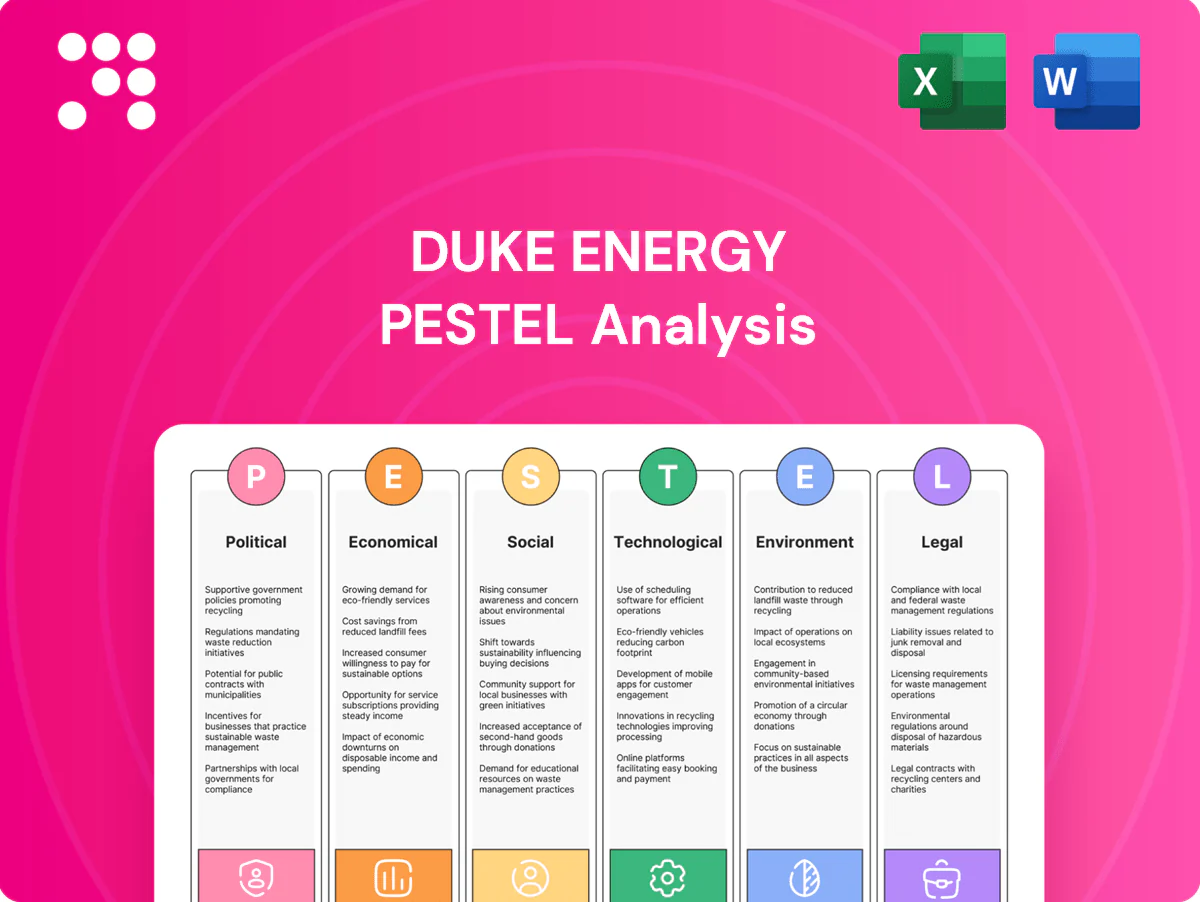

Duke Energy PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political regulation, economic cycles, social expectations, technological shifts, legal pressures, and environmental trends converge to shape Duke Energy’s strategic path. Our concise PESTLE pinpoints risks and opportunities—buy the full analysis for actionable insights and ready-to-use recommendations.

Political factors

State utility regulation

State utility commissions across the Southeast and Midwest set rates, approve investments and shape allowed returns; political shifts in state leadership can tilt priorities between affordability and decarbonization. Duke Energy’s multi‑year capital plan (about $55 billion for 2024–2028) hinges on timely regulatory approvals, with authorized ROEs in key jurisdictions typically around 9–11%, and constructive regulators aiding recovery of grid and generation spend.

