DSV PESTLE Analysis

Skip the Research. Get the Strategy.

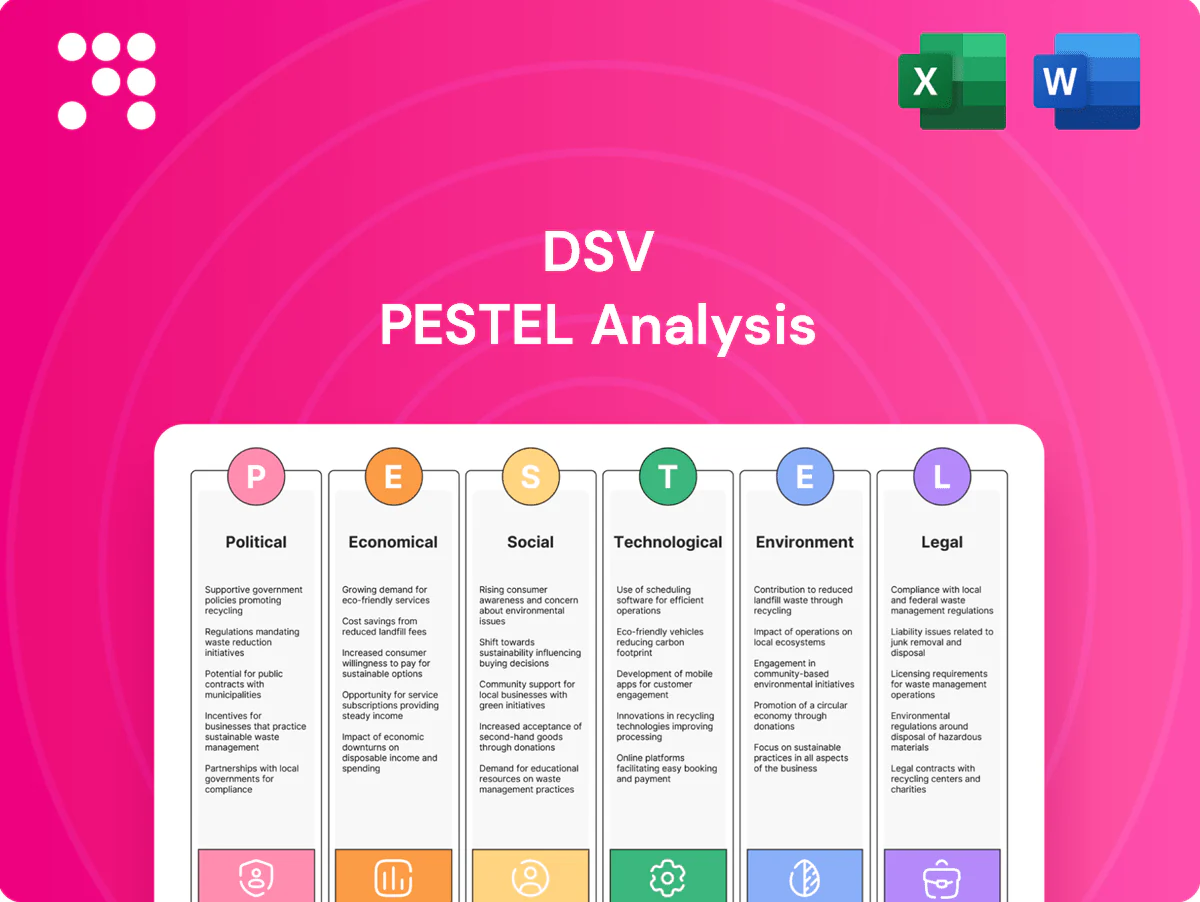

Unlock strategic clarity with our DSV PESTLE analysis—concise yet powerful insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory. Ideal for investors, consultants, and strategists, this brief highlights risks and growth levers you can act on immediately. Purchase the full, fully editable report to access deep-dive intelligence and ready-to-use recommendations.

Political factors

Trade policy shifts

Changes in tariffs, FTAs and customs regimes—over 350 FTAs are in force (WTO, 2024)—directly alter routing, costs and lead times, forcing DSV to re-route capacity and adjust pricing. DSV must flex networks to exploit new corridors while mitigating sudden barriers; scenario planning and multi-country brokerage cuts shock exposure. Proactive government relations help anticipate policy moves.

