Dufry Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

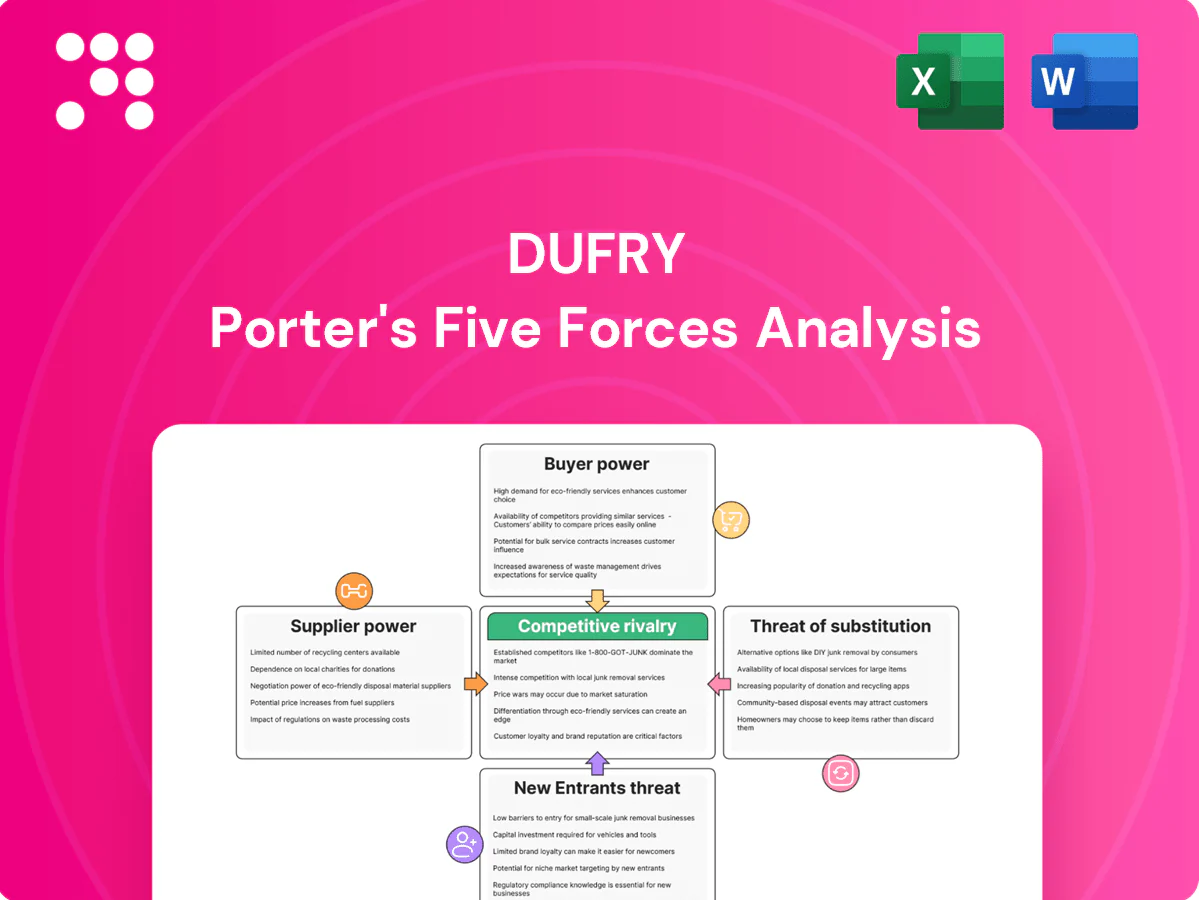

Dufry faces intense competitive rivalry in travel retail, with location advantage but margin pressure from other retailers and online channels. Supplier power is moderate; buyer power fluctuates with travel volumes. Threat of substitutes is low and new entrants face high barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dufry’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Airport landlord power

Airport authorities control scarce retail space via long-term concessions, allowing rents and revenue-share demands often in the 10–30% range (2024 industry reports) and strict assortment rules. Tender terms commonly mandate capex (often millions per major store), staffing and service KPIs, shifting costs to retailers. Location exclusivity is costly to win and easy to lose at renewal, raising fixed costs and reducing Dufry’s negotiation flexibility.