Federal energy policy

FERC transmission planning and cost-allocation rules, notably FERC Order No. 1000 (2011), shape the feasibility of multi-billion-dollar regional grid projects affecting Duke Energy.

Federal incentives from the Inflation Reduction Act (2022) — including enhanced ITC/PTC and clean energy tax provisions — materially shift generation mix and customer program economics.

NERC reliability directives raise compliance and capital costs for grid hardening, and variability in federal policy stability directly affects Duke’s long-cycle investment decisions.

Local permitting and siting

County and municipal politics strongly shape siting for renewables, transmission and gas infrastructure for Duke Energy, which serves about 8 million customers across six states; coordinated approvals are critical to delivering the company’s roughly $23 billion grid investment plan (2023–2028). Community acceptance can expedite interconnection, while opposition commonly adds years to timelines and drives up costs. Partnering with local economic development agencies has unlocked tax and incentive packages on numerous projects, speeding deployment.

Energy security and resilience agenda

Policymakers have elevated grid resilience after extreme weather and cyber threats, pressuring utilities like Duke Energy, which serves about 8 million customers, to harden networks and speed restoration.

- Funding: federal programs since 2021 mobilized tens of billions for resilience

- Mandates: hardening, undergrounding, microgrids

- Cost recovery: political support enables rate mechanisms

- Performance: higher expectations for rapid restoration

Public funding and incentives

Grants and tax credits materially affect Duke Energy project economics for storage, solar and transmission; the Inflation Reduction Act includes a 30% investment tax credit and roughly 369 billion USD in energy/climate investments, shaping project returns. Accessing federal and state funds requires robust compliance and reporting capacity; incentives can lower customer rate impacts for large programs and changes in incentive structures shift capital allocation.

- IRA: 30% ITC; ~$369B energy investment

- Compliance/reporting needed to access funds

- Incentives reduce customer rate impacts

- Policy shifts reallocate capital

Regulatory politics and $55B capex reshape utility grid economics

State utility commissions (ROE ~9–11%) and local politics drive rate approval and siting for Duke Energy (≈8 million customers), underpinning its $55B 2024–2028 capital plan and $23B 2023–2028 grid spend. FERC rules (Order No.1000) and NERC mandates raise compliance and transmission costs. IRA incentives (30% ITC; ~$369B federal energy investment) materially improve project economics but require rigorous reporting.

| Item | Value |

|---|---|

| Customers | ≈8M |

| CapEx 2024–28 | $55B |

| Grid spend 2023–28 | $23B |

| ROE | 9–11% |

| IRA | 30% ITC; ~$369B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely shape Duke Energy’s strategic risks and opportunities, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it delivers actionable, forward-looking insights for scenario planning and funding decisions.

A concise, visually segmented Duke Energy PESTLE summary that relieves briefing pain points by distilling regulatory, market, environmental and technological risks into an easily shareable slide- or print-ready format for quick alignment in meetings and strategy sessions.

Economic factors

Interest rates and capital costs

As a capital-intensive utility, Duke Energy faces borrowing cost sensitivity: the 10-year US Treasury yield ~4.3% (mid-2025) and S&P A- rating underpin debt pricing. Higher market rates compress allowed returns and can push customer rates up, slowing investment pacing. Rate-case outcomes often lag market moves, creating regulatory timing risk. Treasury moves and utility credit spreads (~150–200 bps in 2024) shape financing strategy.

Regional load growth

Duke Energy's regional load growth is driven by population gains, industrial investment, data center expansion and rising EV adoption; the Southeast grew about 1.0% annually versus 0.4% nationally in 2023, supporting capacity additions across Duke's roughly 8 million retail customers. Data center deployments and a US plug‑in EV market share near 7% in 2024 are changing peak profiles with electrification. Accurate forecasts are critical for timely resource planning and avoided capacity shortfalls.

Fuel price volatility

Natural gas price swings (Henry Hub averaged roughly $3/MMBtu in 2024) directly raise Duke Energy’s generation costs and can push customer bills higher. Hedging programs and a diversified mix of gas, nuclear and renewables reduce earnings volatility and thermal fuel exposure. Ongoing coal retirements—about 5.6 GW planned by 2035—shift reliance toward gas and renewables. State fuel-cost recovery riders affect timing of cash flows for fuel expense.

