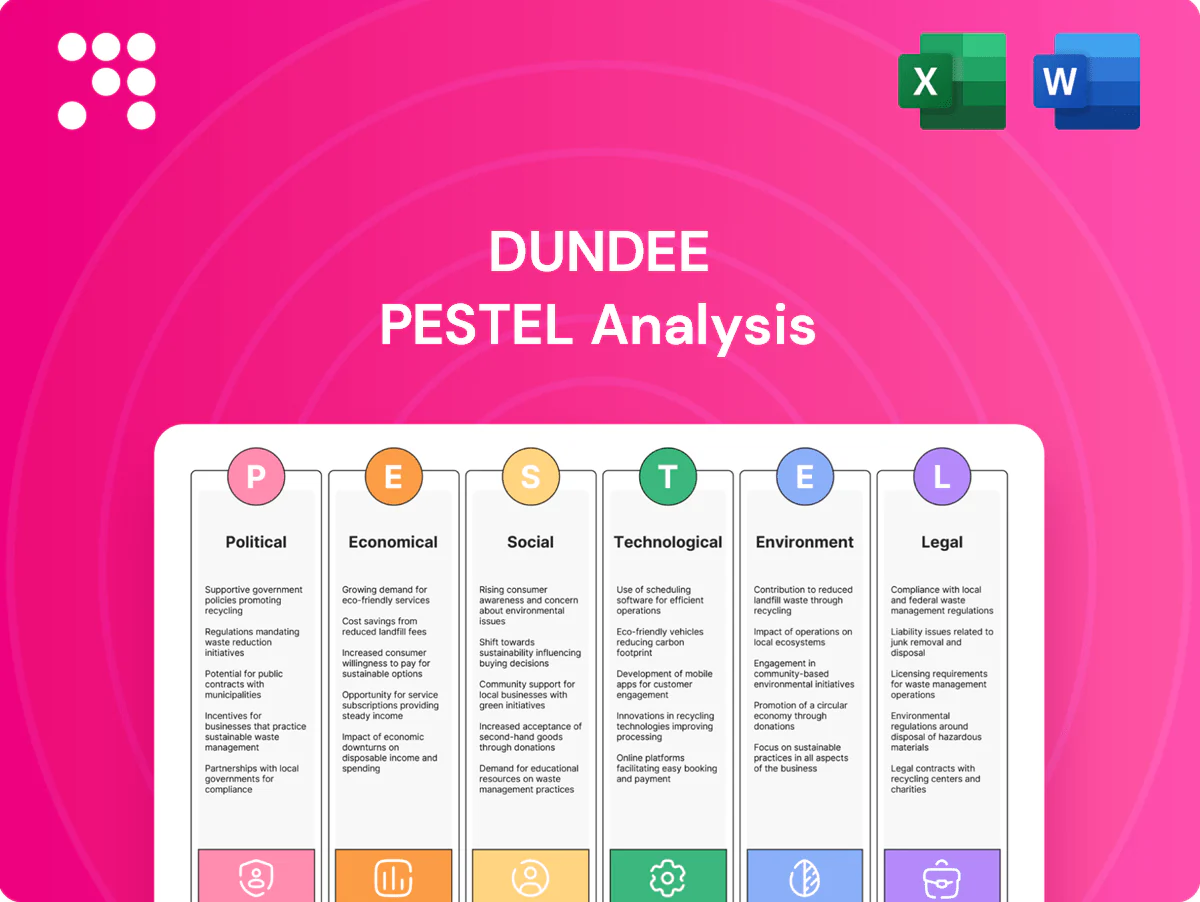

Dundee PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of Dundee—three to five clear insights into political, economic, social, technological, legal and environmental forces shaping its outlook. Perfect for investors and strategists, this ready-made report is fully editable and boardroom-ready. Purchase the full version now for the deep-dive intelligence that powers confident decisions.

Political factors

Host-country stability

Operations span Bulgaria (EU member, population ~6.5 million in 2024), Namibia (stable democracy, population ~2.6 million in 2024) and Serbia (EU candidate, population ~6.6 million in 2024), each with distinct political dynamics. Policy continuity in these jurisdictions generally supports mining, though cabinet changes can slow permitting and approvals. Dundee should maintain multi-level government engagement to manage transitions; country risk diversification buffers isolated disruptions.

