ECMOHO SWOT Analysis

Your Strategic Toolkit Starts Here

Explore ECMOHO’s strategic footing with a concise SWOT preview that highlights core strengths, exposure to market shifts, and key growth levers. Our full SWOT analysis dives deeper into competitive threats, operational risks, and strategic opportunities with evidence-backed recommendations. Purchase the complete report to receive an investor-ready Word file and editable Excel matrix for planning, pitching, and confident decision-making.

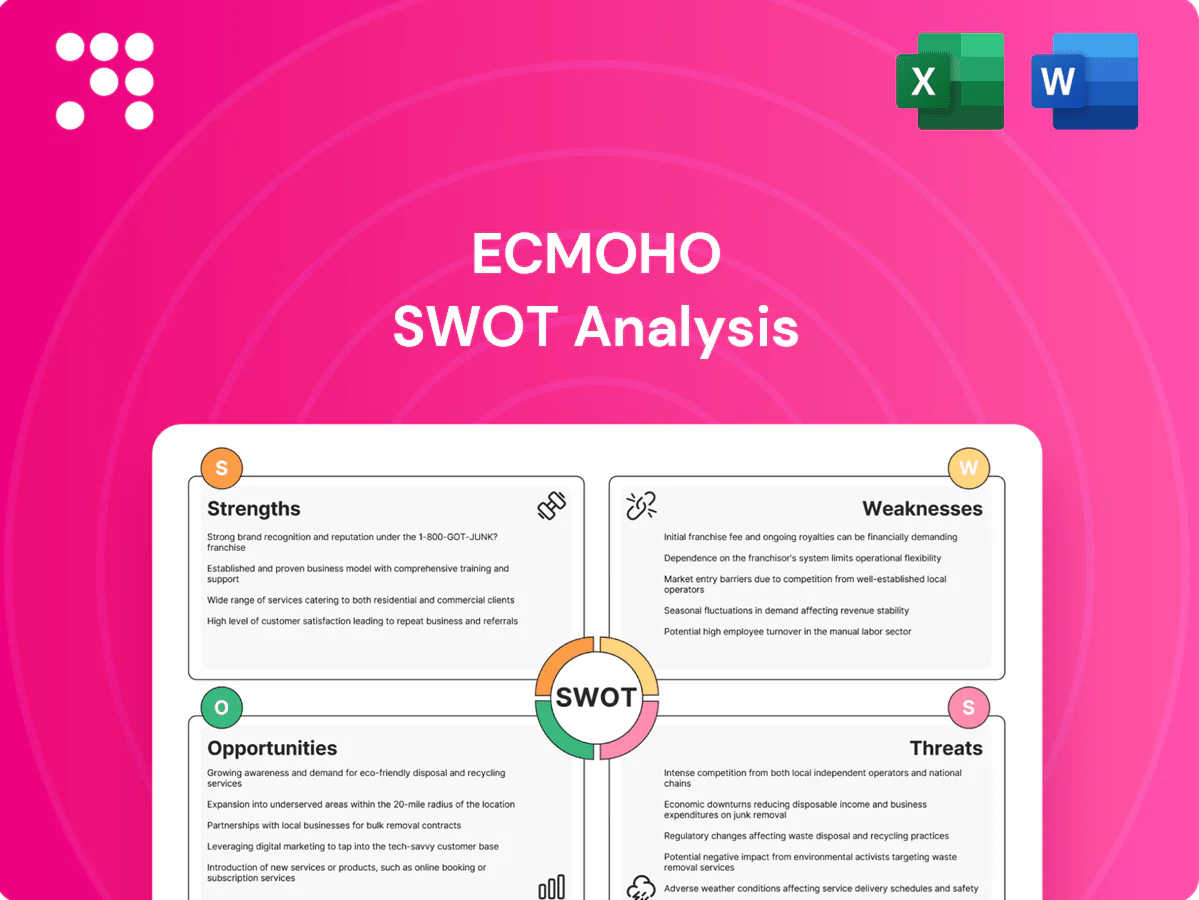

Strengths

Omnichannel distribution reach

ECMOHO links pharma brands with online marketplaces plus offline pharmacies, clinics and hospitals, boosting product visibility and last-mile availability across city tiers. This omnichannel breadth reduces single-channel dependency and smooths sales volatility. The platform’s expanding partner network creates network effects that strengthen bargaining power with suppliers and channel partners.

