Easy Holdings Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

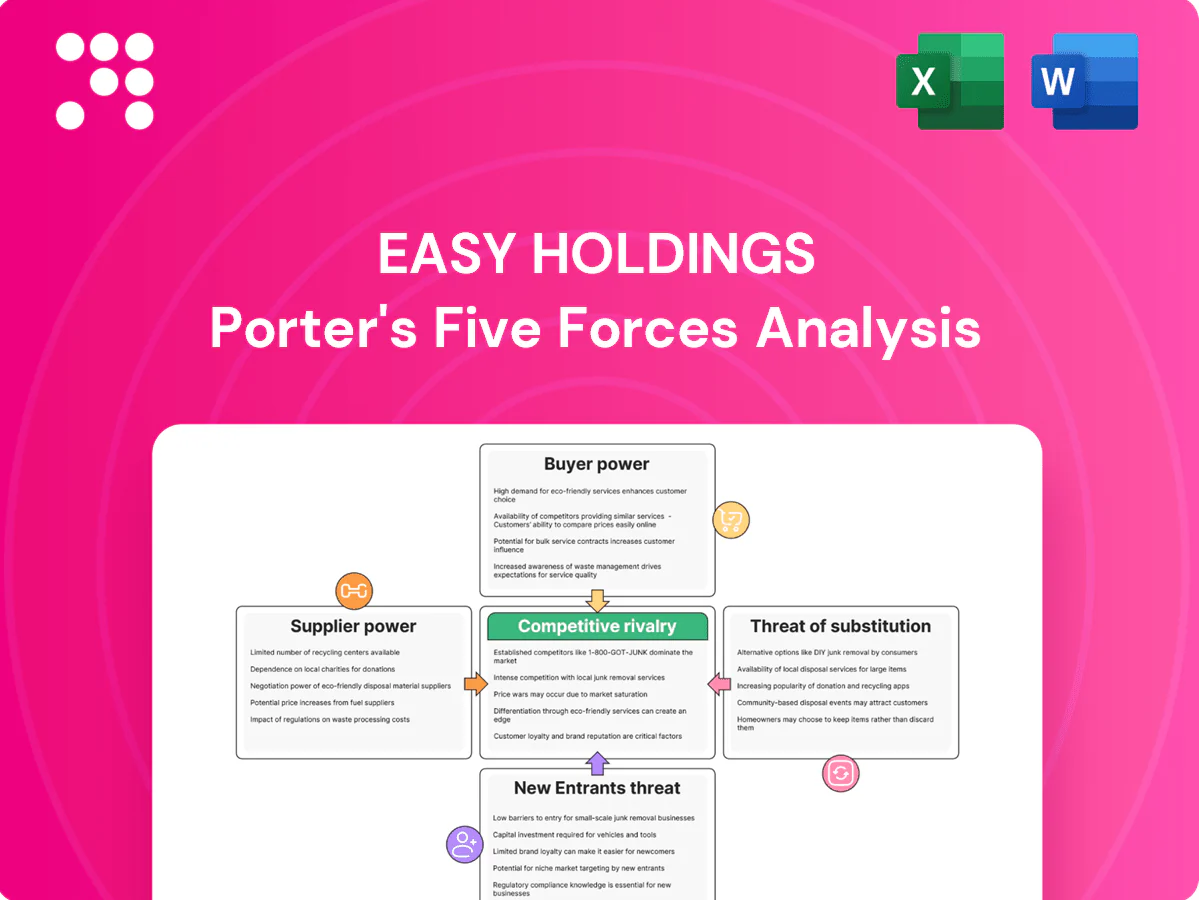

This snapshot outlines Easy Holdings’s competitive pressures across suppliers, buyers, rivals, new entrants and substitutes to help you gauge market intensity. The full Porter's Five Forces Analysis reveals force-by-force ratings, visuals, and strategic implications to inform investment or strategy decisions. Unlock the complete report for a consultant-grade breakdown you can use in presentations and planning.

