dormakaba Holding Porter's Five Forces Analysis

Don't Miss the Bigger Picture

dormakaba Holding operates in a capital‑intensive, consolidation‑prone security and access solutions market where supplier ties, buyer demands, and evolving tech shape margins. Our snapshot highlights competitive intensity, substitution risks, and entry barriers. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized electronics inputs

Access control relies on secure chips, sensors and RF modules sourced from a handful of qualified vendors, with the top 5 chip suppliers supplying roughly 60% of the market (2023–24), giving suppliers significant leverage. Certification and cybersecurity testing often require 6–12 months and strict conformity, limiting quick switching. Multi-sourcing and modular design mitigate risk, but hardware redesigns can cost millions and disrupt revenue cycles.

Metals and precision hardware

Locks, door closers and hinges rely on steel, brass and aluminum produced to tight tolerances, making metals a key input. Commodity price volatility — often showing double-digit year-on-year swings — can compress margins if not hedged. dormakaba mitigates through long-term supplier contracts and in-house machining, which meaningfully reduces but does not eliminate exposure. Procurement hedges and contractual pass-throughs remain necessary.

Software and cloud platforms

APIs, firmware, and cloud services are increasingly central to smart access, making software stacks a core supplier input; Synergy Research Group 2024 shows hyperscalers concentrate ~64% of global cloud market (AWS 32%, Microsoft 21%, Google 11%), amplifying pricing power and lock-in. Dependence on select third‑party clouds and proprietary firmware raises supplier influence and switching costs. Investing in proprietary platforms and open standards (e.g., interoperable APIs, FIDO, MQTT) reduces that leverage by diversifying dependencies and enabling competitive sourcing.

Security components and certifications

Certified cylinders, readers and biometric modules are supplied by specialized vendors, concentrating technical know-how and giving suppliers leverage; dormakaba reported CHF 2.7bn sales in FY2023, increasing reliance on certified inputs. Compliance with EN/ANSI/UL norms restricts substitutes and raises switching costs through recertification timelines and testing. Strategic partnerships and co-development reduce cost volatility and align product roadmaps, lowering procurement risk.

- Specialized suppliers: high technical concentration

- Standards: EN/ANSI/UL raise switching costs

- FY2023 sales: CHF 2.7bn (dormakaba)

- Mitigation: partnerships and co-development

Logistics and installation partners

Distribution networks, installers and integrators directly affect delivery lead times and service quality, and with dormakaba operating in over 50 countries and ~15,000 employees in 2024, partner performance materially impacts customer experience.

Scarcity of skilled technicians in 2024 shifts bargaining power toward partners, while structured training programs and captive service networks help dormakaba rebalance leverage and protect margins.

Concentrated chip and cloud suppliers boost prices and switching costs

Suppliers exert moderate-to-high power: concentrated chip, biometric and certified-component vendors (top5 chips ≈60% 2023–24) and hyperscaler cloud concentration raise prices and switching costs. Commodity metal volatility and lengthy recertification (6–12 months) amplify leverage despite long‑term contracts and in‑house machining. Training, captive service networks and partnerships partially mitigate supplier influence.

| Factor | Metric (2023–24) |

|---|---|

| Top chip suppliers | Top5 ≈60% |

| Cloud market | AWS32% / MSFT21% / GCP11% |

| dormakaba sales | CHF 2.7bn FY2023 |

What is included in the product

Tailored Porter's Five Forces analysis for dormakaba Holding that uncovers competitive drivers, supplier and buyer power, substitute threats, entry barriers, and disruptive trends to inform strategic and investment decisions.

A clear one-sheet summary of dormakaba Holding's Five Forces—perfect for quick decision-making; customize pressure levels with current market data and visualize strategic pressure instantly via an integrated spider chart for board-ready slides.