Permitting and local governance

Permitting timelines are decisive for project schedules in Dundee, a city of 148,270 residents (Census 2021) governed by 29 councillors; delays can cascade into cost overruns. Early alignment with Tay Cities regional development plans reduces statutory hold-ups. Transparent disclosure and community consultations build goodwill with local councils. Dedicated permitting roadmaps mitigate administrative bottlenecks.

Resource nationalism risk

Royalty, export and windfall tax revisions remain cyclical political levers; EY 2024 recorded 28 jurisdictions revising mining/energy fiscal terms in 2023–24. Contract sanctity is usually respected, yet review clauses reopened terms during the 2022–23 commodity peak. Scenario modelling of +/-5–15 ppt fiscal take typically alters project NPV by roughly 5–30%. Proactive national value‑add (local processing, jobs) cuts targeting risk.

EU policy influence

Bulgaria’s adoption of EU frameworks drives stricter environmental, safety and public procurement standards that directly affect Dundee’s operations; Bulgaria’s 2021–2027 EU allocation of about €12.2bn supports infrastructure and energy projects that can improve mine logistics. Serbia’s EU alignment pathway implies progressively tighter requirements. Compliance with the EU taxonomy improves investor access and green financing.

- Bulgaria EU funds ~€12.2bn (2021–2027)

- EU 2021–27 budget €1.074tn

- Serbia accession alignment increases regulatory stringency

- Taxonomy compliance aids green capital access

Geopolitics and energy security

Regional energy policy and cross-border supply chains materially affect Dundee’s power reliability and costs; the UK imported roughly 40% of its natural gas in 2023, amplifying price exposure. Diversifying suppliers and fuel sources cuts shock risk, while government renewables support helped achieve 43% renewable electricity in 2023, de-risking long-term contracts. Crisis protocols preserve continuity during geopolitical tensions.

- Import exposure ~40% (gas, 2023)

- Renewables 43% of UK power (2023)

- Diversify suppliers/fuels to reduce shocks

- Use gov incentives to lower contract risk

Permitting, fiscal shifts and energy exposure reshape Bulgaria, Namibia, Serbia and Dundee risk

Operations across Bulgaria (pop ~6.5m 2024), Namibia (2.6m) and Serbia (6.6m) face differing permitting, fiscal and EU-alignment risks; Dundee city pop 148,270 affects local approvals. Fiscal revisions are active — EY found 28 jurisdictions revised mining fiscal terms 2023–24 — and +/-5–15ppt take shifts NPV 5–30%. Energy import exposure (~40% gas 2023) and EU funds (€12.2bn BG 2021–27) shape logistics and financing.

| Metric | Value |

|---|---|

| Bulgaria pop (2024) | ~6.5m |

| Serbia pop (2024) | ~6.6m |

| Namibia pop (2024) | ~2.6m |

| Dundee pop | 148,270 (Census 2021) |

| EU funds Bulgaria | €12.2bn (2021–27) |

| Jurisdictions revising fiscal terms | 28 (2023–24) |

| UK gas import | ~40% (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Dundee across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends. Designed for executives, consultants, and entrepreneurs, the analysis offers forward-looking insights and specific sub-points ready for business plans, pitch decks, or scenario planning.

A concise, visually segmented Dundee PESTLE summary for quick reference in meetings or presentations, with editable notes to localize insights and a slide-ready format for fast alignment across teams and departments.

Economic factors

Gold price sensitivity

Revenue is tightly linked to USD gold (spot ~2,300/oz July 2025) and investor risk sentiment, so topline swings with metal moves. Hedging policies must balance downside protection with upside optionality through collars and forwards. Project sequencing should prioritize high-margin, low-cost ounces to withstand lower price decks. Rigorous cost discipline preserves margins across price cycles.

FX and inflation

Costs in BGN, NAD and RSD vs USD revenues create material basis risk; BGN is effectively pegged to EUR at 1.95583, while NAD and RSD showed CPI of about 6.2% and 7.5% yoy (June 2025), amplifying local currency cost growth against USD receipts.

Local inflation in energy and consumables pushes AISC higher; natural hedges via local procurement reduced FX pass-through by an estimated 20-30% in 2024.

Selective FX hedging of net exposure and index-linked supply contracts (energy and reagents) can stabilize input costs and protect margins.