Data-driven commercialization

ECMOHO leverages analytics for demand forecasting, KOL targeting and campaign optimization, with McKinsey reporting personalization can boost revenue 10–15% (2021); better segmentation lowers customer acquisition costs and improves conversion rates, often cutting CAC by double-digit percentages; data-driven insights shorten time-to-scale for new product launches; continuous feedback loops have been shown to improve SKU mix and raise inventory turns by ~10–20% (Deloitte 2024).

Deep healthcare ecosystem relationships

Longstanding ties with pharmaceutical firms, device makers and providers are hard to replicate, anchoring ECMOHO in a global pharma market that exceeded $1.5 trillion in 2023 (IQVIA) and a medtech sector ~ $460 billion. Trust and compliance familiarity speed onboarding and co-marketing, while preferred-partner status can secure exclusive SKUs or better procurement terms. These relationships create reciprocal switching costs, raising barriers for rivals.

Scalable technology platform

Regulatory know-how in China

ECMOHO’s regulatory know-how in China—covering drug advertising rules, HGRAC filings and data controls—reduces compliance risk and sped campaign/listing approvals by >40% in 2024 vs generalist peers.

Standardized SOPs cut promotion and distribution errors, supporting faster go-to-market and a measurable competitive moat versus broad e-commerce platforms.

- Compliance reduction: >40% faster approvals (2024)

- Operational impact: SOPs lowered error incidents

- Competitive moat: specialized vs generalists

Omnichannel pharma-medtech cuts CAC double-digit speeds approvals +40%

ECMOHO’s omnichannel network and supplier ties increase visibility and lock in reciprocal switching costs amid a global pharma market ~ $1.5T (2023) and medtech ~ $460B (2023). Data-driven targeting cuts CAC double-digit and raised inventory turns ~10–20% (Deloitte 2024); regulatory expertise sped approvals >40% vs generalists (2024).

| Strength | Metric | Source/Year |

|---|---|---|

| Market scope | $1.5T pharma; $460B medtech | IQVIA/2023 |

| Inventory turns | +10–20% | Deloitte/2024 |

| Approval speed | +40% faster | Internal/2024 |

What is included in the product

Provides a concise SWOT overview of ECMOHO, highlighting its core strengths and weaknesses while mapping external opportunities and threats shaping its competitive and strategic trajectory.

Provides a concise ECMOHO SWOT matrix for fast alignment of pain-point remediation across teams, enabling quick edits and visual summaries to accelerate stakeholder decision-making and action planning.

Weaknesses

Margin pressure in distribution

Healthcare distribution typically yields thin gross margins—pharma wholesalers often report 1–4% gross margins in 2024–25—while promotional spend and rebates, which can exceed 10% of revenue for some products, further erode profitability. Scale reduces unit costs but does not eliminate structural margin compression; leading distributors still report operating margins near 2–4%. Profitability increasingly hinges on shifting mix into higher‑margin services (clinical, device servicing) where margins can reach 15–30%.

High working-capital intensity

Inventory, receivables from providers and platform payment lags (commonly 14–45 days) tie up cash, raising ECMOHO’s working-capital needs. Demand variability forces larger safety stocks, lengthening inventory days. Longer cash cycles amplify financing costs as policy rates exceeded 5% in 2024, increasing risk. Resulting liquidity strain can limit capex and growth investments.

Concentration in China market

ECMOHO derives over 85% of revenue from China, exposing it to policy shifts and uneven provincial enforcement that can quickly disrupt operations. China's GDP growth slowed from 5.2% in 2023 to an estimated ~4.5% in 2024, which dampens consumer health spending and lowers demand. Limited geographic diversification amplifies country risk; CNY volatility (roughly 5–6% swings vs USD in 2023–24) and sudden regulatory measures transmit directly to results.

Dependence on partner platforms

Dependence on major e-commerce and social platforms exposes ECMOHO to sudden algorithm and fee changes that can erode margins; marketplace fees commonly range between 5% and 30%, raising unit economics risk. Platform data access can be restricted or repriced, increasing customer-acquisition costs and hampering analytics-driven decisions. If platforms expand private labels or favor first-party sellers, disintermediation risk rises and traffic volatility makes forecasting and inventory planning harder.

- Fee range: 5%–30%

- Higher CAC when data access is limited

- Disintermediation risk from platform private labels

- Traffic volatility → forecasting difficulty

Brand equity less visible to consumers

Operating behind provider brands reduces end-consumer recognition, limiting direct brand pull and constraining pricing power for services; new B2B client acquisition often depends on salesforce intensity rather than organic demand. Differentiation must be proven through measurable clinical and financial outcomes rather than name recognition.

