DNV GL Group AS Porter's Five Forces Analysis

From Overview to Strategy Blueprint

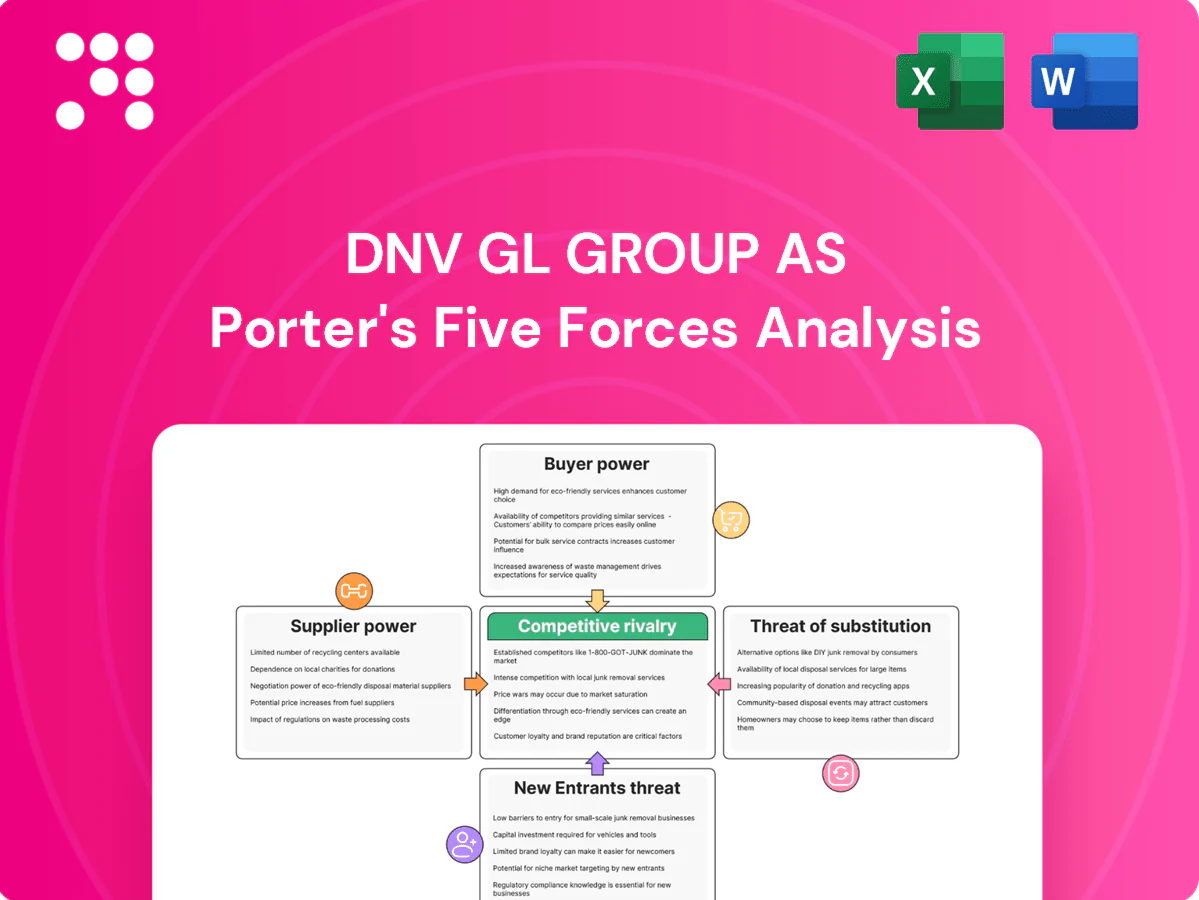

DNV GL Group AS operates in a high-stakes assurance and advisory market where strong brand reputation and scale curb buyer power, while specialized suppliers and regulatory complexity elevate switching costs; threats stem from digital disruptors and niche entrants compressing margins and increasing substitute services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore DNV GL Group AS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce domain talent

DNV depends on scarce domain talent—highly specialized engineers, auditors and experts in maritime, energy and healthcare—making supplier power high; DNV employs roughly 12,000 staff (2023–24) and faces tight markets that lift wage pressure. Certifications and specialized experience create switching frictions and increase retention costs, while reported technical role shortages in 2024 exceed 50% in some sectors, elongating delivery timelines and constraining capacity.