Capital access and cost

Interest-rate cycles and credit-spread volatility pushed average policy rates in major markets to around 4.5% in 2024, lifting corporate financing costs and bank margins. Maintaining investment-grade ESG credentials widens lender pools and correlates with ~20–40 basis points lower spreads in empirical studies. A balanced mix of cash flow, revolvers and offtake prepayments can shave 50–120 bps off WACC. Consistent, transparent guidance sustains market confidence and tighter funding terms.

Supply chain and inputs

Reagents, explosives and critical spares faced pronounced pricing and logistics volatility in 2024, driven by tight chemical markets and intermittent port congestion; multi-sourcing and regional inventories reduced delivery lead times and stockout risk. Long-term vendor partnerships secured better terms and priority allocations, while local content strategies materially lowered landed costs and import exposure.

- Multi-sourcing: reduces single-vendor risk

- Regional inventory: shortens lead times

- Vendor partnerships: improve availability/terms

- Local content: lowers landed cost

Local economic impact

Employment, training and SME development in Dundee generate multiplier effects for the city (population 148,270 per Census 2021), raising incomes and local consumption, while stable operations bolster council revenues and service delivery; demonstrable shared value helps secure operating continuity and community licence to operate, and supplier development programs deepen supply-chain resilience.

- Employment multiplier: local jobs sustain consumption

- Training → SME growth and resilience

- Stable firms support municipal revenue

- Supplier development reduces disruption risk

Permitting, fiscal shifts and energy exposure reshape Bulgaria, Namibia, Serbia and Dundee risk

Revenue tracks USD gold (~2,300/oz July 2025) and risk sentiment, so topline volatility requires collars/forwards and prioritizing high-margin ounces. Local CPI (NAD 6.2% Jun 2025, RSD 7.5%) and BGN peg to EUR raise FX basis risk versus USD receipts. Policy rates ~4.5% (2024) lift funding costs; ESG and blended financing can reduce spreads ~20–120bps.

| Metric | Value |

|---|---|

| Gold (USD/oz) | ~2,300 (Jul 2025) |

| NAD CPI Jun 2025 | 6.2% |

| RSD CPI Jun 2025 | 7.5% |

| Policy rates | ~4.5% (2024) |

Same Document Delivered

Dundee PESTLE Analysis

The Dundee PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment specific to Dundee with no placeholders. The file you see is the final, downloadable version delivered immediately upon checkout.

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of Dundee—three to five clear insights into political, economic, social, technological, legal and environmental forces shaping its outlook. Perfect for investors and strategists, this ready-made report is fully editable and boardroom-ready. Purchase the full version now for the deep-dive intelligence that powers confident decisions.

Political factors

Host-country stability

Operations span Bulgaria (EU member, population ~6.5 million in 2024), Namibia (stable democracy, population ~2.6 million in 2024) and Serbia (EU candidate, population ~6.6 million in 2024), each with distinct political dynamics. Policy continuity in these jurisdictions generally supports mining, though cabinet changes can slow permitting and approvals. Dundee should maintain multi-level government engagement to manage transitions; country risk diversification buffers isolated disruptions.

Permitting and local governance

Permitting timelines are decisive for project schedules in Dundee, a city of 148,270 residents (Census 2021) governed by 29 councillors; delays can cascade into cost overruns. Early alignment with Tay Cities regional development plans reduces statutory hold-ups. Transparent disclosure and community consultations build goodwill with local councils. Dedicated permitting roadmaps mitigate administrative bottlenecks.

Resource nationalism risk

Royalty, export and windfall tax revisions remain cyclical political levers; EY 2024 recorded 28 jurisdictions revising mining/energy fiscal terms in 2023–24. Contract sanctity is usually respected, yet review clauses reopened terms during the 2022–23 commodity peak. Scenario modelling of +/-5–15 ppt fiscal take typically alters project NPV by roughly 5–30%. Proactive national value‑add (local processing, jobs) cuts targeting risk.

EU policy influence

Bulgaria’s adoption of EU frameworks drives stricter environmental, safety and public procurement standards that directly affect Dundee’s operations; Bulgaria’s 2021–2027 EU allocation of about €12.2bn supports infrastructure and energy projects that can improve mine logistics. Serbia’s EU alignment pathway implies progressively tighter requirements. Compliance with the EU taxonomy improves investor access and green financing.

