Dishman Carbogen Amcis Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

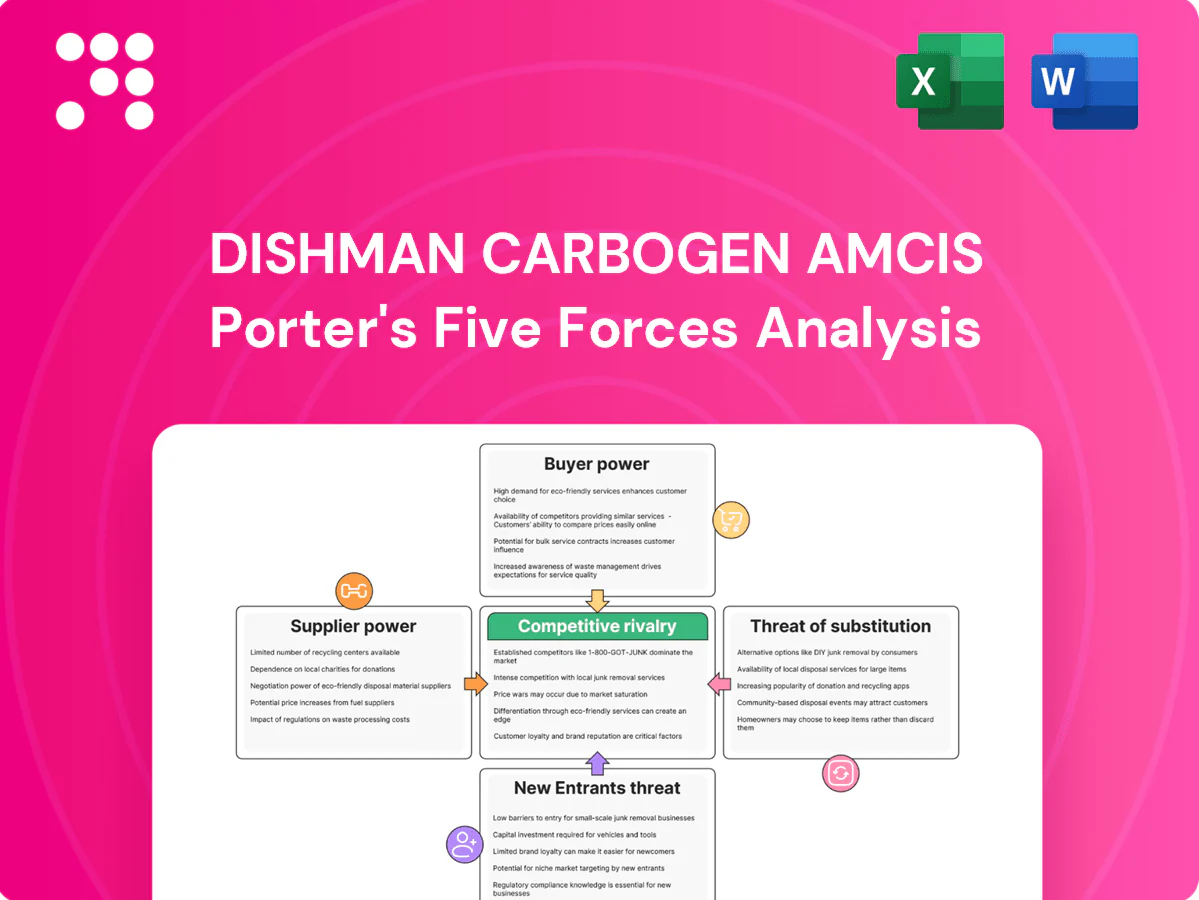

Dishman Carbogen Amcis faces moderate supplier power due to specialized raw materials, while high regulatory barriers and established client relationships limit new entrants; buyer power and substitute threats are nuanced across CDMO segments. Competitive rivalry is intense but innovation and scale offer differentiation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dishman Carbogen Amcis’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty raw materials

APIs and advanced intermediates rely on niche solvents, catalysts and high-purity reagents available from few qualified vendors, giving suppliers pricing and lead-time leverage. Qualification timelines for new suppliers typically run 6–12 months, reducing switching ease. Lead times for specialty inputs often exceed 12 weeks, so Dishman Carbogen Amcis uses dual-sourcing and multi-year contracts to mitigate risk.