Suppliers Bargaining Power

Concentrated agri-commodities

Core inputs (corn, soy, wheat) are funneled through a concentrated set of traders—top four firms account for roughly 60–70% of global trade—giving suppliers strong leverage; CBOT futures saw ~25–30% realized volatility in 2024, while FX swings (emerging market currency moves >10% YTD) drive cost pass-through or margin squeeze; hedging mitigates but cannot stop supply shocks; long-term offtakes cut price risk but reduce procurement flexibility.

Specialty additive licensors

Enzymes, probiotics, amino acids and premix IP for Easy Holdings are concentrated among specialty biotech firms such as Novozymes, DSM and Evonik, creating limited supplier choice in 2024. Proprietary formulations and published performance data drive switching frictions and support premium pricing and exclusivity clauses in co-development deals. Reliance on GRAS, EFSA and USDA trials/certifications further entrenches supplier power and lengthens qualification timelines.

Biosecurity and quality specs

Strict pathogen controls and nutrient specs limit supplier options for Easy Holdings, forcing certification and traceability investments; industry reports in 2024 estimate audits and batch testing raise supplier operating costs by roughly 3–7% annually. Audits, traceability and batch testing costs are frequently passed to buyers, and feed or meat recalls—typically costing $5–25M per incident—heighten supplier criticality. Dual-sourcing reduces single-supplier risk but increases procurement and coordination overhead, often by 10–15% in logistics and quality management.

Logistics and cold-chain dependencies

Logistics and cold-chain bottlenecks (grain inbound and reefer outbound) raise supplier leverage for Easy Holdings; port capacity limits and reefer availability tightened margins after 2023, with Drewry reporting the World Container Index averaged about $1,200 per 40ft in 2024 and reefer slot premiums of 10–20% over dry space.

- Grain logistics constrain input timing

- Port capacity limits outbound throughput

- Reefer shortages raise freight premia

- Local distributors secure better terms

- Forward warehousing reduces disruption risk but increases working capital

Sustainability requirements

- Deforestation-free soy: tighter supplier pool

- Animal welfare: premium-certified suppliers

- Carbon reporting: Scope 3 ~70% influence

- Premiums: 5–15% enforced

- Collaboration: price for access & brand protection

Suppliers hold strong leverage: top traders dominate, CBOT volatile, ESG premiums and Scope 3 risk

Suppliers wield high leverage: top-4 grain traders control ~60–70% of trade; CBOT vol ~25–30% in 2024; enzymes/probiotics concentrated (Novozymes, DSM, Evonik) limiting switching; audits add ~3–7% cost; WCI ≈ $1,200/40ft and reefer premium 10–20%; ESG certified inputs carry 5–15% premiums; Scope 3 ≈70% of emissions, boosting supplier power.

| Metric | 2024 Value |

|---|---|

| Top-4 grain share | 60–70% |

| CBOT vol | 25–30% |

| Audit cost uplift | 3–7% |

| WCI | $1,200/40ft |

| Reefer premium | 10–20% |

| ESG premium | 5–15% |

| Scope 3 | ~70% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Easy Holdings, identifying competitive pressures, supplier and buyer power, substitution risks, and entry barriers that shape its pricing and profitability; includes strategic implications, emerging threats, and opportunities to strengthen market position.

A one-sheet, customizable Porter's Five Forces template for Easy Holdings that maps competitive pressure with a radar chart, requires no macros, and slots directly into decks—so teams can quickly assess threats, test scenarios, and make strategic decisions without specialist help.

Customers Bargaining Power

Consolidated integrators

Large farms and agro-livestock integrators run centralized tenders and buy bulk volumes, extracting discounts typically in the 5–12% range (2024 industry data); their technical teams benchmark feed performance, enabling hard-nosed price and specification negotiations. Multi-year volume contracts, covering roughly 25–40% of B2B sales in 2024, exchange lower prices for demand stability. Losing a top account can cut plant utilization by 10–25%, materially affecting margins.