Inflation and supply chain

Rising prices for transformers, conductors and labor are increasing Duke Energy’s grid capex, with transformer lead times extended to roughly 12–18 months and procurement risks delaying projects; US CPI averaged 3.4% in 2024, pressuring margins. Contract strategies and vendor diversification have become critical as regulatory rate adjustments often lag these cost increases.

- capex pressure: transformer/conductor/labor↑

- lead times: ~12–18 months

- mitigation: contract strategy & vendor diversification

- rate risk: CPI 3.4% (2024) vs lagging rate adjustments

Customer affordability and arrears

Customer affordability and arrears affect Duke Energy—economic cycles shift payment behavior and raise bad debt during downturns; serving about 8 million customers amplifies exposure. Affordability pressures (US CPI 2024: 3.4%) increase political scrutiny of rate hikes; targeted assistance and energy-efficiency programs can curb bills, while revenue stability depends on balanced rate design.

- Economic cycles → higher arrears/bad debt

- ~8 million customers → scale of impact

- US CPI 2024: 3.4% → affordability pressure

- Targeted programs + efficiency → bill moderation

- Balanced rate design → revenue stability

Regulatory politics and $55B capex reshape utility grid economics

Duke Energy is sensitive to borrowing costs (10-yr US Treasury ~4.3% mid-2025; S&P A-), compressing allowed returns and affecting rate timing. Regional load growth (Southeast ~1.0% in 2023) and ~8M customers drive capacity needs amid rising EV and data center demand. Fuel exposure: Henry Hub ~3/MMBtu in 2024; ~5.6 GW coal retirements by 2035 shift mix. CPI 3.4% (2024) and 12–18 month transformer lead times raise capex and timing risk.

| Metric | Value |

|---|---|

| 10-yr Treasury | ~4.3% (mid-2025) |

| Credit spread | ~150–200 bps (2024) |

| Customers | ~8M |

| Southeast growth | ~1.0% (2023) |

| Henry Hub | ~$3/MMBtu (2024) |

| CPI | 3.4% (2024) |

| Transformer lead time | 12–18 months |

| Coal retirements | ~5.6 GW by 2035 |

Preview Before You Purchase

Duke Energy PESTLE Analysis

The Duke Energy PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content, layout, and analysis shown here are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly get this same finished report. What you see is what you’ll own.

Your Competitive Advantage Starts with This Report

Discover how political regulation, economic cycles, social expectations, technological shifts, legal pressures, and environmental trends converge to shape Duke Energy’s strategic path. Our concise PESTLE pinpoints risks and opportunities—buy the full analysis for actionable insights and ready-to-use recommendations.

Political factors

State utility regulation

State utility commissions across the Southeast and Midwest set rates, approve investments and shape allowed returns; political shifts in state leadership can tilt priorities between affordability and decarbonization. Duke Energy’s multi‑year capital plan (about $55 billion for 2024–2028) hinges on timely regulatory approvals, with authorized ROEs in key jurisdictions typically around 9–11%, and constructive regulators aiding recovery of grid and generation spend.

Federal energy policy

FERC transmission planning and cost-allocation rules, notably FERC Order No. 1000 (2011), shape the feasibility of multi-billion-dollar regional grid projects affecting Duke Energy.

Federal incentives from the Inflation Reduction Act (2022) — including enhanced ITC/PTC and clean energy tax provisions — materially shift generation mix and customer program economics.

NERC reliability directives raise compliance and capital costs for grid hardening, and variability in federal policy stability directly affects Duke’s long-cycle investment decisions.

Local permitting and siting

County and municipal politics strongly shape siting for renewables, transmission and gas infrastructure for Duke Energy, which serves about 8 million customers across six states; coordinated approvals are critical to delivering the company’s roughly $23 billion grid investment plan (2023–2028). Community acceptance can expedite interconnection, while opposition commonly adds years to timelines and drives up costs. Partnering with local economic development agencies has unlocked tax and incentive packages on numerous projects, speeding deployment.

Energy security and resilience agenda

Policymakers have elevated grid resilience after extreme weather and cyber threats, pressuring utilities like Duke Energy, which serves about 8 million customers, to harden networks and speed restoration.

