Dometic Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, supply-chain economics, tech adoption, social trends and regulatory pressures will shape Dometic Group’s trajectory with our concise PESTLE overview—designed for investors and strategists who need clarity fast. This snapshot points to key risks and growth levers; the full PESTLE delivers the detailed evidence and strategic recommendations you’ll rely on. Purchase the complete report for immediate, board-ready insights.

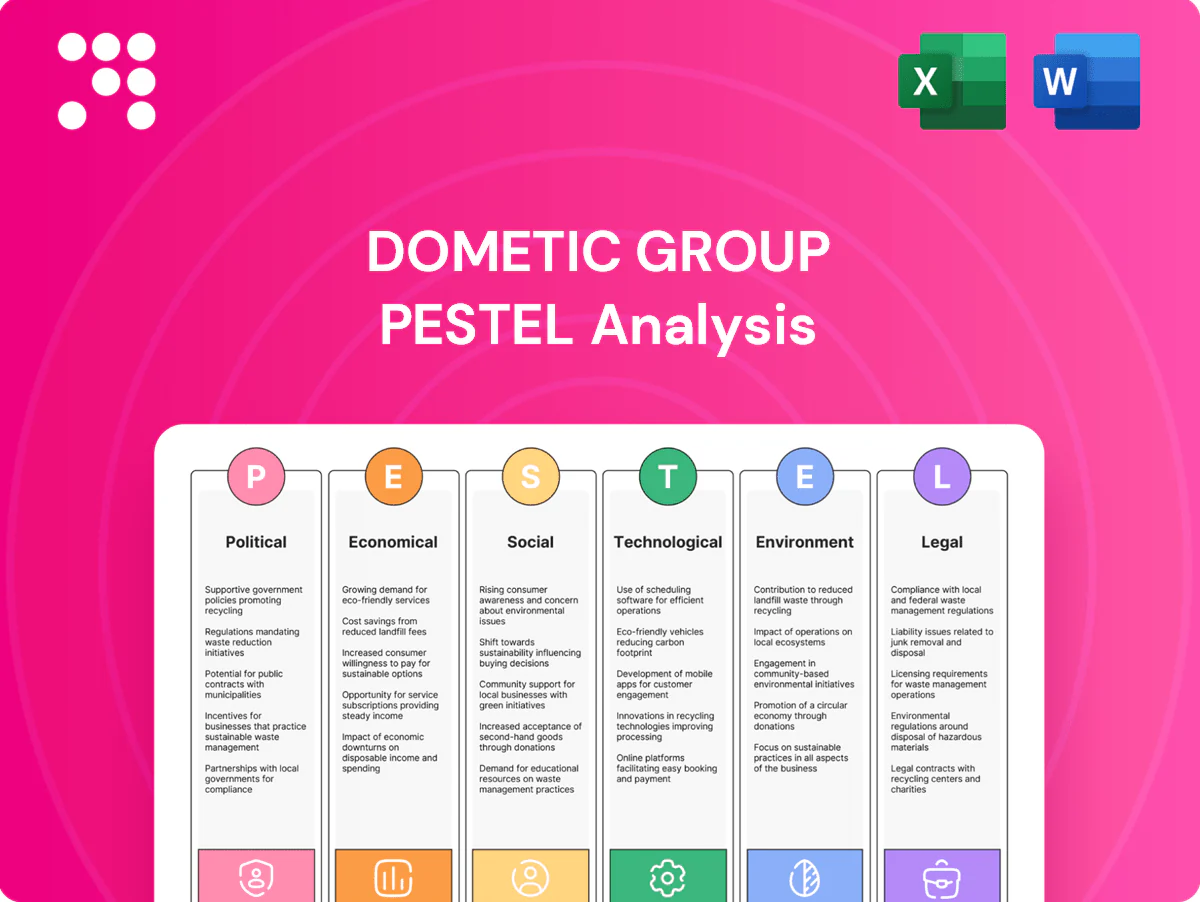

Political factors

Trade policies and tariffs

As a global manufacturer Dometic faces tariff exposure on components and finished goods across the US, EU and Asia, where duties on some traded goods can reach up to 25%. Shifts in trade relations and retaliatory measures can materially alter landed costs and pricing power for RV, marine and automotive product lines. Localizing production and supplier diversification have reduced freight and duty risk in prior cycles. Monitoring agreements such as USMCA, EU-Japan EPA and CPTPP is critical.

