Dow Porter's Five Forces Analysis

Don't Miss the Bigger Picture

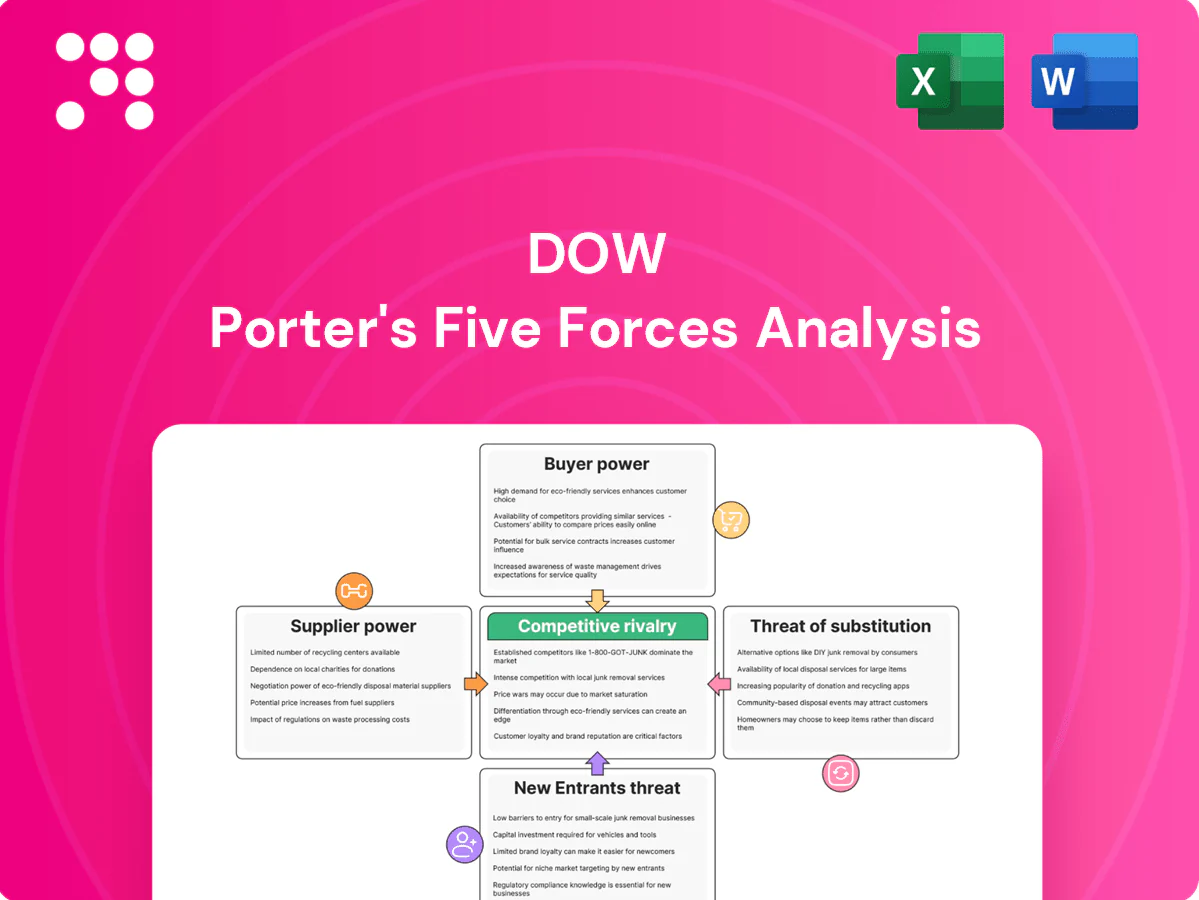

This brief snapshot highlights key competitive dynamics driving Dow—from supplier and buyer power to substitute threats and rivalry intensity. Understand how regulatory shifts and scale advantages shape Dow’s positioning and margins. Unlock the full Porter's Five Forces Analysis to explore Dow’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse feedstock sources

Dow sources hydrocarbons, chlor-alkali, siloxanes and specialty additives from a broad global base, reducing reliance on any single supplier and lowering supplier bargaining power. Regional diversification limits disruption risk from logistics and geopolitics, while long-term contracts and integrated procurement smooth price swings. Tight market episodes, however, can still drive sharp feedstock cost spikes that elevate input inflation risk.