- Funding: federal programs since 2021 mobilized tens of billions for resilience

- Mandates: hardening, undergrounding, microgrids

- Cost recovery: political support enables rate mechanisms

- Performance: higher expectations for rapid restoration

Public funding and incentives

Grants and tax credits materially affect Duke Energy project economics for storage, solar and transmission; the Inflation Reduction Act includes a 30% investment tax credit and roughly 369 billion USD in energy/climate investments, shaping project returns. Accessing federal and state funds requires robust compliance and reporting capacity; incentives can lower customer rate impacts for large programs and changes in incentive structures shift capital allocation.

- IRA: 30% ITC; ~$369B energy investment

- Compliance/reporting needed to access funds

- Incentives reduce customer rate impacts

- Policy shifts reallocate capital

Regulatory politics and $55B capex reshape utility grid economics

State utility commissions (ROE ~9–11%) and local politics drive rate approval and siting for Duke Energy (≈8 million customers), underpinning its $55B 2024–2028 capital plan and $23B 2023–2028 grid spend. FERC rules (Order No.1000) and NERC mandates raise compliance and transmission costs. IRA incentives (30% ITC; ~$369B federal energy investment) materially improve project economics but require rigorous reporting.

| Item | Value |

|---|---|

| Customers | ≈8M |

| CapEx 2024–28 | $55B |

| Grid spend 2023–28 | $23B |

| ROE | 9–11% |

| IRA | 30% ITC; ~$369B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely shape Duke Energy’s strategic risks and opportunities, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it delivers actionable, forward-looking insights for scenario planning and funding decisions.

A concise, visually segmented Duke Energy PESTLE summary that relieves briefing pain points by distilling regulatory, market, environmental and technological risks into an easily shareable slide- or print-ready format for quick alignment in meetings and strategy sessions.

Economic factors

Interest rates and capital costs

As a capital-intensive utility, Duke Energy faces borrowing cost sensitivity: the 10-year US Treasury yield ~4.3% (mid-2025) and S&P A- rating underpin debt pricing. Higher market rates compress allowed returns and can push customer rates up, slowing investment pacing. Rate-case outcomes often lag market moves, creating regulatory timing risk. Treasury moves and utility credit spreads (~150–200 bps in 2024) shape financing strategy.

Regional load growth

Duke Energy's regional load growth is driven by population gains, industrial investment, data center expansion and rising EV adoption; the Southeast grew about 1.0% annually versus 0.4% nationally in 2023, supporting capacity additions across Duke's roughly 8 million retail customers. Data center deployments and a US plug‑in EV market share near 7% in 2024 are changing peak profiles with electrification. Accurate forecasts are critical for timely resource planning and avoided capacity shortfalls.

Fuel price volatility

Natural gas price swings (Henry Hub averaged roughly $3/MMBtu in 2024) directly raise Duke Energy’s generation costs and can push customer bills higher. Hedging programs and a diversified mix of gas, nuclear and renewables reduce earnings volatility and thermal fuel exposure. Ongoing coal retirements—about 5.6 GW planned by 2035—shift reliance toward gas and renewables. State fuel-cost recovery riders affect timing of cash flows for fuel expense.

Inflation and supply chain

Rising prices for transformers, conductors and labor are increasing Duke Energy’s grid capex, with transformer lead times extended to roughly 12–18 months and procurement risks delaying projects; US CPI averaged 3.4% in 2024, pressuring margins. Contract strategies and vendor diversification have become critical as regulatory rate adjustments often lag these cost increases.

- capex pressure: transformer/conductor/labor↑

- lead times: ~12–18 months

- mitigation: contract strategy & vendor diversification

- rate risk: CPI 3.4% (2024) vs lagging rate adjustments

Customer affordability and arrears

Customer affordability and arrears affect Duke Energy—economic cycles shift payment behavior and raise bad debt during downturns; serving about 8 million customers amplifies exposure. Affordability pressures (US CPI 2024: 3.4%) increase political scrutiny of rate hikes; targeted assistance and energy-efficiency programs can curb bills, while revenue stability depends on balanced rate design.