Government infrastructure and tourism spend

Public funding for campgrounds, marinas and roads (US IIJA $1.2 trillion; EU NextGenerationEU €806.9 billion) boosts demand for mobile-living products and infrastructure-dependent RV/marine sales. Stimulus and outdoor-tourism grants can accelerate unit sales as leisure travel rises (US National Park Service ~307 million visits in 2023). Regional spending gaps drive channel mix and inventory planning, while policy-led tourism campaigns increase brand pull-through.

Energy transition policies

Energy transition policies—notably the EU 2035 new petrol/diesel sales phase-out and the Kigali HFC phase-down—push Dometic to adopt DC-ready power, efficient HVAC and low-GWP refrigerants; global EVs reached ~16% of new car sales in 2024, boosting demand for battery and solar-integrated mobile HVAC. Subsidies and mandates (US Inflation Reduction Act ~369 billion USD in clean-energy incentives) shift procurement toward battery-powered and solar solutions. Evolving standards force agile product roadmaps; early alignment unlocks incentives and public procurement eligibility.

Geopolitical supply chain risks

Regional conflicts, sanctions and export controls continue to threaten supplies of compressors, semiconductors and specialty metals used by Dometic, with supply-chain lead times and component costs showing double-digit volatility in 2023–24.

Freight lanes and war-risk insurance have swung by double-digit percentages during 2023–24; dual sourcing, regional assembly and strategic inventory buffers for critical SKUs reduce disruption risk and preserve service levels.

- Impact: compressors, semiconductors, metals

- Freight/insurance: double-digit swings 2023–24

- Mitigation: dual sourcing, regional assembly

- Protection: inventory buffers for critical SKUs

Public health policy variability

Public health policy variability alters travel behavior and campground/marina operations, with UNWTO reporting international arrivals at about 80% of 2019 levels in 2023 and recovery continuing into 2024, so restrictions can temporarily suppress demand while reopenings spur rapid spikes in bookings and OEM accessory sales. Heightened hygiene standards favor Dometic hygiene and sanitation segments and unpredictable policy timing forces tighter production and inventory cadence.

Tariff and trade shocks up to 25% boost low-GWP, DC-ready demand

Dometic faces tariff exposure (up to 25%) and trade volatility; public funding (US IIJA $1.2T; EU NextGenerationEU €806.9B) supports RV/marine demand. Energy policies (EU 2035 phase-out; EVs ~16% of new sales in 2024) push low-GWP/DC-ready products. Conflicts/sanctions drove double-digit component and freight cost swings in 2023–24; dual sourcing and regional assembly mitigate risk.

| Factor | Metric |

|---|---|

| Tariffs | up to 25% |

| Public spend | US $1.2T / EU €806.9B |

| EV penetration | ~16% (2024) |

| Cost volatility | double-digit 2023–24 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Dometic Group, combining data-driven trends and region-specific examples to identify risks, opportunities and forward-looking insights for executives, investors and strategists.

A concise, visually segmented PESTLE summary of Dometic Group that highlights external risks and opportunities, ready to drop into presentations, share across teams, or annotate with region- and business line–specific notes to speed strategic planning and align stakeholders.

Economic factors

Consumer discretionary cycles

RV, marine and premium auto accessories are highly cyclical and track disposable income; weaker demand in downturns is consistent with IMF 2024 world GDP growth of 3.0%, which moderated consumer confidence. Recessions curb big-ticket purchases and aftermarket upgrades, forcing promotions and value-engineered SKUs to defend volumes. As confidence and savings recover, premiumization trends typically resume.

Interest rates and financing

RV and boat sales depend heavily on affordable financing; with the US federal funds rate at 5.25–5.50% in 2024–2025 higher borrowing costs have reduced affordability and slowed dealer inventory turns. Rising rates increase working capital and dealer floorplan costs, while flexible payment options and bundling can mitigate purchase friction; rate normalization typically releases pent-up demand.