Geopolitical instability

Conflicts, sanctions and port closures disrupt air, sea, rail and road flows, as seen when the 2021 Suez blockage cost global trade an estimated 9.6bn USD per day; DSV must secure alternative gateways and diversify carriers to sustain service. Sanctions screening and embargo compliance add operational complexity and costs, while war-risk insurance premiums can spike—Red Sea premiums rose up to ~500% in 2023—raising logistics costs and margin pressure.

Public infrastructure policy

Government funding shapes port and rail capacity: the US Bipartisan Infrastructure Law earmarked $17 billion for ports, waterways and coastal resilience, while the EU Connecting Europe Facility commits €33.71 billion (2021–2027) to transport links. DSV benefits from digitized borders and expanded terminals that cut dwell times; conversely underinvestment raises congestion and demurrage, and public–private pilots can secure priority access.

Bureaucracy and corruption risk

Bureaucratic variability across markets slows customs clearance and raises costs; DSV counters this with strong governance, auditable trails and vetted agents to reduce facilitation risk. Standardized SOPs across operations limit local deviation and help maintain compliance. Transparency tools and whistleblowing channels further protect DSVs reputation and reduce exposure to corruption-related losses.

- Governance: centralized audit trails

- Controls: vetted local agents

- SOPs: standardized global procedures

- Integrity: transparency tools and whistleblowing

Political climate on sustainability

Political momentum from the Paris Agreement and EU Fit for 55 pushes national roadmaps and AFIR targets, making policy support for green corridors and alternative fuels key to lowering operating emissions; subsidies and mandates are shifting fleet and facility CAPEX. Aligning with tender-linked KPIs and reporting can unlock EU/ national incentives and green procurement advantages.

- Policy: Paris Agreement; Fit for 55/AFIR

- Impact: shifts CAPEX to low-emission fleets

- Tender win: alignment with national roadmaps required

- Incentive: KPI reporting unlocks subsidies

350+ FTAs, conflicts and green rules force logistics to reroute

Over 350 FTAs (WTO, 2024) reshape routes, costs and pricing; DSV must re-route capacity and flex networks. Conflicts/sanctions (Suez 2021 ~9.6bn USD/day) and rising war-risk premiums (Red Sea ~+500% in 2023) disrupt flows and raise insurance costs. Infrastructure funding (US $17bn; EU €33.71bn) and green rules (Fit for 55/AFIR) shift CAPEX to low-emission fleets.

| Factor | Key stat |

|---|---|

| FTAs | 350+ (WTO, 2024) |

| Trade shock | 9.6bn USD/day (Suez, 2021) |

| Insurance | +~500% Red Sea (2023) |

| Infrastructure | US $17bn / €33.71bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact DSV, using data-driven trends and region/industry specificity to identify risks and opportunities. Designed for executives, investors and advisors, the analysis offers detailed subpoints, forward-looking insights and clean formatting ready for business plans, pitch decks or scenario planning.

A concise, visually segmented PESTLE summary for DSV that’s easily shared and dropped into presentations, enabling quick alignment across teams and focused discussion on external risks and market positioning.

Economic factors

Global demand cycles

Global trade volumes closely follow GDP, retail sales and industrial output, with IMF projecting global GDP growth near 3.2% in 2025, directly affecting lane utilization across air, sea and road. DSV records revenue volatility as cycles shift, with notable mode mix swings during 2023–24 demand swings. Flexible capacity contracts and sector diversification (e.g., e-commerce, pharma) smooth earnings. Accurate demand forecasting drives pricing and space-allocation decisions.

Fuel and energy costs

Fuel and energy costs—jet, marine and diesel—cascade into surcharges and compress margins, with fuel historically representing roughly 20–40% of freight unit costs and Brent averaging about 86 USD/barrel in 2024 (EIA). DSV mitigates via hedging and efficiency programs to protect unit economics. Route optimization and modal shifts (road to rail/sea) reduce exposure. Rapid, clear customer pass-through mechanisms are essential to recover volatility.