Single-source equipment

Custom reactors, containment systems and HPAPI suites are often single-sourced from specialized OEMs, with HPAPI suite CAPEX commonly exceeding $10 million and custom reactor projects frequently in the multi‑million dollar range; installation, validation and maintenance dependencies therefore raise vendor leverage. Switching incurs regulatory downtime and change‑control costs that can run into hundreds of thousands per day, while multi‑year framework agreements help cap price volatility and secure spare parts.

Regulatory-grade consumables

GMP packaging, filters and chromatography media for Dishman Carbogen Amcis must meet validated standards, and any supplier change typically triggers requalification taking 2–6 months and costing tens of thousands of dollars, raising switching costs. Suppliers can dictate delivery schedules and minimum order quantities (often 1–3 months of supply), constraining flexibility. Strategic inventory buffers (1–3 months on hand) are used to manage disruptions and MOQ effects.

Energy and utilities

Continuous operations in Dishman Carbogen Amcis multipurpose plants are energy-intensive, increasing supplier leverage. Regional utility monopolies and tight grids in India raised bargaining power; industrial tariffs averaged about INR 8–10/kWh in 2024. Energy price volatility squeezed margins in 2024, while hedging and efficiency upgrades partially offset exposure.

- High consumption: continuous runs raise energy dependency

- Regional power markets: monopoly/tight grids boost supplier power

- 2024 tariffs ≈ INR 8–10/kWh; volatility hit margins

- Mitigants: hedging, efficiency upgrades

Logistics and hazardous transport

Shipping regulated chemicals and temperature-sensitive inputs narrows carrier options due to IMDG Code requirements (in force since 1965) and cold-chain mandates, raising per-shipment handling complexity and cost.

Compliance, specialized insurance and limited carriers lift logistics costs and reduce flexibility; port congestion and geopolitical chokepoints in 2024 intensified supplier leverage.

Preferred-carrier programs and long-term contracts stabilize service levels and capacity, concentrating bargaining with a handful of certified providers.

- IMDG Code compliance

- Cold-chain specialization

- Insurance & compliance premiums

- Port congestion & geopolitical risk

- Preferred-carrier stabilization

High supplier leverage: HPAPI CAPEX, long lead times and energy costs drive supply risk

Suppliers hold significant leverage due to niche reagents, long qualification (6–12 months) and lead times (>12 weeks), and high CAPEX for HPAPI suites (typically >$10m). Switching triggers 2–6 month requalification, change‑control costs often hundreds of thousands/day, and 2024 energy tariffs ≈ INR 8–10/kWh raised input costs. Long-term contracts, dual‑sourcing and inventory buffers reduce but do not eliminate supplier power.

| Item | Impact | Mitigant | Metric (2024) |

|---|---|---|---|

| HPAPI CAPEX | High vendor leverage | Multi‑year contracts | > $10m |

| Lead times | Supply risk | Dual‑sourcing, buffers | > 12 weeks |

| Energy | Cost pressure | Hedging, upgrades | INR 8–10/kWh |

What is included in the product

Tailored Porter's Five Forces analysis for Dishman Carbogen Amcis uncovers key drivers of competition, supplier and buyer power, and barriers to entry, highlighting disruptive substitutes and emerging threats to market share.

A clear, one-sheet summary of Dishman Carbogen Amcis’ Five Forces—pinpoints competitive pressures, supplier/customer risks and regulatory threats so you can relieve strategic pain points and make faster, data-driven decisions.

Customers Bargaining Power

Big pharma concentration

Large pharma and biotech clients concentrate demand via sizable, multi-year programs, forcing Dishman Carbogen Amcis to accept tight delivery schedules and long contract cycles. Their sophisticated procurement teams extract tough commercial terms, strict quality KPIs and sustained price pressure. Inclusion on preferred supplier lists commonly gates project access, though strong technical differentiation in complex APIs and ADCs limits customer leverage.

High switching costs

Transferring processes triggers tech transfer, validation and regulatory updates that commonly cost $0.5–5 million and take 6–18 months, raising tangible switching costs. Despite this, a 2024 industry survey found about 35% of pharma customers threaten or use multi-sourcing to negotiate pricing. Lifecycle risk from clinical to commercial phases makes continuity—especially with proven performance—highly valuable. Reliable on-time delivery and quality record effectively lock in relationships.