Concentrated global brands

In 2024 the beauty, spirits and tobacco categories remain concentrated in the hands of a few multinationals, giving suppliers strong bargaining power and control over margins, trade terms and marketing co‑funding. Iconic SKUs and travel exclusives are must‑have drivers of footfall and conversion, often non‑negotiable for retailers. Dufry offsets this pressure through scale buying, centralized category management and data‑sharing partnerships with brand owners.

Limited editions & exclusives

Travel-retail exclusives create strong differentiation but can lock Dufry into supplier programs that require guaranteed volumes or premium display fees; global travel-retail sales were about US$86bn in 2023, concentrating margin opportunity. Access to limited SKUs often needs volume commitments or slotting payments, concentrating sales on a narrow vendor set. Dependence rises when passenger mixes tilt toward whisky/perfume categories with high exclusivity.

Supply chain complexity

Global multi-node logistics to airports, cruise lines and borders markedly raises supplier leverage as Dufry relies on vendor reliability across complex routes; in 2024 Dufry operated roughly 2,200 shops in about 60 countries, amplifying logistics reach and dependency.

- Regulatory/customs/security reduce source substitutability

- Disruptions shift power to continuity-guaranteeing suppliers

- Dufry’s centralized procurement and inventory visibility mitigate risk

Compliance and regulation

Compliance and regulation constrain supplier options for Dufry: excise, labeling and product bans sharply limit alternative sourcing for alcohol and tobacco, forcing reliance on certified suppliers and regional allocations. Compliance costs and premarket approvals are often supplier‑driven, embedding brand standards into Dufry operations and shelf mixes. Sudden regulatory changes can rapidly alter assortments and margins, institutionalizing supplier influence across the value chain.

- Excise/labels limit sourcing

- Supplier‑led compliance embeds standards

- Regulatory shifts reshape assortments/margins

Suppliers drive high airport rents (10–30%) despite global scale and regulatory limits

Suppliers hold high leverage: airport concession rents (10–30% range, 2024) and category exclusives (beauty/spirits/tobacco concentrated) force trade terms, volume guarantees and display fees. Dufry’s scale (≈2,200 shops in ~60 countries, 2024) and centralized procurement mitigate but do not eliminate supplier power; regulatory constraints further reduce substitutability.

| Metric | Value |

|---|---|

| Shops | ≈2,200 (2024) |

| Countries | ≈60 (2024) |

| Travel‑retail sales | US$86bn (2023) |

| Rent/rev‑share | 10–30% (2024) |

What is included in the product

Tailored exclusively for Dufry, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary on how these forces shape pricing, profitability and market positioning.

A concise one-sheet Porter's Five Forces for Dufry that visualizes competitive pressure with a spider chart and customizable scores—ideal for quick board decisions or pitch decks. No complex tools required; swap in current data, duplicate scenarios and integrate into dashboards or Word reports.

Customers Bargaining Power

Captive traveler demand

Airside shoppers face limited alternatives, which reduces individual bargaining power and makes impulse purchases common; global air traffic in 2024 recovered to roughly 90–95% of 2019 levels, sustaining captive demand. Time pressure and convenience further tilt decisions toward on‑site purchase, raising conversion rates despite smaller basket negotiation. Airports and retailers often enforce price parity rules that cap ticket‑free premiums, keeping margins in check. Overall buyer power at point of sale is moderate.

Price transparency

Price transparency in 2024 intensified as mobile search and downtown comparisons let travelers benchmark duty‑free prices, increasing cross‑border visibility. Visible promotions across regions raised sensitivity to deal depth, while currency swings in 2024 amplified perceived value differences. This pressures Dufry to deploy dynamic pricing and targeted offers to protect margins and capture demand.

