis.

Don't Miss the Bigger Picture

Diodes’s Porter’s Five Forces snapshot highlights moderate supplier power, intense rivalry, and rising substitute and entrant threats from tech shifts that pressure margins; niche product strength offers some defense. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Diodes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundries

Wafer foundries and OSATs remain concentrated—TSMC held over 50% of foundry revenue in 2024 and the top three OSATs captured roughly 60% of OSAT revenue—giving suppliers pricing and allocation leverage. Diodes’ reliance on leading nodes for analog/mixed‑signal and specialty processes heightens exposure. Multi‑sourcing reduces risk but qualification complexity limits feasibility. Long lead times in tight cycles shift power to suppliers.

Specialty materials

Silicon wafers, SiC/GaN substrates and specialty gases/chemicals are supplied by few qualified vendors, so tight upstream supply raises input costs and can constrain Diodes’ output; long‑term agreements mitigate risk but shortages amplify supplier power. Automotive‑grade qualification typically takes 12–24 months, further narrowing approved suppliers and increasing procurement leverage and lead times.

Tooling and EDA lock-in

Semiconductor tools, EDA software and test equipment create high switching frictions—EDA market size was about $13.5 billion in 2024 and major tool vendors maintain deep, proprietary stacks. Vendor-specific ecosystems and IP libraries lock processes and designs, raising practical exit costs. License and maintenance fees can be negotiated but remain sticky, and migration risks (often millions in requalification) keep supplier power elevated.

Capacity cycles

In up-cycles capacity is scarce and suppliers prioritize higher‑margin customers, using allocation policies and expedite fees to raise leverage; industry fab utilization moved from pandemic peaks toward roughly 80% in 2024, easing some pressure. In down‑cycles bargaining power shifts back to buyers as lead times shorten and prices soften. Diodes needs LTAs for security but must embed flexibility clauses to navigate volatility and allocation risk.

- Up-cycle: supplier leverage via allocation, expedite fees

- 2024: fab utilization ~80%, easing supplier scarcity

- Down-cycle: buyer leverage returns with shorter lead times

- Diodes: balance LTAs with flexibility clauses

Geo-logistics exposure

Global supply chains face mounting geopolitical, export-control and logistics risks that heighten supplier leverage; Asia accounts for over 75% of global semiconductor manufacturing capacity and TSMC held roughly 54% of the global foundry market in 2024. Regional concentration in Asia raises disruption potential; diversification and buffer inventory mitigate but cannot eliminate shocks. During disruptions suppliers often pass through higher input and freight costs, reinforcing their bargaining power.

- Asia concentration: >75% of fab capacity (2024)

- TSMC foundry share: ~54% (2024)

- Mitigants: diversification, buffer inventory — not full protection

Foundry ~54%, top-3 OSATs ~60% concentrate supply; Asia >75% capacity

Suppliers exert elevated power: TSMC ~54% foundry share and top‑3 OSATs ~60% (2024) concentrate upstream; Asia >75% of fab capacity. EDA market ~$13.5B (2024) and proprietary tools raise switching costs; wafer/SiC/GaN vendors are few. Fab utilization ~80% (2024) tightens allocation in up‑cycles; automotive qual takes 12–24 months, limiting multi‑sourcing.

| Metric | 2024 value |

|---|---|

| TSMC foundry share | ~54% |

| Top‑3 OSAT share | ~60% |

| EDA market | $13.5B |

| Fab capacity in Asia | >75% |

| Fab utilization | ~80% |

What is included in the product

Concise Porter's Five Forces analysis of Diodes, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry-specific disruptors; evaluates how these forces shape pricing, margins, and strategic positioning within the semiconductor component market.

One-sheet Porter's Five Forces for Diodes—instantly highlights supplier, buyer, rivalry, entrant and substitute pressures to speed strategic decisions; customizable pressure levels and a spider chart make evolving market threats and opportunities clear at a glance.

Customers Bargaining Power

Concentrated OEMs/distributors

Large OEMs, Tier-1s and major distributors aggregate demand—Diodes faces concentrated buying power with the top 5 customers/distributors accounting for roughly 40% of revenue in 2024, enabling sustained price pressure and tighter payment and service terms.

Preferred-vendor status increasingly requires volume rebates, fill-rate and on-time delivery metrics tied to quarterly performance; noncompliance can trigger financial penalties or loss of status.

Losing a top account can cut quarterly volumes by double-digit percentages and materially dent margins and working-capital needs.

Price transparency

Discrete and standard analog parts are highly commoditized with visible market pricing; in 2024 electronic marketplaces listed over 30 million SKUs, enabling instant price comparison. Cross-referencing and parametric search increase buyers’ ability to compare and switch, intensifying churn. RFQs routinely force competitive bidding across multiple vendors, putting ASPs under pressure absent strong product or supply-chain differentiation.