Freight rate volatility

Ocean and air spot markets still swing with capacity and disruptions: Xeneta shows ocean spot rates down about 60% from the 2021 peak to 2024, while IATA airfreight rates fell roughly 35% over the same period. DSV’s mix of contract and spot business and global scale—DSV reported DKK 146.7bn revenue and ~89,000 employees in 2023—helps secure allocations and better terms. Data-driven, lane-level pricing tools improve per-lane contribution and stabilize yields.

FX and interest rates

DSV earns roughly 85% of revenue outside Denmark, creating material translation and transaction FX risks; disciplined hedging and natural currency offsets are vital. With policy rates around Fed 5.25% and ECB ~4.0% (mid‑2025), higher rates pressure customer inventories and raise credit risk, so tight working capital management preserves liquidity.

- FX exposure ~85% non‑DKK revenue

- Hedging + natural offsets essential

- Rates: Fed 5.25%, ECB ~4.0% (mid‑2025)

- Working capital discipline = resilience

Labor market dynamics

Driver, warehouse and broker talent shortages have pushed wages and turnover higher, pressuring margins while DSV employed over 75,000 staff in 2024; automation and structured training programs have measurably boosted productivity and retention; nearshoring trends are shifting labor footprints across Europe and the Americas; vendor partnerships help absorb peak-capacity spikes.

- shortage: higher wages, turnover

- automation: productivity + retention

- nearshoring: regional footprint shift

- vendor partnerships: peak capacity cover

350+ FTAs, conflicts and green rules force logistics to reroute

Global GDP ~3.2% (IMF 2025) drives lane demand; DSV revenue cyclicality (DKK146.7bn 2023) requires flexible capacity and lane-level pricing. Brent ~86 USD/bbl (2024) and fuel 20–40% of unit costs pressure margins; hedging and modal shifts mitigate. FX risk ~85% non‑DKK revenue; Fed 5.25% / ECB ~4.0% (mid‑2025) tighten working capital; labour shortages raise wages despite automation gains.

| Metric | Value |

|---|---|

| Global GDP 2025 | ~3.2% |

| Brent 2024 | ~86 USD/bbl |

| DSV Revenue 2023 | DKK 146.7bn |

| FX exposure | ~85% non‑DKK |

Same Document Delivered

DSV PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This DSV PESTLE Analysis delivers a concise, actionable assessment of political, economic, social, technological, legal, and environmental factors affecting DSV. Use it immediately for strategic planning, investment decisions, or competitive analysis.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our DSV PESTLE analysis—concise yet powerful insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory. Ideal for investors, consultants, and strategists, this brief highlights risks and growth levers you can act on immediately. Purchase the full, fully editable report to access deep-dive intelligence and ready-to-use recommendations.

Political factors

Trade policy shifts

Changes in tariffs, FTAs and customs regimes—over 350 FTAs are in force (WTO, 2024)—directly alter routing, costs and lead times, forcing DSV to re-route capacity and adjust pricing. DSV must flex networks to exploit new corridors while mitigating sudden barriers; scenario planning and multi-country brokerage cuts shock exposure. Proactive government relations help anticipate policy moves.

Geopolitical instability

Conflicts, sanctions and port closures disrupt air, sea, rail and road flows, as seen when the 2021 Suez blockage cost global trade an estimated 9.6bn USD per day; DSV must secure alternative gateways and diversify carriers to sustain service. Sanctions screening and embargo compliance add operational complexity and costs, while war-risk insurance premiums can spike—Red Sea premiums rose up to ~500% in 2023—raising logistics costs and margin pressure.

Public infrastructure policy

Government funding shapes port and rail capacity: the US Bipartisan Infrastructure Law earmarked $17 billion for ports, waterways and coastal resilience, while the EU Connecting Europe Facility commits €33.71 billion (2021–2027) to transport links. DSV benefits from digitized borders and expanded terminals that cut dwell times; conversely underinvestment raises congestion and demurrage, and public–private pilots can secure priority access.

Bureaucracy and corruption risk

Bureaucratic variability across markets slows customs clearance and raises costs; DSV counters this with strong governance, auditable trails and vetted agents to reduce facilitation risk. Standardized SOPs across operations limit local deviation and help maintain compliance. Transparency tools and whistleblowing channels further protect DSVs reputation and reduce exposure to corruption-related losses.