Proprietary data and software

Specialized modeling tools, digital twins and proprietary datasets for asset integrity and emissions are supplied by a small set of niche vendors, creating limited alternatives and raising suppliers' bargaining power. High integration costs and rigorous validation requirements for safety-critical modules increase switching costs and effectively lock in toolchains. For mission-critical functionality vendors can command premium pricing and contractual terms, pressuring DNV GL's procurement flexibility.

Accreditation and standards bodies

External accreditation and standards bodies set the mandatory assurance frameworks DNV must follow, and shifts in standards require retraining and tool updates that increase operating costs. Few substitutes exist for recognized accreditations, giving these bodies strong leverage over pricing and service scope. DNV’s participation in standard-setting and its global workforce of about 12,000 employees in 2024 partially mitigates this exposure by shaping outcomes and speeding compliance.

Specialized testing and equipment

Calibrated instruments, specialist labs and inspection technologies are supplied by a limited set of global vendors, creating supply-side concentration that lengthens lead times and enforces strict compliance, reducing DNV GLs ability to switch quickly. Long-term maintenance and calibration contracts add predictable recurring costs and vendor lock-in. DNV GLs bulk purchasing and global scale, however, strengthen its negotiating position and help moderate supplier power.

- Calibrated instruments: limited global suppliers

- Switching barriers: lead times and compliance

- Recurring costs: maintenance and calibration contracts

- Counterbalance: bulk purchasing and global scale

Cloud and cybersecurity vendors

Talent gaps and cloud concentration raise supplier power

DNV relies on scarce domain talent—about 12,000 staff (2023–24) with reported technical shortages >50% in some sectors (2024)—raising supplier power. Niche vendors for digital twins, calibrated instruments and accreditations concentrate supply; hyperscalers hold AWS 32% Azure 23% GCP 11% (Synergy Research 2024). Multi-cloud adoption 92% (Flexera 2024) and DNV scale partly mitigate pressure.

| Category | 2024 metric | Impact |

|---|---|---|

| Talent | 12,000 staff; >50% shortages | High |

| Cloud | AWS32% Azure23% GCP11% | Concentration |

| Multi-cloud | 92% enterprises | Mitigant |

| Niche vendors | Few global suppliers | High switching cost |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks tailored exclusively to DNV GL Group AS. Identifies disruptive forces, substitutes and industry dynamics that shape pricing, profitability and strategic positioning for investors and executives.

DNV GL Group AS Porter's Five Forces one-sheet highlights competitive pressures and regulatory risks, enabling rapid mitigation planning and clear, board-ready recommendations.

Customers Bargaining Power

Concentrated enterprise clients

Large maritime, energy and healthcare clients run competitive tenders and multi-year frameworks (often 3–5 years), with high deal sizes that materially increase buyer negotiation leverage. Procurement sophistication drives rigorous pricing, SLAs and performance clauses; maritime customers underpin ~90% of world trade by volume, raising stakes. DNV’s ~12,000-13,000 global workforce and strong brand partially offset but do not eliminate buyer power.

Switching costs via continuity

Continuity of classification, certification histories and audit trails at DNV—operating in 100+ countries and employing over 13,000 people as of 2024—creates high procedural switching costs that lock in clients once engagements are embedded.

Mid-project transitions risk schedule delays and regulatory rework, raising the effective cost of changing providers during delivery.

These factors temper buyer power, though customers can still re-compete at contract renewal points.

