Eagers Automotive Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Eagers Automotive faces intense rivalry from national dealership groups, moderate supplier influence, and shifting buyer preferences toward online channels; regulatory and capital barriers limit new entrants while substitutes (used-car online platforms) rise. This snapshot highlights core competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Eagers Automotive.

Suppliers Bargaining Power

OEM brand concentration

Major global automakers tightly control allocations, pricing and model mix, with the top five OEMs accounting for about 45% of global vehicle production in 2024, concentrating supplier power; franchise agreements further set standards and limit dealer autonomy. Eagers mitigates risk via a multi-brand portfolio but new-vehicle pipelines still represent roughly 70% of group retail volume, so production or incentive shifts can quickly compress dealer margins.

Inventory and allocation control

Manufacturers control build slots and delivery timing for high-demand models, forcing dealers to accept tougher margins or longer wait times to secure inventory. In tight supply cycles dealers often take less favorable payment and return terms to maintain sales flow. Allocation leverage directly shapes sales velocity and F&I attachment rates by determining retail availability. Eagers’ scale can improve allocation priority but cannot remove OEM gatekeeping over builds and timing.

Parts and service dependency

Genuine parts sourcing remains captive to OEM networks, sustaining supplier bargaining power and limiting procurement leverage; in FY2024 Eagers reported group revenue of AU$13.1bn, highlighting scale but limited parts sourcing flexibility. Warranty work reimbursement rates and policies are OEM-set, constraining aftersales margin optimization and recovery on labor. Eagers offsets this by deploying approved aftermarket options and supplier-approved remanufactured parts where permissible to protect margins.

Technology and data lock-in

OEM-mandated systems for diagnostics and digital retail create significant switching costs for Eagers; compliance with brand standards drives ongoing capex and certification spend. Data-sharing requirements give OEMs advantages in customer ownership and retention, forcing Eagers to invest in integration, security, and throughput to maintain margins and brand access.

- OEM systems raise switching costs

- Ongoing capex for certification

- OEMs gain customer data leverage

- Eagers must invest in integration

Marketing and incentive programs

OEM bonus structures, co-op funds and stair-step incentives in FY2024 shifted pricing power toward manufacturers by driving volume-linked discounts that eroded dealer gross margins; Eagers reported FY2024 revenue AU$11.8bn and used scale to access higher incentive tiers.

Scale partially rebalanced power—larger groups like Eagers capture more co-op allocation—but program design and ultimate discretion remain OEM-controlled.

- OEM bonus structures: volume targets

- Co-op funds: marketing support, tiered access

- Stair-step incentives: discounts tied to monthly/quarterly thresholds

OEM dominance trims dealer margins as AU$13.1bn group faces 70% new-vehicle exposure

OEMs hold strong leverage over allocations, pricing and model mix (top five OEMs ~45% of global production in 2024), constraining Eagers’ margins despite AU$13.1bn group revenue in FY2024; new-vehicle pipelines still ~70% of retail volume so shifts in build/incentives quickly hit profitability. Parts, warranty rules and mandated systems sustain supplier power and raise switching costs, partially offset by Eagers’ scale.

| Metric | 2024 value |

|---|---|

| Group revenue | AU$13.1bn |

| New-vehicle share | ~70% |

| Top5 OEMs global prod | ~45% |

What is included in the product

Tailored Porter's Five Forces for Eagers Automotive, uncovering competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats to assess pricing influence, market share risks, and strategic defenses for stakeholders and investors.

A concise Porter's Five Forces summary for Eagers Automotive that turns complex competitive dynamics into a single, customizable one-sheet—adjust pressure levels, swap your data, and export a ready-to-use spider chart for decks or dashboards.

Customers Bargaining Power

Price transparency

Online listings and comparison tools have empowered buyers—by 2024, about 88% of vehicle purchasers researched options online—letting customers cross-shop across regions instantly, compressing front-end gross and lengthening negotiation cycles. Eagers must deploy data-driven pricing engines and offer value-added bundles (service, warranties, financing) to defend margins and shorten conversion time.

