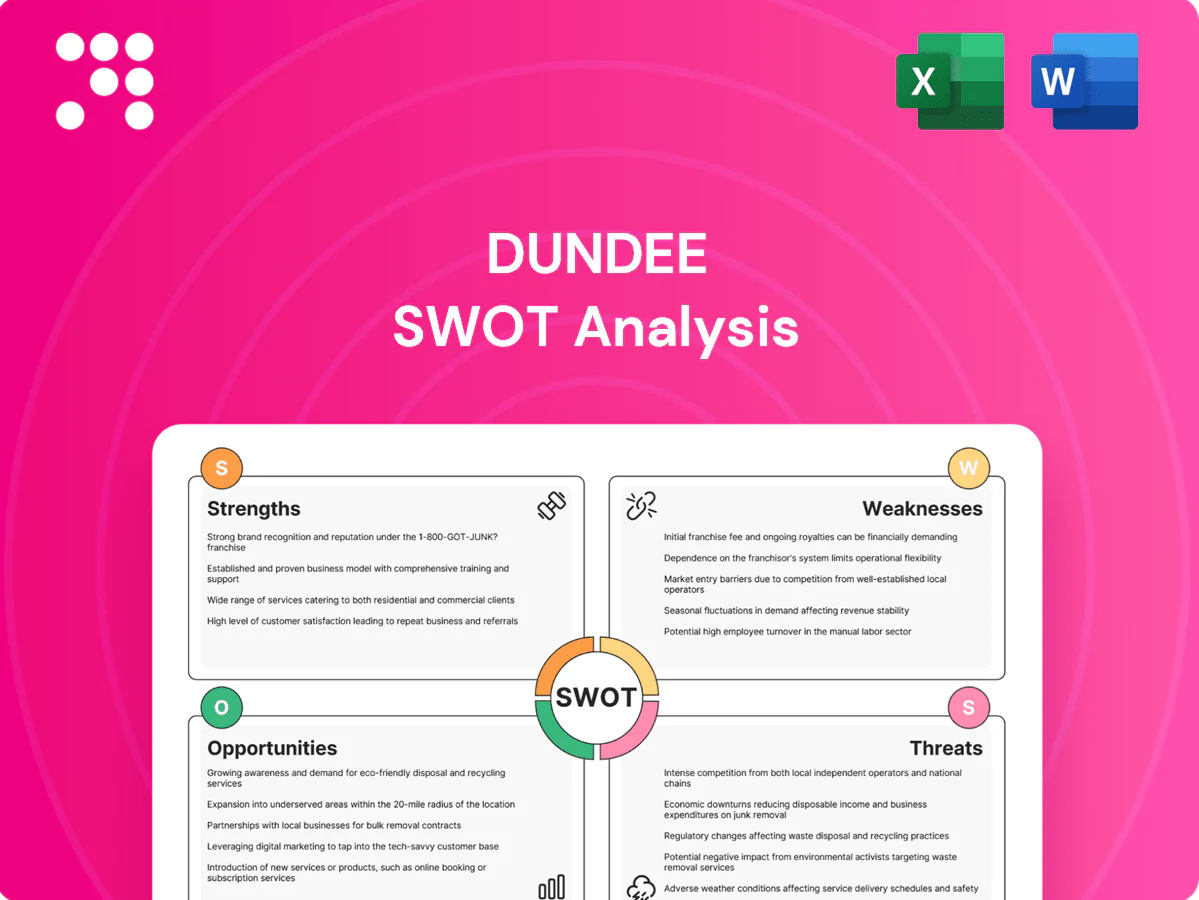

Dundee SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Our Dundee SWOT Analysis highlights the firm's core strengths, competitive risks, and untapped growth avenues in concise, evidence-backed terms. Explore strategic implications for investors and managers. Purchase the full SWOT to access a detailed, editable report and Excel tools. Make data-driven decisions with confidence.

Strengths

Diversified operating footprint

Operations across Bulgaria, Namibia and Serbia create a three-country footprint that reduces single-country risk and broadens market exposure.

Exposure to multiple regulatory and fiscal regimes smooths operational disruptions and tax variability across these three jurisdictions.

Regional diversification widens access to talent and suppliers and allows redeployment of capital among the three operations as conditions change.

End-to-end precious metals capabilities

Spanning acquisition, exploration, development, mining and processing, Dundee captures value across the full precious‑metals chain, lowering unit costs and improving recoveries through process integration. Integrated operations accelerate project timelines and embed technical know‑how and execution discipline across sites. This breadth supports steady pipeline renewal and enhances cash‑flow durability.