- Economic cycles → higher arrears/bad debt

- ~8 million customers → scale of impact

- US CPI 2024: 3.4% → affordability pressure

- Targeted programs + efficiency → bill moderation

- Balanced rate design → revenue stability

Regulatory politics and $55B capex reshape utility grid economics

Duke Energy is sensitive to borrowing costs (10-yr US Treasury ~4.3% mid-2025; S&P A-), compressing allowed returns and affecting rate timing. Regional load growth (Southeast ~1.0% in 2023) and ~8M customers drive capacity needs amid rising EV and data center demand. Fuel exposure: Henry Hub ~3/MMBtu in 2024; ~5.6 GW coal retirements by 2035 shift mix. CPI 3.4% (2024) and 12–18 month transformer lead times raise capex and timing risk.

| Metric | Value |

|---|---|

| 10-yr Treasury | ~4.3% (mid-2025) |

| Credit spread | ~150–200 bps (2024) |

| Customers | ~8M |

| Southeast growth | ~1.0% (2023) |

| Henry Hub | ~$3/MMBtu (2024) |

| CPI | 3.4% (2024) |

| Transformer lead time | 12–18 months |

| Coal retirements | ~5.6 GW by 2035 |

Preview Before You Purchase

Duke Energy PESTLE Analysis

The Duke Energy PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content, layout, and analysis shown here are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly get this same finished report. What you see is what you’ll own.

Description

Your Competitive Advantage Starts with This Report

Discover how political regulation, economic cycles, social expectations, technological shifts, legal pressures, and environmental trends converge to shape Duke Energy’s strategic path. Our concise PESTLE pinpoints risks and opportunities—buy the full analysis for actionable insights and ready-to-use recommendations.

Political factors

State utility regulation

State utility commissions across the Southeast and Midwest set rates, approve investments and shape allowed returns; political shifts in state leadership can tilt priorities between affordability and decarbonization. Duke Energy’s multi‑year capital plan (about $55 billion for 2024–2028) hinges on timely regulatory approvals, with authorized ROEs in key jurisdictions typically around 9–11%, and constructive regulators aiding recovery of grid and generation spend.

Federal energy policy

FERC transmission planning and cost-allocation rules, notably FERC Order No. 1000 (2011), shape the feasibility of multi-billion-dollar regional grid projects affecting Duke Energy.

Federal incentives from the Inflation Reduction Act (2022) — including enhanced ITC/PTC and clean energy tax provisions — materially shift generation mix and customer program economics.

NERC reliability directives raise compliance and capital costs for grid hardening, and variability in federal policy stability directly affects Duke’s long-cycle investment decisions.

Local permitting and siting

County and municipal politics strongly shape siting for renewables, transmission and gas infrastructure for Duke Energy, which serves about 8 million customers across six states; coordinated approvals are critical to delivering the company’s roughly $23 billion grid investment plan (2023–2028). Community acceptance can expedite interconnection, while opposition commonly adds years to timelines and drives up costs. Partnering with local economic development agencies has unlocked tax and incentive packages on numerous projects, speeding deployment.

Energy security and resilience agenda

Policymakers have elevated grid resilience after extreme weather and cyber threats, pressuring utilities like Duke Energy, which serves about 8 million customers, to harden networks and speed restoration.

- Funding: federal programs since 2021 mobilized tens of billions for resilience

- Mandates: hardening, undergrounding, microgrids

- Cost recovery: political support enables rate mechanisms

- Performance: higher expectations for rapid restoration

Public funding and incentives

Grants and tax credits materially affect Duke Energy project economics for storage, solar and transmission; the Inflation Reduction Act includes a 30% investment tax credit and roughly 369 billion USD in energy/climate investments, shaping project returns. Accessing federal and state funds requires robust compliance and reporting capacity; incentives can lower customer rate impacts for large programs and changes in incentive structures shift capital allocation.

- IRA: 30% ITC; ~$369B energy investment

- Compliance/reporting needed to access funds

- Incentives reduce customer rate impacts

- Policy shifts reallocate capital

Regulatory politics and $55B capex reshape utility grid economics

State utility commissions (ROE ~9–11%) and local politics drive rate approval and siting for Duke Energy (≈8 million customers), underpinning its $55B 2024–2028 capital plan and $23B 2023–2028 grid spend. FERC rules (Order No.1000) and NERC mandates raise compliance and transmission costs. IRA incentives (30% ITC; ~$369B federal energy investment) materially improve project economics but require rigorous reporting.

| Item | Value |

|---|---|

| Customers | ≈8M |

| CapEx 2024–28 | $55B |

| Grid spend 2023–28 | $23B |

| ROE | 9–11% |

| IRA | 30% ITC; ~$369B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely shape Duke Energy’s strategic risks and opportunities, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it delivers actionable, forward-looking insights for scenario planning and funding decisions.