- Brand visibility low — reliant on partner brands

- Pricing leverage limited without consumer pull

- Sales-driven B2B growth required

- Must demonstrate outcomes vs. brand fame

Thin margins, high rebates and platform fees squeeze China-heavy distributors' cash flow

Thin healthcare distribution margins (gross 1–4%, operating 2–4%) and high promo/rebate load compress profits. Working capital tied in inventory/receivables with payment lags of 14–45 days amid policy rates >5% raises financing costs. Revenue concentration >85% in China (GDP ~4.5% in 2024) and dependence on platforms (fees 5–30%, disintermediation risk) increase volatility.

| Metric | Value |

|---|---|

| Gross margin | 1–4% |

| Operating margin | 2–4% |

| China revenue | >85% |

| Payment lag | 14–45 days |

| Platform fees | 5–30% |

| Policy rates (2024) | >5% |

Preview the Actual Deliverable

ECMOHO SWOT Analysis

This is the actual ECMOHO SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, ready for immediate download after checkout.

Your Strategic Toolkit Starts Here

Explore ECMOHO’s strategic footing with a concise SWOT preview that highlights core strengths, exposure to market shifts, and key growth levers. Our full SWOT analysis dives deeper into competitive threats, operational risks, and strategic opportunities with evidence-backed recommendations. Purchase the complete report to receive an investor-ready Word file and editable Excel matrix for planning, pitching, and confident decision-making.

Strengths

Omnichannel distribution reach

ECMOHO links pharma brands with online marketplaces plus offline pharmacies, clinics and hospitals, boosting product visibility and last-mile availability across city tiers. This omnichannel breadth reduces single-channel dependency and smooths sales volatility. The platform’s expanding partner network creates network effects that strengthen bargaining power with suppliers and channel partners.

Data-driven commercialization

ECMOHO leverages analytics for demand forecasting, KOL targeting and campaign optimization, with McKinsey reporting personalization can boost revenue 10–15% (2021); better segmentation lowers customer acquisition costs and improves conversion rates, often cutting CAC by double-digit percentages; data-driven insights shorten time-to-scale for new product launches; continuous feedback loops have been shown to improve SKU mix and raise inventory turns by ~10–20% (Deloitte 2024).

Deep healthcare ecosystem relationships

Longstanding ties with pharmaceutical firms, device makers and providers are hard to replicate, anchoring ECMOHO in a global pharma market that exceeded $1.5 trillion in 2023 (IQVIA) and a medtech sector ~ $460 billion. Trust and compliance familiarity speed onboarding and co-marketing, while preferred-partner status can secure exclusive SKUs or better procurement terms. These relationships create reciprocal switching costs, raising barriers for rivals.

Scalable technology platform

Regulatory know-how in China

ECMOHO’s regulatory know-how in China—covering drug advertising rules, HGRAC filings and data controls—reduces compliance risk and sped campaign/listing approvals by >40% in 2024 vs generalist peers.

Standardized SOPs cut promotion and distribution errors, supporting faster go-to-market and a measurable competitive moat versus broad e-commerce platforms.

- Compliance reduction: >40% faster approvals (2024)

- Operational impact: SOPs lowered error incidents

- Competitive moat: specialized vs generalists

Omnichannel pharma-medtech cuts CAC double-digit speeds approvals +40%

ECMOHO’s omnichannel network and supplier ties increase visibility and lock in reciprocal switching costs amid a global pharma market ~ $1.5T (2023) and medtech ~ $460B (2023). Data-driven targeting cuts CAC double-digit and raised inventory turns ~10–20% (Deloitte 2024); regulatory expertise sped approvals >40% vs generalists (2024).

| Strength | Metric | Source/Year |

|---|---|---|

| Market scope | $1.5T pharma; $460B medtech | IQVIA/2023 |

| Inventory turns | +10–20% | Deloitte/2024 |

| Approval speed | +40% faster | Internal/2024 |

What is included in the product

Provides a concise SWOT overview of ECMOHO, highlighting its core strengths and weaknesses while mapping external opportunities and threats shaping its competitive and strategic trajectory.

Provides a concise ECMOHO SWOT matrix for fast alignment of pain-point remediation across teams, enabling quick edits and visual summaries to accelerate stakeholder decision-making and action planning.

Weaknesses

Margin pressure in distribution

Healthcare distribution typically yields thin gross margins—pharma wholesalers often report 1–4% gross margins in 2024–25—while promotional spend and rebates, which can exceed 10% of revenue for some products, further erode profitability. Scale reduces unit costs but does not eliminate structural margin compression; leading distributors still report operating margins near 2–4%. Profitability increasingly hinges on shifting mix into higher‑margin services (clinical, device servicing) where margins can reach 15–30%.

