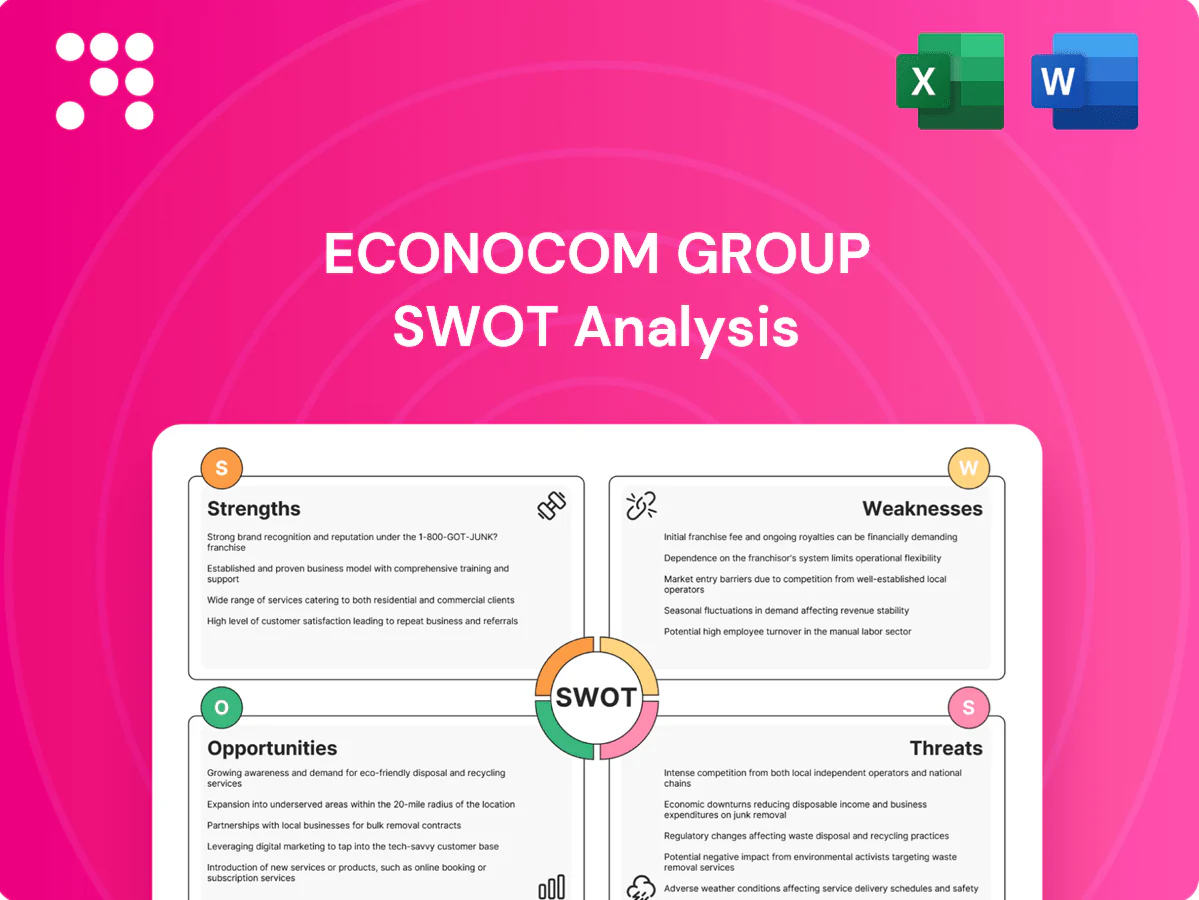

Econocom Group SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Econocom’s hybrid IT and financing model shows clear strengths in digital services and strategic partnerships, but faces margin pressure and competitive disruption; our concise SWOT highlights key risks and growth levers. Want the full, research-backed analysis with editable Word and Excel deliverables to support strategy or investment decisions? Purchase the complete SWOT to unlock detailed findings, financial context, and actionable recommendations.