Regulatory and ESG mandates

Compliance-driven demand tied to mandates like the EU CSRD (covering ~50,000 firms from 2024) lowers price elasticity as buyers prioritize timely certification over cost; assured outcomes trump lowest bids for critical compliance work. In non-mandated advisory engagements price sensitivity rises, increasing bargaining power of cost-conscious clients. Mixed mandated and voluntary demand segments create uneven, segmented buyer power across DNVs service lines.

Service comparability and RFPs

Many assurance scopes are spec-based and easily comparable across providers; 2024 procurement trends show growing reliance on structured RFPs that enable clear price benchmarking and multi-sourcing, while outcome-based KPIs increase scrutiny of fees and contract renewals; differentiation via deep domain expertise and proprietary digital platforms remains key to defend value.

- Spec-based scopes → easier comparison

- Structured RFPs → benchmarking & multi-sourcing

- Outcome KPIs → fee pressure

- Domain depth & digital platforms → defend pricing

Cyclical budget pressures

Energy and maritime cycles drive customer spend and discounting: downturns squeeze contracts and force rate-card cuts, while 2024 upswings pushed buyers to prioritize speed and capacity over price; IMF estimated global GDP growth at about 3.0% in 2024, moderating aggregate demand and influencing procurement timing for DNV GL clients.

- Downturn: higher price sensitivity, tighter scopes

- Upswing: premium for capacity/speed vs price

- Diversification: sector spread smooths buyer power

3-5yr tenders and CSRD for 50,000 firms tighten fees amid IMF ~3.0% GDP

Large clients run competitive multi-year tenders (3–5 yrs) with high deal sizes, giving strong negotiation leverage despite DNV’s ~13,000 workforce and global reach. Compliance mandates (EU CSRD ~50,000 firms from 2024) reduce price sensitivity in certified work, while non-mandated advisory remains price-sensitive. Cyclical demand (IMF 2024 GDP ~3.0%) and structured RFPs increase benchmarking and fee pressure.

| Metric | 2024 |

|---|---|

| Employees | ~13,000 |

| World trade covered | ~90% |

| CSRD firms | ~50,000 |

| IMF GDP | ~3.0% |

Preview Before You Purchase

DNV GL Group AS Porter's Five Forces Analysis

You're looking at the actual DNV GL Group AS Porter's Five Forces Analysis. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It assesses threat of new entrants, supplier and buyer bargaining power, substitutes and competitive rivalry, and includes actionable insights. Instant access and download upon payment.

From Overview to Strategy Blueprint

DNV GL Group AS operates in a high-stakes assurance and advisory market where strong brand reputation and scale curb buyer power, while specialized suppliers and regulatory complexity elevate switching costs; threats stem from digital disruptors and niche entrants compressing margins and increasing substitute services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore DNV GL Group AS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce domain talent

DNV depends on scarce domain talent—highly specialized engineers, auditors and experts in maritime, energy and healthcare—making supplier power high; DNV employs roughly 12,000 staff (2023–24) and faces tight markets that lift wage pressure. Certifications and specialized experience create switching frictions and increase retention costs, while reported technical role shortages in 2024 exceed 50% in some sectors, elongating delivery timelines and constraining capacity.

Proprietary data and software

Specialized modeling tools, digital twins and proprietary datasets for asset integrity and emissions are supplied by a small set of niche vendors, creating limited alternatives and raising suppliers' bargaining power. High integration costs and rigorous validation requirements for safety-critical modules increase switching costs and effectively lock in toolchains. For mission-critical functionality vendors can command premium pricing and contractual terms, pressuring DNV GL's procurement flexibility.

Accreditation and standards bodies

External accreditation and standards bodies set the mandatory assurance frameworks DNV must follow, and shifts in standards require retraining and tool updates that increase operating costs. Few substitutes exist for recognized accreditations, giving these bodies strong leverage over pricing and service scope. DNV’s participation in standard-setting and its global workforce of about 12,000 employees in 2024 partially mitigates this exposure by shaping outcomes and speeding compliance.