High price sensitivity

Feed represents 60–70% of livestock production costs, making buyers highly price elastic; even $5–10/ton differences or a 2–3% price gap commonly trigger switching or reformulation. Transparent CBOT/IEG commodity benchmarks anchor negotiations and compress margins. Customers will only pay premiums when suppliers prove measurable value — typical thresholds are ≥3–5% FCR improvement or ≥5–8% ADG gains.

Performance-based switching

Buyers monitor feed conversion ratios (typical broiler FCR ~1.5–1.8 in 2024), mortality (targets <5%) and health outcomes, and underperformance often triggers immediate trials with rivals. Data-sharing agreements can lock customers in by enabling benchmarking but increase supplier accountability and regulatory scrutiny. Warranty-like performance clauses, increasingly used in 2024, shift measurable risk back to the supplier and accelerate switching decisions.

Private label and co-dev

Private-label demand and custom premixes force Easy Holdings into 5–15% margin concessions as large retailers seek cost-plus deals; co-development ties buyers in but open-book costing commonly limits price upside. IP ownership clauses can shift long-term leverage to customers if not retained by Easy. High service levels and technical advisory (formulation, QC) become primary competitive differentiators.

- margin pressure: 5–15%

- co-dev: open-book caps pricing

- IP terms dictate leverage

- service/technical advisory = key edge

Processed meat channel power

- Listing fees and slotting pressure: concentrated buyers driving access and costs

- Private label ~12% (2024) compresses margins and triggers re-tenders

- Compliance costs (certs/audits) add ~1–2% to COGS

- Brand equity offsets pressure but needs 3–5% sales in marketing

Integrators secure 5–12%; multi-year B2B 25–40%

Large integrators extract 5–12% discounts via centralized tenders; multi-year contracts cover 25–40% of B2B sales (2024) and losing a top account can cut plant utilization 10–25%. Feed is 60–70% of production cost, so $5–10/ton or 2–3% gaps spur switching; private label ~12% (2024) and certifications add 1–2% COGS.

| Metric | 2024 Value |

|---|---|

| Bulk discount | 5–12% |

| Multi-year B2B share | 25–40% |

| Utilization risk | −10–25% |

| Feed cost share | 60–70% |

| Private label | ~12% |

| Certs add | 1–2% COGS |

Preview Before You Purchase

Easy Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Easy Holdings you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the professionally written, fully formatted file ready for download and use the moment you buy. You’re previewing the final version: precisely the same deliverable available to you instantly after payment.

Go Beyond the Preview—Access the Full Strategic Report

This snapshot outlines Easy Holdings’s competitive pressures across suppliers, buyers, rivals, new entrants and substitutes to help you gauge market intensity. The full Porter's Five Forces Analysis reveals force-by-force ratings, visuals, and strategic implications to inform investment or strategy decisions. Unlock the complete report for a consultant-grade breakdown you can use in presentations and planning.

Suppliers Bargaining Power

Concentrated agri-commodities

Core inputs (corn, soy, wheat) are funneled through a concentrated set of traders—top four firms account for roughly 60–70% of global trade—giving suppliers strong leverage; CBOT futures saw ~25–30% realized volatility in 2024, while FX swings (emerging market currency moves >10% YTD) drive cost pass-through or margin squeeze; hedging mitigates but cannot stop supply shocks; long-term offtakes cut price risk but reduce procurement flexibility.

Specialty additive licensors

Enzymes, probiotics, amino acids and premix IP for Easy Holdings are concentrated among specialty biotech firms such as Novozymes, DSM and Evonik, creating limited supplier choice in 2024. Proprietary formulations and published performance data drive switching frictions and support premium pricing and exclusivity clauses in co-development deals. Reliance on GRAS, EFSA and USDA trials/certifications further entrenches supplier power and lengthens qualification timelines.

Biosecurity and quality specs

Strict pathogen controls and nutrient specs limit supplier options for Easy Holdings, forcing certification and traceability investments; industry reports in 2024 estimate audits and batch testing raise supplier operating costs by roughly 3–7% annually. Audits, traceability and batch testing costs are frequently passed to buyers, and feed or meat recalls—typically costing $5–25M per incident—heighten supplier criticality. Dual-sourcing reduces single-supplier risk but increases procurement and coordination overhead, often by 10–15% in logistics and quality management.