Strengths

End-to-end digital lifecycle

Combining consulting, sourcing, integration and managed services gives clients one accountable partner, reducing vendor sprawl and shortening decision cycles. Econocom, listed on Euronext and operating in 19 countries, reported roughly €3.2bn revenue in 2023, and multi-year engagements deepen stickiness while enabling cross-sell and upsell across the digital stack.

Flexible tech financing

Specialization in flexible financing and as-a-service models lets Econocom align client spend with outcomes, overcoming capex constraints and speeding project approvals across its footprint in 18 countries and ~9,800 employees.

These solutions contributed to group revenues of about €2.6bn in 2023 and generate recurring financing income that smooths revenue volatility.

The model differentiates Econocom from pure integrators or resellers by bundling services, hardware and financing into outcome-based contracts.

Enterprise client focus

Serving large organizations enables bigger deal sizes and programmatic rollouts, leveraging Econocoms enterprise references to win complex transformation mandates. Its governance and compliance capabilities align with corporate procurement and regulatory needs, increasing retention and switching costs. Econocom is listed on Euronext Paris and employs over 10,000 people across 20 countries, reinforcing global delivery capacity.

Vendor-agnostic sourcing

Vendor-agnostic sourcing lets Econocom assemble best-fit hardware, software and cloud stacks, aligning solutions to customer needs while leveraging expertise across vendors. This approach boosts negotiating leverage on pricing and SLAs and reduces client lock-in, supporting faster technology refresh cycles; 92% of enterprises used multi-cloud in 2024 (Flexera) which validates demand for flexible sourcing.

- Best-fit solutions

- Stronger pricing & SLA leverage

- Lower vendor lock-in

- Faster refresh cycles

Managed services depth

Managed services depth lets Econocom extend value beyond deployment through lifecycle support, converting installs into ongoing revenue streams and stabilizing margins; similar IT services peers report recurring services often exceeding 40-50% of revenue. Operational data from service contracts drives continuous improvement and upsell signals, strengthening client retention and increasing renewal rates. This recurring model supports predictable cash flows and long-term relationships.

- Lifecycle support: prolonged value capture

- Recurring revenue: stabilizes cash flows

- Service data: informs continuous improvement

- Client retention: boosts renewals

Integrated consulting-to-managed-services drives recurring revenue and €2.6bn scale

Integrated consulting-to-managed-services model, vendor-agnostic sourcing and flexible financing drive high stickiness, larger enterprise deals and recurring revenue, supported by global delivery and compliance capabilities.

| Metric | Value |

|---|---|

| 2023 revenue | €2.6bn |

| Employees | ~10,000 |

| Countries | ~20 |

| Multi-cloud adoption (Flexera 2024) | 92% |

What is included in the product

Provides a concise SWOT analysis of Econocom Group, highlighting internal strengths and weaknesses alongside market opportunities and external threats to inform strategic decisions.

Provides a concise SWOT matrix for fast, visual strategy alignment for Econocom Group, enabling executives to pinpoint digital-transformation strengths and vendor risks quickly while streamlining stakeholder decision-making.

Weaknesses

Margin pressure in reselling

IT sourcing and equipment resale are low-margin and highly competitive: industry resale gross margins typically range 3–7%, putting pressure on Econocom’s hardware lines.

Frequent discounting in large public and corporate tenders can materially erode profitability, sometimes halving transactional margins.

True differentiation must come from expanded services and embedded financing; shifting revenue mix toward managed services and leasing is required to protect gross margins.

Execution complexity

Coordinating consulting, delivery, financing and managed services raises operational risk as interdependent workflows increase points of failure. Multinational rollouts intensify program management and governance demands, stretching local compliance and SLAs. Delays can cascade into penalties or customer churn—McKinsey estimates roughly 70% of digital transformations underdeliver—and scaling reliably requires sustained investment in processes and tooling.

Capital intensity of financing

Offering financing ties up Econocoms balance-sheet capacity, with leasing and asset finance comprising the bulk of on-balance exposures and limiting debt headroom. Rising central-bank rates — ECB policy around 4% in 2024–25 — have pushed funding costs and increased RWAs, squeezing margins. Credit risk and residual-value volatility demand strict underwriting and remarketing controls. This capital intensity can reduce agility versus asset-light competitors.

