Christian Dior Porter's Five Forces Analysis

Don't Miss the Bigger Picture

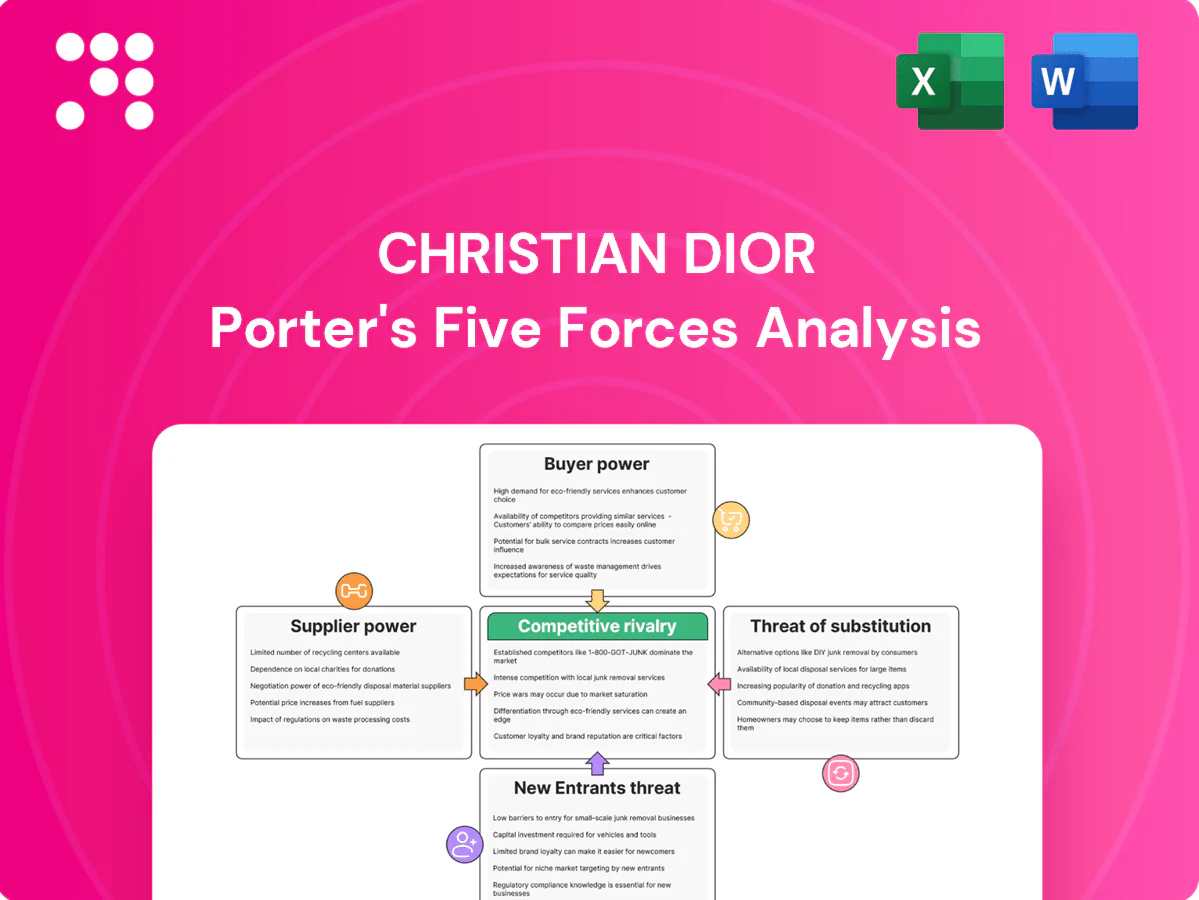

Christian Dior faces intense rivalry, strong buyer expectations, high supplier prestige, moderate entry barriers, and evolving substitute threats shaping luxury dynamics. This snapshot highlights strategic pressure points and competitive levers influencing Dior’s market positioning. Unlock the full Porter's Five Forces Analysis to explore Christian Dior’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce artisanal inputs

Scarce artisanal inputs — high-end leathers, exotic skins, precious stones, rare fragrance molecules and Grand Cru vineyards (Champagne has 17 Grands Crus) — are tightly regulated, with CITES (183 parties) and Kimberley/appellation rules raising supplier leverage. Dior/LVMH, the world’s largest luxury group with ~75 maisons, uses scale and quotas to secure supply, yet availability shocks can sharply raise costs. Long-term contracts and vertical assets (owned wineries, in‑house ateliers) partially mitigate this power.