Logistics and cold-chain dependencies

Logistics and cold-chain bottlenecks (grain inbound and reefer outbound) raise supplier leverage for Easy Holdings; port capacity limits and reefer availability tightened margins after 2023, with Drewry reporting the World Container Index averaged about $1,200 per 40ft in 2024 and reefer slot premiums of 10–20% over dry space.

- Grain logistics constrain input timing

- Port capacity limits outbound throughput

- Reefer shortages raise freight premia

- Local distributors secure better terms

- Forward warehousing reduces disruption risk but increases working capital

Sustainability requirements

- Deforestation-free soy: tighter supplier pool

- Animal welfare: premium-certified suppliers

- Carbon reporting: Scope 3 ~70% influence

- Premiums: 5–15% enforced

- Collaboration: price for access & brand protection

Suppliers hold strong leverage: top traders dominate, CBOT volatile, ESG premiums and Scope 3 risk

Suppliers wield high leverage: top-4 grain traders control ~60–70% of trade; CBOT vol ~25–30% in 2024; enzymes/probiotics concentrated (Novozymes, DSM, Evonik) limiting switching; audits add ~3–7% cost; WCI ≈ $1,200/40ft and reefer premium 10–20%; ESG certified inputs carry 5–15% premiums; Scope 3 ≈70% of emissions, boosting supplier power.

| Metric | 2024 Value |

|---|---|

| Top-4 grain share | 60–70% |

| CBOT vol | 25–30% |

| Audit cost uplift | 3–7% |

| WCI | $1,200/40ft |

| Reefer premium | 10–20% |

| ESG premium | 5–15% |

| Scope 3 | ~70% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Easy Holdings, identifying competitive pressures, supplier and buyer power, substitution risks, and entry barriers that shape its pricing and profitability; includes strategic implications, emerging threats, and opportunities to strengthen market position.

A one-sheet, customizable Porter's Five Forces template for Easy Holdings that maps competitive pressure with a radar chart, requires no macros, and slots directly into decks—so teams can quickly assess threats, test scenarios, and make strategic decisions without specialist help.

Customers Bargaining Power

Consolidated integrators

Large farms and agro-livestock integrators run centralized tenders and buy bulk volumes, extracting discounts typically in the 5–12% range (2024 industry data); their technical teams benchmark feed performance, enabling hard-nosed price and specification negotiations. Multi-year volume contracts, covering roughly 25–40% of B2B sales in 2024, exchange lower prices for demand stability. Losing a top account can cut plant utilization by 10–25%, materially affecting margins.

High price sensitivity

Feed represents 60–70% of livestock production costs, making buyers highly price elastic; even $5–10/ton differences or a 2–3% price gap commonly trigger switching or reformulation. Transparent CBOT/IEG commodity benchmarks anchor negotiations and compress margins. Customers will only pay premiums when suppliers prove measurable value — typical thresholds are ≥3–5% FCR improvement or ≥5–8% ADG gains.

Performance-based switching

Buyers monitor feed conversion ratios (typical broiler FCR ~1.5–1.8 in 2024), mortality (targets <5%) and health outcomes, and underperformance often triggers immediate trials with rivals. Data-sharing agreements can lock customers in by enabling benchmarking but increase supplier accountability and regulatory scrutiny. Warranty-like performance clauses, increasingly used in 2024, shift measurable risk back to the supplier and accelerate switching decisions.

Private label and co-dev

Private-label demand and custom premixes force Easy Holdings into 5–15% margin concessions as large retailers seek cost-plus deals; co-development ties buyers in but open-book costing commonly limits price upside. IP ownership clauses can shift long-term leverage to customers if not retained by Easy. High service levels and technical advisory (formulation, QC) become primary competitive differentiators.