Dependence on enterprise cycles

Dependence on enterprise cycles means budget freezes or elongated approval processes at large clients frequently delay Econocom’s revenue recognition, pushing payments and shifting revenue into later quarters.

Project-based peaks and troughs make capacity planning harder, forcing temporary staffing swings and higher marginal costs during demand spikes.

Economic slowdowns disproportionately reduce transformation spend, leaving revenue visibility uneven absent a strong, contracted backlog.

- Delayed approvals -> shifted revenue recognition

- Peaks/troughs -> capacity and cost volatility

- Slowdowns hit transformation budgets hardest

- Weak backlog -> low revenue visibility

Talent and skills constraints

Talent and skills constraints weaken Econocom as demand for cloud, cybersecurity and data specialists outstrips supply; ISC2 reported a 3.4 million global cybersecurity workforce gap in 2023. Attrition risks cause knowledge loss and delivery slippage, while rising wages compress service margins. Continuous upskilling programs are necessary but add significant cost pressure.

- Demand-supply gap: ISC2 3.4M (2023)

- Attrition → delivery slippage

- Wage inflation compresses margins

- High-cost continuous upskilling

Low-margin hardware (3-7%) and ECB ~4% squeeze profits; services must grow

Low-margin hardware resale (industry gross margins 3–7%) and frequent tender discounting compress profits; services/financing mix must grow to protect margins. Financing ties up balance-sheet while ECB policy ~4% (2024–25) raises funding costs; credit/residual-value risk increases. Talent shortfalls (ISC2 cybersecurity gap 3.4M in 2023) and delivery complexity raise attrition and execution risk; ~70% of digital transformations underdeliver (McKinsey).

| Metric | Value |

|---|---|

| Resale gross margin | 3–7% |

| ECB policy rate | ~4% (2024–25) |

| Cybersecurity workforce gap | 3.4M (ISC2, 2023) |

| Digital transform. underdeliver | ~70% (McKinsey) |

What You See Is What You Get

Econocom Group SWOT Analysis

This is the actual SWOT analysis document for Econocom Group you’ll receive upon purchase—professional, structured, and ready to use. The preview below is taken directly from the full report you'll get. Purchase unlocks the entire in-depth, editable version.

Make Insightful Decisions Backed by Expert Research

Econocom’s hybrid IT and financing model shows clear strengths in digital services and strategic partnerships, but faces margin pressure and competitive disruption; our concise SWOT highlights key risks and growth levers. Want the full, research-backed analysis with editable Word and Excel deliverables to support strategy or investment decisions? Purchase the complete SWOT to unlock detailed findings, financial context, and actionable recommendations.

Strengths

End-to-end digital lifecycle

Combining consulting, sourcing, integration and managed services gives clients one accountable partner, reducing vendor sprawl and shortening decision cycles. Econocom, listed on Euronext and operating in 19 countries, reported roughly €3.2bn revenue in 2023, and multi-year engagements deepen stickiness while enabling cross-sell and upsell across the digital stack.

Flexible tech financing

Specialization in flexible financing and as-a-service models lets Econocom align client spend with outcomes, overcoming capex constraints and speeding project approvals across its footprint in 18 countries and ~9,800 employees.

These solutions contributed to group revenues of about €2.6bn in 2023 and generate recurring financing income that smooths revenue volatility.

The model differentiates Econocom from pure integrators or resellers by bundling services, hardware and financing into outcome-based contracts.

Enterprise client focus

Serving large organizations enables bigger deal sizes and programmatic rollouts, leveraging Econocoms enterprise references to win complex transformation mandates. Its governance and compliance capabilities align with corporate procurement and regulatory needs, increasing retention and switching costs. Econocom is listed on Euronext Paris and employs over 10,000 people across 20 countries, reinforcing global delivery capacity.

