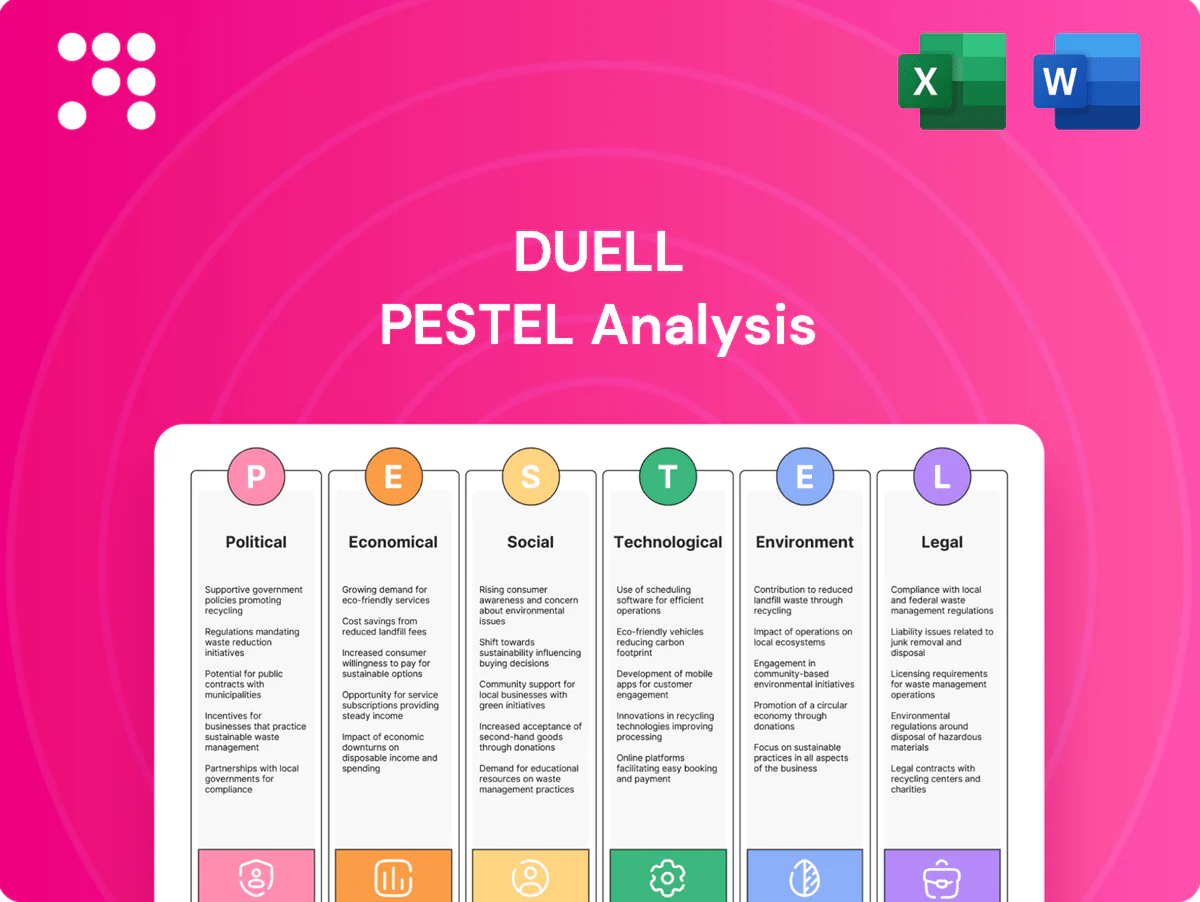

Duell PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological disruption are shaping Duell’s strategic outlook in our concise PESTLE summary. This ready-to-use analysis highlights risks and opportunities for investors, consultants, and planners. Purchase the full PESTLE for the complete, editable breakdown and actionable insights to guide your next decision.

Political factors

EU trade and customs policy

Single market rules and the Union Customs Code govern sourcing and pricing for Duell, with EU goods imports at about €5 trillion annually shaping supply costs. Anti-dumping duties and shifts in common external tariffs can change landed costs and competitiveness. Compliance with EU product origin rules affects brand positioning and margin mix. Monitoring Customs reform and ICS2 (mandatory for air since 2024, expanding through 2025) is critical for cross-border flows.