- Governance: centralized audit trails

- Controls: vetted local agents

- SOPs: standardized global procedures

- Integrity: transparency tools and whistleblowing

Political climate on sustainability

Political momentum from the Paris Agreement and EU Fit for 55 pushes national roadmaps and AFIR targets, making policy support for green corridors and alternative fuels key to lowering operating emissions; subsidies and mandates are shifting fleet and facility CAPEX. Aligning with tender-linked KPIs and reporting can unlock EU/ national incentives and green procurement advantages.

- Policy: Paris Agreement; Fit for 55/AFIR

- Impact: shifts CAPEX to low-emission fleets

- Tender win: alignment with national roadmaps required

- Incentive: KPI reporting unlocks subsidies

350+ FTAs, conflicts and green rules force logistics to reroute

Over 350 FTAs (WTO, 2024) reshape routes, costs and pricing; DSV must re-route capacity and flex networks. Conflicts/sanctions (Suez 2021 ~9.6bn USD/day) and rising war-risk premiums (Red Sea ~+500% in 2023) disrupt flows and raise insurance costs. Infrastructure funding (US $17bn; EU €33.71bn) and green rules (Fit for 55/AFIR) shift CAPEX to low-emission fleets.

| Factor | Key stat |

|---|---|

| FTAs | 350+ (WTO, 2024) |

| Trade shock | 9.6bn USD/day (Suez, 2021) |

| Insurance | +~500% Red Sea (2023) |

| Infrastructure | US $17bn / €33.71bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact DSV, using data-driven trends and region/industry specificity to identify risks and opportunities. Designed for executives, investors and advisors, the analysis offers detailed subpoints, forward-looking insights and clean formatting ready for business plans, pitch decks or scenario planning.

A concise, visually segmented PESTLE summary for DSV that’s easily shared and dropped into presentations, enabling quick alignment across teams and focused discussion on external risks and market positioning.

Economic factors

Global demand cycles

Global trade volumes closely follow GDP, retail sales and industrial output, with IMF projecting global GDP growth near 3.2% in 2025, directly affecting lane utilization across air, sea and road. DSV records revenue volatility as cycles shift, with notable mode mix swings during 2023–24 demand swings. Flexible capacity contracts and sector diversification (e.g., e-commerce, pharma) smooth earnings. Accurate demand forecasting drives pricing and space-allocation decisions.

Fuel and energy costs

Fuel and energy costs—jet, marine and diesel—cascade into surcharges and compress margins, with fuel historically representing roughly 20–40% of freight unit costs and Brent averaging about 86 USD/barrel in 2024 (EIA). DSV mitigates via hedging and efficiency programs to protect unit economics. Route optimization and modal shifts (road to rail/sea) reduce exposure. Rapid, clear customer pass-through mechanisms are essential to recover volatility.

Freight rate volatility

Ocean and air spot markets still swing with capacity and disruptions: Xeneta shows ocean spot rates down about 60% from the 2021 peak to 2024, while IATA airfreight rates fell roughly 35% over the same period. DSV’s mix of contract and spot business and global scale—DSV reported DKK 146.7bn revenue and ~89,000 employees in 2023—helps secure allocations and better terms. Data-driven, lane-level pricing tools improve per-lane contribution and stabilize yields.

FX and interest rates

DSV earns roughly 85% of revenue outside Denmark, creating material translation and transaction FX risks; disciplined hedging and natural currency offsets are vital. With policy rates around Fed 5.25% and ECB ~4.0% (mid‑2025), higher rates pressure customer inventories and raise credit risk, so tight working capital management preserves liquidity.

- FX exposure ~85% non‑DKK revenue

- Hedging + natural offsets essential

- Rates: Fed 5.25%, ECB ~4.0% (mid‑2025)

- Working capital discipline = resilience

Labor market dynamics

Driver, warehouse and broker talent shortages have pushed wages and turnover higher, pressuring margins while DSV employed over 75,000 staff in 2024; automation and structured training programs have measurably boosted productivity and retention; nearshoring trends are shifting labor footprints across Europe and the Americas; vendor partnerships help absorb peak-capacity spikes.