Craftsmanship concentration

Master ateliers, embroiderers and watch/jewelry artisans for Dior are few and capacity-constrained, making their skills non-fungible and raising switching costs and lead times for seasonal collections. Competition from rival maisons for the same workshops increases supplier bargaining power, especially during peak couture cycles. Dior’s selective in-house Métiers d’Art acquisitions reduce but do not eliminate reliance on external masters.

Vertical integration dampener

LVMH's vertical integration—owning tanneries, vineyards, fragrance labs and in-house ateliers—substantially reduces external supplier clout, with the group operating over 70 production sites as of 2024. Backward integration secures quality, secrecy and priority allocation for Christian Dior, while giving strong benchmarking power in price and lead-time negotiations. Remaining exposure persists because certain specialty components and raw materials cannot be fully internalized.

ESG and traceability pressures

Tighter traceability, animal welfare and sustainable sourcing requirements, reinforced by the EU Deforestation Regulation coming into effect in late 2024, shrink Dior’s eligible supplier pool and increase reliance on certified upstream partners. Compliance costs and certification create leverage for those suppliers, while any proven breach poses material reputational risk that discourages aggressive supplier switching. Dior mitigates by multi-sourcing among audited, certified suppliers to balance supply risk and bargaining power.

- Traceability: EUDR (effective 2024) raises verification costs

- Supplier leverage: certified partners capture pricing power

- Reputational risk: breaches limit Dior’s switching

- Mitigation: multi-sourcing + audited partners

Logistics and lead-time rigidity

Luxury quality and handcrafted processes routinely extend lead times to 4–12 weeks, embedding supplier schedules into Dior product calendars; expedites can cost 2–3x and are limited, raising dependence during peak seasons when demand can surge 20–40%. Dior’s advanced forecasting reduces waste, but tourism swings and China volatility in 2024 still strain capacity and let suppliers negotiate priority premiums of 5–15%.

- Lead times: 4–12 weeks

- Expedite cost: 2–3x

- Peak surge: +20–40%

- Supplier premium: 5–15%

Regulated inputs, long lead times and EUDR 2024 boost supplier premiums and leverage

Scarce regulated inputs (CITES 183 parties) and specialist ateliers raise supplier leverage; Dior benefits from LVMH scale (~75 maisons) and 70+ production sites (2024) but cannot fully internalize specialty components. Lead times 4–12 weeks and expedite costs 2–3x enable supplier premiums (5–15%) during peak surges; EUDR (effective 2024) narrows eligible suppliers, increasing certified-partner power.

| Metric | Value |

|---|---|

| CITES parties | 183 |

| LVMH maisons (approx.) | ~75 |

| Production sites (2024) | 70+ |

| Lead times | 4–12 weeks |

| Supplier premium | 5–15% |

| EUDR effective | 2024 |

What is included in the product

Tailored exclusively for Christian Dior, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, entry barriers and substitutes, and highlights disruptive threats and strategic levers shaping Dior’s pricing power and profitability.

A concise, one-sheet Porter's Five Forces for Christian Dior that visualizes competitive pressures with a radar chart, lets you swap in current inputs, and integrates into decks—no macros, ready for quick strategic decisions.

Customers Bargaining Power

Low price sensitivity, high expectations

Affluent Dior clients exhibit low price sensitivity but demand flawless quality and service; LVMH reported Dior-led Fashion & Leather Goods driving group revenue to €86.7bn in 2024, reflecting willingness to pay rather than discount-seeking. That reduces direct price pressure but heightens performance pressure: any lapse risks switching to peer maisons like Chanel or Gucci. Perceived value hinges on heritage, exclusivity and experience, not discounts.

Brand equity and loyalty moat

Dior’s iconic branding and couture halo materially reduce buyer leverage; as a key driver of LVMH’s Fashion & Leather Goods division (about €34bn in 2024), Dior commands pricing power. Signature lines and limited editions create scarcity that flips power toward the house, while waitlists and clienteling deepen switching costs. Loyalty still requires continuous novelty and craftsmanship to sustain retention.

Direct retail control

Owned boutiques and e-commerce (over 200 boutiques worldwide in 2024) minimize intermediary power and discounting, letting Dior control pricing, assortment and client experience and thus constrain buyer bargaining. First-party client data in 2024 enabled personalized offers and CRM-driven retention rather than price concessions. Wholesale in beauty remains broader but curated via partners like Sephora and duty-free channels.