Financing optionality

Buyers can source finance from banks, credit unions and digital lenders, diluting dealer F&I capture; rate comparison platforms increase APR sensitivity and shopping intensity. Eagers counters with integrated F&I offers and faster approvals through dealer networks and captive financing partnerships. Despite these measures, high churn in F&I products weakens per-unit profitability and overall unit economics.

Switching ease across dealers

Multiple franchise networks in metro areas keep switching costs low; Eagers' 200+ outlets in 2024 increased local choice and enabled customers to defect for small price or feature differences. Loyalty programs and bundled service packages have raised retention rates but not fully stemmed churn. Eagers’ footprint improves convenience but does not eliminate the risk of customers moving to rivals for marginal gains.

Fleet and corporate buyers

Fleet and corporate buyers wield strong bargaining power by negotiating volume discounts and strict service SLAs, pressuring margins through competitive tender processes while delivering steady throughput. Eagers leverages scale and broad dealer footprint to meet fleet requirements and capture repeat business, but contract renewals and retendering can reset economics and compress pricing over time.

- Volume discounts drive margin pressure

- Tenders ensure stable sales flow but lower margins

- Scale and network are key competitive advantages

- Renewals can materially change contract economics

Used car information symmetry

Used car information symmetry—driven by vehicle history reports and valuation guides—reduces customer uncertainty and raises bargaining power as buyers expect trade-in and retail pricing aligned to live market values. Rapid repricing is essential to prevent stale inventory and margin erosion. Eagers uses centralized analytics and real-time market feeds to defend margins and accelerate price moves.

- Vehicle history reports increase buyer confidence

- Customers demand market-aligned pricing

- Rapid repricing prevents inventory markdowns

- Eagers central analytics protect margins

88% research online; 200+ outlets boost switching — real-time repricing protects margins

Customers hold elevated bargaining power: 88% researched vehicles online in 2024, enabling cross-shop and price compression; Eagers' 200+ outlets increase local choice and switching. F&I capture diluted by external lenders; Eagers relies on captive partnerships and bundled offers to protect margin. Real-time pricing and centralized analytics are essential to prevent rapid margin erosion on used stock.