Vendor-agnostic sourcing

Vendor-agnostic sourcing lets Econocom assemble best-fit hardware, software and cloud stacks, aligning solutions to customer needs while leveraging expertise across vendors. This approach boosts negotiating leverage on pricing and SLAs and reduces client lock-in, supporting faster technology refresh cycles; 92% of enterprises used multi-cloud in 2024 (Flexera) which validates demand for flexible sourcing.

- Best-fit solutions

- Stronger pricing & SLA leverage

- Lower vendor lock-in

- Faster refresh cycles

Managed services depth

Managed services depth lets Econocom extend value beyond deployment through lifecycle support, converting installs into ongoing revenue streams and stabilizing margins; similar IT services peers report recurring services often exceeding 40-50% of revenue. Operational data from service contracts drives continuous improvement and upsell signals, strengthening client retention and increasing renewal rates. This recurring model supports predictable cash flows and long-term relationships.

- Lifecycle support: prolonged value capture

- Recurring revenue: stabilizes cash flows

- Service data: informs continuous improvement

- Client retention: boosts renewals

Integrated consulting-to-managed-services drives recurring revenue and €2.6bn scale

Integrated consulting-to-managed-services model, vendor-agnostic sourcing and flexible financing drive high stickiness, larger enterprise deals and recurring revenue, supported by global delivery and compliance capabilities.

| Metric | Value |

|---|---|

| 2023 revenue | €2.6bn |

| Employees | ~10,000 |

| Countries | ~20 |

| Multi-cloud adoption (Flexera 2024) | 92% |

What is included in the product

Provides a concise SWOT analysis of Econocom Group, highlighting internal strengths and weaknesses alongside market opportunities and external threats to inform strategic decisions.

Provides a concise SWOT matrix for fast, visual strategy alignment for Econocom Group, enabling executives to pinpoint digital-transformation strengths and vendor risks quickly while streamlining stakeholder decision-making.

Weaknesses

Margin pressure in reselling

IT sourcing and equipment resale are low-margin and highly competitive: industry resale gross margins typically range 3–7%, putting pressure on Econocom’s hardware lines.

Frequent discounting in large public and corporate tenders can materially erode profitability, sometimes halving transactional margins.

True differentiation must come from expanded services and embedded financing; shifting revenue mix toward managed services and leasing is required to protect gross margins.

Execution complexity

Coordinating consulting, delivery, financing and managed services raises operational risk as interdependent workflows increase points of failure. Multinational rollouts intensify program management and governance demands, stretching local compliance and SLAs. Delays can cascade into penalties or customer churn—McKinsey estimates roughly 70% of digital transformations underdeliver—and scaling reliably requires sustained investment in processes and tooling.

Capital intensity of financing

Offering financing ties up Econocoms balance-sheet capacity, with leasing and asset finance comprising the bulk of on-balance exposures and limiting debt headroom. Rising central-bank rates — ECB policy around 4% in 2024–25 — have pushed funding costs and increased RWAs, squeezing margins. Credit risk and residual-value volatility demand strict underwriting and remarketing controls. This capital intensity can reduce agility versus asset-light competitors.

Dependence on enterprise cycles

Dependence on enterprise cycles means budget freezes or elongated approval processes at large clients frequently delay Econocom’s revenue recognition, pushing payments and shifting revenue into later quarters.

Project-based peaks and troughs make capacity planning harder, forcing temporary staffing swings and higher marginal costs during demand spikes.

Economic slowdowns disproportionately reduce transformation spend, leaving revenue visibility uneven absent a strong, contracted backlog.

- Delayed approvals -> shifted revenue recognition

- Peaks/troughs -> capacity and cost volatility

- Slowdowns hit transformation budgets hardest

- Weak backlog -> low revenue visibility

Talent and skills constraints

Talent and skills constraints weaken Econocom as demand for cloud, cybersecurity and data specialists outstrips supply; ISC2 reported a 3.4 million global cybersecurity workforce gap in 2023. Attrition risks cause knowledge loss and delivery slippage, while rising wages compress service margins. Continuous upskilling programs are necessary but add significant cost pressure.