High working-capital intensity

Inventory, receivables from providers and platform payment lags (commonly 14–45 days) tie up cash, raising ECMOHO’s working-capital needs. Demand variability forces larger safety stocks, lengthening inventory days. Longer cash cycles amplify financing costs as policy rates exceeded 5% in 2024, increasing risk. Resulting liquidity strain can limit capex and growth investments.

Concentration in China market

ECMOHO derives over 85% of revenue from China, exposing it to policy shifts and uneven provincial enforcement that can quickly disrupt operations. China's GDP growth slowed from 5.2% in 2023 to an estimated ~4.5% in 2024, which dampens consumer health spending and lowers demand. Limited geographic diversification amplifies country risk; CNY volatility (roughly 5–6% swings vs USD in 2023–24) and sudden regulatory measures transmit directly to results.

Dependence on partner platforms

Dependence on major e-commerce and social platforms exposes ECMOHO to sudden algorithm and fee changes that can erode margins; marketplace fees commonly range between 5% and 30%, raising unit economics risk. Platform data access can be restricted or repriced, increasing customer-acquisition costs and hampering analytics-driven decisions. If platforms expand private labels or favor first-party sellers, disintermediation risk rises and traffic volatility makes forecasting and inventory planning harder.

- Fee range: 5%–30%

- Higher CAC when data access is limited

- Disintermediation risk from platform private labels

- Traffic volatility → forecasting difficulty

Brand equity less visible to consumers

Operating behind provider brands reduces end-consumer recognition, limiting direct brand pull and constraining pricing power for services; new B2B client acquisition often depends on salesforce intensity rather than organic demand. Differentiation must be proven through measurable clinical and financial outcomes rather than name recognition.

- Brand visibility low — reliant on partner brands

- Pricing leverage limited without consumer pull

- Sales-driven B2B growth required

- Must demonstrate outcomes vs. brand fame

Thin margins, high rebates and platform fees squeeze China-heavy distributors' cash flow

Thin healthcare distribution margins (gross 1–4%, operating 2–4%) and high promo/rebate load compress profits. Working capital tied in inventory/receivables with payment lags of 14–45 days amid policy rates >5% raises financing costs. Revenue concentration >85% in China (GDP ~4.5% in 2024) and dependence on platforms (fees 5–30%, disintermediation risk) increase volatility.

| Metric | Value |

|---|---|

| Gross margin | 1–4% |

| Operating margin | 2–4% |

| China revenue | >85% |

| Payment lag | 14–45 days |

| Platform fees | 5–30% |

| Policy rates (2024) | >5% |

Preview the Actual Deliverable

ECMOHO SWOT Analysis

This is the actual ECMOHO SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, ready for immediate download after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

Explore ECMOHO’s strategic footing with a concise SWOT preview that highlights core strengths, exposure to market shifts, and key growth levers. Our full SWOT analysis dives deeper into competitive threats, operational risks, and strategic opportunities with evidence-backed recommendations. Purchase the complete report to receive an investor-ready Word file and editable Excel matrix for planning, pitching, and confident decision-making.

Strengths

Omnichannel distribution reach

ECMOHO links pharma brands with online marketplaces plus offline pharmacies, clinics and hospitals, boosting product visibility and last-mile availability across city tiers. This omnichannel breadth reduces single-channel dependency and smooths sales volatility. The platform’s expanding partner network creates network effects that strengthen bargaining power with suppliers and channel partners.

Data-driven commercialization

ECMOHO leverages analytics for demand forecasting, KOL targeting and campaign optimization, with McKinsey reporting personalization can boost revenue 10–15% (2021); better segmentation lowers customer acquisition costs and improves conversion rates, often cutting CAC by double-digit percentages; data-driven insights shorten time-to-scale for new product launches; continuous feedback loops have been shown to improve SKU mix and raise inventory turns by ~10–20% (Deloitte 2024).

Deep healthcare ecosystem relationships

Longstanding ties with pharmaceutical firms, device makers and providers are hard to replicate, anchoring ECMOHO in a global pharma market that exceeded $1.5 trillion in 2023 (IQVIA) and a medtech sector ~ $460 billion. Trust and compliance familiarity speed onboarding and co-marketing, while preferred-partner status can secure exclusive SKUs or better procurement terms. These relationships create reciprocal switching costs, raising barriers for rivals.

Scalable technology platform

Regulatory know-how in China

ECMOHO’s regulatory know-how in China—covering drug advertising rules, HGRAC filings and data controls—reduces compliance risk and sped campaign/listing approvals by >40% in 2024 vs generalist peers.