Loyalty and pre‑order

Dufry's CRM, memberships and click-and-collect raise switching costs by personalizing offers and locking loyalty; Dufry reported over 10 million loyalty members in 2024, boosting repeat purchase rates. Pre-order channels lock demand before travel day, reducing on-the-spot price sensitivity. These tools convert fragmented buyers into lower-elasticity repeat customers, so buyer power falls as engagement rises.

Passenger mix volatility

Passenger mix volatility shifts nationality, route and income bands, changing category demand and price elasticity; by 2024 many markets recovered to >90% of 2019 arrivals, amplifying volatility across corridors. Group tours and cruise cohorts (still ~pre-pandemic scale in 2024) negotiate bulk deals via intermediaries, while business vs leisure mix alters premium uptake; Dufry must adapt assortments to stabilize margins.

- Nationality shifts → category demand

- Route/income → price elasticity

- Group/cohort bargaining power

- Business vs leisure → premium sales

- Assortment agility required

Airline and tour intermediaries

Airline, OTA and cruise co-marketing bundles demand upstream, enabling partners to negotiate commissions and category exclusives that compress Dufry margins; OTAs account for over 50% of online travel bookings in 2024, amplifying their leverage.

These intermediaries drive high footfall but extract economics via fees and preferred placements, making intermediated buyer power materially stronger than that of individual travelers.

- Co-marketing scale: aggregates upstream demand

- Commission/exclusive leverage: reduces retailer margins

- 2024 OTA share: >50% online bookings

- Net effect: higher intermediated buyer power vs individual travelers

Airside shoppers captive as traffic nears 90–95% and OTAs squeeze margins

Airside shoppers remain relatively captive as 2024 air traffic recovered to ~90–95% of 2019, limiting individual bargaining power. Mobile price transparency and currency swings raise comparison pressure, while Dufry's >10m loyalty members and pre-order reduce elasticity. Intermediaries (OTAs >50% online bookings) exert stronger negotiated leverage, compressing retailer margins.

| Metric | 2024 |

|---|---|

| Air traffic vs 2019 | ~90–95% |

| Dufry loyalty members | >10 million |

| OTA share online bookings | >50% |

Preview Before You Purchase

Dufry Porter's Five Forces Analysis

This preview shows the exact Dufry Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the fully formatted, ready-to-use analysis covering supplier and buyer power, competitive rivalry, threats of new entrants and substitutes, and strategic implications. Once you buy, you'll have instant access to this identical document for download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Dufry faces intense competitive rivalry in travel retail, with location advantage but margin pressure from other retailers and online channels. Supplier power is moderate; buyer power fluctuates with travel volumes. Threat of substitutes is low and new entrants face high barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dufry’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Airport landlord power

Airport authorities control scarce retail space via long-term concessions, allowing rents and revenue-share demands often in the 10–30% range (2024 industry reports) and strict assortment rules. Tender terms commonly mandate capex (often millions per major store), staffing and service KPIs, shifting costs to retailers. Location exclusivity is costly to win and easy to lose at renewal, raising fixed costs and reducing Dufry’s negotiation flexibility.

Concentrated global brands

In 2024 the beauty, spirits and tobacco categories remain concentrated in the hands of a few multinationals, giving suppliers strong bargaining power and control over margins, trade terms and marketing co‑funding. Iconic SKUs and travel exclusives are must‑have drivers of footfall and conversion, often non‑negotiable for retailers. Dufry offsets this pressure through scale buying, centralized category management and data‑sharing partnerships with brand owners.

Limited editions & exclusives

Travel-retail exclusives create strong differentiation but can lock Dufry into supplier programs that require guaranteed volumes or premium display fees; global travel-retail sales were about US$86bn in 2023, concentrating margin opportunity. Access to limited SKUs often needs volume commitments or slotting payments, concentrating sales on a narrow vendor set. Dependence rises when passenger mixes tilt toward whisky/perfume categories with high exclusivity.

Supply chain complexity

Global multi-node logistics to airports, cruise lines and borders markedly raises supplier leverage as Dufry relies on vendor reliability across complex routes; in 2024 Dufry operated roughly 2,200 shops in about 60 countries, amplifying logistics reach and dependency.