Energy and naphtha sensitivity

Crude oil (Brent averaged about $86/bbl in 2024), natural gas (Henry Hub ~ $3.70/MMBtu in 2024) and NGL swings strongly drive resin and intermediates cost, increasing supplier leverage during price spikes via pass-throughs. Dow’s hedging programs and integrated steam cracker operations reduce but cannot fully eliminate exposure to feedstock volatility. Contract pricing formulas and indexation partially offset timing gaps, but short-term spikes still pressure margins.

Specialty inputs scarcity

Certain catalysts, high-purity monomers and silicone precursors have few qualified vendors, raising supplier bargaining power due to costly qualification and regulatory hurdles. Dow notes in its 2024 Form 10-K that switching suppliers for critical feedstocks incurs high technical and approval costs, empowering niche suppliers. Dow mitigates risk via dual-sourcing strategies and in-house technical standards to preserve production continuity.

Logistics and infrastructure constraints

Pipeline, port, and rail capacity can bottleneck inbound materials, and when logistics tighten carriers and terminal operators capture leverage via higher rates and allocation; industry spikes in transport surcharges have exceeded 30% during tight periods. Dow’s global footprint and private terminals mitigate but do not eliminate exposure, and weather events or strikes can sharply amplify delays and costs.

- Pipeline/port/rail bottlenecks

- Carriers gain rate/allocation leverage (~30% surcharge spikes)

- Dow private assets lower but not remove risk

- Weather/strikes amplify disruptions

Backward integration options

Dow’s partial upstream integration in crackers and chlor-alkali reduces supplier leverage for key feedstocks, with internal technology and scale strengthening procurement negotiating positions while lowering exposure to spot-market volatility. Full self-sufficiency across all inputs remains uneconomic, prompting selective strategic joint ventures to secure supply and share capital intensity. These JVs target feedstock gaps and specialty intermediates rather than complete verticalization.

Input swings, niche catalysts and 30% logistics amplify vendor leverage

Dow’s broad global sourcing, partial upstream integration and long-term contracts lower supplier bargaining power, but 2024 feedstock volatility (Brent ~$86/bbl; Henry Hub ~$3.70/MMBtu) and NGL swings still create episodic supplier leverage. Niche catalysts and silicone precursors remain high-power suppliers due to few qualified vendors and costly requalification. Logistics surcharges have spiked ~30% in tight periods, elevating short-term input risk.

| Metric | 2024 Value | Implication |

|---|---|---|

| Brent | $86/bbl | drives resin costs |

| Henry Hub | $3.70/MMBtu | impacts crackers |

| Logistics surcharge | ~30% | short-term margin pressure |

| Supplier concentration | High for catalysts | switching costs |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored for Dow, uncovering competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and emerging disruptors that affect pricing, margins, and market share.

A concise Five Forces dashboard that highlights competitive pressures and actionable levers—ideal for rapid strategy pivots and boardroom decisions.

Customers Bargaining Power

Large OEMs and converters

Packaging majors, auto OEMs, and building-product converters buy at scale and negotiate aggressively; the global packaging market was valued at about 1.05 trillion USD in 2024, concentrating buying power. Their volume concentration yields price concessions and favorable service terms, with multi-year supply agreements (typically 3–5 years) standardizing formulas but squeezing margins. Dow in 2024 traded price for share and customer stickiness as a strategic response.

Product differentiation via performance

Engineered grades, application know-how and technical services make direct comparability difficult; in 2024 specialty/high-spec materials represented over 50% of industry value, reducing pure price-based competition. When performance is mission-critical, switching risk and qualification cycles deter buyers and sustain supplier leverage. Commodity grades face far greater price pressure and lower margins.

Switching costs and qualification

End-users face tooling, certification and regulatory requalification—FDA 510(k) and similar pathways in 2024 typically add ~4–6 months and validation programs (automotive, medical) can extend 12–36 months and cost $100k–$1M+, which slows churn and supports pricing discipline. Healthcare and mobility face the longest cycles; packaging switches in weeks–a few months, raising buyer leverage.