Commodity and freight costs

Aluminum (LME avg ~2,300 USD/t in 2024), steel, plastics and refrigerants remain key drivers of COGS volatility for Dometic, while elevated but normalized ocean freight—down roughly 60% from 2021–22 peaks by 2024—continues to pressure margins. Surcharges and dynamic pricing allow partial pass-through of short-term spikes. Long-term supply contracts and hedging programs reduce input variability. Design-to-cost initiatives and localization further stabilize gross margin.

Exchange rate fluctuations

Dometic reports in SEK and earns multi-currency revenue, creating translation and transaction risk; a stronger USD or EUR can depress reported SEK sales while reducing imported input costs. The company uses natural hedges and derivatives to smooth earnings and enforces pricing discipline and regional sourcing to bolster resilience.

- Listed on Nasdaq Stockholm, reports in SEK

- Uses natural hedges and financial instruments to reduce volatility

- Pricing discipline and regional sourcing strengthen margins

Outdoor recreation demand trends

Secular growth in camping, boating and van conversions continues to expand Dometic’s addressable market; the U.S. outdoor economy was reported at about 862 billion USD in 2022, underpinning sustained consumer demand.

Macro slowdowns can pause unit growth but strong aftermarket replacement and fleet refresh cycles (rental/commercial) provide recurring revenue and stability; emerging markets (APAC, LATAM) are enlarging the customer base over time.

- Outdoor economy: 862B USD (2022)

- Aftermarket/replacements: recurring demand buffer

- Fleet refresh: stabilizes revenue

- Emerging markets: long-term expansion

Tariff and trade shocks up to 25% boost low-GWP, DC-ready demand

Demand for Dometic’s RV, marine and premium-auto products remains cyclical, tied to disposable income and IMF 2024 world GDP growth of 3.0%, with higher 2024–25 US rates (5.25–5.50%) weighing on affordability. Input-cost volatility (aluminum ~2,300 USD/t in 2024) and elevated freight pressure margins; hedging, regional sourcing and aftermarket stability mitigate impact.

| Metric | Value |

|---|---|

| IMF world GDP (2024) | 3.0% |

| US fed funds (2024–25) | 5.25–5.50% |

| Aluminum LME (2024 avg) | ~2,300 USD/t |

| Outdoor economy (US, 2022) | 862B USD |

What You See Is What You Get

Dometic Group PESTLE Analysis

The Dometic Group PESTLE Analysis provides a concise, actionable assessment of political, economic, sociocultural, technological, legal, and environmental factors affecting Dometic. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes data-driven insights and strategic implications ready for immediate application.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, supply-chain economics, tech adoption, social trends and regulatory pressures will shape Dometic Group’s trajectory with our concise PESTLE overview—designed for investors and strategists who need clarity fast. This snapshot points to key risks and growth levers; the full PESTLE delivers the detailed evidence and strategic recommendations you’ll rely on. Purchase the complete report for immediate, board-ready insights.

Political factors

Trade policies and tariffs

As a global manufacturer Dometic faces tariff exposure on components and finished goods across the US, EU and Asia, where duties on some traded goods can reach up to 25%. Shifts in trade relations and retaliatory measures can materially alter landed costs and pricing power for RV, marine and automotive product lines. Localizing production and supplier diversification have reduced freight and duty risk in prior cycles. Monitoring agreements such as USMCA, EU-Japan EPA and CPTPP is critical.

Government infrastructure and tourism spend

Public funding for campgrounds, marinas and roads (US IIJA $1.2 trillion; EU NextGenerationEU €806.9 billion) boosts demand for mobile-living products and infrastructure-dependent RV/marine sales. Stimulus and outdoor-tourism grants can accelerate unit sales as leisure travel rises (US National Park Service ~307 million visits in 2023). Regional spending gaps drive channel mix and inventory planning, while policy-led tourism campaigns increase brand pull-through.

Energy transition policies

Energy transition policies—notably the EU 2035 new petrol/diesel sales phase-out and the Kigali HFC phase-down—push Dometic to adopt DC-ready power, efficient HVAC and low-GWP refrigerants; global EVs reached ~16% of new car sales in 2024, boosting demand for battery and solar-integrated mobile HVAC. Subsidies and mandates (US Inflation Reduction Act ~369 billion USD in clean-energy incentives) shift procurement toward battery-powered and solar solutions. Evolving standards force agile product roadmaps; early alignment unlocks incentives and public procurement eligibility.