- Regulatory/customs/security reduce source substitutability

- Disruptions shift power to continuity-guaranteeing suppliers

- Dufry’s centralized procurement and inventory visibility mitigate risk

Compliance and regulation

Compliance and regulation constrain supplier options for Dufry: excise, labeling and product bans sharply limit alternative sourcing for alcohol and tobacco, forcing reliance on certified suppliers and regional allocations. Compliance costs and premarket approvals are often supplier‑driven, embedding brand standards into Dufry operations and shelf mixes. Sudden regulatory changes can rapidly alter assortments and margins, institutionalizing supplier influence across the value chain.

- Excise/labels limit sourcing

- Supplier‑led compliance embeds standards

- Regulatory shifts reshape assortments/margins

Suppliers drive high airport rents (10–30%) despite global scale and regulatory limits

Suppliers hold high leverage: airport concession rents (10–30% range, 2024) and category exclusives (beauty/spirits/tobacco concentrated) force trade terms, volume guarantees and display fees. Dufry’s scale (≈2,200 shops in ~60 countries, 2024) and centralized procurement mitigate but do not eliminate supplier power; regulatory constraints further reduce substitutability.

| Metric | Value |

|---|---|

| Shops | ≈2,200 (2024) |

| Countries | ≈60 (2024) |

| Travel‑retail sales | US$86bn (2023) |

| Rent/rev‑share | 10–30% (2024) |

What is included in the product

Tailored exclusively for Dufry, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary on how these forces shape pricing, profitability and market positioning.

A concise one-sheet Porter's Five Forces for Dufry that visualizes competitive pressure with a spider chart and customizable scores—ideal for quick board decisions or pitch decks. No complex tools required; swap in current data, duplicate scenarios and integrate into dashboards or Word reports.

Customers Bargaining Power

Captive traveler demand

Airside shoppers face limited alternatives, which reduces individual bargaining power and makes impulse purchases common; global air traffic in 2024 recovered to roughly 90–95% of 2019 levels, sustaining captive demand. Time pressure and convenience further tilt decisions toward on‑site purchase, raising conversion rates despite smaller basket negotiation. Airports and retailers often enforce price parity rules that cap ticket‑free premiums, keeping margins in check. Overall buyer power at point of sale is moderate.

Price transparency

Price transparency in 2024 intensified as mobile search and downtown comparisons let travelers benchmark duty‑free prices, increasing cross‑border visibility. Visible promotions across regions raised sensitivity to deal depth, while currency swings in 2024 amplified perceived value differences. This pressures Dufry to deploy dynamic pricing and targeted offers to protect margins and capture demand.

Loyalty and pre‑order

Dufry's CRM, memberships and click-and-collect raise switching costs by personalizing offers and locking loyalty; Dufry reported over 10 million loyalty members in 2024, boosting repeat purchase rates. Pre-order channels lock demand before travel day, reducing on-the-spot price sensitivity. These tools convert fragmented buyers into lower-elasticity repeat customers, so buyer power falls as engagement rises.

Passenger mix volatility

Passenger mix volatility shifts nationality, route and income bands, changing category demand and price elasticity; by 2024 many markets recovered to >90% of 2019 arrivals, amplifying volatility across corridors. Group tours and cruise cohorts (still ~pre-pandemic scale in 2024) negotiate bulk deals via intermediaries, while business vs leisure mix alters premium uptake; Dufry must adapt assortments to stabilize margins.

- Nationality shifts → category demand

- Route/income → price elasticity

- Group/cohort bargaining power

- Business vs leisure → premium sales

- Assortment agility required

Airline and tour intermediaries

Airline, OTA and cruise co-marketing bundles demand upstream, enabling partners to negotiate commissions and category exclusives that compress Dufry margins; OTAs account for over 50% of online travel bookings in 2024, amplifying their leverage.

