East West Bancorp Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

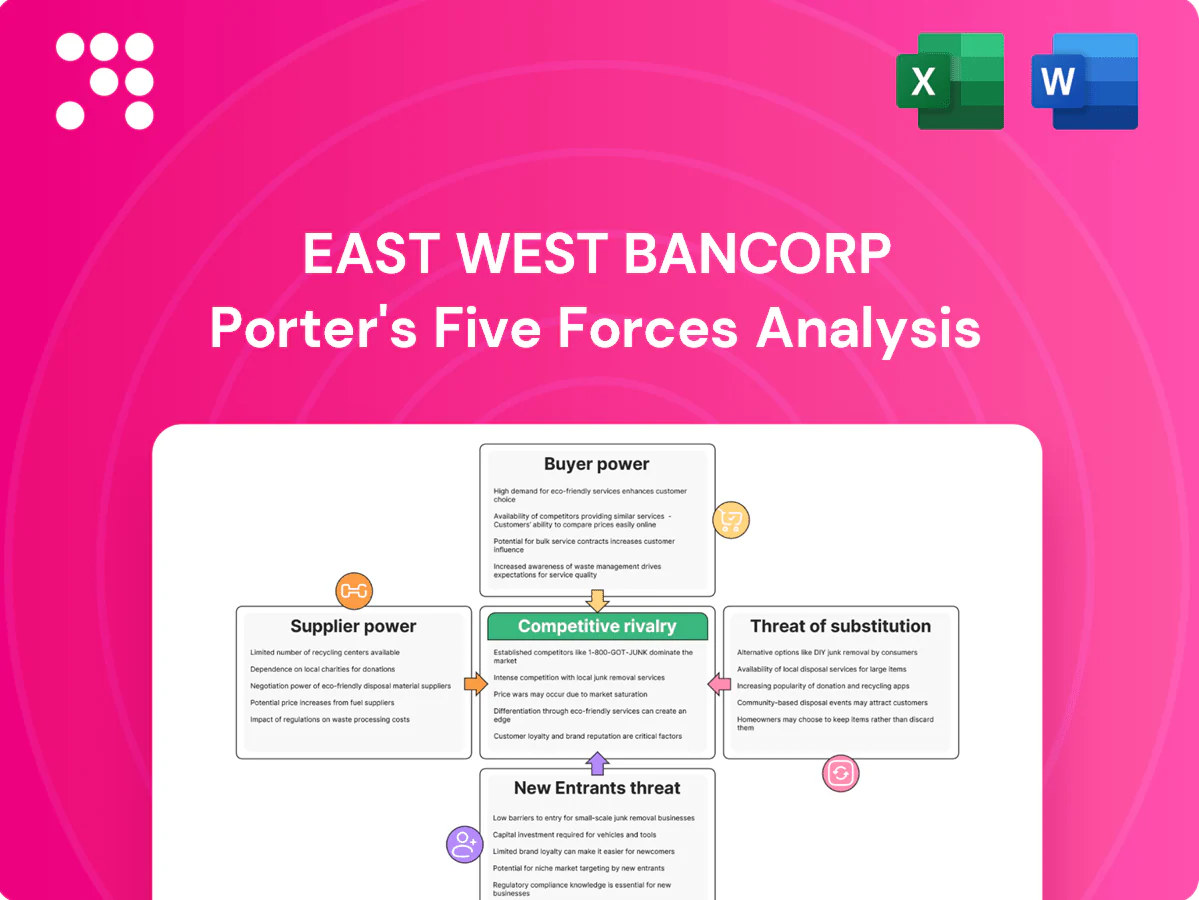

East West Bancorp faces moderate buyer power and strong regional competition, while scale advantages and regulatory barriers limit new entrants; supplier and substitute threats remain contained but digital disruption raises margin risk. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore East West Bancorp’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of funding sources

Deposits are East West Bancorp’s primary funding input, representing roughly 80% of funding in 2024, with large commercial and affluent accounts that can reprice rapidly. Wholesale lines and brokered deposits provided about 12% of funding in 2024, adding optionality but increasing market dependence. This concentration raises supplier power during tightening cycles; growing core retail, sticky deposits reduces that leverage.