Geopolitical supply chain risks

Regional conflicts, sanctions and export controls continue to threaten supplies of compressors, semiconductors and specialty metals used by Dometic, with supply-chain lead times and component costs showing double-digit volatility in 2023–24.

Freight lanes and war-risk insurance have swung by double-digit percentages during 2023–24; dual sourcing, regional assembly and strategic inventory buffers for critical SKUs reduce disruption risk and preserve service levels.

- Impact: compressors, semiconductors, metals

- Freight/insurance: double-digit swings 2023–24

- Mitigation: dual sourcing, regional assembly

- Protection: inventory buffers for critical SKUs

Public health policy variability

Public health policy variability alters travel behavior and campground/marina operations, with UNWTO reporting international arrivals at about 80% of 2019 levels in 2023 and recovery continuing into 2024, so restrictions can temporarily suppress demand while reopenings spur rapid spikes in bookings and OEM accessory sales. Heightened hygiene standards favor Dometic hygiene and sanitation segments and unpredictable policy timing forces tighter production and inventory cadence.

Tariff and trade shocks up to 25% boost low-GWP, DC-ready demand

Dometic faces tariff exposure (up to 25%) and trade volatility; public funding (US IIJA $1.2T; EU NextGenerationEU €806.9B) supports RV/marine demand. Energy policies (EU 2035 phase-out; EVs ~16% of new sales in 2024) push low-GWP/DC-ready products. Conflicts/sanctions drove double-digit component and freight cost swings in 2023–24; dual sourcing and regional assembly mitigate risk.

| Factor | Metric |

|---|---|

| Tariffs | up to 25% |

| Public spend | US $1.2T / EU €806.9B |

| EV penetration | ~16% (2024) |

| Cost volatility | double-digit 2023–24 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Dometic Group, combining data-driven trends and region-specific examples to identify risks, opportunities and forward-looking insights for executives, investors and strategists.

A concise, visually segmented PESTLE summary of Dometic Group that highlights external risks and opportunities, ready to drop into presentations, share across teams, or annotate with region- and business line–specific notes to speed strategic planning and align stakeholders.

Economic factors

Consumer discretionary cycles

RV, marine and premium auto accessories are highly cyclical and track disposable income; weaker demand in downturns is consistent with IMF 2024 world GDP growth of 3.0%, which moderated consumer confidence. Recessions curb big-ticket purchases and aftermarket upgrades, forcing promotions and value-engineered SKUs to defend volumes. As confidence and savings recover, premiumization trends typically resume.

Interest rates and financing

RV and boat sales depend heavily on affordable financing; with the US federal funds rate at 5.25–5.50% in 2024–2025 higher borrowing costs have reduced affordability and slowed dealer inventory turns. Rising rates increase working capital and dealer floorplan costs, while flexible payment options and bundling can mitigate purchase friction; rate normalization typically releases pent-up demand.

Commodity and freight costs

Aluminum (LME avg ~2,300 USD/t in 2024), steel, plastics and refrigerants remain key drivers of COGS volatility for Dometic, while elevated but normalized ocean freight—down roughly 60% from 2021–22 peaks by 2024—continues to pressure margins. Surcharges and dynamic pricing allow partial pass-through of short-term spikes. Long-term supply contracts and hedging programs reduce input variability. Design-to-cost initiatives and localization further stabilize gross margin.

Exchange rate fluctuations

Dometic reports in SEK and earns multi-currency revenue, creating translation and transaction risk; a stronger USD or EUR can depress reported SEK sales while reducing imported input costs. The company uses natural hedges and derivatives to smooth earnings and enforces pricing discipline and regional sourcing to bolster resilience.

- Listed on Nasdaq Stockholm, reports in SEK

- Uses natural hedges and financial instruments to reduce volatility

- Pricing discipline and regional sourcing strengthen margins

Outdoor recreation demand trends

Secular growth in camping, boating and van conversions continues to expand Dometic’s addressable market; the U.S. outdoor economy was reported at about 862 billion USD in 2022, underpinning sustained consumer demand.

Macro slowdowns can pause unit growth but strong aftermarket replacement and fleet refresh cycles (rental/commercial) provide recurring revenue and stability; emerging markets (APAC, LATAM) are enlarging the customer base over time.