- shortage: higher wages, turnover

- automation: productivity + retention

- nearshoring: regional footprint shift

- vendor partnerships: peak capacity cover

350+ FTAs, conflicts and green rules force logistics to reroute

Global GDP ~3.2% (IMF 2025) drives lane demand; DSV revenue cyclicality (DKK146.7bn 2023) requires flexible capacity and lane-level pricing. Brent ~86 USD/bbl (2024) and fuel 20–40% of unit costs pressure margins; hedging and modal shifts mitigate. FX risk ~85% non‑DKK revenue; Fed 5.25% / ECB ~4.0% (mid‑2025) tighten working capital; labour shortages raise wages despite automation gains.

| Metric | Value |

|---|---|

| Global GDP 2025 | ~3.2% |

| Brent 2024 | ~86 USD/bbl |

| DSV Revenue 2023 | DKK 146.7bn |

| FX exposure | ~85% non‑DKK |

Same Document Delivered

DSV PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This DSV PESTLE Analysis delivers a concise, actionable assessment of political, economic, social, technological, legal, and environmental factors affecting DSV. Use it immediately for strategic planning, investment decisions, or competitive analysis.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our DSV PESTLE analysis—concise yet powerful insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory. Ideal for investors, consultants, and strategists, this brief highlights risks and growth levers you can act on immediately. Purchase the full, fully editable report to access deep-dive intelligence and ready-to-use recommendations.

Political factors

Trade policy shifts

Changes in tariffs, FTAs and customs regimes—over 350 FTAs are in force (WTO, 2024)—directly alter routing, costs and lead times, forcing DSV to re-route capacity and adjust pricing. DSV must flex networks to exploit new corridors while mitigating sudden barriers; scenario planning and multi-country brokerage cuts shock exposure. Proactive government relations help anticipate policy moves.

Geopolitical instability

Conflicts, sanctions and port closures disrupt air, sea, rail and road flows, as seen when the 2021 Suez blockage cost global trade an estimated 9.6bn USD per day; DSV must secure alternative gateways and diversify carriers to sustain service. Sanctions screening and embargo compliance add operational complexity and costs, while war-risk insurance premiums can spike—Red Sea premiums rose up to ~500% in 2023—raising logistics costs and margin pressure.

Public infrastructure policy

Government funding shapes port and rail capacity: the US Bipartisan Infrastructure Law earmarked $17 billion for ports, waterways and coastal resilience, while the EU Connecting Europe Facility commits €33.71 billion (2021–2027) to transport links. DSV benefits from digitized borders and expanded terminals that cut dwell times; conversely underinvestment raises congestion and demurrage, and public–private pilots can secure priority access.

Bureaucracy and corruption risk

Bureaucratic variability across markets slows customs clearance and raises costs; DSV counters this with strong governance, auditable trails and vetted agents to reduce facilitation risk. Standardized SOPs across operations limit local deviation and help maintain compliance. Transparency tools and whistleblowing channels further protect DSVs reputation and reduce exposure to corruption-related losses.

- Governance: centralized audit trails

- Controls: vetted local agents

- SOPs: standardized global procedures

- Integrity: transparency tools and whistleblowing

Political climate on sustainability

Political momentum from the Paris Agreement and EU Fit for 55 pushes national roadmaps and AFIR targets, making policy support for green corridors and alternative fuels key to lowering operating emissions; subsidies and mandates are shifting fleet and facility CAPEX. Aligning with tender-linked KPIs and reporting can unlock EU/ national incentives and green procurement advantages.