Social media transparency

Social media transparency—reviews, influencers and 2024 resale market visibility (resale market ~ $33bn in 2024)—drives near-instant information symmetry; customers benchmark across brands and collections in real time, raising qualitative bargaining power even where prices remain stable. Dior must defend premiums through storytelling and perceived scarcity to retain margin.

- Reviews boost cross-brand comparison

- Influencers amplify product signals

- Resale prices set external benchmarks

- Storytelling and scarcity justify premiums

Regional and segment mix

Chinese, US and Middle Eastern clientele drove Dior volumes in 2024, with Asia ex-Japan ~40% and North America ~30% of luxury demand while Middle East showed double-digit growth, producing divergent tastes and purchase cycles. Travel retail and macro swings (tourism recovery +8–12% in 2024) shift customer leverage episodically. Beauty buyers—larger in number and slightly more price-aware—anchor recurring revenue, while a tiered product ladder (beauty, ready-to-wear, couture) balances broad reach with maintained exclusivity.

- Regional mix: Asia ex-Japan ~40%

- North America ~30%

- Middle East: double-digit growth 2024

- Travel retail impact: +8–12% tourism rebound

- Beauty vs couture: beauty = larger, more price-sensitive base

Affluent luxury clients show low price sensitivity; exclusivity and resale sustain pricing power

Affluent Dior clients show low price sensitivity but demand impeccable quality; LVMH reported €86.7bn group revenue in 2024 with Dior-led Fashion & Leather Goods ~€34bn, supporting pricing power. Brand exclusivity, waitlists and clienteling raise switching costs, while social media and a $33bn resale market increase informational leverage. Owned >200 boutiques and CRM limit intermediary bargaining.

| Metric | 2024 |

|---|---|

| Group revenue (LVMH) | €86.7bn |

| Dior F&LG | €34bn |

| Boutiques | >200 |

| Resale market | $33bn |

| Asia ex-Japan | ~40% |

Preview the Actual Deliverable

Christian Dior Porter's Five Forces Analysis

This preview shows the exact Christian Dior Porter's Five Forces Analysis you'll receive upon purchase—fully researched and professionally formatted, with no placeholders or mockups. The document displayed here is the complete, ready-to-use file available for immediate download after payment. You're viewing the final deliverable, identical to the file delivered to customers.

Don't Miss the Bigger Picture

Christian Dior faces intense rivalry, strong buyer expectations, high supplier prestige, moderate entry barriers, and evolving substitute threats shaping luxury dynamics. This snapshot highlights strategic pressure points and competitive levers influencing Dior’s market positioning. Unlock the full Porter's Five Forces Analysis to explore Christian Dior’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce artisanal inputs

Scarce artisanal inputs — high-end leathers, exotic skins, precious stones, rare fragrance molecules and Grand Cru vineyards (Champagne has 17 Grands Crus) — are tightly regulated, with CITES (183 parties) and Kimberley/appellation rules raising supplier leverage. Dior/LVMH, the world’s largest luxury group with ~75 maisons, uses scale and quotas to secure supply, yet availability shocks can sharply raise costs. Long-term contracts and vertical assets (owned wineries, in‑house ateliers) partially mitigate this power.

Craftsmanship concentration

Master ateliers, embroiderers and watch/jewelry artisans for Dior are few and capacity-constrained, making their skills non-fungible and raising switching costs and lead times for seasonal collections. Competition from rival maisons for the same workshops increases supplier bargaining power, especially during peak couture cycles. Dior’s selective in-house Métiers d’Art acquisitions reduce but do not eliminate reliance on external masters.

Vertical integration dampener

LVMH's vertical integration—owning tanneries, vineyards, fragrance labs and in-house ateliers—substantially reduces external supplier clout, with the group operating over 70 production sites as of 2024. Backward integration secures quality, secrecy and priority allocation for Christian Dior, while giving strong benchmarking power in price and lead-time negotiations. Remaining exposure persists because certain specialty components and raw materials cannot be fully internalized.

ESG and traceability pressures

Tighter traceability, animal welfare and sustainable sourcing requirements, reinforced by the EU Deforestation Regulation coming into effect in late 2024, shrink Dior’s eligible supplier pool and increase reliance on certified upstream partners. Compliance costs and certification create leverage for those suppliers, while any proven breach poses material reputational risk that discourages aggressive supplier switching. Dior mitigates by multi-sourcing among audited, certified suppliers to balance supply risk and bargaining power.