Qualification stickiness

Product qualifications, particularly automotive and industrial, raise switching costs through 12–36 month PPAP/AEC cycles and mandated dual-sourcing by many OEMs, slowing vendor changes. Second-sourcing remains common, preserving buyer leverage despite qualification barriers. Multi-year lifecycles of 5–15 years mean design-in wins can lock demand if supplier performance and support remain strong.

Demand cyclicality

End-market cyclicality drives inventory corrections and order pushouts, with customers renegotiating terms when volumes swing over 20% year-over-year; VMI/consignment programs and flexible LTAs absorb variability, while forecast accuracy (variance >15%) becomes a key negotiation lever for Diodes and its buyers.

- Volume swings >20%

- Forecast variance >15%

- VMI/consignment as leverage

- Flexible LTAs used to reprice

Value-added solutions

Application-specific, high-reliability, and power-efficiency parts from Diodes reduce direct comparability across suppliers, limiting buyer leverage; strong FAE support and extensive reference designs further lower customer bargaining power by speeding integration and reducing design risk. A broader product portfolio simplifies procurement and enables bundle pricing, while performance and reliability often outweigh lowest-price bidding in critical systems.

- Application-specific parts reduce commoditization

- FAE support and reference designs cut buyer switching costs

- Broad portfolio enables bundled procurement

- Reliability/performance can trump price in critical applications

Top-5 hold ≈ 40%; 30M+ SKUs pressure prices

Top 5 customers/distributors ≈40% of revenue in 2024, concentrating buying power and pressuring price, payment and service terms.

30M+ SKUs on electronic marketplaces in 2024 plus RFQ sourcing keep ASPs under pressure, though 12–36 month automotive/industrial qualifications and dual-sourcing slow switching.

Volume swings >20% and forecast variance >15% make VMI/consignment and flexible LTAs key buyer levers; application-specific parts, FAE support and bundled offers can preserve premium pricing.

| Metric | 2024 Value | Implication |

|---|---|---|

| Top-5 revenue | ≈40% | High buyer leverage |

| Market SKUs | 30M+ | Price transparency |

| Forecast variance | >15% | Negotiation leverage |

Full Version Awaits

Diodes Porter's Five Forces Analysis

This preview presents the Diodes Porter's Five Forces Analysis exactly as delivered upon purchase—no placeholders or samples. The full, professionally formatted document you see here is ready for immediate download and use the moment you complete your order. What’s shown is the actual file you’ll receive. No surprises, just the finished analysis.

Description

Don't Miss the Bigger Picture

Diodes’s Porter’s Five Forces snapshot highlights moderate supplier power, intense rivalry, and rising substitute and entrant threats from tech shifts that pressure margins; niche product strength offers some defense. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Diodes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundries

Wafer foundries and OSATs remain concentrated—TSMC held over 50% of foundry revenue in 2024 and the top three OSATs captured roughly 60% of OSAT revenue—giving suppliers pricing and allocation leverage. Diodes’ reliance on leading nodes for analog/mixed‑signal and specialty processes heightens exposure. Multi‑sourcing reduces risk but qualification complexity limits feasibility. Long lead times in tight cycles shift power to suppliers.

Specialty materials

Silicon wafers, SiC/GaN substrates and specialty gases/chemicals are supplied by few qualified vendors, so tight upstream supply raises input costs and can constrain Diodes’ output; long‑term agreements mitigate risk but shortages amplify supplier power. Automotive‑grade qualification typically takes 12–24 months, further narrowing approved suppliers and increasing procurement leverage and lead times.

Tooling and EDA lock-in

Semiconductor tools, EDA software and test equipment create high switching frictions—EDA market size was about $13.5 billion in 2024 and major tool vendors maintain deep, proprietary stacks. Vendor-specific ecosystems and IP libraries lock processes and designs, raising practical exit costs. License and maintenance fees can be negotiated but remain sticky, and migration risks (often millions in requalification) keep supplier power elevated.

Capacity cycles

In up-cycles capacity is scarce and suppliers prioritize higher‑margin customers, using allocation policies and expedite fees to raise leverage; industry fab utilization moved from pandemic peaks toward roughly 80% in 2024, easing some pressure. In down‑cycles bargaining power shifts back to buyers as lead times shorten and prices soften. Diodes needs LTAs for security but must embed flexibility clauses to navigate volatility and allocation risk.

- Up-cycle: supplier leverage via allocation, expedite fees

- 2024: fab utilization ~80%, easing supplier scarcity

- Down-cycle: buyer leverage returns with shorter lead times

- Diodes: balance LTAs with flexibility clauses

Geo-logistics exposure

Global supply chains face mounting geopolitical, export-control and logistics risks that heighten supplier leverage; Asia accounts for over 75% of global semiconductor manufacturing capacity and TSMC held roughly 54% of the global foundry market in 2024. Regional concentration in Asia raises disruption potential; diversification and buffer inventory mitigate but cannot eliminate shocks. During disruptions suppliers often pass through higher input and freight costs, reinforcing their bargaining power.