- Policy: Paris Agreement; Fit for 55/AFIR

- Impact: shifts CAPEX to low-emission fleets

- Tender win: alignment with national roadmaps required

- Incentive: KPI reporting unlocks subsidies

350+ FTAs, conflicts and green rules force logistics to reroute

Over 350 FTAs (WTO, 2024) reshape routes, costs and pricing; DSV must re-route capacity and flex networks. Conflicts/sanctions (Suez 2021 ~9.6bn USD/day) and rising war-risk premiums (Red Sea ~+500% in 2023) disrupt flows and raise insurance costs. Infrastructure funding (US $17bn; EU €33.71bn) and green rules (Fit for 55/AFIR) shift CAPEX to low-emission fleets.

| Factor | Key stat |

|---|---|

| FTAs | 350+ (WTO, 2024) |

| Trade shock | 9.6bn USD/day (Suez, 2021) |

| Insurance | +~500% Red Sea (2023) |

| Infrastructure | US $17bn / €33.71bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact DSV, using data-driven trends and region/industry specificity to identify risks and opportunities. Designed for executives, investors and advisors, the analysis offers detailed subpoints, forward-looking insights and clean formatting ready for business plans, pitch decks or scenario planning.

A concise, visually segmented PESTLE summary for DSV that’s easily shared and dropped into presentations, enabling quick alignment across teams and focused discussion on external risks and market positioning.

Economic factors

Global demand cycles

Global trade volumes closely follow GDP, retail sales and industrial output, with IMF projecting global GDP growth near 3.2% in 2025, directly affecting lane utilization across air, sea and road. DSV records revenue volatility as cycles shift, with notable mode mix swings during 2023–24 demand swings. Flexible capacity contracts and sector diversification (e.g., e-commerce, pharma) smooth earnings. Accurate demand forecasting drives pricing and space-allocation decisions.

Fuel and energy costs

Fuel and energy costs—jet, marine and diesel—cascade into surcharges and compress margins, with fuel historically representing roughly 20–40% of freight unit costs and Brent averaging about 86 USD/barrel in 2024 (EIA). DSV mitigates via hedging and efficiency programs to protect unit economics. Route optimization and modal shifts (road to rail/sea) reduce exposure. Rapid, clear customer pass-through mechanisms are essential to recover volatility.

Freight rate volatility

Ocean and air spot markets still swing with capacity and disruptions: Xeneta shows ocean spot rates down about 60% from the 2021 peak to 2024, while IATA airfreight rates fell roughly 35% over the same period. DSV’s mix of contract and spot business and global scale—DSV reported DKK 146.7bn revenue and ~89,000 employees in 2023—helps secure allocations and better terms. Data-driven, lane-level pricing tools improve per-lane contribution and stabilize yields.

FX and interest rates

DSV earns roughly 85% of revenue outside Denmark, creating material translation and transaction FX risks; disciplined hedging and natural currency offsets are vital. With policy rates around Fed 5.25% and ECB ~4.0% (mid‑2025), higher rates pressure customer inventories and raise credit risk, so tight working capital management preserves liquidity.

- FX exposure ~85% non‑DKK revenue

- Hedging + natural offsets essential

- Rates: Fed 5.25%, ECB ~4.0% (mid‑2025)

- Working capital discipline = resilience

Labor market dynamics

Driver, warehouse and broker talent shortages have pushed wages and turnover higher, pressuring margins while DSV employed over 75,000 staff in 2024; automation and structured training programs have measurably boosted productivity and retention; nearshoring trends are shifting labor footprints across Europe and the Americas; vendor partnerships help absorb peak-capacity spikes.

- shortage: higher wages, turnover

- automation: productivity + retention

- nearshoring: regional footprint shift

- vendor partnerships: peak capacity cover

350+ FTAs, conflicts and green rules force logistics to reroute

Global GDP ~3.2% (IMF 2025) drives lane demand; DSV revenue cyclicality (DKK146.7bn 2023) requires flexible capacity and lane-level pricing. Brent ~86 USD/bbl (2024) and fuel 20–40% of unit costs pressure margins; hedging and modal shifts mitigate. FX risk ~85% non‑DKK revenue; Fed 5.25% / ECB ~4.0% (mid‑2025) tighten working capital; labour shortages raise wages despite automation gains.

| Metric | Value |

|---|---|

| Global GDP 2025 | ~3.2% |

| Brent 2024 | ~86 USD/bbl |

| DSV Revenue 2023 | DKK 146.7bn |

| FX exposure | ~85% non‑DKK |

Same Document Delivered

DSV PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This DSV PESTLE Analysis delivers a concise, actionable assessment of political, economic, social, technological, legal, and environmental factors affecting DSV. Use it immediately for strategic planning, investment decisions, or competitive analysis.