Customers Bargaining Power

Large enterprise and OEM accounts

Large enterprise and OEM accounts such as hospitality chains, healthcare networks and commercial REITs buy at scale and force volume discounts through multi-site RFPs, raising price sensitivity and driving procurement toward lowest net cost. Dormakaba reported CHF 2.9 billion in 2024 sales, so losing or winning a few large accounts materially affects revenue. Offering lifecycle services, managed SLAs and multi-year maintenance contracts helps justify premiums and materially reduces churn risk.

Channel integrators and distributors

Security integrators and distributors wield strong influence over product selection and can switch brands across projects, pressuring margins; dormakaba reported roughly CHF 2.6 billion in sales in FY2023, reflecting channel-driven revenue. Rebates and certification tiers materially shape integrator loyalty and penetration on large projects. Offering integration tools, developer APIs and predictable inventory availability strengthens dormakaba’s bargaining position and repeat business.

High switching costs for systems

High switching costs for systems create strong lock-in at dormakaba, a top-3 global access provider in 2024; deployed card formats, credentials and door hardware tie customers to installed bases. Data migration and re-certification materially discourage switching, reducing buyer power, while growing interoperability (industry market ~13.5bn USD in 2024) can weaken lock-in yet expands addressable demand.

Price transparency and TCO focus

Buyers now benchmark hardware prices and SaaS fees across vendors, squeezing margins as dormakaba reported CHF 2.6bn revenue in 2024 and faces standardized procurement. TCO, including maintenance and energy, drives negotiations with customers citing lifecycle costs as decisive. Bundled offerings and energy‑efficient devices help preserve margins by shifting focus from upfront price to value.

- Price benchmarking: cross-vendor SaaS comparisons

- TCO focus: maintenance + energy influence bids

- Defensive play: bundles and energy-efficient devices

Compliance and security outcomes

Regulated buyers in 2024 prioritize certifications, uptime and cyber-hardening over lowest price; documented incident response and multi-year firmware support lower procurement risk and shift leverage to vendors with proven security performance. The IBM 2024 Cost of a Data Breach report cites an average breach cost of $4.45M, raising stakes for buyer security demands.

Large RFPs make few account swings material; CHF 2.9bn sales amplify impact

Large enterprise RFPs force volume discounts; dormakaba’s CHF 2.9bn 2024 sales mean a few account wins/losses are material. Channels and integrators steer specification and margins; rebates/certs shape loyalty. High installed-base switching costs lock customers in, though rising interoperability (access market ~13.5bn USD 2024) weakens this over time.