Wholesale and capital market dependence

East West Bancorp relies on wholesale funding—FHLB advances, repo and senior debt—for liquidity and growth; with total assets near 58.5 billion in 2024, these sources are material to its balance sheet. In stressed markets providers can tighten terms, lift haircuts or widen spreads, raising funding costs and rolling risk exactly when liquidity is most needed. Maintaining strong liquidity coverage and contingent funding commitments reduces this supplier bargaining power and tail risk.

Technology and data vendor lock-in

Core banking, payments, cybersecurity and risk systems come from a concentrated vendor base, with top providers capturing roughly 60–70% of the US core market. Core replacements typically cost $50M–$200M and take 2–4 years, raising supplier pricing power. EWBC’s scale helps negotiate, but bespoke cross‑border needs add complexity. Multi‑vendor architectures and APIs can reduce lock‑in.

Specialized talent as a scarce input

Relationship bankers, trade finance specialists and bilingual compliance staff are pivotal for East West Bancorp’s US–Greater China corridor; their scarcity increases wage pressure and poaching risk, especially during credit booms and regulatory ramp‑ups; targeted retention programs and internal training pipelines materially lower supplier power and operational vulnerability.

- Key roles: relationship bankers, trade finance, bilingual compliance

- Risks: higher wages, poaching in hot cycles

- Mitigants: retention programs, training pipelines

Correspondent banks and payment rails

Correspondent banks and payment rails are critical for EWBC’s cross‑border clearing and FX liquidity; de‑risking and sanctions reduce available counterparties and boost supplier leverage, tightening pricing and service levels during geopolitical stress. Federal funds in 2024 averaged 5.25–5.50%, widening FX spreads and funding costs for corridors.

- De‑risking shrinks counterparty pool

- Sanctions raise pricing/service risk

- Diversified corridors + in‑house FX lower exposure

Deposits ≈80% concentration raises rollover risk, funding costs

Suppliers exert moderate‑high power: deposits ≈80% of funding (2024), wholesale ≈12% on $58.5B assets, making rollover risk material; FHLB/repo concentration raises costs in stress. Core vendors capture ~60–70% market; replacements cost $50M–$200M. Scarce bilingual relationship/compliance staff lift wage/poaching risk; liquidity buffers and retention reduce leverage.

| Metric | 2024 |

|---|---|

| Deposits (% funding) | ≈80% |

| Wholesale funding | ≈12% |

| Total assets | $58.5B |

| Core vendor share | 60–70% |

| Fed funds | 5.25–5.50% |

What is included in the product

Tailored Porter's Five Forces analysis for East West Bancorp, assessing competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes to reveal key drivers of profitability, emerging risks from fintech and regional banks, and strategic barriers that protect its market position.

A clear one-sheet Porter's Five Forces for East West Bancorp—quickly spot credit, competitive and regulatory pressures to simplify strategic decisions and investor decks.

Customers Bargaining Power

Rate sensitivity of depositors

Commercial and affluent clients are highly rate aware and in 2024 moved rapidly to higher-yield alternatives, increasing pricing pressure on deposits and compressing EWBCs NIM. EWBC must balance retention with margin discipline, selectively pricing core relationships while limiting spread erosion. Emphasizing value-added services—wealth management, treasury, and relationship banking—helps justify below-top-of-market rates to preserve loyalty.

Switching costs are moderate

Digital onboarding and treasury API integration have lowered frictions—East West Bancorp, with roughly $53 billion in assets in 2024, reports faster client activation—yet complex credit facilities, trade services and cross‑border cash management create meaningful switching costs that preserve client stickiness. Buyers increasingly use competitive bids to push down fees and tighten covenants, but deep relationship coverage and tailored commercial lending remain a potent defensive moat.