Nordic and European industrial policy

Nordic and European industrial policy shapes Duell through subsidies and incentives for electrification, manufacturing and logistics that influence suppliers and dealer investment decisions. EU targets 55% greenhouse gas reduction by 2030 and instruments like NextGenerationEU (€806.9bn) and the 2021–2027 Cohesion Policy (€392.8bn) fund green infrastructure, enabling public procurement and regional distribution hubs that can lower costs. Divergent national rules in Finland, Sweden, Norway and Denmark complicate network optimization, while policy-driven upgrades to ports, rail and cold chains enhance delivery reliability.

Geopolitical risk and sanctions

Russia-related sanctions and wider Baltic tensions elevate supply-chain and payment risks; EU/US measures since 2022 and selective SWIFT exclusions constrain bank routing. Restrictions on dual-use items and tech exports have already disrupted catalogs and timelines for spare parts. Insurance and financing constraints — war-risk premiums spiked up to 700% on some Black Sea routes in 2022 — increase working capital needs. Scenario planning (buffers, alternative suppliers, payment corridors) protects dealer service levels.

Energy and transport policies

Energy and transport policies reshape freight economics: EU carbon prices averaged ~€90–€110/t in 2024–H1 2025 and EU diesel averaged ~€1.70/L in 2024, while expanding fuel taxation and road tolls raise per-km costs; green corridor and low-emission truck incentives (EU funding >€500m for corridor pilots 2021–24) shift last-mile partners and SLAs, and national winter road maintenance regimes alter seasonal reliability, so coordination with 3PLs reduces policy-driven lead-time volatility.

- Fuel tax + tolls increase unit cost

- EU carbon ~€90–110/t (2024–H1 2025)

- Diesel ~€1.70/L (EU 2024)

- €500m+ green corridor funding (2021–24)

- 3PL coordination cuts lead-time risk

Political stability and regulatory harmonization

Stable Nordic governance supports long-term contracts and planning, and Nordic states consistently rank in the top 10 of Transparency International's CPI (2024), but divergent national implementations of EU directives create compliance complexity; the EU VAT gap was €137bn (2022/23), increasing cross-border VAT risk while e-invoicing mandates and PEPPOL growth force system alignment.

- Top10_CPI_2024

- EU_VAT_gap_€137bn_22/23

- e-invoicing_PEPPOL_alignment

- harmonized_dealer_docs_reduce_friction

EU customs, carbon pricing and VAT gap reshape Nordic import costs and freight pricing

EU customs, ICS2 (air mandatory 2024) and anti-dumping rules directly affect Duell's landed costs and compliance. Green industrial funds (NextGenerationEU €806.9bn) and EU carbon ~€90–110/t (2024–H1 2025) shift supplier investment and freight pricing. Nordic governance is stable (Top10 CPI 2024) but VAT gap €137bn raises cross-border tax risk.

| Indicator | Value |

|---|---|

| NextGenerationEU | €806.9bn |

| EU carbon (2024–H1 2025) | €90–110/t |

| Diesel (EU 2024) | €1.70/L |

| EU VAT gap (22/23) | €137bn |

What is included in the product

Explores how macro-environmental forces uniquely affect Duell across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives, investors, and strategists.

Duell PESTLE provides a clean, summarized version of the full analysis—visually segmented by PESTLE categories for quick interpretation and easily dropped into presentations or shared across teams for fast alignment.

Economic factors

Consumer discretionary cycles

Powersports and marine spending is highly cyclical and closely tracks real incomes and consumer confidence; downturns typically depress apparel and accessories first, then core parts and units. Counter-seasonal and maintenance SKUs often buffer revenue volatility by providing steady aftermarket demand. Flexible purchasing and inventory policies reduce markdown risk and protect margins during demand swings.

Currency fluctuations (EUR, SEK, NOK)

FX swings (EUR/SEK ~10.8–12.4, EUR/NOK ~10.0–11.5 in 2024–H1 2025) raise import costs and force cross-border price moves across Duell’s Nordic footprint. Hedging and multi-currency price lists have stabilized margins, while currency-driven demand shifts have reallocated sales between Sweden, Norway and EU. Supplier contracts with currency clauses share risk.

Inflation and interest rates

Input-cost inflation (U.S. CPI 2024: 3.4%) pushes MSRP higher, compressing demand and unit volumes; Duell must weigh price increases against price elasticity. Higher policy rates (Fed funds 5.25–5.5% in 2024–25) and auto loan rates (~8–10% in 2024) tighten dealer financing and consumer credit for vehicles and upgrades. Early-buy programs and extended terms can lift sell-in but strain cash flow and working capital. Rigorous cost discipline and SKU rationalization protect margin and free cash.