Specialized testing and equipment

Calibrated instruments, specialist labs and inspection technologies are supplied by a limited set of global vendors, creating supply-side concentration that lengthens lead times and enforces strict compliance, reducing DNV GLs ability to switch quickly. Long-term maintenance and calibration contracts add predictable recurring costs and vendor lock-in. DNV GLs bulk purchasing and global scale, however, strengthen its negotiating position and help moderate supplier power.

- Calibrated instruments: limited global suppliers

- Switching barriers: lead times and compliance

- Recurring costs: maintenance and calibration contracts

- Counterbalance: bulk purchasing and global scale

Cloud and cybersecurity vendors

Talent gaps and cloud concentration raise supplier power

DNV relies on scarce domain talent—about 12,000 staff (2023–24) with reported technical shortages >50% in some sectors (2024)—raising supplier power. Niche vendors for digital twins, calibrated instruments and accreditations concentrate supply; hyperscalers hold AWS 32% Azure 23% GCP 11% (Synergy Research 2024). Multi-cloud adoption 92% (Flexera 2024) and DNV scale partly mitigate pressure.

| Category | 2024 metric | Impact |

|---|---|---|

| Talent | 12,000 staff; >50% shortages | High |

| Cloud | AWS32% Azure23% GCP11% | Concentration |

| Multi-cloud | 92% enterprises | Mitigant |

| Niche vendors | Few global suppliers | High switching cost |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks tailored exclusively to DNV GL Group AS. Identifies disruptive forces, substitutes and industry dynamics that shape pricing, profitability and strategic positioning for investors and executives.

DNV GL Group AS Porter's Five Forces one-sheet highlights competitive pressures and regulatory risks, enabling rapid mitigation planning and clear, board-ready recommendations.

Customers Bargaining Power

Concentrated enterprise clients

Large maritime, energy and healthcare clients run competitive tenders and multi-year frameworks (often 3–5 years), with high deal sizes that materially increase buyer negotiation leverage. Procurement sophistication drives rigorous pricing, SLAs and performance clauses; maritime customers underpin ~90% of world trade by volume, raising stakes. DNV’s ~12,000-13,000 global workforce and strong brand partially offset but do not eliminate buyer power.

Switching costs via continuity

Continuity of classification, certification histories and audit trails at DNV—operating in 100+ countries and employing over 13,000 people as of 2024—creates high procedural switching costs that lock in clients once engagements are embedded.

Mid-project transitions risk schedule delays and regulatory rework, raising the effective cost of changing providers during delivery.

These factors temper buyer power, though customers can still re-compete at contract renewal points.

Regulatory and ESG mandates

Compliance-driven demand tied to mandates like the EU CSRD (covering ~50,000 firms from 2024) lowers price elasticity as buyers prioritize timely certification over cost; assured outcomes trump lowest bids for critical compliance work. In non-mandated advisory engagements price sensitivity rises, increasing bargaining power of cost-conscious clients. Mixed mandated and voluntary demand segments create uneven, segmented buyer power across DNVs service lines.

Service comparability and RFPs

Many assurance scopes are spec-based and easily comparable across providers; 2024 procurement trends show growing reliance on structured RFPs that enable clear price benchmarking and multi-sourcing, while outcome-based KPIs increase scrutiny of fees and contract renewals; differentiation via deep domain expertise and proprietary digital platforms remains key to defend value.

- Spec-based scopes → easier comparison

- Structured RFPs → benchmarking & multi-sourcing

- Outcome KPIs → fee pressure

- Domain depth & digital platforms → defend pricing

Cyclical budget pressures

Energy and maritime cycles drive customer spend and discounting: downturns squeeze contracts and force rate-card cuts, while 2024 upswings pushed buyers to prioritize speed and capacity over price; IMF estimated global GDP growth at about 3.0% in 2024, moderating aggregate demand and influencing procurement timing for DNV GL clients.