| Metric | Value (2024) |

|---|---|

| dormakaba sales | CHF 2.9bn |

| Access market size | ~13.5bn USD |

| Avg breach cost (IBM) | $4.45M |

Preview the Actual Deliverable

dormakaba Holding Porter's Five Forces Analysis

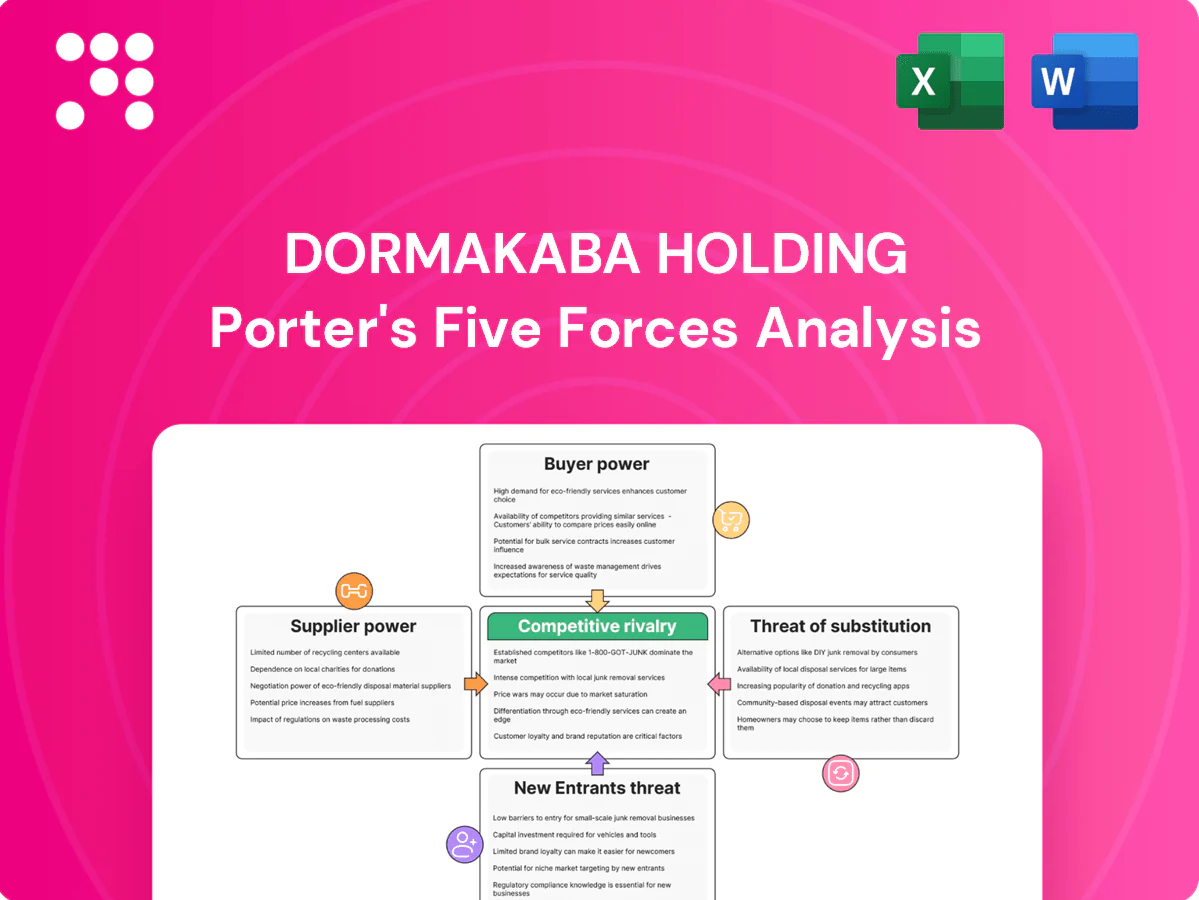

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The dormakaba Holding Porter's Five Forces Analysis provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products specific to the security and access solutions industry. It's fully formatted, actionable, and ready for immediate download and use.

Don't Miss the Bigger Picture

dormakaba Holding operates in a capital‑intensive, consolidation‑prone security and access solutions market where supplier ties, buyer demands, and evolving tech shape margins. Our snapshot highlights competitive intensity, substitution risks, and entry barriers. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized electronics inputs

Access control relies on secure chips, sensors and RF modules sourced from a handful of qualified vendors, with the top 5 chip suppliers supplying roughly 60% of the market (2023–24), giving suppliers significant leverage. Certification and cybersecurity testing often require 6–12 months and strict conformity, limiting quick switching. Multi-sourcing and modular design mitigate risk, but hardware redesigns can cost millions and disrupt revenue cycles.

Metals and precision hardware

Locks, door closers and hinges rely on steel, brass and aluminum produced to tight tolerances, making metals a key input. Commodity price volatility — often showing double-digit year-on-year swings — can compress margins if not hedged. dormakaba mitigates through long-term supplier contracts and in-house machining, which meaningfully reduces but does not eliminate exposure. Procurement hedges and contractual pass-throughs remain necessary.

Software and cloud platforms

APIs, firmware, and cloud services are increasingly central to smart access, making software stacks a core supplier input; Synergy Research Group 2024 shows hyperscalers concentrate ~64% of global cloud market (AWS 32%, Microsoft 21%, Google 11%), amplifying pricing power and lock-in. Dependence on select third‑party clouds and proprietary firmware raises supplier influence and switching costs. Investing in proprietary platforms and open standards (e.g., interoperable APIs, FIDO, MQTT) reduces that leverage by diversifying dependencies and enabling competitive sourcing.