- Traceability: EUDR (effective 2024) raises verification costs

- Supplier leverage: certified partners capture pricing power

- Reputational risk: breaches limit Dior’s switching

- Mitigation: multi-sourcing + audited partners

Logistics and lead-time rigidity

Luxury quality and handcrafted processes routinely extend lead times to 4–12 weeks, embedding supplier schedules into Dior product calendars; expedites can cost 2–3x and are limited, raising dependence during peak seasons when demand can surge 20–40%. Dior’s advanced forecasting reduces waste, but tourism swings and China volatility in 2024 still strain capacity and let suppliers negotiate priority premiums of 5–15%.

- Lead times: 4–12 weeks

- Expedite cost: 2–3x

- Peak surge: +20–40%

- Supplier premium: 5–15%

Regulated inputs, long lead times and EUDR 2024 boost supplier premiums and leverage

Scarce regulated inputs (CITES 183 parties) and specialist ateliers raise supplier leverage; Dior benefits from LVMH scale (~75 maisons) and 70+ production sites (2024) but cannot fully internalize specialty components. Lead times 4–12 weeks and expedite costs 2–3x enable supplier premiums (5–15%) during peak surges; EUDR (effective 2024) narrows eligible suppliers, increasing certified-partner power.

| Metric | Value |

|---|---|

| CITES parties | 183 |

| LVMH maisons (approx.) | ~75 |

| Production sites (2024) | 70+ |

| Lead times | 4–12 weeks |

| Supplier premium | 5–15% |

| EUDR effective | 2024 |

What is included in the product

Tailored exclusively for Christian Dior, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, entry barriers and substitutes, and highlights disruptive threats and strategic levers shaping Dior’s pricing power and profitability.

A concise, one-sheet Porter's Five Forces for Christian Dior that visualizes competitive pressures with a radar chart, lets you swap in current inputs, and integrates into decks—no macros, ready for quick strategic decisions.

Customers Bargaining Power

Low price sensitivity, high expectations

Affluent Dior clients exhibit low price sensitivity but demand flawless quality and service; LVMH reported Dior-led Fashion & Leather Goods driving group revenue to €86.7bn in 2024, reflecting willingness to pay rather than discount-seeking. That reduces direct price pressure but heightens performance pressure: any lapse risks switching to peer maisons like Chanel or Gucci. Perceived value hinges on heritage, exclusivity and experience, not discounts.

Brand equity and loyalty moat

Dior’s iconic branding and couture halo materially reduce buyer leverage; as a key driver of LVMH’s Fashion & Leather Goods division (about €34bn in 2024), Dior commands pricing power. Signature lines and limited editions create scarcity that flips power toward the house, while waitlists and clienteling deepen switching costs. Loyalty still requires continuous novelty and craftsmanship to sustain retention.

Direct retail control

Owned boutiques and e-commerce (over 200 boutiques worldwide in 2024) minimize intermediary power and discounting, letting Dior control pricing, assortment and client experience and thus constrain buyer bargaining. First-party client data in 2024 enabled personalized offers and CRM-driven retention rather than price concessions. Wholesale in beauty remains broader but curated via partners like Sephora and duty-free channels.

Social media transparency

Social media transparency—reviews, influencers and 2024 resale market visibility (resale market ~ $33bn in 2024)—drives near-instant information symmetry; customers benchmark across brands and collections in real time, raising qualitative bargaining power even where prices remain stable. Dior must defend premiums through storytelling and perceived scarcity to retain margin.

- Reviews boost cross-brand comparison

- Influencers amplify product signals

- Resale prices set external benchmarks

- Storytelling and scarcity justify premiums

Regional and segment mix

Chinese, US and Middle Eastern clientele drove Dior volumes in 2024, with Asia ex-Japan ~40% and North America ~30% of luxury demand while Middle East showed double-digit growth, producing divergent tastes and purchase cycles. Travel retail and macro swings (tourism recovery +8–12% in 2024) shift customer leverage episodically. Beauty buyers—larger in number and slightly more price-aware—anchor recurring revenue, while a tiered product ladder (beauty, ready-to-wear, couture) balances broad reach with maintained exclusivity.