- Bulgaria EU funds ~€12.2bn (2021–2027)

- EU 2021–27 budget €1.074tn

- Serbia accession alignment increases regulatory stringency

- Taxonomy compliance aids green capital access

Geopolitics and energy security

Regional energy policy and cross-border supply chains materially affect Dundee’s power reliability and costs; the UK imported roughly 40% of its natural gas in 2023, amplifying price exposure. Diversifying suppliers and fuel sources cuts shock risk, while government renewables support helped achieve 43% renewable electricity in 2023, de-risking long-term contracts. Crisis protocols preserve continuity during geopolitical tensions.

- Import exposure ~40% (gas, 2023)

- Renewables 43% of UK power (2023)

- Diversify suppliers/fuels to reduce shocks

- Use gov incentives to lower contract risk

Permitting, fiscal shifts and energy exposure reshape Bulgaria, Namibia, Serbia and Dundee risk

Operations across Bulgaria (pop ~6.5m 2024), Namibia (2.6m) and Serbia (6.6m) face differing permitting, fiscal and EU-alignment risks; Dundee city pop 148,270 affects local approvals. Fiscal revisions are active — EY found 28 jurisdictions revised mining fiscal terms 2023–24 — and +/-5–15ppt take shifts NPV 5–30%. Energy import exposure (~40% gas 2023) and EU funds (€12.2bn BG 2021–27) shape logistics and financing.

| Metric | Value |

|---|---|

| Bulgaria pop (2024) | ~6.5m |

| Serbia pop (2024) | ~6.6m |

| Namibia pop (2024) | ~2.6m |

| Dundee pop | 148,270 (Census 2021) |

| EU funds Bulgaria | €12.2bn (2021–27) |

| Jurisdictions revising fiscal terms | 28 (2023–24) |

| UK gas import | ~40% (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Dundee across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends. Designed for executives, consultants, and entrepreneurs, the analysis offers forward-looking insights and specific sub-points ready for business plans, pitch decks, or scenario planning.

A concise, visually segmented Dundee PESTLE summary for quick reference in meetings or presentations, with editable notes to localize insights and a slide-ready format for fast alignment across teams and departments.

Economic factors

Gold price sensitivity

Revenue is tightly linked to USD gold (spot ~2,300/oz July 2025) and investor risk sentiment, so topline swings with metal moves. Hedging policies must balance downside protection with upside optionality through collars and forwards. Project sequencing should prioritize high-margin, low-cost ounces to withstand lower price decks. Rigorous cost discipline preserves margins across price cycles.

FX and inflation

Costs in BGN, NAD and RSD vs USD revenues create material basis risk; BGN is effectively pegged to EUR at 1.95583, while NAD and RSD showed CPI of about 6.2% and 7.5% yoy (June 2025), amplifying local currency cost growth against USD receipts.

Local inflation in energy and consumables pushes AISC higher; natural hedges via local procurement reduced FX pass-through by an estimated 20-30% in 2024.

Selective FX hedging of net exposure and index-linked supply contracts (energy and reagents) can stabilize input costs and protect margins.

Capital access and cost

Interest-rate cycles and credit-spread volatility pushed average policy rates in major markets to around 4.5% in 2024, lifting corporate financing costs and bank margins. Maintaining investment-grade ESG credentials widens lender pools and correlates with ~20–40 basis points lower spreads in empirical studies. A balanced mix of cash flow, revolvers and offtake prepayments can shave 50–120 bps off WACC. Consistent, transparent guidance sustains market confidence and tighter funding terms.

Supply chain and inputs

Reagents, explosives and critical spares faced pronounced pricing and logistics volatility in 2024, driven by tight chemical markets and intermittent port congestion; multi-sourcing and regional inventories reduced delivery lead times and stockout risk. Long-term vendor partnerships secured better terms and priority allocations, while local content strategies materially lowered landed costs and import exposure.

- Multi-sourcing: reduces single-vendor risk

- Regional inventory: shortens lead times

- Vendor partnerships: improve availability/terms

- Local content: lowers landed cost

Local economic impact

Employment, training and SME development in Dundee generate multiplier effects for the city (population 148,270 per Census 2021), raising incomes and local consumption, while stable operations bolster council revenues and service delivery; demonstrable shared value helps secure operating continuity and community licence to operate, and supplier development programs deepen supply-chain resilience.