Security components and certifications

Certified cylinders, readers and biometric modules are supplied by specialized vendors, concentrating technical know-how and giving suppliers leverage; dormakaba reported CHF 2.7bn sales in FY2023, increasing reliance on certified inputs. Compliance with EN/ANSI/UL norms restricts substitutes and raises switching costs through recertification timelines and testing. Strategic partnerships and co-development reduce cost volatility and align product roadmaps, lowering procurement risk.

- Specialized suppliers: high technical concentration

- Standards: EN/ANSI/UL raise switching costs

- FY2023 sales: CHF 2.7bn (dormakaba)

- Mitigation: partnerships and co-development

Logistics and installation partners

Distribution networks, installers and integrators directly affect delivery lead times and service quality, and with dormakaba operating in over 50 countries and ~15,000 employees in 2024, partner performance materially impacts customer experience.

Scarcity of skilled technicians in 2024 shifts bargaining power toward partners, while structured training programs and captive service networks help dormakaba rebalance leverage and protect margins.

Concentrated chip and cloud suppliers boost prices and switching costs

Suppliers exert moderate-to-high power: concentrated chip, biometric and certified-component vendors (top5 chips ≈60% 2023–24) and hyperscaler cloud concentration raise prices and switching costs. Commodity metal volatility and lengthy recertification (6–12 months) amplify leverage despite long‑term contracts and in‑house machining. Training, captive service networks and partnerships partially mitigate supplier influence.

| Factor | Metric (2023–24) |

|---|---|

| Top chip suppliers | Top5 ≈60% |

| Cloud market | AWS32% / MSFT21% / GCP11% |

| dormakaba sales | CHF 2.7bn FY2023 |

What is included in the product

Tailored Porter's Five Forces analysis for dormakaba Holding that uncovers competitive drivers, supplier and buyer power, substitute threats, entry barriers, and disruptive trends to inform strategic and investment decisions.

A clear one-sheet summary of dormakaba Holding's Five Forces—perfect for quick decision-making; customize pressure levels with current market data and visualize strategic pressure instantly via an integrated spider chart for board-ready slides.

Customers Bargaining Power

Large enterprise and OEM accounts

Large enterprise and OEM accounts such as hospitality chains, healthcare networks and commercial REITs buy at scale and force volume discounts through multi-site RFPs, raising price sensitivity and driving procurement toward lowest net cost. Dormakaba reported CHF 2.9 billion in 2024 sales, so losing or winning a few large accounts materially affects revenue. Offering lifecycle services, managed SLAs and multi-year maintenance contracts helps justify premiums and materially reduces churn risk.

Channel integrators and distributors

Security integrators and distributors wield strong influence over product selection and can switch brands across projects, pressuring margins; dormakaba reported roughly CHF 2.6 billion in sales in FY2023, reflecting channel-driven revenue. Rebates and certification tiers materially shape integrator loyalty and penetration on large projects. Offering integration tools, developer APIs and predictable inventory availability strengthens dormakaba’s bargaining position and repeat business.

High switching costs for systems

High switching costs for systems create strong lock-in at dormakaba, a top-3 global access provider in 2024; deployed card formats, credentials and door hardware tie customers to installed bases. Data migration and re-certification materially discourage switching, reducing buyer power, while growing interoperability (industry market ~13.5bn USD in 2024) can weaken lock-in yet expands addressable demand.

Price transparency and TCO focus

Buyers now benchmark hardware prices and SaaS fees across vendors, squeezing margins as dormakaba reported CHF 2.6bn revenue in 2024 and faces standardized procurement. TCO, including maintenance and energy, drives negotiations with customers citing lifecycle costs as decisive. Bundled offerings and energy‑efficient devices help preserve margins by shifting focus from upfront price to value.