- Regional mix: Asia ex-Japan ~40%

- North America ~30%

- Middle East: double-digit growth 2024

- Travel retail impact: +8–12% tourism rebound

- Beauty vs couture: beauty = larger, more price-sensitive base

Affluent luxury clients show low price sensitivity; exclusivity and resale sustain pricing power

Affluent Dior clients show low price sensitivity but demand impeccable quality; LVMH reported €86.7bn group revenue in 2024 with Dior-led Fashion & Leather Goods ~€34bn, supporting pricing power. Brand exclusivity, waitlists and clienteling raise switching costs, while social media and a $33bn resale market increase informational leverage. Owned >200 boutiques and CRM limit intermediary bargaining.

| Metric | 2024 |

|---|---|

| Group revenue (LVMH) | €86.7bn |

| Dior F&LG | €34bn |

| Boutiques | >200 |

| Resale market | $33bn |

| Asia ex-Japan | ~40% |

Preview the Actual Deliverable

Christian Dior Porter's Five Forces Analysis

This preview shows the exact Christian Dior Porter's Five Forces Analysis you'll receive upon purchase—fully researched and professionally formatted, with no placeholders or mockups. The document displayed here is the complete, ready-to-use file available for immediate download after payment. You're viewing the final deliverable, identical to the file delivered to customers.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Christian Dior faces intense rivalry, strong buyer expectations, high supplier prestige, moderate entry barriers, and evolving substitute threats shaping luxury dynamics. This snapshot highlights strategic pressure points and competitive levers influencing Dior’s market positioning. Unlock the full Porter's Five Forces Analysis to explore Christian Dior’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce artisanal inputs

Scarce artisanal inputs — high-end leathers, exotic skins, precious stones, rare fragrance molecules and Grand Cru vineyards (Champagne has 17 Grands Crus) — are tightly regulated, with CITES (183 parties) and Kimberley/appellation rules raising supplier leverage. Dior/LVMH, the world’s largest luxury group with ~75 maisons, uses scale and quotas to secure supply, yet availability shocks can sharply raise costs. Long-term contracts and vertical assets (owned wineries, in‑house ateliers) partially mitigate this power.

Craftsmanship concentration

Master ateliers, embroiderers and watch/jewelry artisans for Dior are few and capacity-constrained, making their skills non-fungible and raising switching costs and lead times for seasonal collections. Competition from rival maisons for the same workshops increases supplier bargaining power, especially during peak couture cycles. Dior’s selective in-house Métiers d’Art acquisitions reduce but do not eliminate reliance on external masters.

Vertical integration dampener

LVMH's vertical integration—owning tanneries, vineyards, fragrance labs and in-house ateliers—substantially reduces external supplier clout, with the group operating over 70 production sites as of 2024. Backward integration secures quality, secrecy and priority allocation for Christian Dior, while giving strong benchmarking power in price and lead-time negotiations. Remaining exposure persists because certain specialty components and raw materials cannot be fully internalized.

ESG and traceability pressures

Tighter traceability, animal welfare and sustainable sourcing requirements, reinforced by the EU Deforestation Regulation coming into effect in late 2024, shrink Dior’s eligible supplier pool and increase reliance on certified upstream partners. Compliance costs and certification create leverage for those suppliers, while any proven breach poses material reputational risk that discourages aggressive supplier switching. Dior mitigates by multi-sourcing among audited, certified suppliers to balance supply risk and bargaining power.

- Traceability: EUDR (effective 2024) raises verification costs

- Supplier leverage: certified partners capture pricing power

- Reputational risk: breaches limit Dior’s switching

- Mitigation: multi-sourcing + audited partners

Logistics and lead-time rigidity

Luxury quality and handcrafted processes routinely extend lead times to 4–12 weeks, embedding supplier schedules into Dior product calendars; expedites can cost 2–3x and are limited, raising dependence during peak seasons when demand can surge 20–40%. Dior’s advanced forecasting reduces waste, but tourism swings and China volatility in 2024 still strain capacity and let suppliers negotiate priority premiums of 5–15%.