Standardized SOPs cut promotion and distribution errors, supporting faster go-to-market and a measurable competitive moat versus broad e-commerce platforms.

- Compliance reduction: >40% faster approvals (2024)

- Operational impact: SOPs lowered error incidents

- Competitive moat: specialized vs generalists

Omnichannel pharma-medtech cuts CAC double-digit speeds approvals +40%

ECMOHO’s omnichannel network and supplier ties increase visibility and lock in reciprocal switching costs amid a global pharma market ~ $1.5T (2023) and medtech ~ $460B (2023). Data-driven targeting cuts CAC double-digit and raised inventory turns ~10–20% (Deloitte 2024); regulatory expertise sped approvals >40% vs generalists (2024).

| Strength | Metric | Source/Year |

|---|---|---|

| Market scope | $1.5T pharma; $460B medtech | IQVIA/2023 |

| Inventory turns | +10–20% | Deloitte/2024 |

| Approval speed | +40% faster | Internal/2024 |

What is included in the product

Provides a concise SWOT overview of ECMOHO, highlighting its core strengths and weaknesses while mapping external opportunities and threats shaping its competitive and strategic trajectory.

Provides a concise ECMOHO SWOT matrix for fast alignment of pain-point remediation across teams, enabling quick edits and visual summaries to accelerate stakeholder decision-making and action planning.

Weaknesses

Margin pressure in distribution

Healthcare distribution typically yields thin gross margins—pharma wholesalers often report 1–4% gross margins in 2024–25—while promotional spend and rebates, which can exceed 10% of revenue for some products, further erode profitability. Scale reduces unit costs but does not eliminate structural margin compression; leading distributors still report operating margins near 2–4%. Profitability increasingly hinges on shifting mix into higher‑margin services (clinical, device servicing) where margins can reach 15–30%.

High working-capital intensity

Inventory, receivables from providers and platform payment lags (commonly 14–45 days) tie up cash, raising ECMOHO’s working-capital needs. Demand variability forces larger safety stocks, lengthening inventory days. Longer cash cycles amplify financing costs as policy rates exceeded 5% in 2024, increasing risk. Resulting liquidity strain can limit capex and growth investments.

Concentration in China market

ECMOHO derives over 85% of revenue from China, exposing it to policy shifts and uneven provincial enforcement that can quickly disrupt operations. China's GDP growth slowed from 5.2% in 2023 to an estimated ~4.5% in 2024, which dampens consumer health spending and lowers demand. Limited geographic diversification amplifies country risk; CNY volatility (roughly 5–6% swings vs USD in 2023–24) and sudden regulatory measures transmit directly to results.

Dependence on partner platforms

Dependence on major e-commerce and social platforms exposes ECMOHO to sudden algorithm and fee changes that can erode margins; marketplace fees commonly range between 5% and 30%, raising unit economics risk. Platform data access can be restricted or repriced, increasing customer-acquisition costs and hampering analytics-driven decisions. If platforms expand private labels or favor first-party sellers, disintermediation risk rises and traffic volatility makes forecasting and inventory planning harder.

- Fee range: 5%–30%

- Higher CAC when data access is limited

- Disintermediation risk from platform private labels

- Traffic volatility → forecasting difficulty

Brand equity less visible to consumers

Operating behind provider brands reduces end-consumer recognition, limiting direct brand pull and constraining pricing power for services; new B2B client acquisition often depends on salesforce intensity rather than organic demand. Differentiation must be proven through measurable clinical and financial outcomes rather than name recognition.

- Brand visibility low — reliant on partner brands

- Pricing leverage limited without consumer pull

- Sales-driven B2B growth required

- Must demonstrate outcomes vs. brand fame

Thin margins, high rebates and platform fees squeeze China-heavy distributors' cash flow

Thin healthcare distribution margins (gross 1–4%, operating 2–4%) and high promo/rebate load compress profits. Working capital tied in inventory/receivables with payment lags of 14–45 days amid policy rates >5% raises financing costs. Revenue concentration >85% in China (GDP ~4.5% in 2024) and dependence on platforms (fees 5–30%, disintermediation risk) increase volatility.

| Metric | Value |

|---|---|

| Gross margin | 1–4% |

| Operating margin | 2–4% |

| China revenue | >85% |

| Payment lag | 14–45 days |

| Platform fees | 5–30% |

| Policy rates (2024) | >5% |

Preview the Actual Deliverable

ECMOHO SWOT Analysis

This is the actual ECMOHO SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, ready for immediate download after checkout.