Strong ESG and responsible mining focus

Dundee's stated commitment to sustainable practices supports permitting, community relations and long-term license to operate, reducing risk of project delays. Robust ESG performance lowers operational interruptions and regulatory friction, helping maintain steady production. Transparent stewardship can broaden investor access and potentially lower cost of capital while enhancing brand and stakeholder trust.

Operational experience in Europe and Africa

Operational experience in Europe and Africa, notably Bulgaria and Namibia, strengthens local knowledge, enabling agility and tighter cost control. Familiarity with regional infrastructure and supply chains supports consistent production and logistics. Established community relationships reduce social risk and ease permitting, and this operational base is directly transferable to nearby greenfield or brownfield projects.

- 2 countries: Bulgaria, Namibia

- Improved cost control and agility

- Stronger supply-chain reliability

- Community ties mitigate social risk

Exploration and development pipeline

Active projects and prospects provide clear organic growth options, with brownfield drilling programs focused on extending mine life and improving unit economics. Greenfield exploration in Serbia offers meaningful upside optionality to the resource base. A balanced pipeline across brownfield and greenfield workstreams supports reserve replacement and future production continuity.

- Organic growth via active projects

- Brownfield drilling extends mine life

- Serbia greenfield exploration upsides

- Balanced pipeline sustains reserves

Tri-country mining platform: integrated value chain, lower costs and scalable growth

Three-country footprint (Bulgaria, Namibia, Serbia) reduces single-country risk and broadens market exposure.

Integrated value chain from exploration to processing lowers unit costs and accelerates project delivery.

Strong local experience and community ties in Bulgaria and Namibia improve permitting and cost control.

Active brownfield work and Serbia greenfield exploration provide organic growth optionality.

| Metric | Value |

|---|---|

| Countries | 3 |

| Producing countries | 2 |

| Greenfield country | 1 (Serbia) |

What is included in the product

Provides a concise SWOT overview of Dundee’s internal strengths and weaknesses and the external opportunities and threats shaping its market position. Highlights strategic advantages, operational gaps, and risks to inform decision-making.

Provides a concise Dundee SWOT matrix that rapidly pinpoints strategic pain points and aligns remediation actions for faster decision-making.

Weaknesses

Commodity price dependence

Revenue is highly sensitive to gold and by-product prices — with gold averaging about $2,100/oz in 2024, a 10% price decline would materially compress margins and reduce EBITDA. Downturns constrain discretionary investment and can defer capital projects and exploration spending. Hedging options are often limited by company policy or market liquidity, and cash flow volatility (quarterly swings of 20–30% observed in mining peers) can impede funding for growth.

Portfolio concentration

Portfolio concentration in Dundee stems from reliance on a limited number of core mines, which raises asset-specific risk and makes company-level outcomes sensitive to individual-site performance.

Unplanned outages or grade variability at any of these assets can disproportionately hit production and cash flow, while concentration amplifies country and regulatory exposure around key jurisdictions.

Diversifying by increasing asset count or joint-venture exposure remains a strategic challenge for reducing volatility and improving operational resilience.

Capital intensity and permitting timelines

New mines and processing facilities require large upfront capital—typically hundreds of millions to over US$1 billion for greenfield projects—straining Dundee’s balance sheet and funding needs. Long permitting cycles, often 3–7 years in major jurisdictions, delay cash flow and raise carrying costs. Equipment and labor cost inflation (roughly 10–20% 2020–24) pressures budgets, and schedule slippage can cut project IRRs by several percentage points per year delayed.

Operational complexity in processing

Processing complex concentrates raises technical risk: industry cases in 2024 noted metallurgical variability driving recovery swings up to 5 percentage points and occasional throughput losses of 10–20%, increasing unit costs; specialized environmental controls in 2024 pushed compliance and OPEX higher, and any processing bottleneck can cascade quickly into lower mine performance.

- Technical risk: higher failure rates

- Recovery volatility: ±5 ppt (2024)

- Throughput hit: 10–20% losses

- Compliance/OPEX up in 2024

FX and cost-base exposure

Costs and revenues in multiple currencies create translation and transaction risk, while local inflation in key operating regions can outpace commodity-driven revenue gains; supply-chain disruptions have pushed input costs higher and hedging programs may not fully offset sudden FX or commodity volatility.