Concentration in key metros

Clientele clusters in CA, NY, TX and MA where strong Asian American communities drive relationship banking, giving local competitors alternative providers and pricing leverage. Regional economic slowdowns in these metros amplify renegotiation pressure on fees and loan terms. East West’s expanding geographic and sector diversification—including commercial real estate, C&I and wealth channels—helps blunt concentrated buyer power.

Credit structure negotiation

Middle‑market borrowers increasingly press on covenants, collateral packages and amortization schedules; syndicated deals and private credit alternatives (private debt AUM > $1T in 2024) amplify borrower leverage. East West Bancorp’s US–China cross‑border franchise (headquartered in Pasadena) helps it command terms despite pressure, while disciplined underwriting curbs concessions.

- Middle‑market covenant and collateral pressure

- Private credit scale > $1T (2024) boosts borrower options

- EWBC cross‑border franchise secures pricing

- Disciplined underwriting limits concessions

Service expectations and responsiveness

Clients demand seamless FX, payments, and bilingual support across time zones; 64% of corporate treasurers in 2024 ranked digital responsiveness as a top selection factor, raising buyer leverage when service gaps occur and prompting rapid switching.

Superior turnaround and tailored solutions at East West blunt pure price competition, and ongoing CX investment reduces elasticity of demand, preserving fee margins.

- Service-driven switching increases buyer leverage

- Bilingual, 24/7 support cited by 64% (2024)

- Faster turnaround lowers price sensitivity

Clients pressure pricing; cross-border services and private credit sustain margins

Customers exert moderate-to-high bargaining power: rate-sensitive commercial and affluent clients (EWBC assets $53B in 2024) push deposit pricing and fee compression, while deep relationship services and US–China cross‑border capabilities preserve margins. Digital responsiveness (64% of treasurers in 2024) and private credit scale (> $1T in 2024) raise switching options, but tailored lending and underwriting limit concessions.

| Metric | 2024 |

|---|---|

| EWBC assets | $53B |

| Private credit AUM | > $1T |

| Treasure digital priority | 64% |

Preview Before You Purchase

East West Bancorp Porter's Five Forces Analysis

This Porter’s Five Forces analysis of East West Bancorp examines competitive rivalry, buyer and supplier power, threats of new entrants and substitutes, and strategic implications for margins and growth. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

A Must-Have Tool for Decision-Makers

East West Bancorp faces moderate buyer power and strong regional competition, while scale advantages and regulatory barriers limit new entrants; supplier and substitute threats remain contained but digital disruption raises margin risk. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore East West Bancorp’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of funding sources

Deposits are East West Bancorp’s primary funding input, representing roughly 80% of funding in 2024, with large commercial and affluent accounts that can reprice rapidly. Wholesale lines and brokered deposits provided about 12% of funding in 2024, adding optionality but increasing market dependence. This concentration raises supplier power during tightening cycles; growing core retail, sticky deposits reduces that leverage.

Wholesale and capital market dependence

East West Bancorp relies on wholesale funding—FHLB advances, repo and senior debt—for liquidity and growth; with total assets near 58.5 billion in 2024, these sources are material to its balance sheet. In stressed markets providers can tighten terms, lift haircuts or widen spreads, raising funding costs and rolling risk exactly when liquidity is most needed. Maintaining strong liquidity coverage and contingent funding commitments reduces this supplier bargaining power and tail risk.

Technology and data vendor lock-in

Core banking, payments, cybersecurity and risk systems come from a concentrated vendor base, with top providers capturing roughly 60–70% of the US core market. Core replacements typically cost $50M–$200M and take 2–4 years, raising supplier pricing power. EWBC’s scale helps negotiate, but bespoke cross‑border needs add complexity. Multi‑vendor architectures and APIs can reduce lock‑in.