- Downturn: higher price sensitivity, tighter scopes

- Upswing: premium for capacity/speed vs price

- Diversification: sector spread smooths buyer power

3-5yr tenders and CSRD for 50,000 firms tighten fees amid IMF ~3.0% GDP

Large clients run competitive multi-year tenders (3–5 yrs) with high deal sizes, giving strong negotiation leverage despite DNV’s ~13,000 workforce and global reach. Compliance mandates (EU CSRD ~50,000 firms from 2024) reduce price sensitivity in certified work, while non-mandated advisory remains price-sensitive. Cyclical demand (IMF 2024 GDP ~3.0%) and structured RFPs increase benchmarking and fee pressure.

| Metric | 2024 |

|---|---|

| Employees | ~13,000 |

| World trade covered | ~90% |

| CSRD firms | ~50,000 |

| IMF GDP | ~3.0% |

Preview Before You Purchase

DNV GL Group AS Porter's Five Forces Analysis

You're looking at the actual DNV GL Group AS Porter's Five Forces Analysis. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It assesses threat of new entrants, supplier and buyer bargaining power, substitutes and competitive rivalry, and includes actionable insights. Instant access and download upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

DNV GL Group AS operates in a high-stakes assurance and advisory market where strong brand reputation and scale curb buyer power, while specialized suppliers and regulatory complexity elevate switching costs; threats stem from digital disruptors and niche entrants compressing margins and increasing substitute services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore DNV GL Group AS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce domain talent

DNV depends on scarce domain talent—highly specialized engineers, auditors and experts in maritime, energy and healthcare—making supplier power high; DNV employs roughly 12,000 staff (2023–24) and faces tight markets that lift wage pressure. Certifications and specialized experience create switching frictions and increase retention costs, while reported technical role shortages in 2024 exceed 50% in some sectors, elongating delivery timelines and constraining capacity.

Proprietary data and software

Specialized modeling tools, digital twins and proprietary datasets for asset integrity and emissions are supplied by a small set of niche vendors, creating limited alternatives and raising suppliers' bargaining power. High integration costs and rigorous validation requirements for safety-critical modules increase switching costs and effectively lock in toolchains. For mission-critical functionality vendors can command premium pricing and contractual terms, pressuring DNV GL's procurement flexibility.

Accreditation and standards bodies

External accreditation and standards bodies set the mandatory assurance frameworks DNV must follow, and shifts in standards require retraining and tool updates that increase operating costs. Few substitutes exist for recognized accreditations, giving these bodies strong leverage over pricing and service scope. DNV’s participation in standard-setting and its global workforce of about 12,000 employees in 2024 partially mitigates this exposure by shaping outcomes and speeding compliance.

Specialized testing and equipment

Calibrated instruments, specialist labs and inspection technologies are supplied by a limited set of global vendors, creating supply-side concentration that lengthens lead times and enforces strict compliance, reducing DNV GLs ability to switch quickly. Long-term maintenance and calibration contracts add predictable recurring costs and vendor lock-in. DNV GLs bulk purchasing and global scale, however, strengthen its negotiating position and help moderate supplier power.

- Calibrated instruments: limited global suppliers

- Switching barriers: lead times and compliance

- Recurring costs: maintenance and calibration contracts

- Counterbalance: bulk purchasing and global scale

Cloud and cybersecurity vendors

Talent gaps and cloud concentration raise supplier power

DNV relies on scarce domain talent—about 12,000 staff (2023–24) with reported technical shortages >50% in some sectors (2024)—raising supplier power. Niche vendors for digital twins, calibrated instruments and accreditations concentrate supply; hyperscalers hold AWS 32% Azure 23% GCP 11% (Synergy Research 2024). Multi-cloud adoption 92% (Flexera 2024) and DNV scale partly mitigate pressure.

| Category | 2024 metric | Impact |

|---|---|---|

| Talent | 12,000 staff; >50% shortages | High |

| Cloud | AWS32% Azure23% GCP11% | Concentration |

| Multi-cloud | 92% enterprises | Mitigant |

| Niche vendors | Few global suppliers | High switching cost |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks tailored exclusively to DNV GL Group AS. Identifies disruptive forces, substitutes and industry dynamics that shape pricing, profitability and strategic positioning for investors and executives.