Price transparency

Benchmarking across global CDMOs reveals price variance up to 3x for comparable services, enabling clients to shop rates and yields. Open-book models in process development often compress CDMO margins and shift risk, prompting clients to demand shared-savings arrangements on yield/process gains. Clear, quantified value articulation—cost-per-kg reductions or time-to-clinic savings—counters pure price plays and preserves Dishman Carbogen Amcis's premium.

Quality and compliance demands

Customers exert strong power through zero-defect expectations and audit rights; deviations trigger chargebacks, rework, or lost contracts, pressuring Dishman Carbogen Amcis to sustain near-perfect compliance. Robust QA and inspection readiness lower concession rates and limit price or penalty exposure. A proven inspection history strengthens negotiating leverage with large pharma buyers.

- Zero-defect audits

- Chargeback/rework risk

- QA reduces concessions

- Inspection track record = leverage

Pipeline volatility

Clinical attrition (~86% aggregate failure rate) lets customers delay or cancel orders, shifting volume risk to CDMOs; buyers increasingly demand flexible capacity and take-or-pay clauses (present in ~40% of new contracts in 2024), forcing CDMOs to absorb slot risk. Volume uncertainty compresses pricing and complicates slot allocation, often cutting realized yields by 5–12%. Portfolio diversification across 30+ clients balances exposure.

- Clinical attrition ~86%

- Take-or-pay in ~40% of 2024 contracts

- Pricing hit 5–12%

- Client base 30+ to diversify

Customers Hold Leverage: 35% Multi-sourcing, 40% Take-or-Pay, High Attrition Shifts Risk

Customers exert strong bargaining power: 35% use multi-sourcing, 40% of 2024 contracts include take-or-pay, and ~86% clinical attrition shifts volume risk to CDMOs; switching costs ($0.5–5M, 6–18 months) and technical differentiation in complex APIs/ADCs partially limit leverage.

| Metric | Value |

|---|---|

| Multi-sourcing | 35% |

| Take-or-pay (2024) | 40% |

| Clinical attrition | ~86% |

| Switching cost | $0.5–5M; 6–18m |

Preview Before You Purchase

Dishman Carbogen Amcis Porter's Five Forces Analysis

This Porter's Five Forces analysis for Dishman Carbogen Amcis is the full, professionally formatted document you see here — it examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. This preview is the exact file you'll receive immediately after purchase, with no placeholders or mockups. It's ready for download and immediate use in your strategic or investment work.

A Must-Have Tool for Decision-Makers

Dishman Carbogen Amcis faces moderate supplier power due to specialized raw materials, while high regulatory barriers and established client relationships limit new entrants; buyer power and substitute threats are nuanced across CDMO segments. Competitive rivalry is intense but innovation and scale offer differentiation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dishman Carbogen Amcis’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty raw materials

APIs and advanced intermediates rely on niche solvents, catalysts and high-purity reagents available from few qualified vendors, giving suppliers pricing and lead-time leverage. Qualification timelines for new suppliers typically run 6–12 months, reducing switching ease. Lead times for specialty inputs often exceed 12 weeks, so Dishman Carbogen Amcis uses dual-sourcing and multi-year contracts to mitigate risk.

Single-source equipment

Custom reactors, containment systems and HPAPI suites are often single-sourced from specialized OEMs, with HPAPI suite CAPEX commonly exceeding $10 million and custom reactor projects frequently in the multi‑million dollar range; installation, validation and maintenance dependencies therefore raise vendor leverage. Switching incurs regulatory downtime and change‑control costs that can run into hundreds of thousands per day, while multi‑year framework agreements help cap price volatility and secure spare parts.

Regulatory-grade consumables

GMP packaging, filters and chromatography media for Dishman Carbogen Amcis must meet validated standards, and any supplier change typically triggers requalification taking 2–6 months and costing tens of thousands of dollars, raising switching costs. Suppliers can dictate delivery schedules and minimum order quantities (often 1–3 months of supply), constraining flexibility. Strategic inventory buffers (1–3 months on hand) are used to manage disruptions and MOQ effects.

Energy and utilities

Continuous operations in Dishman Carbogen Amcis multipurpose plants are energy-intensive, increasing supplier leverage. Regional utility monopolies and tight grids in India raised bargaining power; industrial tariffs averaged about INR 8–10/kWh in 2024. Energy price volatility squeezed margins in 2024, while hedging and efficiency upgrades partially offset exposure.