Specialized talent as a scarce input

Relationship bankers, trade finance specialists and bilingual compliance staff are pivotal for East West Bancorp’s US–Greater China corridor; their scarcity increases wage pressure and poaching risk, especially during credit booms and regulatory ramp‑ups; targeted retention programs and internal training pipelines materially lower supplier power and operational vulnerability.

- Key roles: relationship bankers, trade finance, bilingual compliance

- Risks: higher wages, poaching in hot cycles

- Mitigants: retention programs, training pipelines

Correspondent banks and payment rails

Correspondent banks and payment rails are critical for EWBC’s cross‑border clearing and FX liquidity; de‑risking and sanctions reduce available counterparties and boost supplier leverage, tightening pricing and service levels during geopolitical stress. Federal funds in 2024 averaged 5.25–5.50%, widening FX spreads and funding costs for corridors.

- De‑risking shrinks counterparty pool

- Sanctions raise pricing/service risk

- Diversified corridors + in‑house FX lower exposure

Deposits ≈80% concentration raises rollover risk, funding costs

Suppliers exert moderate‑high power: deposits ≈80% of funding (2024), wholesale ≈12% on $58.5B assets, making rollover risk material; FHLB/repo concentration raises costs in stress. Core vendors capture ~60–70% market; replacements cost $50M–$200M. Scarce bilingual relationship/compliance staff lift wage/poaching risk; liquidity buffers and retention reduce leverage.

| Metric | 2024 |

|---|---|

| Deposits (% funding) | ≈80% |

| Wholesale funding | ≈12% |

| Total assets | $58.5B |

| Core vendor share | 60–70% |

| Fed funds | 5.25–5.50% |

What is included in the product

Tailored Porter's Five Forces analysis for East West Bancorp, assessing competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes to reveal key drivers of profitability, emerging risks from fintech and regional banks, and strategic barriers that protect its market position.

A clear one-sheet Porter's Five Forces for East West Bancorp—quickly spot credit, competitive and regulatory pressures to simplify strategic decisions and investor decks.

Customers Bargaining Power

Rate sensitivity of depositors

Commercial and affluent clients are highly rate aware and in 2024 moved rapidly to higher-yield alternatives, increasing pricing pressure on deposits and compressing EWBCs NIM. EWBC must balance retention with margin discipline, selectively pricing core relationships while limiting spread erosion. Emphasizing value-added services—wealth management, treasury, and relationship banking—helps justify below-top-of-market rates to preserve loyalty.

Switching costs are moderate

Digital onboarding and treasury API integration have lowered frictions—East West Bancorp, with roughly $53 billion in assets in 2024, reports faster client activation—yet complex credit facilities, trade services and cross‑border cash management create meaningful switching costs that preserve client stickiness. Buyers increasingly use competitive bids to push down fees and tighten covenants, but deep relationship coverage and tailored commercial lending remain a potent defensive moat.

Concentration in key metros

Clientele clusters in CA, NY, TX and MA where strong Asian American communities drive relationship banking, giving local competitors alternative providers and pricing leverage. Regional economic slowdowns in these metros amplify renegotiation pressure on fees and loan terms. East West’s expanding geographic and sector diversification—including commercial real estate, C&I and wealth channels—helps blunt concentrated buyer power.

Credit structure negotiation

Middle‑market borrowers increasingly press on covenants, collateral packages and amortization schedules; syndicated deals and private credit alternatives (private debt AUM > $1T in 2024) amplify borrower leverage. East West Bancorp’s US–China cross‑border franchise (headquartered in Pasadena) helps it command terms despite pressure, while disciplined underwriting curbs concessions.

- Middle‑market covenant and collateral pressure

- Private credit scale > $1T (2024) boosts borrower options

- EWBC cross‑border franchise secures pricing

- Disciplined underwriting limits concessions

Service expectations and responsiveness

Clients demand seamless FX, payments, and bilingual support across time zones; 64% of corporate treasurers in 2024 ranked digital responsiveness as a top selection factor, raising buyer leverage when service gaps occur and prompting rapid switching.