- Employment multiplier: local jobs sustain consumption

- Training → SME growth and resilience

- Stable firms support municipal revenue

- Supplier development reduces disruption risk

Permitting, fiscal shifts and energy exposure reshape Bulgaria, Namibia, Serbia and Dundee risk

Revenue tracks USD gold (~2,300/oz July 2025) and risk sentiment, so topline volatility requires collars/forwards and prioritizing high-margin ounces. Local CPI (NAD 6.2% Jun 2025, RSD 7.5%) and BGN peg to EUR raise FX basis risk versus USD receipts. Policy rates ~4.5% (2024) lift funding costs; ESG and blended financing can reduce spreads ~20–120bps.

| Metric | Value |

|---|---|

| Gold (USD/oz) | ~2,300 (Jul 2025) |

| NAD CPI Jun 2025 | 6.2% |

| RSD CPI Jun 2025 | 7.5% |

| Policy rates | ~4.5% (2024) |

Same Document Delivered

Dundee PESTLE Analysis

The Dundee PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment specific to Dundee with no placeholders. The file you see is the final, downloadable version delivered immediately upon checkout.

Description

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of Dundee—three to five clear insights into political, economic, social, technological, legal and environmental forces shaping its outlook. Perfect for investors and strategists, this ready-made report is fully editable and boardroom-ready. Purchase the full version now for the deep-dive intelligence that powers confident decisions.

Political factors

Host-country stability

Operations span Bulgaria (EU member, population ~6.5 million in 2024), Namibia (stable democracy, population ~2.6 million in 2024) and Serbia (EU candidate, population ~6.6 million in 2024), each with distinct political dynamics. Policy continuity in these jurisdictions generally supports mining, though cabinet changes can slow permitting and approvals. Dundee should maintain multi-level government engagement to manage transitions; country risk diversification buffers isolated disruptions.

Permitting and local governance

Permitting timelines are decisive for project schedules in Dundee, a city of 148,270 residents (Census 2021) governed by 29 councillors; delays can cascade into cost overruns. Early alignment with Tay Cities regional development plans reduces statutory hold-ups. Transparent disclosure and community consultations build goodwill with local councils. Dedicated permitting roadmaps mitigate administrative bottlenecks.

Resource nationalism risk

Royalty, export and windfall tax revisions remain cyclical political levers; EY 2024 recorded 28 jurisdictions revising mining/energy fiscal terms in 2023–24. Contract sanctity is usually respected, yet review clauses reopened terms during the 2022–23 commodity peak. Scenario modelling of +/-5–15 ppt fiscal take typically alters project NPV by roughly 5–30%. Proactive national value‑add (local processing, jobs) cuts targeting risk.

EU policy influence

Bulgaria’s adoption of EU frameworks drives stricter environmental, safety and public procurement standards that directly affect Dundee’s operations; Bulgaria’s 2021–2027 EU allocation of about €12.2bn supports infrastructure and energy projects that can improve mine logistics. Serbia’s EU alignment pathway implies progressively tighter requirements. Compliance with the EU taxonomy improves investor access and green financing.

- Bulgaria EU funds ~€12.2bn (2021–2027)

- EU 2021–27 budget €1.074tn

- Serbia accession alignment increases regulatory stringency

- Taxonomy compliance aids green capital access

Geopolitics and energy security

Regional energy policy and cross-border supply chains materially affect Dundee’s power reliability and costs; the UK imported roughly 40% of its natural gas in 2023, amplifying price exposure. Diversifying suppliers and fuel sources cuts shock risk, while government renewables support helped achieve 43% renewable electricity in 2023, de-risking long-term contracts. Crisis protocols preserve continuity during geopolitical tensions.