- Lead times: 4–12 weeks

- Expedite cost: 2–3x

- Peak surge: +20–40%

- Supplier premium: 5–15%

Regulated inputs, long lead times and EUDR 2024 boost supplier premiums and leverage

Scarce regulated inputs (CITES 183 parties) and specialist ateliers raise supplier leverage; Dior benefits from LVMH scale (~75 maisons) and 70+ production sites (2024) but cannot fully internalize specialty components. Lead times 4–12 weeks and expedite costs 2–3x enable supplier premiums (5–15%) during peak surges; EUDR (effective 2024) narrows eligible suppliers, increasing certified-partner power.

| Metric | Value |

|---|---|

| CITES parties | 183 |

| LVMH maisons (approx.) | ~75 |

| Production sites (2024) | 70+ |

| Lead times | 4–12 weeks |

| Supplier premium | 5–15% |

| EUDR effective | 2024 |

What is included in the product

Tailored exclusively for Christian Dior, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, entry barriers and substitutes, and highlights disruptive threats and strategic levers shaping Dior’s pricing power and profitability.

A concise, one-sheet Porter's Five Forces for Christian Dior that visualizes competitive pressures with a radar chart, lets you swap in current inputs, and integrates into decks—no macros, ready for quick strategic decisions.

Customers Bargaining Power

Low price sensitivity, high expectations

Affluent Dior clients exhibit low price sensitivity but demand flawless quality and service; LVMH reported Dior-led Fashion & Leather Goods driving group revenue to €86.7bn in 2024, reflecting willingness to pay rather than discount-seeking. That reduces direct price pressure but heightens performance pressure: any lapse risks switching to peer maisons like Chanel or Gucci. Perceived value hinges on heritage, exclusivity and experience, not discounts.

Brand equity and loyalty moat

Dior’s iconic branding and couture halo materially reduce buyer leverage; as a key driver of LVMH’s Fashion & Leather Goods division (about €34bn in 2024), Dior commands pricing power. Signature lines and limited editions create scarcity that flips power toward the house, while waitlists and clienteling deepen switching costs. Loyalty still requires continuous novelty and craftsmanship to sustain retention.

Direct retail control

Owned boutiques and e-commerce (over 200 boutiques worldwide in 2024) minimize intermediary power and discounting, letting Dior control pricing, assortment and client experience and thus constrain buyer bargaining. First-party client data in 2024 enabled personalized offers and CRM-driven retention rather than price concessions. Wholesale in beauty remains broader but curated via partners like Sephora and duty-free channels.

Social media transparency

Social media transparency—reviews, influencers and 2024 resale market visibility (resale market ~ $33bn in 2024)—drives near-instant information symmetry; customers benchmark across brands and collections in real time, raising qualitative bargaining power even where prices remain stable. Dior must defend premiums through storytelling and perceived scarcity to retain margin.

- Reviews boost cross-brand comparison

- Influencers amplify product signals

- Resale prices set external benchmarks

- Storytelling and scarcity justify premiums

Regional and segment mix

Chinese, US and Middle Eastern clientele drove Dior volumes in 2024, with Asia ex-Japan ~40% and North America ~30% of luxury demand while Middle East showed double-digit growth, producing divergent tastes and purchase cycles. Travel retail and macro swings (tourism recovery +8–12% in 2024) shift customer leverage episodically. Beauty buyers—larger in number and slightly more price-aware—anchor recurring revenue, while a tiered product ladder (beauty, ready-to-wear, couture) balances broad reach with maintained exclusivity.

- Regional mix: Asia ex-Japan ~40%

- North America ~30%

- Middle East: double-digit growth 2024

- Travel retail impact: +8–12% tourism rebound

- Beauty vs couture: beauty = larger, more price-sensitive base

Affluent luxury clients show low price sensitivity; exclusivity and resale sustain pricing power

Affluent Dior clients show low price sensitivity but demand impeccable quality; LVMH reported €86.7bn group revenue in 2024 with Dior-led Fashion & Leather Goods ~€34bn, supporting pricing power. Brand exclusivity, waitlists and clienteling raise switching costs, while social media and a $33bn resale market increase informational leverage. Owned >200 boutiques and CRM limit intermediary bargaining.

| Metric | 2024 |

|---|---|

| Group revenue (LVMH) | €86.7bn |

| Dior F&LG | €34bn |

| Boutiques | >200 |

| Resale market | $33bn |

| Asia ex-Japan | ~40% |

Preview the Actual Deliverable

Christian Dior Porter's Five Forces Analysis

This preview shows the exact Christian Dior Porter's Five Forces Analysis you'll receive upon purchase—fully researched and professionally formatted, with no placeholders or mockups. The document displayed here is the complete, ready-to-use file available for immediate download after payment. You're viewing the final deliverable, identical to the file delivered to customers.