- margin pressure: 5–15%

- co-dev: open-book caps pricing

- IP terms dictate leverage

- service/technical advisory = key edge

Processed meat channel power

- Listing fees and slotting pressure: concentrated buyers driving access and costs

- Private label ~12% (2024) compresses margins and triggers re-tenders

- Compliance costs (certs/audits) add ~1–2% to COGS

- Brand equity offsets pressure but needs 3–5% sales in marketing

Integrators secure 5–12%; multi-year B2B 25–40%

Large integrators extract 5–12% discounts via centralized tenders; multi-year contracts cover 25–40% of B2B sales (2024) and losing a top account can cut plant utilization 10–25%. Feed is 60–70% of production cost, so $5–10/ton or 2–3% gaps spur switching; private label ~12% (2024) and certifications add 1–2% COGS.

| Metric | 2024 Value |

|---|---|

| Bulk discount | 5–12% |

| Multi-year B2B share | 25–40% |

| Utilization risk | −10–25% |

| Feed cost share | 60–70% |

| Private label | ~12% |

| Certs add | 1–2% COGS |

Preview Before You Purchase

Easy Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Easy Holdings you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the professionally written, fully formatted file ready for download and use the moment you buy. You’re previewing the final version: precisely the same deliverable available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

This snapshot outlines Easy Holdings’s competitive pressures across suppliers, buyers, rivals, new entrants and substitutes to help you gauge market intensity. The full Porter's Five Forces Analysis reveals force-by-force ratings, visuals, and strategic implications to inform investment or strategy decisions. Unlock the complete report for a consultant-grade breakdown you can use in presentations and planning.

Suppliers Bargaining Power

Concentrated agri-commodities

Core inputs (corn, soy, wheat) are funneled through a concentrated set of traders—top four firms account for roughly 60–70% of global trade—giving suppliers strong leverage; CBOT futures saw ~25–30% realized volatility in 2024, while FX swings (emerging market currency moves >10% YTD) drive cost pass-through or margin squeeze; hedging mitigates but cannot stop supply shocks; long-term offtakes cut price risk but reduce procurement flexibility.

Specialty additive licensors

Enzymes, probiotics, amino acids and premix IP for Easy Holdings are concentrated among specialty biotech firms such as Novozymes, DSM and Evonik, creating limited supplier choice in 2024. Proprietary formulations and published performance data drive switching frictions and support premium pricing and exclusivity clauses in co-development deals. Reliance on GRAS, EFSA and USDA trials/certifications further entrenches supplier power and lengthens qualification timelines.

Biosecurity and quality specs

Strict pathogen controls and nutrient specs limit supplier options for Easy Holdings, forcing certification and traceability investments; industry reports in 2024 estimate audits and batch testing raise supplier operating costs by roughly 3–7% annually. Audits, traceability and batch testing costs are frequently passed to buyers, and feed or meat recalls—typically costing $5–25M per incident—heighten supplier criticality. Dual-sourcing reduces single-supplier risk but increases procurement and coordination overhead, often by 10–15% in logistics and quality management.

Logistics and cold-chain dependencies

Logistics and cold-chain bottlenecks (grain inbound and reefer outbound) raise supplier leverage for Easy Holdings; port capacity limits and reefer availability tightened margins after 2023, with Drewry reporting the World Container Index averaged about $1,200 per 40ft in 2024 and reefer slot premiums of 10–20% over dry space.

- Grain logistics constrain input timing

- Port capacity limits outbound throughput

- Reefer shortages raise freight premia

- Local distributors secure better terms

- Forward warehousing reduces disruption risk but increases working capital

Sustainability requirements

- Deforestation-free soy: tighter supplier pool

- Animal welfare: premium-certified suppliers

- Carbon reporting: Scope 3 ~70% influence

- Premiums: 5–15% enforced

- Collaboration: price for access & brand protection

Suppliers hold strong leverage: top traders dominate, CBOT volatile, ESG premiums and Scope 3 risk