- Multi-currency exposure: translation & transaction risk

- Local inflation can exceed commodity price lifts

- Supply-chain shocks raise input costs

- Hedges mitigate but do not eliminate volatility

Gold revenue risk: 10% price drop can materially compress EBITDA

Revenue tied to gold (avg $2,100/oz in 2024) makes margins highly price-sensitive; a 10% gold drop materially compresses EBITDA. Heavy capex (hundreds of millions to >$1bn for greenfield), 3–7 year permits and 10–20% equipment/labor inflation strain funding. Metallurgical recovery volatility (±5 ppt in 2024) and 10–20% throughput hits raise unit costs; FX/local inflation and supply shocks add cash‑flow volatility.

| Metric | 2024/2025 | Impact |

|---|---|---|

| Gold price | $2,100/oz (2024) | EBITDA sensitivity |

| Greenfield capex | >$1bn | Balance sheet strain |

| Permitting | 3–7 yrs | Delayed cash flow |

| Recovery volatility | ±5 ppt (2024) | Unit cost up |

| Throughput loss | 10–20% | Production hit |

| Cash‑flow swings | 20–30% | Funding risk |

Preview the Actual Deliverable

Dundee SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Dive Deeper Into the Company’s Strategic Blueprint

Our Dundee SWOT Analysis highlights the firm's core strengths, competitive risks, and untapped growth avenues in concise, evidence-backed terms. Explore strategic implications for investors and managers. Purchase the full SWOT to access a detailed, editable report and Excel tools. Make data-driven decisions with confidence.

Strengths

Diversified operating footprint

Operations across Bulgaria, Namibia and Serbia create a three-country footprint that reduces single-country risk and broadens market exposure.

Exposure to multiple regulatory and fiscal regimes smooths operational disruptions and tax variability across these three jurisdictions.

Regional diversification widens access to talent and suppliers and allows redeployment of capital among the three operations as conditions change.

End-to-end precious metals capabilities

Spanning acquisition, exploration, development, mining and processing, Dundee captures value across the full precious‑metals chain, lowering unit costs and improving recoveries through process integration. Integrated operations accelerate project timelines and embed technical know‑how and execution discipline across sites. This breadth supports steady pipeline renewal and enhances cash‑flow durability.

Strong ESG and responsible mining focus

Dundee's stated commitment to sustainable practices supports permitting, community relations and long-term license to operate, reducing risk of project delays. Robust ESG performance lowers operational interruptions and regulatory friction, helping maintain steady production. Transparent stewardship can broaden investor access and potentially lower cost of capital while enhancing brand and stakeholder trust.

Operational experience in Europe and Africa

Operational experience in Europe and Africa, notably Bulgaria and Namibia, strengthens local knowledge, enabling agility and tighter cost control. Familiarity with regional infrastructure and supply chains supports consistent production and logistics. Established community relationships reduce social risk and ease permitting, and this operational base is directly transferable to nearby greenfield or brownfield projects.

- 2 countries: Bulgaria, Namibia

- Improved cost control and agility

- Stronger supply-chain reliability

- Community ties mitigate social risk

Exploration and development pipeline

Active projects and prospects provide clear organic growth options, with brownfield drilling programs focused on extending mine life and improving unit economics. Greenfield exploration in Serbia offers meaningful upside optionality to the resource base. A balanced pipeline across brownfield and greenfield workstreams supports reserve replacement and future production continuity.

- Organic growth via active projects

- Brownfield drilling extends mine life

- Serbia greenfield exploration upsides

- Balanced pipeline sustains reserves

Tri-country mining platform: integrated value chain, lower costs and scalable growth

Three-country footprint (Bulgaria, Namibia, Serbia) reduces single-country risk and broadens market exposure.

Integrated value chain from exploration to processing lowers unit costs and accelerates project delivery.

Strong local experience and community ties in Bulgaria and Namibia improve permitting and cost control.

Active brownfield work and Serbia greenfield exploration provide organic growth optionality.

| Metric | Value |

|---|---|

| Countries | 3 |

| Producing countries | 2 |

| Greenfield country | 1 (Serbia) |

What is included in the product

Provides a concise SWOT overview of Dundee’s internal strengths and weaknesses and the external opportunities and threats shaping its market position. Highlights strategic advantages, operational gaps, and risks to inform decision-making.

Provides a concise Dundee SWOT matrix that rapidly pinpoints strategic pain points and aligns remediation actions for faster decision-making.

Weaknesses

Commodity price dependence

Revenue is highly sensitive to gold and by-product prices — with gold averaging about $2,100/oz in 2024, a 10% price decline would materially compress margins and reduce EBITDA. Downturns constrain discretionary investment and can defer capital projects and exploration spending. Hedging options are often limited by company policy or market liquidity, and cash flow volatility (quarterly swings of 20–30% observed in mining peers) can impede funding for growth.

Portfolio concentration

Portfolio concentration in Dundee stems from reliance on a limited number of core mines, which raises asset-specific risk and makes company-level outcomes sensitive to individual-site performance.