Access to alternatives and tenders

Buyers run competitive tenders across global resin producers, leveraging daily spot-price benchmarks from ICIS, Platts and other indices to strengthen negotiation leverage. Visibility to these benchmarks and digital procurement tools increases price transparency and shortens sourcing cycles. Dow responds by emphasizing solution selling and value-in-use claims to shift focus from spot price to lifecycle value.

- Benchmark sources: ICIS, Platts, IHS

- Buyer tools: digital procurement, e-tenders

- Dow strategy: solution selling, value-in-use

Sustainability and EPR demands

Customers increasingly require recyclability, bio-based content and lower carbon footprints, and 2024 procurement trends show recycled-content and EPR compliance clauses becoming standard in EU and North American tenders.

These regulations create quasi-spec lock-ins that let buyers demand upgrades without price uplift, while Dow’s decarbonization and circular-product portfolio can reclaim margin through value-added offerings tied to certifications.

Certifications and verified life-cycle data now influence award decisions and supplier selection in 2024 procurement rounds.

- 2024 trend: recycled-content and EPR clauses common in major tenders

- Dow: leverages circular products to recapture value

- Certifications: decisive in contract awards

Buyer scale, 3–5yr contracts and specialty materials raise switching costs, compress margins

Buyers (packaging majors, auto OEMs, converters) concentrate volume—global packaging market ≈ 1.05 trillion USD in 2024—securing multi-year (3–5 yr) contracts that compress supplier margins. Specialty/high-spec materials >50% of industry value in 2024, raising switching costs and protecting supplier pricing. Procurement uses ICIS/Platts benchmarks and EPR/recycled-content clauses (standard in EU/NA), while qualification adds 4–36 months and $100k–$1M+.

| Metric | 2024 | Impact |

|---|---|---|

| Packaging market | ≈1.05T USD | Buyer scale → price leverage |

| Specialty share | >50% value | Reduces pure price competition |

| Contract length | 3–5 yrs | Sustains volume commitments |

| Qualification cost/time | $100k–$1M+, 4–36 months | Slows churn, protects margins |

| Procurement clauses | EPR/recycled standard (EU/NA) | Spec-driven demands |

Same Document Delivered

Dow Porter's Five Forces Analysis

This preview is the exact Dow Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is professionally written and fully formatted for immediate download and use. What you see here is the final deliverable, ready for your analysis and decision-making.

Don't Miss the Bigger Picture

This brief snapshot highlights key competitive dynamics driving Dow—from supplier and buyer power to substitute threats and rivalry intensity. Understand how regulatory shifts and scale advantages shape Dow’s positioning and margins. Unlock the full Porter's Five Forces Analysis to explore Dow’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse feedstock sources

Dow sources hydrocarbons, chlor-alkali, siloxanes and specialty additives from a broad global base, reducing reliance on any single supplier and lowering supplier bargaining power. Regional diversification limits disruption risk from logistics and geopolitics, while long-term contracts and integrated procurement smooth price swings. Tight market episodes, however, can still drive sharp feedstock cost spikes that elevate input inflation risk.

Energy and naphtha sensitivity

Crude oil (Brent averaged about $86/bbl in 2024), natural gas (Henry Hub ~ $3.70/MMBtu in 2024) and NGL swings strongly drive resin and intermediates cost, increasing supplier leverage during price spikes via pass-throughs. Dow’s hedging programs and integrated steam cracker operations reduce but cannot fully eliminate exposure to feedstock volatility. Contract pricing formulas and indexation partially offset timing gaps, but short-term spikes still pressure margins.

Specialty inputs scarcity

Certain catalysts, high-purity monomers and silicone precursors have few qualified vendors, raising supplier bargaining power due to costly qualification and regulatory hurdles. Dow notes in its 2024 Form 10-K that switching suppliers for critical feedstocks incurs high technical and approval costs, empowering niche suppliers. Dow mitigates risk via dual-sourcing strategies and in-house technical standards to preserve production continuity.