Freight and warehousing costs

Ocean, road, and parcel rates directly compress gross margins on bulky items—container rates fell roughly 80% from 2021 peaks to 2024 (Drewry), while US diesel averaged about $3.50/gal in 2024 (EIA); labor scarcity and rising energy costs pushed 3PL and warehouse fees higher, and improvements in network design and slotting cut handling cost per line; better forecast accuracy can lower expedited shipments by up to 30%.

- Ocean rates down ~80% vs 2021 (Drewry)

- US diesel ≈ $3.50/gal (2024, EIA)

- Forecast accuracy → expedited cuts up to 30%

- Slotting/network design reduces cost per line

Dealer network health

Dealer solvency and inventory turns (typically ~4–6 turns/year in retail in 2024) directly govern Duell’s sell-through and cash conversion; weak solvency compresses orders and raises aged stock. Consolidation shifts bargaining power and can change territory coverage rapidly in 2024–25. Better data-sharing raises assortment accuracy and replenishment speed, while targeted coop marketing boosts local demand.

- Dealer solvency: liquidity risk affects orders

- Inventory turns: ~4–6/year impacts cash flow

- Consolidation: alters bargaining/coverage

- Data-sharing: improves replenishment

- Coop marketing: drives local sell-through

EU customs, carbon pricing and VAT gap reshape Nordic import costs and freight pricing

Demand is cyclical, tied to real incomes and confidence; aftermarket SKUs cushion volatility. FX (EUR/SEK 10.8–12.4; EUR/NOK 10.0–11.5 in 2024–H1 2025), higher rates (Fed 5.25–5.5%) and CPI 3.4% compress margins and volumes. Logistics and dealer solvency (inventory turns 4–6/yr) directly affect cash conversion and sell-through.

| Metric | 2024–H1 2025 |

|---|---|

| EUR/SEK | 10.8–12.4 |

| EUR/NOK | 10.0–11.5 |

| Fed funds | 5.25–5.5% |

| CPI (US) | 3.4% |

| Inventory turns | 4–6/yr |

Full Version Awaits

Duell PESTLE Analysis

The preview shown here is the exact Duell PESTLE Analysis document you’ll receive after purchase—fully formatted, complete, and ready to use. The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured analysis you’ll own.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological disruption are shaping Duell’s strategic outlook in our concise PESTLE summary. This ready-to-use analysis highlights risks and opportunities for investors, consultants, and planners. Purchase the full PESTLE for the complete, editable breakdown and actionable insights to guide your next decision.

Political factors

EU trade and customs policy

Single market rules and the Union Customs Code govern sourcing and pricing for Duell, with EU goods imports at about €5 trillion annually shaping supply costs. Anti-dumping duties and shifts in common external tariffs can change landed costs and competitiveness. Compliance with EU product origin rules affects brand positioning and margin mix. Monitoring Customs reform and ICS2 (mandatory for air since 2024, expanding through 2025) is critical for cross-border flows.

Nordic and European industrial policy

Nordic and European industrial policy shapes Duell through subsidies and incentives for electrification, manufacturing and logistics that influence suppliers and dealer investment decisions. EU targets 55% greenhouse gas reduction by 2030 and instruments like NextGenerationEU (€806.9bn) and the 2021–2027 Cohesion Policy (€392.8bn) fund green infrastructure, enabling public procurement and regional distribution hubs that can lower costs. Divergent national rules in Finland, Sweden, Norway and Denmark complicate network optimization, while policy-driven upgrades to ports, rail and cold chains enhance delivery reliability.

Geopolitical risk and sanctions

Russia-related sanctions and wider Baltic tensions elevate supply-chain and payment risks; EU/US measures since 2022 and selective SWIFT exclusions constrain bank routing. Restrictions on dual-use items and tech exports have already disrupted catalogs and timelines for spare parts. Insurance and financing constraints — war-risk premiums spiked up to 700% on some Black Sea routes in 2022 — increase working capital needs. Scenario planning (buffers, alternative suppliers, payment corridors) protects dealer service levels.