DNV GL Group AS Porter's Five Forces one-sheet highlights competitive pressures and regulatory risks, enabling rapid mitigation planning and clear, board-ready recommendations.

Customers Bargaining Power

Concentrated enterprise clients

Large maritime, energy and healthcare clients run competitive tenders and multi-year frameworks (often 3–5 years), with high deal sizes that materially increase buyer negotiation leverage. Procurement sophistication drives rigorous pricing, SLAs and performance clauses; maritime customers underpin ~90% of world trade by volume, raising stakes. DNV’s ~12,000-13,000 global workforce and strong brand partially offset but do not eliminate buyer power.

Switching costs via continuity

Continuity of classification, certification histories and audit trails at DNV—operating in 100+ countries and employing over 13,000 people as of 2024—creates high procedural switching costs that lock in clients once engagements are embedded.

Mid-project transitions risk schedule delays and regulatory rework, raising the effective cost of changing providers during delivery.

These factors temper buyer power, though customers can still re-compete at contract renewal points.

Regulatory and ESG mandates

Compliance-driven demand tied to mandates like the EU CSRD (covering ~50,000 firms from 2024) lowers price elasticity as buyers prioritize timely certification over cost; assured outcomes trump lowest bids for critical compliance work. In non-mandated advisory engagements price sensitivity rises, increasing bargaining power of cost-conscious clients. Mixed mandated and voluntary demand segments create uneven, segmented buyer power across DNVs service lines.

Service comparability and RFPs

Many assurance scopes are spec-based and easily comparable across providers; 2024 procurement trends show growing reliance on structured RFPs that enable clear price benchmarking and multi-sourcing, while outcome-based KPIs increase scrutiny of fees and contract renewals; differentiation via deep domain expertise and proprietary digital platforms remains key to defend value.

- Spec-based scopes → easier comparison

- Structured RFPs → benchmarking & multi-sourcing

- Outcome KPIs → fee pressure

- Domain depth & digital platforms → defend pricing

Cyclical budget pressures

Energy and maritime cycles drive customer spend and discounting: downturns squeeze contracts and force rate-card cuts, while 2024 upswings pushed buyers to prioritize speed and capacity over price; IMF estimated global GDP growth at about 3.0% in 2024, moderating aggregate demand and influencing procurement timing for DNV GL clients.

- Downturn: higher price sensitivity, tighter scopes

- Upswing: premium for capacity/speed vs price

- Diversification: sector spread smooths buyer power

3-5yr tenders and CSRD for 50,000 firms tighten fees amid IMF ~3.0% GDP

Large clients run competitive multi-year tenders (3–5 yrs) with high deal sizes, giving strong negotiation leverage despite DNV’s ~13,000 workforce and global reach. Compliance mandates (EU CSRD ~50,000 firms from 2024) reduce price sensitivity in certified work, while non-mandated advisory remains price-sensitive. Cyclical demand (IMF 2024 GDP ~3.0%) and structured RFPs increase benchmarking and fee pressure.

| Metric | 2024 |

|---|---|

| Employees | ~13,000 |

| World trade covered | ~90% |

| CSRD firms | ~50,000 |

| IMF GDP | ~3.0% |

Preview Before You Purchase

DNV GL Group AS Porter's Five Forces Analysis

You're looking at the actual DNV GL Group AS Porter's Five Forces Analysis. This preview shows the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It assesses threat of new entrants, supplier and buyer bargaining power, substitutes and competitive rivalry, and includes actionable insights. Instant access and download upon payment.