- Demand-supply gap: ISC2 3.4M (2023)

- Attrition → delivery slippage

- Wage inflation compresses margins

- High-cost continuous upskilling

Low-margin hardware (3-7%) and ECB ~4% squeeze profits; services must grow

Low-margin hardware resale (industry gross margins 3–7%) and frequent tender discounting compress profits; services/financing mix must grow to protect margins. Financing ties up balance-sheet while ECB policy ~4% (2024–25) raises funding costs; credit/residual-value risk increases. Talent shortfalls (ISC2 cybersecurity gap 3.4M in 2023) and delivery complexity raise attrition and execution risk; ~70% of digital transformations underdeliver (McKinsey).

| Metric | Value |

|---|---|

| Resale gross margin | 3–7% |

| ECB policy rate | ~4% (2024–25) |

| Cybersecurity workforce gap | 3.4M (ISC2, 2023) |

| Digital transform. underdeliver | ~70% (McKinsey) |

What You See Is What You Get

Econocom Group SWOT Analysis

This is the actual SWOT analysis document for Econocom Group you’ll receive upon purchase—professional, structured, and ready to use. The preview below is taken directly from the full report you'll get. Purchase unlocks the entire in-depth, editable version.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Econocom’s hybrid IT and financing model shows clear strengths in digital services and strategic partnerships, but faces margin pressure and competitive disruption; our concise SWOT highlights key risks and growth levers. Want the full, research-backed analysis with editable Word and Excel deliverables to support strategy or investment decisions? Purchase the complete SWOT to unlock detailed findings, financial context, and actionable recommendations.

Strengths

End-to-end digital lifecycle

Combining consulting, sourcing, integration and managed services gives clients one accountable partner, reducing vendor sprawl and shortening decision cycles. Econocom, listed on Euronext and operating in 19 countries, reported roughly €3.2bn revenue in 2023, and multi-year engagements deepen stickiness while enabling cross-sell and upsell across the digital stack.

Flexible tech financing

Specialization in flexible financing and as-a-service models lets Econocom align client spend with outcomes, overcoming capex constraints and speeding project approvals across its footprint in 18 countries and ~9,800 employees.

These solutions contributed to group revenues of about €2.6bn in 2023 and generate recurring financing income that smooths revenue volatility.

The model differentiates Econocom from pure integrators or resellers by bundling services, hardware and financing into outcome-based contracts.

Enterprise client focus

Serving large organizations enables bigger deal sizes and programmatic rollouts, leveraging Econocoms enterprise references to win complex transformation mandates. Its governance and compliance capabilities align with corporate procurement and regulatory needs, increasing retention and switching costs. Econocom is listed on Euronext Paris and employs over 10,000 people across 20 countries, reinforcing global delivery capacity.

Vendor-agnostic sourcing

Vendor-agnostic sourcing lets Econocom assemble best-fit hardware, software and cloud stacks, aligning solutions to customer needs while leveraging expertise across vendors. This approach boosts negotiating leverage on pricing and SLAs and reduces client lock-in, supporting faster technology refresh cycles; 92% of enterprises used multi-cloud in 2024 (Flexera) which validates demand for flexible sourcing.

- Best-fit solutions

- Stronger pricing & SLA leverage

- Lower vendor lock-in

- Faster refresh cycles

Managed services depth

Managed services depth lets Econocom extend value beyond deployment through lifecycle support, converting installs into ongoing revenue streams and stabilizing margins; similar IT services peers report recurring services often exceeding 40-50% of revenue. Operational data from service contracts drives continuous improvement and upsell signals, strengthening client retention and increasing renewal rates. This recurring model supports predictable cash flows and long-term relationships.