- High consumption: continuous runs raise energy dependency

- Regional power markets: monopoly/tight grids boost supplier power

- 2024 tariffs ≈ INR 8–10/kWh; volatility hit margins

- Mitigants: hedging, efficiency upgrades

Logistics and hazardous transport

Shipping regulated chemicals and temperature-sensitive inputs narrows carrier options due to IMDG Code requirements (in force since 1965) and cold-chain mandates, raising per-shipment handling complexity and cost.

Compliance, specialized insurance and limited carriers lift logistics costs and reduce flexibility; port congestion and geopolitical chokepoints in 2024 intensified supplier leverage.

Preferred-carrier programs and long-term contracts stabilize service levels and capacity, concentrating bargaining with a handful of certified providers.

- IMDG Code compliance

- Cold-chain specialization

- Insurance & compliance premiums

- Port congestion & geopolitical risk

- Preferred-carrier stabilization

High supplier leverage: HPAPI CAPEX, long lead times and energy costs drive supply risk

Suppliers hold significant leverage due to niche reagents, long qualification (6–12 months) and lead times (>12 weeks), and high CAPEX for HPAPI suites (typically >$10m). Switching triggers 2–6 month requalification, change‑control costs often hundreds of thousands/day, and 2024 energy tariffs ≈ INR 8–10/kWh raised input costs. Long-term contracts, dual‑sourcing and inventory buffers reduce but do not eliminate supplier power.

| Item | Impact | Mitigant | Metric (2024) |

|---|---|---|---|

| HPAPI CAPEX | High vendor leverage | Multi‑year contracts | > $10m |

| Lead times | Supply risk | Dual‑sourcing, buffers | > 12 weeks |

| Energy | Cost pressure | Hedging, upgrades | INR 8–10/kWh |

What is included in the product

Tailored Porter's Five Forces analysis for Dishman Carbogen Amcis uncovers key drivers of competition, supplier and buyer power, and barriers to entry, highlighting disruptive substitutes and emerging threats to market share.

A clear, one-sheet summary of Dishman Carbogen Amcis’ Five Forces—pinpoints competitive pressures, supplier/customer risks and regulatory threats so you can relieve strategic pain points and make faster, data-driven decisions.

Customers Bargaining Power

Big pharma concentration

Large pharma and biotech clients concentrate demand via sizable, multi-year programs, forcing Dishman Carbogen Amcis to accept tight delivery schedules and long contract cycles. Their sophisticated procurement teams extract tough commercial terms, strict quality KPIs and sustained price pressure. Inclusion on preferred supplier lists commonly gates project access, though strong technical differentiation in complex APIs and ADCs limits customer leverage.

High switching costs

Transferring processes triggers tech transfer, validation and regulatory updates that commonly cost $0.5–5 million and take 6–18 months, raising tangible switching costs. Despite this, a 2024 industry survey found about 35% of pharma customers threaten or use multi-sourcing to negotiate pricing. Lifecycle risk from clinical to commercial phases makes continuity—especially with proven performance—highly valuable. Reliable on-time delivery and quality record effectively lock in relationships.

Price transparency

Benchmarking across global CDMOs reveals price variance up to 3x for comparable services, enabling clients to shop rates and yields. Open-book models in process development often compress CDMO margins and shift risk, prompting clients to demand shared-savings arrangements on yield/process gains. Clear, quantified value articulation—cost-per-kg reductions or time-to-clinic savings—counters pure price plays and preserves Dishman Carbogen Amcis's premium.

Quality and compliance demands

Customers exert strong power through zero-defect expectations and audit rights; deviations trigger chargebacks, rework, or lost contracts, pressuring Dishman Carbogen Amcis to sustain near-perfect compliance. Robust QA and inspection readiness lower concession rates and limit price or penalty exposure. A proven inspection history strengthens negotiating leverage with large pharma buyers.

- Zero-defect audits

- Chargeback/rework risk

- QA reduces concessions

- Inspection track record = leverage

Pipeline volatility

Clinical attrition (~86% aggregate failure rate) lets customers delay or cancel orders, shifting volume risk to CDMOs; buyers increasingly demand flexible capacity and take-or-pay clauses (present in ~40% of new contracts in 2024), forcing CDMOs to absorb slot risk. Volume uncertainty compresses pricing and complicates slot allocation, often cutting realized yields by 5–12%. Portfolio diversification across 30+ clients balances exposure.