| Metric | 2024 value | Impact |

|---|---|---|

| Online research | 88% | Higher price transparency |

| Outlets | 200+ | Lower switching costs |

| Real-time repricing | Implemented | Protects margins |

Same Document Delivered

Eagers Automotive Porter's Five Forces Analysis

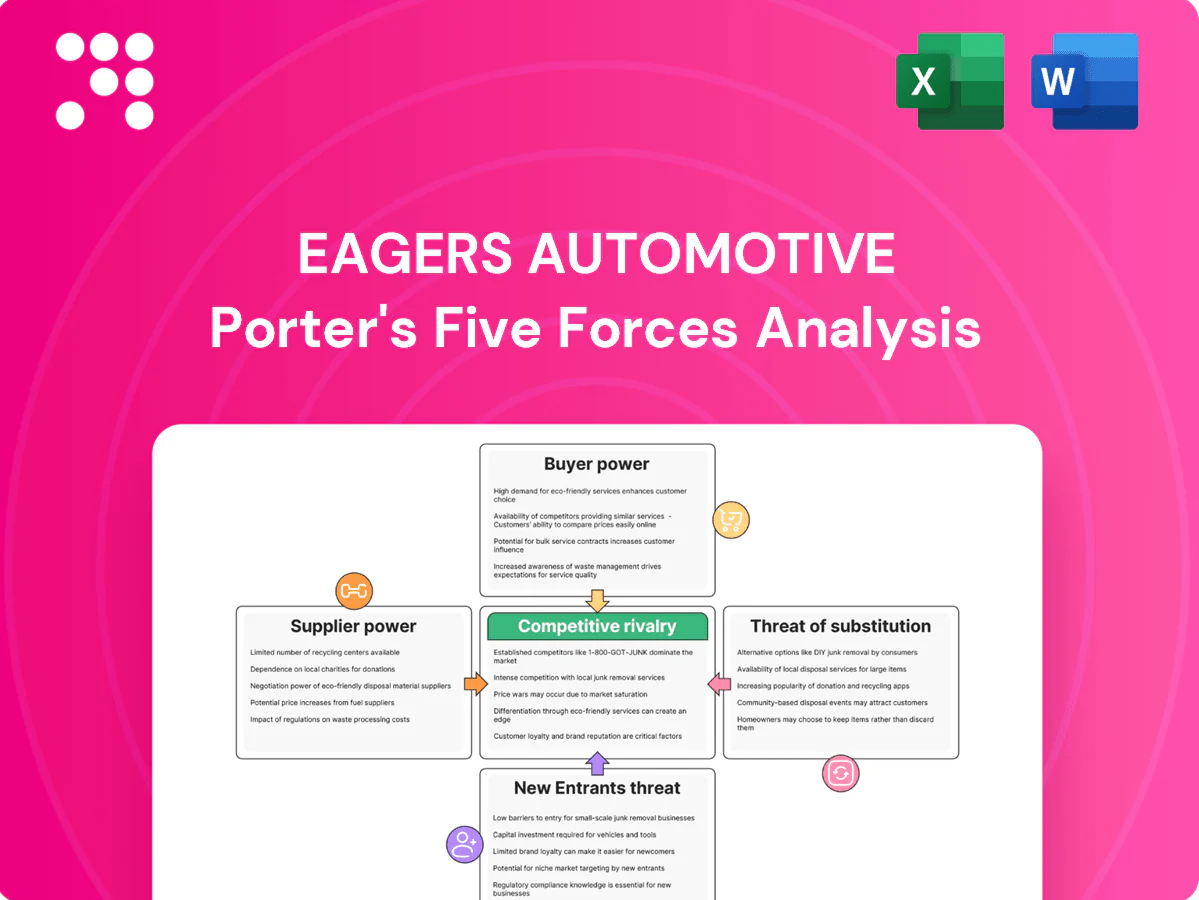

This preview shows the exact Porter's Five Forces analysis for Eagers Automotive you'll receive—no placeholders, no mockups. It assesses threat of entrants, buyer and supplier power, substitute products, and competitive rivalry with professional formatting and citations. Purchase grants immediate access to this ready-to-use, fully formatted document.

Go Beyond the Preview—Access the Full Strategic Report

Eagers Automotive faces intense rivalry from national dealership groups, moderate supplier influence, and shifting buyer preferences toward online channels; regulatory and capital barriers limit new entrants while substitutes (used-car online platforms) rise. This snapshot highlights core competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Eagers Automotive.

Suppliers Bargaining Power

OEM brand concentration

Major global automakers tightly control allocations, pricing and model mix, with the top five OEMs accounting for about 45% of global vehicle production in 2024, concentrating supplier power; franchise agreements further set standards and limit dealer autonomy. Eagers mitigates risk via a multi-brand portfolio but new-vehicle pipelines still represent roughly 70% of group retail volume, so production or incentive shifts can quickly compress dealer margins.

Inventory and allocation control

Manufacturers control build slots and delivery timing for high-demand models, forcing dealers to accept tougher margins or longer wait times to secure inventory. In tight supply cycles dealers often take less favorable payment and return terms to maintain sales flow. Allocation leverage directly shapes sales velocity and F&I attachment rates by determining retail availability. Eagers’ scale can improve allocation priority but cannot remove OEM gatekeeping over builds and timing.

Parts and service dependency

Genuine parts sourcing remains captive to OEM networks, sustaining supplier bargaining power and limiting procurement leverage; in FY2024 Eagers reported group revenue of AU$13.1bn, highlighting scale but limited parts sourcing flexibility. Warranty work reimbursement rates and policies are OEM-set, constraining aftersales margin optimization and recovery on labor. Eagers offsets this by deploying approved aftermarket options and supplier-approved remanufactured parts where permissible to protect margins.