These intermediaries drive high footfall but extract economics via fees and preferred placements, making intermediated buyer power materially stronger than that of individual travelers.

- Co-marketing scale: aggregates upstream demand

- Commission/exclusive leverage: reduces retailer margins

- 2024 OTA share: >50% online bookings

- Net effect: higher intermediated buyer power vs individual travelers

Airside shoppers captive as traffic nears 90–95% and OTAs squeeze margins

Airside shoppers remain relatively captive as 2024 air traffic recovered to ~90–95% of 2019, limiting individual bargaining power. Mobile price transparency and currency swings raise comparison pressure, while Dufry's >10m loyalty members and pre-order reduce elasticity. Intermediaries (OTAs >50% online bookings) exert stronger negotiated leverage, compressing retailer margins.

| Metric | 2024 |

|---|---|

| Air traffic vs 2019 | ~90–95% |

| Dufry loyalty members | >10 million |

| OTA share online bookings | >50% |

Preview Before You Purchase

Dufry Porter's Five Forces Analysis

This preview shows the exact Dufry Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the fully formatted, ready-to-use analysis covering supplier and buyer power, competitive rivalry, threats of new entrants and substitutes, and strategic implications. Once you buy, you'll have instant access to this identical document for download and use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Dufry faces intense competitive rivalry in travel retail, with location advantage but margin pressure from other retailers and online channels. Supplier power is moderate; buyer power fluctuates with travel volumes. Threat of substitutes is low and new entrants face high barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dufry’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Airport landlord power

Airport authorities control scarce retail space via long-term concessions, allowing rents and revenue-share demands often in the 10–30% range (2024 industry reports) and strict assortment rules. Tender terms commonly mandate capex (often millions per major store), staffing and service KPIs, shifting costs to retailers. Location exclusivity is costly to win and easy to lose at renewal, raising fixed costs and reducing Dufry’s negotiation flexibility.

Concentrated global brands

In 2024 the beauty, spirits and tobacco categories remain concentrated in the hands of a few multinationals, giving suppliers strong bargaining power and control over margins, trade terms and marketing co‑funding. Iconic SKUs and travel exclusives are must‑have drivers of footfall and conversion, often non‑negotiable for retailers. Dufry offsets this pressure through scale buying, centralized category management and data‑sharing partnerships with brand owners.

Limited editions & exclusives

Travel-retail exclusives create strong differentiation but can lock Dufry into supplier programs that require guaranteed volumes or premium display fees; global travel-retail sales were about US$86bn in 2023, concentrating margin opportunity. Access to limited SKUs often needs volume commitments or slotting payments, concentrating sales on a narrow vendor set. Dependence rises when passenger mixes tilt toward whisky/perfume categories with high exclusivity.

Supply chain complexity

Global multi-node logistics to airports, cruise lines and borders markedly raises supplier leverage as Dufry relies on vendor reliability across complex routes; in 2024 Dufry operated roughly 2,200 shops in about 60 countries, amplifying logistics reach and dependency.

- Regulatory/customs/security reduce source substitutability

- Disruptions shift power to continuity-guaranteeing suppliers

- Dufry’s centralized procurement and inventory visibility mitigate risk

Compliance and regulation

Compliance and regulation constrain supplier options for Dufry: excise, labeling and product bans sharply limit alternative sourcing for alcohol and tobacco, forcing reliance on certified suppliers and regional allocations. Compliance costs and premarket approvals are often supplier‑driven, embedding brand standards into Dufry operations and shelf mixes. Sudden regulatory changes can rapidly alter assortments and margins, institutionalizing supplier influence across the value chain.

- Excise/labels limit sourcing

- Supplier‑led compliance embeds standards

- Regulatory shifts reshape assortments/margins

Suppliers drive high airport rents (10–30%) despite global scale and regulatory limits

Suppliers hold high leverage: airport concession rents (10–30% range, 2024) and category exclusives (beauty/spirits/tobacco concentrated) force trade terms, volume guarantees and display fees. Dufry’s scale (≈2,200 shops in ~60 countries, 2024) and centralized procurement mitigate but do not eliminate supplier power; regulatory constraints further reduce substitutability.

| Metric | Value |

|---|---|

| Shops | ≈2,200 (2024) |

| Countries | ≈60 (2024) |

| Travel‑retail sales | US$86bn (2023) |

| Rent/rev‑share | 10–30% (2024) |

What is included in the product

Tailored exclusively for Dufry, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary on how these forces shape pricing, profitability and market positioning.