Unplanned outages or grade variability at any of these assets can disproportionately hit production and cash flow, while concentration amplifies country and regulatory exposure around key jurisdictions.

Diversifying by increasing asset count or joint-venture exposure remains a strategic challenge for reducing volatility and improving operational resilience.

Capital intensity and permitting timelines

New mines and processing facilities require large upfront capital—typically hundreds of millions to over US$1 billion for greenfield projects—straining Dundee’s balance sheet and funding needs. Long permitting cycles, often 3–7 years in major jurisdictions, delay cash flow and raise carrying costs. Equipment and labor cost inflation (roughly 10–20% 2020–24) pressures budgets, and schedule slippage can cut project IRRs by several percentage points per year delayed.

Operational complexity in processing

Processing complex concentrates raises technical risk: industry cases in 2024 noted metallurgical variability driving recovery swings up to 5 percentage points and occasional throughput losses of 10–20%, increasing unit costs; specialized environmental controls in 2024 pushed compliance and OPEX higher, and any processing bottleneck can cascade quickly into lower mine performance.

- Technical risk: higher failure rates

- Recovery volatility: ±5 ppt (2024)

- Throughput hit: 10–20% losses

- Compliance/OPEX up in 2024

FX and cost-base exposure

Costs and revenues in multiple currencies create translation and transaction risk, while local inflation in key operating regions can outpace commodity-driven revenue gains; supply-chain disruptions have pushed input costs higher and hedging programs may not fully offset sudden FX or commodity volatility.

- Multi-currency exposure: translation & transaction risk

- Local inflation can exceed commodity price lifts

- Supply-chain shocks raise input costs

- Hedges mitigate but do not eliminate volatility

Gold revenue risk: 10% price drop can materially compress EBITDA

Revenue tied to gold (avg $2,100/oz in 2024) makes margins highly price-sensitive; a 10% gold drop materially compresses EBITDA. Heavy capex (hundreds of millions to >$1bn for greenfield), 3–7 year permits and 10–20% equipment/labor inflation strain funding. Metallurgical recovery volatility (±5 ppt in 2024) and 10–20% throughput hits raise unit costs; FX/local inflation and supply shocks add cash‑flow volatility.

| Metric | 2024/2025 | Impact |

|---|---|---|

| Gold price | $2,100/oz (2024) | EBITDA sensitivity |

| Greenfield capex | >$1bn | Balance sheet strain |

| Permitting | 3–7 yrs | Delayed cash flow |

| Recovery volatility | ±5 ppt (2024) | Unit cost up |

| Throughput loss | 10–20% | Production hit |

| Cash‑flow swings | 20–30% | Funding risk |

Preview the Actual Deliverable

Dundee SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Our Dundee SWOT Analysis highlights the firm's core strengths, competitive risks, and untapped growth avenues in concise, evidence-backed terms. Explore strategic implications for investors and managers. Purchase the full SWOT to access a detailed, editable report and Excel tools. Make data-driven decisions with confidence.

Strengths

Diversified operating footprint

Operations across Bulgaria, Namibia and Serbia create a three-country footprint that reduces single-country risk and broadens market exposure.

Exposure to multiple regulatory and fiscal regimes smooths operational disruptions and tax variability across these three jurisdictions.

Regional diversification widens access to talent and suppliers and allows redeployment of capital among the three operations as conditions change.

End-to-end precious metals capabilities

Spanning acquisition, exploration, development, mining and processing, Dundee captures value across the full precious‑metals chain, lowering unit costs and improving recoveries through process integration. Integrated operations accelerate project timelines and embed technical know‑how and execution discipline across sites. This breadth supports steady pipeline renewal and enhances cash‑flow durability.

Strong ESG and responsible mining focus

Dundee's stated commitment to sustainable practices supports permitting, community relations and long-term license to operate, reducing risk of project delays. Robust ESG performance lowers operational interruptions and regulatory friction, helping maintain steady production. Transparent stewardship can broaden investor access and potentially lower cost of capital while enhancing brand and stakeholder trust.

Operational experience in Europe and Africa

Operational experience in Europe and Africa, notably Bulgaria and Namibia, strengthens local knowledge, enabling agility and tighter cost control. Familiarity with regional infrastructure and supply chains supports consistent production and logistics. Established community relationships reduce social risk and ease permitting, and this operational base is directly transferable to nearby greenfield or brownfield projects.