Logistics and infrastructure constraints

Pipeline, port, and rail capacity can bottleneck inbound materials, and when logistics tighten carriers and terminal operators capture leverage via higher rates and allocation; industry spikes in transport surcharges have exceeded 30% during tight periods. Dow’s global footprint and private terminals mitigate but do not eliminate exposure, and weather events or strikes can sharply amplify delays and costs.

- Pipeline/port/rail bottlenecks

- Carriers gain rate/allocation leverage (~30% surcharge spikes)

- Dow private assets lower but not remove risk

- Weather/strikes amplify disruptions

Backward integration options

Dow’s partial upstream integration in crackers and chlor-alkali reduces supplier leverage for key feedstocks, with internal technology and scale strengthening procurement negotiating positions while lowering exposure to spot-market volatility. Full self-sufficiency across all inputs remains uneconomic, prompting selective strategic joint ventures to secure supply and share capital intensity. These JVs target feedstock gaps and specialty intermediates rather than complete verticalization.

Input swings, niche catalysts and 30% logistics amplify vendor leverage

Dow’s broad global sourcing, partial upstream integration and long-term contracts lower supplier bargaining power, but 2024 feedstock volatility (Brent ~$86/bbl; Henry Hub ~$3.70/MMBtu) and NGL swings still create episodic supplier leverage. Niche catalysts and silicone precursors remain high-power suppliers due to few qualified vendors and costly requalification. Logistics surcharges have spiked ~30% in tight periods, elevating short-term input risk.

| Metric | 2024 Value | Implication |

|---|---|---|

| Brent | $86/bbl | drives resin costs |

| Henry Hub | $3.70/MMBtu | impacts crackers |

| Logistics surcharge | ~30% | short-term margin pressure |

| Supplier concentration | High for catalysts | switching costs |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored for Dow, uncovering competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and emerging disruptors that affect pricing, margins, and market share.

A concise Five Forces dashboard that highlights competitive pressures and actionable levers—ideal for rapid strategy pivots and boardroom decisions.

Customers Bargaining Power

Large OEMs and converters

Packaging majors, auto OEMs, and building-product converters buy at scale and negotiate aggressively; the global packaging market was valued at about 1.05 trillion USD in 2024, concentrating buying power. Their volume concentration yields price concessions and favorable service terms, with multi-year supply agreements (typically 3–5 years) standardizing formulas but squeezing margins. Dow in 2024 traded price for share and customer stickiness as a strategic response.

Product differentiation via performance

Engineered grades, application know-how and technical services make direct comparability difficult; in 2024 specialty/high-spec materials represented over 50% of industry value, reducing pure price-based competition. When performance is mission-critical, switching risk and qualification cycles deter buyers and sustain supplier leverage. Commodity grades face far greater price pressure and lower margins.

Switching costs and qualification

End-users face tooling, certification and regulatory requalification—FDA 510(k) and similar pathways in 2024 typically add ~4–6 months and validation programs (automotive, medical) can extend 12–36 months and cost $100k–$1M+, which slows churn and supports pricing discipline. Healthcare and mobility face the longest cycles; packaging switches in weeks–a few months, raising buyer leverage.

Access to alternatives and tenders

Buyers run competitive tenders across global resin producers, leveraging daily spot-price benchmarks from ICIS, Platts and other indices to strengthen negotiation leverage. Visibility to these benchmarks and digital procurement tools increases price transparency and shortens sourcing cycles. Dow responds by emphasizing solution selling and value-in-use claims to shift focus from spot price to lifecycle value.

- Benchmark sources: ICIS, Platts, IHS

- Buyer tools: digital procurement, e-tenders

- Dow strategy: solution selling, value-in-use

Sustainability and EPR demands

Customers increasingly require recyclability, bio-based content and lower carbon footprints, and 2024 procurement trends show recycled-content and EPR compliance clauses becoming standard in EU and North American tenders.

These regulations create quasi-spec lock-ins that let buyers demand upgrades without price uplift, while Dow’s decarbonization and circular-product portfolio can reclaim margin through value-added offerings tied to certifications.

Certifications and verified life-cycle data now influence award decisions and supplier selection in 2024 procurement rounds.