A concise one-sheet Porter's Five Forces for Dufry that visualizes competitive pressure with a spider chart and customizable scores—ideal for quick board decisions or pitch decks. No complex tools required; swap in current data, duplicate scenarios and integrate into dashboards or Word reports.

Customers Bargaining Power

Captive traveler demand

Airside shoppers face limited alternatives, which reduces individual bargaining power and makes impulse purchases common; global air traffic in 2024 recovered to roughly 90–95% of 2019 levels, sustaining captive demand. Time pressure and convenience further tilt decisions toward on‑site purchase, raising conversion rates despite smaller basket negotiation. Airports and retailers often enforce price parity rules that cap ticket‑free premiums, keeping margins in check. Overall buyer power at point of sale is moderate.

Price transparency

Price transparency in 2024 intensified as mobile search and downtown comparisons let travelers benchmark duty‑free prices, increasing cross‑border visibility. Visible promotions across regions raised sensitivity to deal depth, while currency swings in 2024 amplified perceived value differences. This pressures Dufry to deploy dynamic pricing and targeted offers to protect margins and capture demand.

Loyalty and pre‑order

Dufry's CRM, memberships and click-and-collect raise switching costs by personalizing offers and locking loyalty; Dufry reported over 10 million loyalty members in 2024, boosting repeat purchase rates. Pre-order channels lock demand before travel day, reducing on-the-spot price sensitivity. These tools convert fragmented buyers into lower-elasticity repeat customers, so buyer power falls as engagement rises.

Passenger mix volatility

Passenger mix volatility shifts nationality, route and income bands, changing category demand and price elasticity; by 2024 many markets recovered to >90% of 2019 arrivals, amplifying volatility across corridors. Group tours and cruise cohorts (still ~pre-pandemic scale in 2024) negotiate bulk deals via intermediaries, while business vs leisure mix alters premium uptake; Dufry must adapt assortments to stabilize margins.

- Nationality shifts → category demand

- Route/income → price elasticity

- Group/cohort bargaining power

- Business vs leisure → premium sales

- Assortment agility required

Airline and tour intermediaries

Airline, OTA and cruise co-marketing bundles demand upstream, enabling partners to negotiate commissions and category exclusives that compress Dufry margins; OTAs account for over 50% of online travel bookings in 2024, amplifying their leverage.

These intermediaries drive high footfall but extract economics via fees and preferred placements, making intermediated buyer power materially stronger than that of individual travelers.

- Co-marketing scale: aggregates upstream demand

- Commission/exclusive leverage: reduces retailer margins

- 2024 OTA share: >50% online bookings

- Net effect: higher intermediated buyer power vs individual travelers

Airside shoppers captive as traffic nears 90–95% and OTAs squeeze margins

Airside shoppers remain relatively captive as 2024 air traffic recovered to ~90–95% of 2019, limiting individual bargaining power. Mobile price transparency and currency swings raise comparison pressure, while Dufry's >10m loyalty members and pre-order reduce elasticity. Intermediaries (OTAs >50% online bookings) exert stronger negotiated leverage, compressing retailer margins.

| Metric | 2024 |

|---|---|

| Air traffic vs 2019 | ~90–95% |

| Dufry loyalty members | >10 million |

| OTA share online bookings | >50% |

Preview Before You Purchase

Dufry Porter's Five Forces Analysis

This preview shows the exact Dufry Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the fully formatted, ready-to-use analysis covering supplier and buyer power, competitive rivalry, threats of new entrants and substitutes, and strategic implications. Once you buy, you'll have instant access to this identical document for download and use.