- Lifecycle support: prolonged value capture

- Recurring revenue: stabilizes cash flows

- Service data: informs continuous improvement

- Client retention: boosts renewals

Integrated consulting-to-managed-services drives recurring revenue and €2.6bn scale

Integrated consulting-to-managed-services model, vendor-agnostic sourcing and flexible financing drive high stickiness, larger enterprise deals and recurring revenue, supported by global delivery and compliance capabilities.

| Metric | Value |

|---|---|

| 2023 revenue | €2.6bn |

| Employees | ~10,000 |

| Countries | ~20 |

| Multi-cloud adoption (Flexera 2024) | 92% |

What is included in the product

Provides a concise SWOT analysis of Econocom Group, highlighting internal strengths and weaknesses alongside market opportunities and external threats to inform strategic decisions.

Provides a concise SWOT matrix for fast, visual strategy alignment for Econocom Group, enabling executives to pinpoint digital-transformation strengths and vendor risks quickly while streamlining stakeholder decision-making.

Weaknesses

Margin pressure in reselling

IT sourcing and equipment resale are low-margin and highly competitive: industry resale gross margins typically range 3–7%, putting pressure on Econocom’s hardware lines.

Frequent discounting in large public and corporate tenders can materially erode profitability, sometimes halving transactional margins.

True differentiation must come from expanded services and embedded financing; shifting revenue mix toward managed services and leasing is required to protect gross margins.

Execution complexity

Coordinating consulting, delivery, financing and managed services raises operational risk as interdependent workflows increase points of failure. Multinational rollouts intensify program management and governance demands, stretching local compliance and SLAs. Delays can cascade into penalties or customer churn—McKinsey estimates roughly 70% of digital transformations underdeliver—and scaling reliably requires sustained investment in processes and tooling.

Capital intensity of financing

Offering financing ties up Econocoms balance-sheet capacity, with leasing and asset finance comprising the bulk of on-balance exposures and limiting debt headroom. Rising central-bank rates — ECB policy around 4% in 2024–25 — have pushed funding costs and increased RWAs, squeezing margins. Credit risk and residual-value volatility demand strict underwriting and remarketing controls. This capital intensity can reduce agility versus asset-light competitors.

Dependence on enterprise cycles

Dependence on enterprise cycles means budget freezes or elongated approval processes at large clients frequently delay Econocom’s revenue recognition, pushing payments and shifting revenue into later quarters.

Project-based peaks and troughs make capacity planning harder, forcing temporary staffing swings and higher marginal costs during demand spikes.

Economic slowdowns disproportionately reduce transformation spend, leaving revenue visibility uneven absent a strong, contracted backlog.

- Delayed approvals -> shifted revenue recognition

- Peaks/troughs -> capacity and cost volatility

- Slowdowns hit transformation budgets hardest

- Weak backlog -> low revenue visibility

Talent and skills constraints

Talent and skills constraints weaken Econocom as demand for cloud, cybersecurity and data specialists outstrips supply; ISC2 reported a 3.4 million global cybersecurity workforce gap in 2023. Attrition risks cause knowledge loss and delivery slippage, while rising wages compress service margins. Continuous upskilling programs are necessary but add significant cost pressure.

- Demand-supply gap: ISC2 3.4M (2023)

- Attrition → delivery slippage

- Wage inflation compresses margins

- High-cost continuous upskilling

Low-margin hardware (3-7%) and ECB ~4% squeeze profits; services must grow

Low-margin hardware resale (industry gross margins 3–7%) and frequent tender discounting compress profits; services/financing mix must grow to protect margins. Financing ties up balance-sheet while ECB policy ~4% (2024–25) raises funding costs; credit/residual-value risk increases. Talent shortfalls (ISC2 cybersecurity gap 3.4M in 2023) and delivery complexity raise attrition and execution risk; ~70% of digital transformations underdeliver (McKinsey).

| Metric | Value |

|---|---|

| Resale gross margin | 3–7% |

| ECB policy rate | ~4% (2024–25) |

| Cybersecurity workforce gap | 3.4M (ISC2, 2023) |

| Digital transform. underdeliver | ~70% (McKinsey) |

What You See Is What You Get

Econocom Group SWOT Analysis

This is the actual SWOT analysis document for Econocom Group you’ll receive upon purchase—professional, structured, and ready to use. The preview below is taken directly from the full report you'll get. Purchase unlocks the entire in-depth, editable version.