- 2024 trend: recycled-content and EPR clauses common in major tenders

- Dow: leverages circular products to recapture value

- Certifications: decisive in contract awards

Buyer scale, 3–5yr contracts and specialty materials raise switching costs, compress margins

Buyers (packaging majors, auto OEMs, converters) concentrate volume—global packaging market ≈ 1.05 trillion USD in 2024—securing multi-year (3–5 yr) contracts that compress supplier margins. Specialty/high-spec materials >50% of industry value in 2024, raising switching costs and protecting supplier pricing. Procurement uses ICIS/Platts benchmarks and EPR/recycled-content clauses (standard in EU/NA), while qualification adds 4–36 months and $100k–$1M+.

| Metric | 2024 | Impact |

|---|---|---|

| Packaging market | ≈1.05T USD | Buyer scale → price leverage |

| Specialty share | >50% value | Reduces pure price competition |

| Contract length | 3–5 yrs | Sustains volume commitments |

| Qualification cost/time | $100k–$1M+, 4–36 months | Slows churn, protects margins |

| Procurement clauses | EPR/recycled standard (EU/NA) | Spec-driven demands |

Same Document Delivered

Dow Porter's Five Forces Analysis

This preview is the exact Dow Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is professionally written and fully formatted for immediate download and use. What you see here is the final deliverable, ready for your analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

This brief snapshot highlights key competitive dynamics driving Dow—from supplier and buyer power to substitute threats and rivalry intensity. Understand how regulatory shifts and scale advantages shape Dow’s positioning and margins. Unlock the full Porter's Five Forces Analysis to explore Dow’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse feedstock sources

Dow sources hydrocarbons, chlor-alkali, siloxanes and specialty additives from a broad global base, reducing reliance on any single supplier and lowering supplier bargaining power. Regional diversification limits disruption risk from logistics and geopolitics, while long-term contracts and integrated procurement smooth price swings. Tight market episodes, however, can still drive sharp feedstock cost spikes that elevate input inflation risk.

Energy and naphtha sensitivity

Crude oil (Brent averaged about $86/bbl in 2024), natural gas (Henry Hub ~ $3.70/MMBtu in 2024) and NGL swings strongly drive resin and intermediates cost, increasing supplier leverage during price spikes via pass-throughs. Dow’s hedging programs and integrated steam cracker operations reduce but cannot fully eliminate exposure to feedstock volatility. Contract pricing formulas and indexation partially offset timing gaps, but short-term spikes still pressure margins.

Specialty inputs scarcity

Certain catalysts, high-purity monomers and silicone precursors have few qualified vendors, raising supplier bargaining power due to costly qualification and regulatory hurdles. Dow notes in its 2024 Form 10-K that switching suppliers for critical feedstocks incurs high technical and approval costs, empowering niche suppliers. Dow mitigates risk via dual-sourcing strategies and in-house technical standards to preserve production continuity.

Logistics and infrastructure constraints

Pipeline, port, and rail capacity can bottleneck inbound materials, and when logistics tighten carriers and terminal operators capture leverage via higher rates and allocation; industry spikes in transport surcharges have exceeded 30% during tight periods. Dow’s global footprint and private terminals mitigate but do not eliminate exposure, and weather events or strikes can sharply amplify delays and costs.

- Pipeline/port/rail bottlenecks

- Carriers gain rate/allocation leverage (~30% surcharge spikes)

- Dow private assets lower but not remove risk

- Weather/strikes amplify disruptions

Backward integration options

Dow’s partial upstream integration in crackers and chlor-alkali reduces supplier leverage for key feedstocks, with internal technology and scale strengthening procurement negotiating positions while lowering exposure to spot-market volatility. Full self-sufficiency across all inputs remains uneconomic, prompting selective strategic joint ventures to secure supply and share capital intensity. These JVs target feedstock gaps and specialty intermediates rather than complete verticalization.