Technology and data lock-in

OEM-mandated systems for diagnostics and digital retail create significant switching costs for Eagers; compliance with brand standards drives ongoing capex and certification spend. Data-sharing requirements give OEMs advantages in customer ownership and retention, forcing Eagers to invest in integration, security, and throughput to maintain margins and brand access.

- OEM systems raise switching costs

- Ongoing capex for certification

- OEMs gain customer data leverage

- Eagers must invest in integration

Marketing and incentive programs

OEM bonus structures, co-op funds and stair-step incentives in FY2024 shifted pricing power toward manufacturers by driving volume-linked discounts that eroded dealer gross margins; Eagers reported FY2024 revenue AU$11.8bn and used scale to access higher incentive tiers.

Scale partially rebalanced power—larger groups like Eagers capture more co-op allocation—but program design and ultimate discretion remain OEM-controlled.

- OEM bonus structures: volume targets

- Co-op funds: marketing support, tiered access

- Stair-step incentives: discounts tied to monthly/quarterly thresholds

OEM dominance trims dealer margins as AU$13.1bn group faces 70% new-vehicle exposure

OEMs hold strong leverage over allocations, pricing and model mix (top five OEMs ~45% of global production in 2024), constraining Eagers’ margins despite AU$13.1bn group revenue in FY2024; new-vehicle pipelines still ~70% of retail volume so shifts in build/incentives quickly hit profitability. Parts, warranty rules and mandated systems sustain supplier power and raise switching costs, partially offset by Eagers’ scale.

| Metric | 2024 value |

|---|---|

| Group revenue | AU$13.1bn |

| New-vehicle share | ~70% |

| Top5 OEMs global prod | ~45% |

What is included in the product

Tailored Porter's Five Forces for Eagers Automotive, uncovering competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats to assess pricing influence, market share risks, and strategic defenses for stakeholders and investors.

A concise Porter's Five Forces summary for Eagers Automotive that turns complex competitive dynamics into a single, customizable one-sheet—adjust pressure levels, swap your data, and export a ready-to-use spider chart for decks or dashboards.

Customers Bargaining Power

Price transparency

Online listings and comparison tools have empowered buyers—by 2024, about 88% of vehicle purchasers researched options online—letting customers cross-shop across regions instantly, compressing front-end gross and lengthening negotiation cycles. Eagers must deploy data-driven pricing engines and offer value-added bundles (service, warranties, financing) to defend margins and shorten conversion time.

Financing optionality

Buyers can source finance from banks, credit unions and digital lenders, diluting dealer F&I capture; rate comparison platforms increase APR sensitivity and shopping intensity. Eagers counters with integrated F&I offers and faster approvals through dealer networks and captive financing partnerships. Despite these measures, high churn in F&I products weakens per-unit profitability and overall unit economics.

Switching ease across dealers

Multiple franchise networks in metro areas keep switching costs low; Eagers' 200+ outlets in 2024 increased local choice and enabled customers to defect for small price or feature differences. Loyalty programs and bundled service packages have raised retention rates but not fully stemmed churn. Eagers’ footprint improves convenience but does not eliminate the risk of customers moving to rivals for marginal gains.

Fleet and corporate buyers

Fleet and corporate buyers wield strong bargaining power by negotiating volume discounts and strict service SLAs, pressuring margins through competitive tender processes while delivering steady throughput. Eagers leverages scale and broad dealer footprint to meet fleet requirements and capture repeat business, but contract renewals and retendering can reset economics and compress pricing over time.

- Volume discounts drive margin pressure

- Tenders ensure stable sales flow but lower margins

- Scale and network are key competitive advantages

- Renewals can materially change contract economics

Used car information symmetry

Used car information symmetry—driven by vehicle history reports and valuation guides—reduces customer uncertainty and raises bargaining power as buyers expect trade-in and retail pricing aligned to live market values. Rapid repricing is essential to prevent stale inventory and margin erosion. Eagers uses centralized analytics and real-time market feeds to defend margins and accelerate price moves.