Energy and transport policies

Energy and transport policies reshape freight economics: EU carbon prices averaged ~€90–€110/t in 2024–H1 2025 and EU diesel averaged ~€1.70/L in 2024, while expanding fuel taxation and road tolls raise per-km costs; green corridor and low-emission truck incentives (EU funding >€500m for corridor pilots 2021–24) shift last-mile partners and SLAs, and national winter road maintenance regimes alter seasonal reliability, so coordination with 3PLs reduces policy-driven lead-time volatility.

- Fuel tax + tolls increase unit cost

- EU carbon ~€90–110/t (2024–H1 2025)

- Diesel ~€1.70/L (EU 2024)

- €500m+ green corridor funding (2021–24)

- 3PL coordination cuts lead-time risk

Political stability and regulatory harmonization

Stable Nordic governance supports long-term contracts and planning, and Nordic states consistently rank in the top 10 of Transparency International's CPI (2024), but divergent national implementations of EU directives create compliance complexity; the EU VAT gap was €137bn (2022/23), increasing cross-border VAT risk while e-invoicing mandates and PEPPOL growth force system alignment.

- Top10_CPI_2024

- EU_VAT_gap_€137bn_22/23

- e-invoicing_PEPPOL_alignment

- harmonized_dealer_docs_reduce_friction

EU customs, carbon pricing and VAT gap reshape Nordic import costs and freight pricing

EU customs, ICS2 (air mandatory 2024) and anti-dumping rules directly affect Duell's landed costs and compliance. Green industrial funds (NextGenerationEU €806.9bn) and EU carbon ~€90–110/t (2024–H1 2025) shift supplier investment and freight pricing. Nordic governance is stable (Top10 CPI 2024) but VAT gap €137bn raises cross-border tax risk.

| Indicator | Value |

|---|---|

| NextGenerationEU | €806.9bn |

| EU carbon (2024–H1 2025) | €90–110/t |

| Diesel (EU 2024) | €1.70/L |

| EU VAT gap (22/23) | €137bn |

What is included in the product

Explores how macro-environmental forces uniquely affect Duell across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives, investors, and strategists.

Duell PESTLE provides a clean, summarized version of the full analysis—visually segmented by PESTLE categories for quick interpretation and easily dropped into presentations or shared across teams for fast alignment.

Economic factors

Consumer discretionary cycles

Powersports and marine spending is highly cyclical and closely tracks real incomes and consumer confidence; downturns typically depress apparel and accessories first, then core parts and units. Counter-seasonal and maintenance SKUs often buffer revenue volatility by providing steady aftermarket demand. Flexible purchasing and inventory policies reduce markdown risk and protect margins during demand swings.

Currency fluctuations (EUR, SEK, NOK)

FX swings (EUR/SEK ~10.8–12.4, EUR/NOK ~10.0–11.5 in 2024–H1 2025) raise import costs and force cross-border price moves across Duell’s Nordic footprint. Hedging and multi-currency price lists have stabilized margins, while currency-driven demand shifts have reallocated sales between Sweden, Norway and EU. Supplier contracts with currency clauses share risk.

Inflation and interest rates

Input-cost inflation (U.S. CPI 2024: 3.4%) pushes MSRP higher, compressing demand and unit volumes; Duell must weigh price increases against price elasticity. Higher policy rates (Fed funds 5.25–5.5% in 2024–25) and auto loan rates (~8–10% in 2024) tighten dealer financing and consumer credit for vehicles and upgrades. Early-buy programs and extended terms can lift sell-in but strain cash flow and working capital. Rigorous cost discipline and SKU rationalization protect margin and free cash.

Freight and warehousing costs

Ocean, road, and parcel rates directly compress gross margins on bulky items—container rates fell roughly 80% from 2021 peaks to 2024 (Drewry), while US diesel averaged about $3.50/gal in 2024 (EIA); labor scarcity and rising energy costs pushed 3PL and warehouse fees higher, and improvements in network design and slotting cut handling cost per line; better forecast accuracy can lower expedited shipments by up to 30%.

- Ocean rates down ~80% vs 2021 (Drewry)

- US diesel ≈ $3.50/gal (2024, EIA)

- Forecast accuracy → expedited cuts up to 30%

- Slotting/network design reduces cost per line

Dealer network health

Dealer solvency and inventory turns (typically ~4–6 turns/year in retail in 2024) directly govern Duell’s sell-through and cash conversion; weak solvency compresses orders and raises aged stock. Consolidation shifts bargaining power and can change territory coverage rapidly in 2024–25. Better data-sharing raises assortment accuracy and replenishment speed, while targeted coop marketing boosts local demand.