- Price benchmarking: cross-vendor SaaS comparisons

- TCO focus: maintenance + energy influence bids

- Defensive play: bundles and energy-efficient devices

Compliance and security outcomes

Regulated buyers in 2024 prioritize certifications, uptime and cyber-hardening over lowest price; documented incident response and multi-year firmware support lower procurement risk and shift leverage to vendors with proven security performance. The IBM 2024 Cost of a Data Breach report cites an average breach cost of $4.45M, raising stakes for buyer security demands.

Large RFPs make few account swings material; CHF 2.9bn sales amplify impact

Large enterprise RFPs force volume discounts; dormakaba’s CHF 2.9bn 2024 sales mean a few account wins/losses are material. Channels and integrators steer specification and margins; rebates/certs shape loyalty. High installed-base switching costs lock customers in, though rising interoperability (access market ~13.5bn USD 2024) weakens this over time.

| Metric | Value (2024) |

|---|---|

| dormakaba sales | CHF 2.9bn |

| Access market size | ~13.5bn USD |

| Avg breach cost (IBM) | $4.45M |

Preview the Actual Deliverable

dormakaba Holding Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The dormakaba Holding Porter's Five Forces Analysis provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products specific to the security and access solutions industry. It's fully formatted, actionable, and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

dormakaba Holding operates in a capital‑intensive, consolidation‑prone security and access solutions market where supplier ties, buyer demands, and evolving tech shape margins. Our snapshot highlights competitive intensity, substitution risks, and entry barriers. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized electronics inputs

Access control relies on secure chips, sensors and RF modules sourced from a handful of qualified vendors, with the top 5 chip suppliers supplying roughly 60% of the market (2023–24), giving suppliers significant leverage. Certification and cybersecurity testing often require 6–12 months and strict conformity, limiting quick switching. Multi-sourcing and modular design mitigate risk, but hardware redesigns can cost millions and disrupt revenue cycles.

Metals and precision hardware

Locks, door closers and hinges rely on steel, brass and aluminum produced to tight tolerances, making metals a key input. Commodity price volatility — often showing double-digit year-on-year swings — can compress margins if not hedged. dormakaba mitigates through long-term supplier contracts and in-house machining, which meaningfully reduces but does not eliminate exposure. Procurement hedges and contractual pass-throughs remain necessary.

Software and cloud platforms

APIs, firmware, and cloud services are increasingly central to smart access, making software stacks a core supplier input; Synergy Research Group 2024 shows hyperscalers concentrate ~64% of global cloud market (AWS 32%, Microsoft 21%, Google 11%), amplifying pricing power and lock-in. Dependence on select third‑party clouds and proprietary firmware raises supplier influence and switching costs. Investing in proprietary platforms and open standards (e.g., interoperable APIs, FIDO, MQTT) reduces that leverage by diversifying dependencies and enabling competitive sourcing.

Security components and certifications

Certified cylinders, readers and biometric modules are supplied by specialized vendors, concentrating technical know-how and giving suppliers leverage; dormakaba reported CHF 2.7bn sales in FY2023, increasing reliance on certified inputs. Compliance with EN/ANSI/UL norms restricts substitutes and raises switching costs through recertification timelines and testing. Strategic partnerships and co-development reduce cost volatility and align product roadmaps, lowering procurement risk.

- Specialized suppliers: high technical concentration

- Standards: EN/ANSI/UL raise switching costs

- FY2023 sales: CHF 2.7bn (dormakaba)

- Mitigation: partnerships and co-development

Logistics and installation partners

Distribution networks, installers and integrators directly affect delivery lead times and service quality, and with dormakaba operating in over 50 countries and ~15,000 employees in 2024, partner performance materially impacts customer experience.

Scarcity of skilled technicians in 2024 shifts bargaining power toward partners, while structured training programs and captive service networks help dormakaba rebalance leverage and protect margins.