- Vehicle history reports increase buyer confidence

- Customers demand market-aligned pricing

- Rapid repricing prevents inventory markdowns

- Eagers central analytics protect margins

88% research online; 200+ outlets boost switching — real-time repricing protects margins

Customers hold elevated bargaining power: 88% researched vehicles online in 2024, enabling cross-shop and price compression; Eagers' 200+ outlets increase local choice and switching. F&I capture diluted by external lenders; Eagers relies on captive partnerships and bundled offers to protect margin. Real-time pricing and centralized analytics are essential to prevent rapid margin erosion on used stock.

| Metric | 2024 value | Impact |

|---|---|---|

| Online research | 88% | Higher price transparency |

| Outlets | 200+ | Lower switching costs |

| Real-time repricing | Implemented | Protects margins |

Same Document Delivered

Eagers Automotive Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Eagers Automotive you'll receive—no placeholders, no mockups. It assesses threat of entrants, buyer and supplier power, substitute products, and competitive rivalry with professional formatting and citations. Purchase grants immediate access to this ready-to-use, fully formatted document.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Eagers Automotive faces intense rivalry from national dealership groups, moderate supplier influence, and shifting buyer preferences toward online channels; regulatory and capital barriers limit new entrants while substitutes (used-car online platforms) rise. This snapshot highlights core competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Eagers Automotive.

Suppliers Bargaining Power

OEM brand concentration

Major global automakers tightly control allocations, pricing and model mix, with the top five OEMs accounting for about 45% of global vehicle production in 2024, concentrating supplier power; franchise agreements further set standards and limit dealer autonomy. Eagers mitigates risk via a multi-brand portfolio but new-vehicle pipelines still represent roughly 70% of group retail volume, so production or incentive shifts can quickly compress dealer margins.

Inventory and allocation control

Manufacturers control build slots and delivery timing for high-demand models, forcing dealers to accept tougher margins or longer wait times to secure inventory. In tight supply cycles dealers often take less favorable payment and return terms to maintain sales flow. Allocation leverage directly shapes sales velocity and F&I attachment rates by determining retail availability. Eagers’ scale can improve allocation priority but cannot remove OEM gatekeeping over builds and timing.

Parts and service dependency

Genuine parts sourcing remains captive to OEM networks, sustaining supplier bargaining power and limiting procurement leverage; in FY2024 Eagers reported group revenue of AU$13.1bn, highlighting scale but limited parts sourcing flexibility. Warranty work reimbursement rates and policies are OEM-set, constraining aftersales margin optimization and recovery on labor. Eagers offsets this by deploying approved aftermarket options and supplier-approved remanufactured parts where permissible to protect margins.

Technology and data lock-in

OEM-mandated systems for diagnostics and digital retail create significant switching costs for Eagers; compliance with brand standards drives ongoing capex and certification spend. Data-sharing requirements give OEMs advantages in customer ownership and retention, forcing Eagers to invest in integration, security, and throughput to maintain margins and brand access.

- OEM systems raise switching costs

- Ongoing capex for certification

- OEMs gain customer data leverage

- Eagers must invest in integration

Marketing and incentive programs

OEM bonus structures, co-op funds and stair-step incentives in FY2024 shifted pricing power toward manufacturers by driving volume-linked discounts that eroded dealer gross margins; Eagers reported FY2024 revenue AU$11.8bn and used scale to access higher incentive tiers.

Scale partially rebalanced power—larger groups like Eagers capture more co-op allocation—but program design and ultimate discretion remain OEM-controlled.