- Asia concentration: >75% of fab capacity (2024)

- TSMC foundry share: ~54% (2024)

- Mitigants: diversification, buffer inventory — not full protection

Foundry ~54%, top-3 OSATs ~60% concentrate supply; Asia >75% capacity

Suppliers exert elevated power: TSMC ~54% foundry share and top‑3 OSATs ~60% (2024) concentrate upstream; Asia >75% of fab capacity. EDA market ~$13.5B (2024) and proprietary tools raise switching costs; wafer/SiC/GaN vendors are few. Fab utilization ~80% (2024) tightens allocation in up‑cycles; automotive qual takes 12–24 months, limiting multi‑sourcing.

| Metric | 2024 value |

|---|---|

| TSMC foundry share | ~54% |

| Top‑3 OSAT share | ~60% |

| EDA market | $13.5B |

| Fab capacity in Asia | >75% |

| Fab utilization | ~80% |

What is included in the product

Concise Porter's Five Forces analysis of Diodes, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry-specific disruptors; evaluates how these forces shape pricing, margins, and strategic positioning within the semiconductor component market.

One-sheet Porter's Five Forces for Diodes—instantly highlights supplier, buyer, rivalry, entrant and substitute pressures to speed strategic decisions; customizable pressure levels and a spider chart make evolving market threats and opportunities clear at a glance.

Customers Bargaining Power

Concentrated OEMs/distributors

Large OEMs, Tier-1s and major distributors aggregate demand—Diodes faces concentrated buying power with the top 5 customers/distributors accounting for roughly 40% of revenue in 2024, enabling sustained price pressure and tighter payment and service terms.

Preferred-vendor status increasingly requires volume rebates, fill-rate and on-time delivery metrics tied to quarterly performance; noncompliance can trigger financial penalties or loss of status.

Losing a top account can cut quarterly volumes by double-digit percentages and materially dent margins and working-capital needs.

Price transparency

Discrete and standard analog parts are highly commoditized with visible market pricing; in 2024 electronic marketplaces listed over 30 million SKUs, enabling instant price comparison. Cross-referencing and parametric search increase buyers’ ability to compare and switch, intensifying churn. RFQs routinely force competitive bidding across multiple vendors, putting ASPs under pressure absent strong product or supply-chain differentiation.

Qualification stickiness

Product qualifications, particularly automotive and industrial, raise switching costs through 12–36 month PPAP/AEC cycles and mandated dual-sourcing by many OEMs, slowing vendor changes. Second-sourcing remains common, preserving buyer leverage despite qualification barriers. Multi-year lifecycles of 5–15 years mean design-in wins can lock demand if supplier performance and support remain strong.

Demand cyclicality

End-market cyclicality drives inventory corrections and order pushouts, with customers renegotiating terms when volumes swing over 20% year-over-year; VMI/consignment programs and flexible LTAs absorb variability, while forecast accuracy (variance >15%) becomes a key negotiation lever for Diodes and its buyers.

- Volume swings >20%

- Forecast variance >15%

- VMI/consignment as leverage

- Flexible LTAs used to reprice

Value-added solutions

Application-specific, high-reliability, and power-efficiency parts from Diodes reduce direct comparability across suppliers, limiting buyer leverage; strong FAE support and extensive reference designs further lower customer bargaining power by speeding integration and reducing design risk. A broader product portfolio simplifies procurement and enables bundle pricing, while performance and reliability often outweigh lowest-price bidding in critical systems.

- Application-specific parts reduce commoditization

- FAE support and reference designs cut buyer switching costs

- Broad portfolio enables bundled procurement

- Reliability/performance can trump price in critical applications

Top-5 hold ≈ 40%; 30M+ SKUs pressure prices

Top 5 customers/distributors ≈40% of revenue in 2024, concentrating buying power and pressuring price, payment and service terms.

30M+ SKUs on electronic marketplaces in 2024 plus RFQ sourcing keep ASPs under pressure, though 12–36 month automotive/industrial qualifications and dual-sourcing slow switching.

Volume swings >20% and forecast variance >15% make VMI/consignment and flexible LTAs key buyer levers; application-specific parts, FAE support and bundled offers can preserve premium pricing.

| Metric | 2024 Value | Implication |

|---|---|---|

| Top-5 revenue | ≈40% | High buyer leverage |

| Market SKUs | 30M+ | Price transparency |

| Forecast variance | >15% | Negotiation leverage |

Full Version Awaits

Diodes Porter's Five Forces Analysis

This preview presents the Diodes Porter's Five Forces Analysis exactly as delivered upon purchase—no placeholders or samples. The full, professionally formatted document you see here is ready for immediate download and use the moment you complete your order. What’s shown is the actual file you’ll receive. No surprises, just the finished analysis.