Suppliers wield high leverage: top-4 grain traders control ~60–70% of trade; CBOT vol ~25–30% in 2024; enzymes/probiotics concentrated (Novozymes, DSM, Evonik) limiting switching; audits add ~3–7% cost; WCI ≈ $1,200/40ft and reefer premium 10–20%; ESG certified inputs carry 5–15% premiums; Scope 3 ≈70% of emissions, boosting supplier power.

| Metric | 2024 Value |

|---|---|

| Top-4 grain share | 60–70% |

| CBOT vol | 25–30% |

| Audit cost uplift | 3–7% |

| WCI | $1,200/40ft |

| Reefer premium | 10–20% |

| ESG premium | 5–15% |

| Scope 3 | ~70% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Easy Holdings, identifying competitive pressures, supplier and buyer power, substitution risks, and entry barriers that shape its pricing and profitability; includes strategic implications, emerging threats, and opportunities to strengthen market position.

A one-sheet, customizable Porter's Five Forces template for Easy Holdings that maps competitive pressure with a radar chart, requires no macros, and slots directly into decks—so teams can quickly assess threats, test scenarios, and make strategic decisions without specialist help.

Customers Bargaining Power

Consolidated integrators

Large farms and agro-livestock integrators run centralized tenders and buy bulk volumes, extracting discounts typically in the 5–12% range (2024 industry data); their technical teams benchmark feed performance, enabling hard-nosed price and specification negotiations. Multi-year volume contracts, covering roughly 25–40% of B2B sales in 2024, exchange lower prices for demand stability. Losing a top account can cut plant utilization by 10–25%, materially affecting margins.

High price sensitivity

Feed represents 60–70% of livestock production costs, making buyers highly price elastic; even $5–10/ton differences or a 2–3% price gap commonly trigger switching or reformulation. Transparent CBOT/IEG commodity benchmarks anchor negotiations and compress margins. Customers will only pay premiums when suppliers prove measurable value — typical thresholds are ≥3–5% FCR improvement or ≥5–8% ADG gains.

Performance-based switching

Buyers monitor feed conversion ratios (typical broiler FCR ~1.5–1.8 in 2024), mortality (targets <5%) and health outcomes, and underperformance often triggers immediate trials with rivals. Data-sharing agreements can lock customers in by enabling benchmarking but increase supplier accountability and regulatory scrutiny. Warranty-like performance clauses, increasingly used in 2024, shift measurable risk back to the supplier and accelerate switching decisions.

Private label and co-dev

Private-label demand and custom premixes force Easy Holdings into 5–15% margin concessions as large retailers seek cost-plus deals; co-development ties buyers in but open-book costing commonly limits price upside. IP ownership clauses can shift long-term leverage to customers if not retained by Easy. High service levels and technical advisory (formulation, QC) become primary competitive differentiators.

- margin pressure: 5–15%

- co-dev: open-book caps pricing

- IP terms dictate leverage

- service/technical advisory = key edge

Processed meat channel power

- Listing fees and slotting pressure: concentrated buyers driving access and costs

- Private label ~12% (2024) compresses margins and triggers re-tenders

- Compliance costs (certs/audits) add ~1–2% to COGS

- Brand equity offsets pressure but needs 3–5% sales in marketing

Integrators secure 5–12%; multi-year B2B 25–40%

Large integrators extract 5–12% discounts via centralized tenders; multi-year contracts cover 25–40% of B2B sales (2024) and losing a top account can cut plant utilization 10–25%. Feed is 60–70% of production cost, so $5–10/ton or 2–3% gaps spur switching; private label ~12% (2024) and certifications add 1–2% COGS.

| Metric | 2024 Value |

|---|---|

| Bulk discount | 5–12% |

| Multi-year B2B share | 25–40% |

| Utilization risk | −10–25% |

| Feed cost share | 60–70% |

| Private label | ~12% |

| Certs add | 1–2% COGS |

Preview Before You Purchase

Easy Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Easy Holdings you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the professionally written, fully formatted file ready for download and use the moment you buy. You’re previewing the final version: precisely the same deliverable available to you instantly after payment.