- Clinical attrition ~86%

- Take-or-pay in ~40% of 2024 contracts

- Pricing hit 5–12%

- Client base 30+ to diversify

Customers Hold Leverage: 35% Multi-sourcing, 40% Take-or-Pay, High Attrition Shifts Risk

Customers exert strong bargaining power: 35% use multi-sourcing, 40% of 2024 contracts include take-or-pay, and ~86% clinical attrition shifts volume risk to CDMOs; switching costs ($0.5–5M, 6–18 months) and technical differentiation in complex APIs/ADCs partially limit leverage.

| Metric | Value |

|---|---|

| Multi-sourcing | 35% |

| Take-or-pay (2024) | 40% |

| Clinical attrition | ~86% |

| Switching cost | $0.5–5M; 6–18m |

Preview Before You Purchase

Dishman Carbogen Amcis Porter's Five Forces Analysis

This Porter's Five Forces analysis for Dishman Carbogen Amcis is the full, professionally formatted document you see here — it examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. This preview is the exact file you'll receive immediately after purchase, with no placeholders or mockups. It's ready for download and immediate use in your strategic or investment work.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Dishman Carbogen Amcis faces moderate supplier power due to specialized raw materials, while high regulatory barriers and established client relationships limit new entrants; buyer power and substitute threats are nuanced across CDMO segments. Competitive rivalry is intense but innovation and scale offer differentiation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dishman Carbogen Amcis’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty raw materials

APIs and advanced intermediates rely on niche solvents, catalysts and high-purity reagents available from few qualified vendors, giving suppliers pricing and lead-time leverage. Qualification timelines for new suppliers typically run 6–12 months, reducing switching ease. Lead times for specialty inputs often exceed 12 weeks, so Dishman Carbogen Amcis uses dual-sourcing and multi-year contracts to mitigate risk.

Single-source equipment

Custom reactors, containment systems and HPAPI suites are often single-sourced from specialized OEMs, with HPAPI suite CAPEX commonly exceeding $10 million and custom reactor projects frequently in the multi‑million dollar range; installation, validation and maintenance dependencies therefore raise vendor leverage. Switching incurs regulatory downtime and change‑control costs that can run into hundreds of thousands per day, while multi‑year framework agreements help cap price volatility and secure spare parts.

Regulatory-grade consumables

GMP packaging, filters and chromatography media for Dishman Carbogen Amcis must meet validated standards, and any supplier change typically triggers requalification taking 2–6 months and costing tens of thousands of dollars, raising switching costs. Suppliers can dictate delivery schedules and minimum order quantities (often 1–3 months of supply), constraining flexibility. Strategic inventory buffers (1–3 months on hand) are used to manage disruptions and MOQ effects.

Energy and utilities

Continuous operations in Dishman Carbogen Amcis multipurpose plants are energy-intensive, increasing supplier leverage. Regional utility monopolies and tight grids in India raised bargaining power; industrial tariffs averaged about INR 8–10/kWh in 2024. Energy price volatility squeezed margins in 2024, while hedging and efficiency upgrades partially offset exposure.

- High consumption: continuous runs raise energy dependency

- Regional power markets: monopoly/tight grids boost supplier power

- 2024 tariffs ≈ INR 8–10/kWh; volatility hit margins

- Mitigants: hedging, efficiency upgrades

Logistics and hazardous transport

Shipping regulated chemicals and temperature-sensitive inputs narrows carrier options due to IMDG Code requirements (in force since 1965) and cold-chain mandates, raising per-shipment handling complexity and cost.

Compliance, specialized insurance and limited carriers lift logistics costs and reduce flexibility; port congestion and geopolitical chokepoints in 2024 intensified supplier leverage.

Preferred-carrier programs and long-term contracts stabilize service levels and capacity, concentrating bargaining with a handful of certified providers.