- 2 countries: Bulgaria, Namibia

- Improved cost control and agility

- Stronger supply-chain reliability

- Community ties mitigate social risk

Exploration and development pipeline

Active projects and prospects provide clear organic growth options, with brownfield drilling programs focused on extending mine life and improving unit economics. Greenfield exploration in Serbia offers meaningful upside optionality to the resource base. A balanced pipeline across brownfield and greenfield workstreams supports reserve replacement and future production continuity.

- Organic growth via active projects

- Brownfield drilling extends mine life

- Serbia greenfield exploration upsides

- Balanced pipeline sustains reserves

Tri-country mining platform: integrated value chain, lower costs and scalable growth

Three-country footprint (Bulgaria, Namibia, Serbia) reduces single-country risk and broadens market exposure.

Integrated value chain from exploration to processing lowers unit costs and accelerates project delivery.

Strong local experience and community ties in Bulgaria and Namibia improve permitting and cost control.

Active brownfield work and Serbia greenfield exploration provide organic growth optionality.

| Metric | Value |

|---|---|

| Countries | 3 |

| Producing countries | 2 |

| Greenfield country | 1 (Serbia) |

What is included in the product

Provides a concise SWOT overview of Dundee’s internal strengths and weaknesses and the external opportunities and threats shaping its market position. Highlights strategic advantages, operational gaps, and risks to inform decision-making.

Provides a concise Dundee SWOT matrix that rapidly pinpoints strategic pain points and aligns remediation actions for faster decision-making.

Weaknesses

Commodity price dependence

Revenue is highly sensitive to gold and by-product prices — with gold averaging about $2,100/oz in 2024, a 10% price decline would materially compress margins and reduce EBITDA. Downturns constrain discretionary investment and can defer capital projects and exploration spending. Hedging options are often limited by company policy or market liquidity, and cash flow volatility (quarterly swings of 20–30% observed in mining peers) can impede funding for growth.

Portfolio concentration

Portfolio concentration in Dundee stems from reliance on a limited number of core mines, which raises asset-specific risk and makes company-level outcomes sensitive to individual-site performance.

Unplanned outages or grade variability at any of these assets can disproportionately hit production and cash flow, while concentration amplifies country and regulatory exposure around key jurisdictions.

Diversifying by increasing asset count or joint-venture exposure remains a strategic challenge for reducing volatility and improving operational resilience.

Capital intensity and permitting timelines

New mines and processing facilities require large upfront capital—typically hundreds of millions to over US$1 billion for greenfield projects—straining Dundee’s balance sheet and funding needs. Long permitting cycles, often 3–7 years in major jurisdictions, delay cash flow and raise carrying costs. Equipment and labor cost inflation (roughly 10–20% 2020–24) pressures budgets, and schedule slippage can cut project IRRs by several percentage points per year delayed.

Operational complexity in processing

Processing complex concentrates raises technical risk: industry cases in 2024 noted metallurgical variability driving recovery swings up to 5 percentage points and occasional throughput losses of 10–20%, increasing unit costs; specialized environmental controls in 2024 pushed compliance and OPEX higher, and any processing bottleneck can cascade quickly into lower mine performance.

- Technical risk: higher failure rates

- Recovery volatility: ±5 ppt (2024)

- Throughput hit: 10–20% losses

- Compliance/OPEX up in 2024

FX and cost-base exposure

Costs and revenues in multiple currencies create translation and transaction risk, while local inflation in key operating regions can outpace commodity-driven revenue gains; supply-chain disruptions have pushed input costs higher and hedging programs may not fully offset sudden FX or commodity volatility.

- Multi-currency exposure: translation & transaction risk

- Local inflation can exceed commodity price lifts

- Supply-chain shocks raise input costs

- Hedges mitigate but do not eliminate volatility

Gold revenue risk: 10% price drop can materially compress EBITDA

Revenue tied to gold (avg $2,100/oz in 2024) makes margins highly price-sensitive; a 10% gold drop materially compresses EBITDA. Heavy capex (hundreds of millions to >$1bn for greenfield), 3–7 year permits and 10–20% equipment/labor inflation strain funding. Metallurgical recovery volatility (±5 ppt in 2024) and 10–20% throughput hits raise unit costs; FX/local inflation and supply shocks add cash‑flow volatility.

| Metric | 2024/2025 | Impact |

|---|---|---|

| Gold price | $2,100/oz (2024) | EBITDA sensitivity |

| Greenfield capex | >$1bn | Balance sheet strain |

| Permitting | 3–7 yrs | Delayed cash flow |

| Recovery volatility | ±5 ppt (2024) | Unit cost up |

| Throughput loss | 10–20% | Production hit |

| Cash‑flow swings | 20–30% | Funding risk |

Preview the Actual Deliverable

Dundee SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, detailed version immediately after checkout.