Input swings, niche catalysts and 30% logistics amplify vendor leverage

Dow’s broad global sourcing, partial upstream integration and long-term contracts lower supplier bargaining power, but 2024 feedstock volatility (Brent ~$86/bbl; Henry Hub ~$3.70/MMBtu) and NGL swings still create episodic supplier leverage. Niche catalysts and silicone precursors remain high-power suppliers due to few qualified vendors and costly requalification. Logistics surcharges have spiked ~30% in tight periods, elevating short-term input risk.

| Metric | 2024 Value | Implication |

|---|---|---|

| Brent | $86/bbl | drives resin costs |

| Henry Hub | $3.70/MMBtu | impacts crackers |

| Logistics surcharge | ~30% | short-term margin pressure |

| Supplier concentration | High for catalysts | switching costs |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored for Dow, uncovering competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and emerging disruptors that affect pricing, margins, and market share.

A concise Five Forces dashboard that highlights competitive pressures and actionable levers—ideal for rapid strategy pivots and boardroom decisions.

Customers Bargaining Power

Large OEMs and converters

Packaging majors, auto OEMs, and building-product converters buy at scale and negotiate aggressively; the global packaging market was valued at about 1.05 trillion USD in 2024, concentrating buying power. Their volume concentration yields price concessions and favorable service terms, with multi-year supply agreements (typically 3–5 years) standardizing formulas but squeezing margins. Dow in 2024 traded price for share and customer stickiness as a strategic response.

Product differentiation via performance

Engineered grades, application know-how and technical services make direct comparability difficult; in 2024 specialty/high-spec materials represented over 50% of industry value, reducing pure price-based competition. When performance is mission-critical, switching risk and qualification cycles deter buyers and sustain supplier leverage. Commodity grades face far greater price pressure and lower margins.

Switching costs and qualification

End-users face tooling, certification and regulatory requalification—FDA 510(k) and similar pathways in 2024 typically add ~4–6 months and validation programs (automotive, medical) can extend 12–36 months and cost $100k–$1M+, which slows churn and supports pricing discipline. Healthcare and mobility face the longest cycles; packaging switches in weeks–a few months, raising buyer leverage.

Access to alternatives and tenders

Buyers run competitive tenders across global resin producers, leveraging daily spot-price benchmarks from ICIS, Platts and other indices to strengthen negotiation leverage. Visibility to these benchmarks and digital procurement tools increases price transparency and shortens sourcing cycles. Dow responds by emphasizing solution selling and value-in-use claims to shift focus from spot price to lifecycle value.

- Benchmark sources: ICIS, Platts, IHS

- Buyer tools: digital procurement, e-tenders

- Dow strategy: solution selling, value-in-use

Sustainability and EPR demands

Customers increasingly require recyclability, bio-based content and lower carbon footprints, and 2024 procurement trends show recycled-content and EPR compliance clauses becoming standard in EU and North American tenders.

These regulations create quasi-spec lock-ins that let buyers demand upgrades without price uplift, while Dow’s decarbonization and circular-product portfolio can reclaim margin through value-added offerings tied to certifications.

Certifications and verified life-cycle data now influence award decisions and supplier selection in 2024 procurement rounds.

- 2024 trend: recycled-content and EPR clauses common in major tenders

- Dow: leverages circular products to recapture value

- Certifications: decisive in contract awards

Buyer scale, 3–5yr contracts and specialty materials raise switching costs, compress margins

Buyers (packaging majors, auto OEMs, converters) concentrate volume—global packaging market ≈ 1.05 trillion USD in 2024—securing multi-year (3–5 yr) contracts that compress supplier margins. Specialty/high-spec materials >50% of industry value in 2024, raising switching costs and protecting supplier pricing. Procurement uses ICIS/Platts benchmarks and EPR/recycled-content clauses (standard in EU/NA), while qualification adds 4–36 months and $100k–$1M+.

| Metric | 2024 | Impact |

|---|---|---|

| Packaging market | ≈1.05T USD | Buyer scale → price leverage |

| Specialty share | >50% value | Reduces pure price competition |

| Contract length | 3–5 yrs | Sustains volume commitments |

| Qualification cost/time | $100k–$1M+, 4–36 months | Slows churn, protects margins |

| Procurement clauses | EPR/recycled standard (EU/NA) | Spec-driven demands |

Same Document Delivered

Dow Porter's Five Forces Analysis

This preview is the exact Dow Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is professionally written and fully formatted for immediate download and use. What you see here is the final deliverable, ready for your analysis and decision-making.