- Outdoor economy: 862B USD (2022)

- Aftermarket/replacements: recurring demand buffer

- Fleet refresh: stabilizes revenue

- Emerging markets: long-term expansion

Tariff and trade shocks up to 25% boost low-GWP, DC-ready demand

Demand for Dometic’s RV, marine and premium-auto products remains cyclical, tied to disposable income and IMF 2024 world GDP growth of 3.0%, with higher 2024–25 US rates (5.25–5.50%) weighing on affordability. Input-cost volatility (aluminum ~2,300 USD/t in 2024) and elevated freight pressure margins; hedging, regional sourcing and aftermarket stability mitigate impact.

| Metric | Value |

|---|---|

| IMF world GDP (2024) | 3.0% |

| US fed funds (2024–25) | 5.25–5.50% |

| Aluminum LME (2024 avg) | ~2,300 USD/t |

| Outdoor economy (US, 2022) | 862B USD |

What You See Is What You Get

Dometic Group PESTLE Analysis

The Dometic Group PESTLE Analysis provides a concise, actionable assessment of political, economic, sociocultural, technological, legal, and environmental factors affecting Dometic. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes data-driven insights and strategic implications ready for immediate application.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, supply-chain economics, tech adoption, social trends and regulatory pressures will shape Dometic Group’s trajectory with our concise PESTLE overview—designed for investors and strategists who need clarity fast. This snapshot points to key risks and growth levers; the full PESTLE delivers the detailed evidence and strategic recommendations you’ll rely on. Purchase the complete report for immediate, board-ready insights.

Political factors

Trade policies and tariffs

As a global manufacturer Dometic faces tariff exposure on components and finished goods across the US, EU and Asia, where duties on some traded goods can reach up to 25%. Shifts in trade relations and retaliatory measures can materially alter landed costs and pricing power for RV, marine and automotive product lines. Localizing production and supplier diversification have reduced freight and duty risk in prior cycles. Monitoring agreements such as USMCA, EU-Japan EPA and CPTPP is critical.

Government infrastructure and tourism spend

Public funding for campgrounds, marinas and roads (US IIJA $1.2 trillion; EU NextGenerationEU €806.9 billion) boosts demand for mobile-living products and infrastructure-dependent RV/marine sales. Stimulus and outdoor-tourism grants can accelerate unit sales as leisure travel rises (US National Park Service ~307 million visits in 2023). Regional spending gaps drive channel mix and inventory planning, while policy-led tourism campaigns increase brand pull-through.

Energy transition policies

Energy transition policies—notably the EU 2035 new petrol/diesel sales phase-out and the Kigali HFC phase-down—push Dometic to adopt DC-ready power, efficient HVAC and low-GWP refrigerants; global EVs reached ~16% of new car sales in 2024, boosting demand for battery and solar-integrated mobile HVAC. Subsidies and mandates (US Inflation Reduction Act ~369 billion USD in clean-energy incentives) shift procurement toward battery-powered and solar solutions. Evolving standards force agile product roadmaps; early alignment unlocks incentives and public procurement eligibility.

Geopolitical supply chain risks

Regional conflicts, sanctions and export controls continue to threaten supplies of compressors, semiconductors and specialty metals used by Dometic, with supply-chain lead times and component costs showing double-digit volatility in 2023–24.

Freight lanes and war-risk insurance have swung by double-digit percentages during 2023–24; dual sourcing, regional assembly and strategic inventory buffers for critical SKUs reduce disruption risk and preserve service levels.

- Impact: compressors, semiconductors, metals

- Freight/insurance: double-digit swings 2023–24

- Mitigation: dual sourcing, regional assembly

- Protection: inventory buffers for critical SKUs

Public health policy variability

Public health policy variability alters travel behavior and campground/marina operations, with UNWTO reporting international arrivals at about 80% of 2019 levels in 2023 and recovery continuing into 2024, so restrictions can temporarily suppress demand while reopenings spur rapid spikes in bookings and OEM accessory sales. Heightened hygiene standards favor Dometic hygiene and sanitation segments and unpredictable policy timing forces tighter production and inventory cadence.