- Dealer solvency: liquidity risk affects orders

- Inventory turns: ~4–6/year impacts cash flow

- Consolidation: alters bargaining/coverage

- Data-sharing: improves replenishment

- Coop marketing: drives local sell-through

EU customs, carbon pricing and VAT gap reshape Nordic import costs and freight pricing

Demand is cyclical, tied to real incomes and confidence; aftermarket SKUs cushion volatility. FX (EUR/SEK 10.8–12.4; EUR/NOK 10.0–11.5 in 2024–H1 2025), higher rates (Fed 5.25–5.5%) and CPI 3.4% compress margins and volumes. Logistics and dealer solvency (inventory turns 4–6/yr) directly affect cash conversion and sell-through.

| Metric | 2024–H1 2025 |

|---|---|

| EUR/SEK | 10.8–12.4 |

| EUR/NOK | 10.0–11.5 |

| Fed funds | 5.25–5.5% |

| CPI (US) | 3.4% |

| Inventory turns | 4–6/yr |

Full Version Awaits

Duell PESTLE Analysis

The preview shown here is the exact Duell PESTLE Analysis document you’ll receive after purchase—fully formatted, complete, and ready to use. The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured analysis you’ll own.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological disruption are shaping Duell’s strategic outlook in our concise PESTLE summary. This ready-to-use analysis highlights risks and opportunities for investors, consultants, and planners. Purchase the full PESTLE for the complete, editable breakdown and actionable insights to guide your next decision.

Political factors

EU trade and customs policy

Single market rules and the Union Customs Code govern sourcing and pricing for Duell, with EU goods imports at about €5 trillion annually shaping supply costs. Anti-dumping duties and shifts in common external tariffs can change landed costs and competitiveness. Compliance with EU product origin rules affects brand positioning and margin mix. Monitoring Customs reform and ICS2 (mandatory for air since 2024, expanding through 2025) is critical for cross-border flows.

Nordic and European industrial policy

Nordic and European industrial policy shapes Duell through subsidies and incentives for electrification, manufacturing and logistics that influence suppliers and dealer investment decisions. EU targets 55% greenhouse gas reduction by 2030 and instruments like NextGenerationEU (€806.9bn) and the 2021–2027 Cohesion Policy (€392.8bn) fund green infrastructure, enabling public procurement and regional distribution hubs that can lower costs. Divergent national rules in Finland, Sweden, Norway and Denmark complicate network optimization, while policy-driven upgrades to ports, rail and cold chains enhance delivery reliability.

Geopolitical risk and sanctions

Russia-related sanctions and wider Baltic tensions elevate supply-chain and payment risks; EU/US measures since 2022 and selective SWIFT exclusions constrain bank routing. Restrictions on dual-use items and tech exports have already disrupted catalogs and timelines for spare parts. Insurance and financing constraints — war-risk premiums spiked up to 700% on some Black Sea routes in 2022 — increase working capital needs. Scenario planning (buffers, alternative suppliers, payment corridors) protects dealer service levels.

Energy and transport policies

Energy and transport policies reshape freight economics: EU carbon prices averaged ~€90–€110/t in 2024–H1 2025 and EU diesel averaged ~€1.70/L in 2024, while expanding fuel taxation and road tolls raise per-km costs; green corridor and low-emission truck incentives (EU funding >€500m for corridor pilots 2021–24) shift last-mile partners and SLAs, and national winter road maintenance regimes alter seasonal reliability, so coordination with 3PLs reduces policy-driven lead-time volatility.

- Fuel tax + tolls increase unit cost

- EU carbon ~€90–110/t (2024–H1 2025)

- Diesel ~€1.70/L (EU 2024)

- €500m+ green corridor funding (2021–24)

- 3PL coordination cuts lead-time risk

Political stability and regulatory harmonization

Stable Nordic governance supports long-term contracts and planning, and Nordic states consistently rank in the top 10 of Transparency International's CPI (2024), but divergent national implementations of EU directives create compliance complexity; the EU VAT gap was €137bn (2022/23), increasing cross-border VAT risk while e-invoicing mandates and PEPPOL growth force system alignment.