Superior turnaround and tailored solutions at East West blunt pure price competition, and ongoing CX investment reduces elasticity of demand, preserving fee margins.

- Service-driven switching increases buyer leverage

- Bilingual, 24/7 support cited by 64% (2024)

- Faster turnaround lowers price sensitivity

Clients pressure pricing; cross-border services and private credit sustain margins

Customers exert moderate-to-high bargaining power: rate-sensitive commercial and affluent clients (EWBC assets $53B in 2024) push deposit pricing and fee compression, while deep relationship services and US–China cross‑border capabilities preserve margins. Digital responsiveness (64% of treasurers in 2024) and private credit scale (> $1T in 2024) raise switching options, but tailored lending and underwriting limit concessions.

| Metric | 2024 |

|---|---|

| EWBC assets | $53B |

| Private credit AUM | > $1T |

| Treasure digital priority | 64% |

Preview Before You Purchase

East West Bancorp Porter's Five Forces Analysis

This Porter’s Five Forces analysis of East West Bancorp examines competitive rivalry, buyer and supplier power, threats of new entrants and substitutes, and strategic implications for margins and growth. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

East West Bancorp faces moderate buyer power and strong regional competition, while scale advantages and regulatory barriers limit new entrants; supplier and substitute threats remain contained but digital disruption raises margin risk. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore East West Bancorp’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of funding sources

Deposits are East West Bancorp’s primary funding input, representing roughly 80% of funding in 2024, with large commercial and affluent accounts that can reprice rapidly. Wholesale lines and brokered deposits provided about 12% of funding in 2024, adding optionality but increasing market dependence. This concentration raises supplier power during tightening cycles; growing core retail, sticky deposits reduces that leverage.

Wholesale and capital market dependence

East West Bancorp relies on wholesale funding—FHLB advances, repo and senior debt—for liquidity and growth; with total assets near 58.5 billion in 2024, these sources are material to its balance sheet. In stressed markets providers can tighten terms, lift haircuts or widen spreads, raising funding costs and rolling risk exactly when liquidity is most needed. Maintaining strong liquidity coverage and contingent funding commitments reduces this supplier bargaining power and tail risk.

Technology and data vendor lock-in

Core banking, payments, cybersecurity and risk systems come from a concentrated vendor base, with top providers capturing roughly 60–70% of the US core market. Core replacements typically cost $50M–$200M and take 2–4 years, raising supplier pricing power. EWBC’s scale helps negotiate, but bespoke cross‑border needs add complexity. Multi‑vendor architectures and APIs can reduce lock‑in.

Specialized talent as a scarce input

Relationship bankers, trade finance specialists and bilingual compliance staff are pivotal for East West Bancorp’s US–Greater China corridor; their scarcity increases wage pressure and poaching risk, especially during credit booms and regulatory ramp‑ups; targeted retention programs and internal training pipelines materially lower supplier power and operational vulnerability.

- Key roles: relationship bankers, trade finance, bilingual compliance

- Risks: higher wages, poaching in hot cycles

- Mitigants: retention programs, training pipelines

Correspondent banks and payment rails

Correspondent banks and payment rails are critical for EWBC’s cross‑border clearing and FX liquidity; de‑risking and sanctions reduce available counterparties and boost supplier leverage, tightening pricing and service levels during geopolitical stress. Federal funds in 2024 averaged 5.25–5.50%, widening FX spreads and funding costs for corridors.