Tariff and trade shocks up to 25% boost low-GWP, DC-ready demand

Dometic faces tariff exposure (up to 25%) and trade volatility; public funding (US IIJA $1.2T; EU NextGenerationEU €806.9B) supports RV/marine demand. Energy policies (EU 2035 phase-out; EVs ~16% of new sales in 2024) push low-GWP/DC-ready products. Conflicts/sanctions drove double-digit component and freight cost swings in 2023–24; dual sourcing and regional assembly mitigate risk.

| Factor | Metric |

|---|---|

| Tariffs | up to 25% |

| Public spend | US $1.2T / EU €806.9B |

| EV penetration | ~16% (2024) |

| Cost volatility | double-digit 2023–24 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Dometic Group, combining data-driven trends and region-specific examples to identify risks, opportunities and forward-looking insights for executives, investors and strategists.

A concise, visually segmented PESTLE summary of Dometic Group that highlights external risks and opportunities, ready to drop into presentations, share across teams, or annotate with region- and business line–specific notes to speed strategic planning and align stakeholders.

Economic factors

Consumer discretionary cycles

RV, marine and premium auto accessories are highly cyclical and track disposable income; weaker demand in downturns is consistent with IMF 2024 world GDP growth of 3.0%, which moderated consumer confidence. Recessions curb big-ticket purchases and aftermarket upgrades, forcing promotions and value-engineered SKUs to defend volumes. As confidence and savings recover, premiumization trends typically resume.

Interest rates and financing

RV and boat sales depend heavily on affordable financing; with the US federal funds rate at 5.25–5.50% in 2024–2025 higher borrowing costs have reduced affordability and slowed dealer inventory turns. Rising rates increase working capital and dealer floorplan costs, while flexible payment options and bundling can mitigate purchase friction; rate normalization typically releases pent-up demand.

Commodity and freight costs

Aluminum (LME avg ~2,300 USD/t in 2024), steel, plastics and refrigerants remain key drivers of COGS volatility for Dometic, while elevated but normalized ocean freight—down roughly 60% from 2021–22 peaks by 2024—continues to pressure margins. Surcharges and dynamic pricing allow partial pass-through of short-term spikes. Long-term supply contracts and hedging programs reduce input variability. Design-to-cost initiatives and localization further stabilize gross margin.

Exchange rate fluctuations

Dometic reports in SEK and earns multi-currency revenue, creating translation and transaction risk; a stronger USD or EUR can depress reported SEK sales while reducing imported input costs. The company uses natural hedges and derivatives to smooth earnings and enforces pricing discipline and regional sourcing to bolster resilience.

- Listed on Nasdaq Stockholm, reports in SEK

- Uses natural hedges and financial instruments to reduce volatility

- Pricing discipline and regional sourcing strengthen margins

Outdoor recreation demand trends

Secular growth in camping, boating and van conversions continues to expand Dometic’s addressable market; the U.S. outdoor economy was reported at about 862 billion USD in 2022, underpinning sustained consumer demand.

Macro slowdowns can pause unit growth but strong aftermarket replacement and fleet refresh cycles (rental/commercial) provide recurring revenue and stability; emerging markets (APAC, LATAM) are enlarging the customer base over time.

- Outdoor economy: 862B USD (2022)

- Aftermarket/replacements: recurring demand buffer

- Fleet refresh: stabilizes revenue

- Emerging markets: long-term expansion

Tariff and trade shocks up to 25% boost low-GWP, DC-ready demand

Demand for Dometic’s RV, marine and premium-auto products remains cyclical, tied to disposable income and IMF 2024 world GDP growth of 3.0%, with higher 2024–25 US rates (5.25–5.50%) weighing on affordability. Input-cost volatility (aluminum ~2,300 USD/t in 2024) and elevated freight pressure margins; hedging, regional sourcing and aftermarket stability mitigate impact.

| Metric | Value |

|---|---|

| IMF world GDP (2024) | 3.0% |

| US fed funds (2024–25) | 5.25–5.50% |

| Aluminum LME (2024 avg) | ~2,300 USD/t |

| Outdoor economy (US, 2022) | 862B USD |

What You See Is What You Get

Dometic Group PESTLE Analysis

The Dometic Group PESTLE Analysis provides a concise, actionable assessment of political, economic, sociocultural, technological, legal, and environmental factors affecting Dometic. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes data-driven insights and strategic implications ready for immediate application.