- Import exposure ~40% (gas, 2023)

- Renewables 43% of UK power (2023)

- Diversify suppliers/fuels to reduce shocks

- Use gov incentives to lower contract risk

Permitting, fiscal shifts and energy exposure reshape Bulgaria, Namibia, Serbia and Dundee risk

Operations across Bulgaria (pop ~6.5m 2024), Namibia (2.6m) and Serbia (6.6m) face differing permitting, fiscal and EU-alignment risks; Dundee city pop 148,270 affects local approvals. Fiscal revisions are active — EY found 28 jurisdictions revised mining fiscal terms 2023–24 — and +/-5–15ppt take shifts NPV 5–30%. Energy import exposure (~40% gas 2023) and EU funds (€12.2bn BG 2021–27) shape logistics and financing.

| Metric | Value |

|---|---|

| Bulgaria pop (2024) | ~6.5m |

| Serbia pop (2024) | ~6.6m |

| Namibia pop (2024) | ~2.6m |

| Dundee pop | 148,270 (Census 2021) |

| EU funds Bulgaria | €12.2bn (2021–27) |

| Jurisdictions revising fiscal terms | 28 (2023–24) |

| UK gas import | ~40% (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Dundee across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends. Designed for executives, consultants, and entrepreneurs, the analysis offers forward-looking insights and specific sub-points ready for business plans, pitch decks, or scenario planning.

A concise, visually segmented Dundee PESTLE summary for quick reference in meetings or presentations, with editable notes to localize insights and a slide-ready format for fast alignment across teams and departments.

Economic factors

Gold price sensitivity

Revenue is tightly linked to USD gold (spot ~2,300/oz July 2025) and investor risk sentiment, so topline swings with metal moves. Hedging policies must balance downside protection with upside optionality through collars and forwards. Project sequencing should prioritize high-margin, low-cost ounces to withstand lower price decks. Rigorous cost discipline preserves margins across price cycles.

FX and inflation

Costs in BGN, NAD and RSD vs USD revenues create material basis risk; BGN is effectively pegged to EUR at 1.95583, while NAD and RSD showed CPI of about 6.2% and 7.5% yoy (June 2025), amplifying local currency cost growth against USD receipts.

Local inflation in energy and consumables pushes AISC higher; natural hedges via local procurement reduced FX pass-through by an estimated 20-30% in 2024.

Selective FX hedging of net exposure and index-linked supply contracts (energy and reagents) can stabilize input costs and protect margins.

Capital access and cost

Interest-rate cycles and credit-spread volatility pushed average policy rates in major markets to around 4.5% in 2024, lifting corporate financing costs and bank margins. Maintaining investment-grade ESG credentials widens lender pools and correlates with ~20–40 basis points lower spreads in empirical studies. A balanced mix of cash flow, revolvers and offtake prepayments can shave 50–120 bps off WACC. Consistent, transparent guidance sustains market confidence and tighter funding terms.

Supply chain and inputs

Reagents, explosives and critical spares faced pronounced pricing and logistics volatility in 2024, driven by tight chemical markets and intermittent port congestion; multi-sourcing and regional inventories reduced delivery lead times and stockout risk. Long-term vendor partnerships secured better terms and priority allocations, while local content strategies materially lowered landed costs and import exposure.

- Multi-sourcing: reduces single-vendor risk

- Regional inventory: shortens lead times

- Vendor partnerships: improve availability/terms

- Local content: lowers landed cost

Local economic impact

Employment, training and SME development in Dundee generate multiplier effects for the city (population 148,270 per Census 2021), raising incomes and local consumption, while stable operations bolster council revenues and service delivery; demonstrable shared value helps secure operating continuity and community licence to operate, and supplier development programs deepen supply-chain resilience.

- Employment multiplier: local jobs sustain consumption

- Training → SME growth and resilience

- Stable firms support municipal revenue

- Supplier development reduces disruption risk

Permitting, fiscal shifts and energy exposure reshape Bulgaria, Namibia, Serbia and Dundee risk

Revenue tracks USD gold (~2,300/oz July 2025) and risk sentiment, so topline volatility requires collars/forwards and prioritizing high-margin ounces. Local CPI (NAD 6.2% Jun 2025, RSD 7.5%) and BGN peg to EUR raise FX basis risk versus USD receipts. Policy rates ~4.5% (2024) lift funding costs; ESG and blended financing can reduce spreads ~20–120bps.

| Metric | Value |

|---|---|

| Gold (USD/oz) | ~2,300 (Jul 2025) |

| NAD CPI Jun 2025 | 6.2% |

| RSD CPI Jun 2025 | 7.5% |

| Policy rates | ~4.5% (2024) |

Same Document Delivered

Dundee PESTLE Analysis

The Dundee PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment specific to Dundee with no placeholders. The file you see is the final, downloadable version delivered immediately upon checkout.