Concentrated chip and cloud suppliers boost prices and switching costs

Suppliers exert moderate-to-high power: concentrated chip, biometric and certified-component vendors (top5 chips ≈60% 2023–24) and hyperscaler cloud concentration raise prices and switching costs. Commodity metal volatility and lengthy recertification (6–12 months) amplify leverage despite long‑term contracts and in‑house machining. Training, captive service networks and partnerships partially mitigate supplier influence.

| Factor | Metric (2023–24) |

|---|---|

| Top chip suppliers | Top5 ≈60% |

| Cloud market | AWS32% / MSFT21% / GCP11% |

| dormakaba sales | CHF 2.7bn FY2023 |

What is included in the product

Tailored Porter's Five Forces analysis for dormakaba Holding that uncovers competitive drivers, supplier and buyer power, substitute threats, entry barriers, and disruptive trends to inform strategic and investment decisions.

A clear one-sheet summary of dormakaba Holding's Five Forces—perfect for quick decision-making; customize pressure levels with current market data and visualize strategic pressure instantly via an integrated spider chart for board-ready slides.

Customers Bargaining Power

Large enterprise and OEM accounts

Large enterprise and OEM accounts such as hospitality chains, healthcare networks and commercial REITs buy at scale and force volume discounts through multi-site RFPs, raising price sensitivity and driving procurement toward lowest net cost. Dormakaba reported CHF 2.9 billion in 2024 sales, so losing or winning a few large accounts materially affects revenue. Offering lifecycle services, managed SLAs and multi-year maintenance contracts helps justify premiums and materially reduces churn risk.

Channel integrators and distributors

Security integrators and distributors wield strong influence over product selection and can switch brands across projects, pressuring margins; dormakaba reported roughly CHF 2.6 billion in sales in FY2023, reflecting channel-driven revenue. Rebates and certification tiers materially shape integrator loyalty and penetration on large projects. Offering integration tools, developer APIs and predictable inventory availability strengthens dormakaba’s bargaining position and repeat business.

High switching costs for systems

High switching costs for systems create strong lock-in at dormakaba, a top-3 global access provider in 2024; deployed card formats, credentials and door hardware tie customers to installed bases. Data migration and re-certification materially discourage switching, reducing buyer power, while growing interoperability (industry market ~13.5bn USD in 2024) can weaken lock-in yet expands addressable demand.

Price transparency and TCO focus

Buyers now benchmark hardware prices and SaaS fees across vendors, squeezing margins as dormakaba reported CHF 2.6bn revenue in 2024 and faces standardized procurement. TCO, including maintenance and energy, drives negotiations with customers citing lifecycle costs as decisive. Bundled offerings and energy‑efficient devices help preserve margins by shifting focus from upfront price to value.

- Price benchmarking: cross-vendor SaaS comparisons

- TCO focus: maintenance + energy influence bids

- Defensive play: bundles and energy-efficient devices

Compliance and security outcomes

Regulated buyers in 2024 prioritize certifications, uptime and cyber-hardening over lowest price; documented incident response and multi-year firmware support lower procurement risk and shift leverage to vendors with proven security performance. The IBM 2024 Cost of a Data Breach report cites an average breach cost of $4.45M, raising stakes for buyer security demands.

Large RFPs make few account swings material; CHF 2.9bn sales amplify impact

Large enterprise RFPs force volume discounts; dormakaba’s CHF 2.9bn 2024 sales mean a few account wins/losses are material. Channels and integrators steer specification and margins; rebates/certs shape loyalty. High installed-base switching costs lock customers in, though rising interoperability (access market ~13.5bn USD 2024) weakens this over time.

| Metric | Value (2024) |

|---|---|

| dormakaba sales | CHF 2.9bn |

| Access market size | ~13.5bn USD |

| Avg breach cost (IBM) | $4.45M |

Preview the Actual Deliverable

dormakaba Holding Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The dormakaba Holding Porter's Five Forces Analysis provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products specific to the security and access solutions industry. It's fully formatted, actionable, and ready for immediate download and use.