A concise, visually segmented Duke Energy PESTLE summary that relieves briefing pain points by distilling regulatory, market, environmental and technological risks into an easily shareable slide- or print-ready format for quick alignment in meetings and strategy sessions.

Economic factors

Interest rates and capital costs

As a capital-intensive utility, Duke Energy faces borrowing cost sensitivity: the 10-year US Treasury yield ~4.3% (mid-2025) and S&P A- rating underpin debt pricing. Higher market rates compress allowed returns and can push customer rates up, slowing investment pacing. Rate-case outcomes often lag market moves, creating regulatory timing risk. Treasury moves and utility credit spreads (~150–200 bps in 2024) shape financing strategy.

Regional load growth

Duke Energy's regional load growth is driven by population gains, industrial investment, data center expansion and rising EV adoption; the Southeast grew about 1.0% annually versus 0.4% nationally in 2023, supporting capacity additions across Duke's roughly 8 million retail customers. Data center deployments and a US plug‑in EV market share near 7% in 2024 are changing peak profiles with electrification. Accurate forecasts are critical for timely resource planning and avoided capacity shortfalls.

Fuel price volatility

Natural gas price swings (Henry Hub averaged roughly $3/MMBtu in 2024) directly raise Duke Energy’s generation costs and can push customer bills higher. Hedging programs and a diversified mix of gas, nuclear and renewables reduce earnings volatility and thermal fuel exposure. Ongoing coal retirements—about 5.6 GW planned by 2035—shift reliance toward gas and renewables. State fuel-cost recovery riders affect timing of cash flows for fuel expense.

Inflation and supply chain

Rising prices for transformers, conductors and labor are increasing Duke Energy’s grid capex, with transformer lead times extended to roughly 12–18 months and procurement risks delaying projects; US CPI averaged 3.4% in 2024, pressuring margins. Contract strategies and vendor diversification have become critical as regulatory rate adjustments often lag these cost increases.

- capex pressure: transformer/conductor/labor↑

- lead times: ~12–18 months

- mitigation: contract strategy & vendor diversification

- rate risk: CPI 3.4% (2024) vs lagging rate adjustments

Customer affordability and arrears

Customer affordability and arrears affect Duke Energy—economic cycles shift payment behavior and raise bad debt during downturns; serving about 8 million customers amplifies exposure. Affordability pressures (US CPI 2024: 3.4%) increase political scrutiny of rate hikes; targeted assistance and energy-efficiency programs can curb bills, while revenue stability depends on balanced rate design.

- Economic cycles → higher arrears/bad debt

- ~8 million customers → scale of impact

- US CPI 2024: 3.4% → affordability pressure

- Targeted programs + efficiency → bill moderation

- Balanced rate design → revenue stability

Regulatory politics and $55B capex reshape utility grid economics

Duke Energy is sensitive to borrowing costs (10-yr US Treasury ~4.3% mid-2025; S&P A-), compressing allowed returns and affecting rate timing. Regional load growth (Southeast ~1.0% in 2023) and ~8M customers drive capacity needs amid rising EV and data center demand. Fuel exposure: Henry Hub ~3/MMBtu in 2024; ~5.6 GW coal retirements by 2035 shift mix. CPI 3.4% (2024) and 12–18 month transformer lead times raise capex and timing risk.

| Metric | Value |

|---|---|

| 10-yr Treasury | ~4.3% (mid-2025) |

| Credit spread | ~150–200 bps (2024) |

| Customers | ~8M |

| Southeast growth | ~1.0% (2023) |

| Henry Hub | ~$3/MMBtu (2024) |

| CPI | 3.4% (2024) |

| Transformer lead time | 12–18 months |

| Coal retirements | ~5.6 GW by 2035 |

Preview Before You Purchase

Duke Energy PESTLE Analysis

The Duke Energy PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content, layout, and analysis shown here are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly get this same finished report. What you see is what you’ll own.