- Top10_CPI_2024

- EU_VAT_gap_€137bn_22/23

- e-invoicing_PEPPOL_alignment

- harmonized_dealer_docs_reduce_friction

EU customs, carbon pricing and VAT gap reshape Nordic import costs and freight pricing

EU customs, ICS2 (air mandatory 2024) and anti-dumping rules directly affect Duell's landed costs and compliance. Green industrial funds (NextGenerationEU €806.9bn) and EU carbon ~€90–110/t (2024–H1 2025) shift supplier investment and freight pricing. Nordic governance is stable (Top10 CPI 2024) but VAT gap €137bn raises cross-border tax risk.

| Indicator | Value |

|---|---|

| NextGenerationEU | €806.9bn |

| EU carbon (2024–H1 2025) | €90–110/t |

| Diesel (EU 2024) | €1.70/L |

| EU VAT gap (22/23) | €137bn |

What is included in the product

Explores how macro-environmental forces uniquely affect Duell across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives, investors, and strategists.

Duell PESTLE provides a clean, summarized version of the full analysis—visually segmented by PESTLE categories for quick interpretation and easily dropped into presentations or shared across teams for fast alignment.

Economic factors

Consumer discretionary cycles

Powersports and marine spending is highly cyclical and closely tracks real incomes and consumer confidence; downturns typically depress apparel and accessories first, then core parts and units. Counter-seasonal and maintenance SKUs often buffer revenue volatility by providing steady aftermarket demand. Flexible purchasing and inventory policies reduce markdown risk and protect margins during demand swings.

Currency fluctuations (EUR, SEK, NOK)

FX swings (EUR/SEK ~10.8–12.4, EUR/NOK ~10.0–11.5 in 2024–H1 2025) raise import costs and force cross-border price moves across Duell’s Nordic footprint. Hedging and multi-currency price lists have stabilized margins, while currency-driven demand shifts have reallocated sales between Sweden, Norway and EU. Supplier contracts with currency clauses share risk.

Inflation and interest rates

Input-cost inflation (U.S. CPI 2024: 3.4%) pushes MSRP higher, compressing demand and unit volumes; Duell must weigh price increases against price elasticity. Higher policy rates (Fed funds 5.25–5.5% in 2024–25) and auto loan rates (~8–10% in 2024) tighten dealer financing and consumer credit for vehicles and upgrades. Early-buy programs and extended terms can lift sell-in but strain cash flow and working capital. Rigorous cost discipline and SKU rationalization protect margin and free cash.

Freight and warehousing costs

Ocean, road, and parcel rates directly compress gross margins on bulky items—container rates fell roughly 80% from 2021 peaks to 2024 (Drewry), while US diesel averaged about $3.50/gal in 2024 (EIA); labor scarcity and rising energy costs pushed 3PL and warehouse fees higher, and improvements in network design and slotting cut handling cost per line; better forecast accuracy can lower expedited shipments by up to 30%.

- Ocean rates down ~80% vs 2021 (Drewry)

- US diesel ≈ $3.50/gal (2024, EIA)

- Forecast accuracy → expedited cuts up to 30%

- Slotting/network design reduces cost per line

Dealer network health

Dealer solvency and inventory turns (typically ~4–6 turns/year in retail in 2024) directly govern Duell’s sell-through and cash conversion; weak solvency compresses orders and raises aged stock. Consolidation shifts bargaining power and can change territory coverage rapidly in 2024–25. Better data-sharing raises assortment accuracy and replenishment speed, while targeted coop marketing boosts local demand.

- Dealer solvency: liquidity risk affects orders

- Inventory turns: ~4–6/year impacts cash flow

- Consolidation: alters bargaining/coverage

- Data-sharing: improves replenishment

- Coop marketing: drives local sell-through

EU customs, carbon pricing and VAT gap reshape Nordic import costs and freight pricing

Demand is cyclical, tied to real incomes and confidence; aftermarket SKUs cushion volatility. FX (EUR/SEK 10.8–12.4; EUR/NOK 10.0–11.5 in 2024–H1 2025), higher rates (Fed 5.25–5.5%) and CPI 3.4% compress margins and volumes. Logistics and dealer solvency (inventory turns 4–6/yr) directly affect cash conversion and sell-through.

| Metric | 2024–H1 2025 |

|---|---|

| EUR/SEK | 10.8–12.4 |

| EUR/NOK | 10.0–11.5 |

| Fed funds | 5.25–5.5% |

| CPI (US) | 3.4% |

| Inventory turns | 4–6/yr |

Full Version Awaits

Duell PESTLE Analysis

The preview shown here is the exact Duell PESTLE Analysis document you’ll receive after purchase—fully formatted, complete, and ready to use. The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured analysis you’ll own.