- IMDG Code compliance

- Cold-chain specialization

- Insurance & compliance premiums

- Port congestion & geopolitical risk

- Preferred-carrier stabilization

High supplier leverage: HPAPI CAPEX, long lead times and energy costs drive supply risk

Suppliers hold significant leverage due to niche reagents, long qualification (6–12 months) and lead times (>12 weeks), and high CAPEX for HPAPI suites (typically >$10m). Switching triggers 2–6 month requalification, change‑control costs often hundreds of thousands/day, and 2024 energy tariffs ≈ INR 8–10/kWh raised input costs. Long-term contracts, dual‑sourcing and inventory buffers reduce but do not eliminate supplier power.

| Item | Impact | Mitigant | Metric (2024) |

|---|---|---|---|

| HPAPI CAPEX | High vendor leverage | Multi‑year contracts | > $10m |

| Lead times | Supply risk | Dual‑sourcing, buffers | > 12 weeks |

| Energy | Cost pressure | Hedging, upgrades | INR 8–10/kWh |

What is included in the product

Tailored Porter's Five Forces analysis for Dishman Carbogen Amcis uncovers key drivers of competition, supplier and buyer power, and barriers to entry, highlighting disruptive substitutes and emerging threats to market share.

A clear, one-sheet summary of Dishman Carbogen Amcis’ Five Forces—pinpoints competitive pressures, supplier/customer risks and regulatory threats so you can relieve strategic pain points and make faster, data-driven decisions.

Customers Bargaining Power

Big pharma concentration

Large pharma and biotech clients concentrate demand via sizable, multi-year programs, forcing Dishman Carbogen Amcis to accept tight delivery schedules and long contract cycles. Their sophisticated procurement teams extract tough commercial terms, strict quality KPIs and sustained price pressure. Inclusion on preferred supplier lists commonly gates project access, though strong technical differentiation in complex APIs and ADCs limits customer leverage.

High switching costs

Transferring processes triggers tech transfer, validation and regulatory updates that commonly cost $0.5–5 million and take 6–18 months, raising tangible switching costs. Despite this, a 2024 industry survey found about 35% of pharma customers threaten or use multi-sourcing to negotiate pricing. Lifecycle risk from clinical to commercial phases makes continuity—especially with proven performance—highly valuable. Reliable on-time delivery and quality record effectively lock in relationships.

Price transparency

Benchmarking across global CDMOs reveals price variance up to 3x for comparable services, enabling clients to shop rates and yields. Open-book models in process development often compress CDMO margins and shift risk, prompting clients to demand shared-savings arrangements on yield/process gains. Clear, quantified value articulation—cost-per-kg reductions or time-to-clinic savings—counters pure price plays and preserves Dishman Carbogen Amcis's premium.

Quality and compliance demands

Customers exert strong power through zero-defect expectations and audit rights; deviations trigger chargebacks, rework, or lost contracts, pressuring Dishman Carbogen Amcis to sustain near-perfect compliance. Robust QA and inspection readiness lower concession rates and limit price or penalty exposure. A proven inspection history strengthens negotiating leverage with large pharma buyers.

- Zero-defect audits

- Chargeback/rework risk

- QA reduces concessions

- Inspection track record = leverage

Pipeline volatility

Clinical attrition (~86% aggregate failure rate) lets customers delay or cancel orders, shifting volume risk to CDMOs; buyers increasingly demand flexible capacity and take-or-pay clauses (present in ~40% of new contracts in 2024), forcing CDMOs to absorb slot risk. Volume uncertainty compresses pricing and complicates slot allocation, often cutting realized yields by 5–12%. Portfolio diversification across 30+ clients balances exposure.

- Clinical attrition ~86%

- Take-or-pay in ~40% of 2024 contracts

- Pricing hit 5–12%

- Client base 30+ to diversify

Customers Hold Leverage: 35% Multi-sourcing, 40% Take-or-Pay, High Attrition Shifts Risk

Customers exert strong bargaining power: 35% use multi-sourcing, 40% of 2024 contracts include take-or-pay, and ~86% clinical attrition shifts volume risk to CDMOs; switching costs ($0.5–5M, 6–18 months) and technical differentiation in complex APIs/ADCs partially limit leverage.

| Metric | Value |

|---|---|

| Multi-sourcing | 35% |

| Take-or-pay (2024) | 40% |

| Clinical attrition | ~86% |

| Switching cost | $0.5–5M; 6–18m |

Preview Before You Purchase

Dishman Carbogen Amcis Porter's Five Forces Analysis

This Porter's Five Forces analysis for Dishman Carbogen Amcis is the full, professionally formatted document you see here — it examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. This preview is the exact file you'll receive immediately after purchase, with no placeholders or mockups. It's ready for download and immediate use in your strategic or investment work.