- OEM bonus structures: volume targets

- Co-op funds: marketing support, tiered access

- Stair-step incentives: discounts tied to monthly/quarterly thresholds

OEM dominance trims dealer margins as AU$13.1bn group faces 70% new-vehicle exposure

OEMs hold strong leverage over allocations, pricing and model mix (top five OEMs ~45% of global production in 2024), constraining Eagers’ margins despite AU$13.1bn group revenue in FY2024; new-vehicle pipelines still ~70% of retail volume so shifts in build/incentives quickly hit profitability. Parts, warranty rules and mandated systems sustain supplier power and raise switching costs, partially offset by Eagers’ scale.

| Metric | 2024 value |

|---|---|

| Group revenue | AU$13.1bn |

| New-vehicle share | ~70% |

| Top5 OEMs global prod | ~45% |

What is included in the product

Tailored Porter's Five Forces for Eagers Automotive, uncovering competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats to assess pricing influence, market share risks, and strategic defenses for stakeholders and investors.

A concise Porter's Five Forces summary for Eagers Automotive that turns complex competitive dynamics into a single, customizable one-sheet—adjust pressure levels, swap your data, and export a ready-to-use spider chart for decks or dashboards.

Customers Bargaining Power

Price transparency

Online listings and comparison tools have empowered buyers—by 2024, about 88% of vehicle purchasers researched options online—letting customers cross-shop across regions instantly, compressing front-end gross and lengthening negotiation cycles. Eagers must deploy data-driven pricing engines and offer value-added bundles (service, warranties, financing) to defend margins and shorten conversion time.

Financing optionality

Buyers can source finance from banks, credit unions and digital lenders, diluting dealer F&I capture; rate comparison platforms increase APR sensitivity and shopping intensity. Eagers counters with integrated F&I offers and faster approvals through dealer networks and captive financing partnerships. Despite these measures, high churn in F&I products weakens per-unit profitability and overall unit economics.

Switching ease across dealers

Multiple franchise networks in metro areas keep switching costs low; Eagers' 200+ outlets in 2024 increased local choice and enabled customers to defect for small price or feature differences. Loyalty programs and bundled service packages have raised retention rates but not fully stemmed churn. Eagers’ footprint improves convenience but does not eliminate the risk of customers moving to rivals for marginal gains.

Fleet and corporate buyers

Fleet and corporate buyers wield strong bargaining power by negotiating volume discounts and strict service SLAs, pressuring margins through competitive tender processes while delivering steady throughput. Eagers leverages scale and broad dealer footprint to meet fleet requirements and capture repeat business, but contract renewals and retendering can reset economics and compress pricing over time.

- Volume discounts drive margin pressure

- Tenders ensure stable sales flow but lower margins

- Scale and network are key competitive advantages

- Renewals can materially change contract economics

Used car information symmetry

Used car information symmetry—driven by vehicle history reports and valuation guides—reduces customer uncertainty and raises bargaining power as buyers expect trade-in and retail pricing aligned to live market values. Rapid repricing is essential to prevent stale inventory and margin erosion. Eagers uses centralized analytics and real-time market feeds to defend margins and accelerate price moves.

- Vehicle history reports increase buyer confidence

- Customers demand market-aligned pricing

- Rapid repricing prevents inventory markdowns

- Eagers central analytics protect margins

88% research online; 200+ outlets boost switching — real-time repricing protects margins

Customers hold elevated bargaining power: 88% researched vehicles online in 2024, enabling cross-shop and price compression; Eagers' 200+ outlets increase local choice and switching. F&I capture diluted by external lenders; Eagers relies on captive partnerships and bundled offers to protect margin. Real-time pricing and centralized analytics are essential to prevent rapid margin erosion on used stock.

| Metric | 2024 value | Impact |

|---|---|---|

| Online research | 88% | Higher price transparency |

| Outlets | 200+ | Lower switching costs |

| Real-time repricing | Implemented | Protects margins |

Same Document Delivered

Eagers Automotive Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Eagers Automotive you'll receive—no placeholders, no mockups. It assesses threat of entrants, buyer and supplier power, substitute products, and competitive rivalry with professional formatting and citations. Purchase grants immediate access to this ready-to-use, fully formatted document.