- De‑risking shrinks counterparty pool

- Sanctions raise pricing/service risk

- Diversified corridors + in‑house FX lower exposure

Deposits ≈80% concentration raises rollover risk, funding costs

Suppliers exert moderate‑high power: deposits ≈80% of funding (2024), wholesale ≈12% on $58.5B assets, making rollover risk material; FHLB/repo concentration raises costs in stress. Core vendors capture ~60–70% market; replacements cost $50M–$200M. Scarce bilingual relationship/compliance staff lift wage/poaching risk; liquidity buffers and retention reduce leverage.

| Metric | 2024 |

|---|---|

| Deposits (% funding) | ≈80% |

| Wholesale funding | ≈12% |

| Total assets | $58.5B |

| Core vendor share | 60–70% |

| Fed funds | 5.25–5.50% |

What is included in the product

Tailored Porter's Five Forces analysis for East West Bancorp, assessing competitive rivalry, buyer and supplier power, threat of new entrants, and substitutes to reveal key drivers of profitability, emerging risks from fintech and regional banks, and strategic barriers that protect its market position.

A clear one-sheet Porter's Five Forces for East West Bancorp—quickly spot credit, competitive and regulatory pressures to simplify strategic decisions and investor decks.

Customers Bargaining Power

Rate sensitivity of depositors

Commercial and affluent clients are highly rate aware and in 2024 moved rapidly to higher-yield alternatives, increasing pricing pressure on deposits and compressing EWBCs NIM. EWBC must balance retention with margin discipline, selectively pricing core relationships while limiting spread erosion. Emphasizing value-added services—wealth management, treasury, and relationship banking—helps justify below-top-of-market rates to preserve loyalty.

Switching costs are moderate

Digital onboarding and treasury API integration have lowered frictions—East West Bancorp, with roughly $53 billion in assets in 2024, reports faster client activation—yet complex credit facilities, trade services and cross‑border cash management create meaningful switching costs that preserve client stickiness. Buyers increasingly use competitive bids to push down fees and tighten covenants, but deep relationship coverage and tailored commercial lending remain a potent defensive moat.

Concentration in key metros

Clientele clusters in CA, NY, TX and MA where strong Asian American communities drive relationship banking, giving local competitors alternative providers and pricing leverage. Regional economic slowdowns in these metros amplify renegotiation pressure on fees and loan terms. East West’s expanding geographic and sector diversification—including commercial real estate, C&I and wealth channels—helps blunt concentrated buyer power.

Credit structure negotiation

Middle‑market borrowers increasingly press on covenants, collateral packages and amortization schedules; syndicated deals and private credit alternatives (private debt AUM > $1T in 2024) amplify borrower leverage. East West Bancorp’s US–China cross‑border franchise (headquartered in Pasadena) helps it command terms despite pressure, while disciplined underwriting curbs concessions.

- Middle‑market covenant and collateral pressure

- Private credit scale > $1T (2024) boosts borrower options

- EWBC cross‑border franchise secures pricing

- Disciplined underwriting limits concessions

Service expectations and responsiveness

Clients demand seamless FX, payments, and bilingual support across time zones; 64% of corporate treasurers in 2024 ranked digital responsiveness as a top selection factor, raising buyer leverage when service gaps occur and prompting rapid switching.

Superior turnaround and tailored solutions at East West blunt pure price competition, and ongoing CX investment reduces elasticity of demand, preserving fee margins.

- Service-driven switching increases buyer leverage

- Bilingual, 24/7 support cited by 64% (2024)

- Faster turnaround lowers price sensitivity

Clients pressure pricing; cross-border services and private credit sustain margins

Customers exert moderate-to-high bargaining power: rate-sensitive commercial and affluent clients (EWBC assets $53B in 2024) push deposit pricing and fee compression, while deep relationship services and US–China cross‑border capabilities preserve margins. Digital responsiveness (64% of treasurers in 2024) and private credit scale (> $1T in 2024) raise switching options, but tailored lending and underwriting limit concessions.

| Metric | 2024 |

|---|---|

| EWBC assets | $53B |

| Private credit AUM | > $1T |

| Treasure digital priority | 64% |

Preview Before You Purchase

East West Bancorp Porter's Five Forces Analysis

This Porter’s Five Forces analysis of East West Bancorp examines competitive rivalry, buyer and supplier power, threats of new entrants and substitutes, and strategic implications for margins and growth. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.