Danel Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

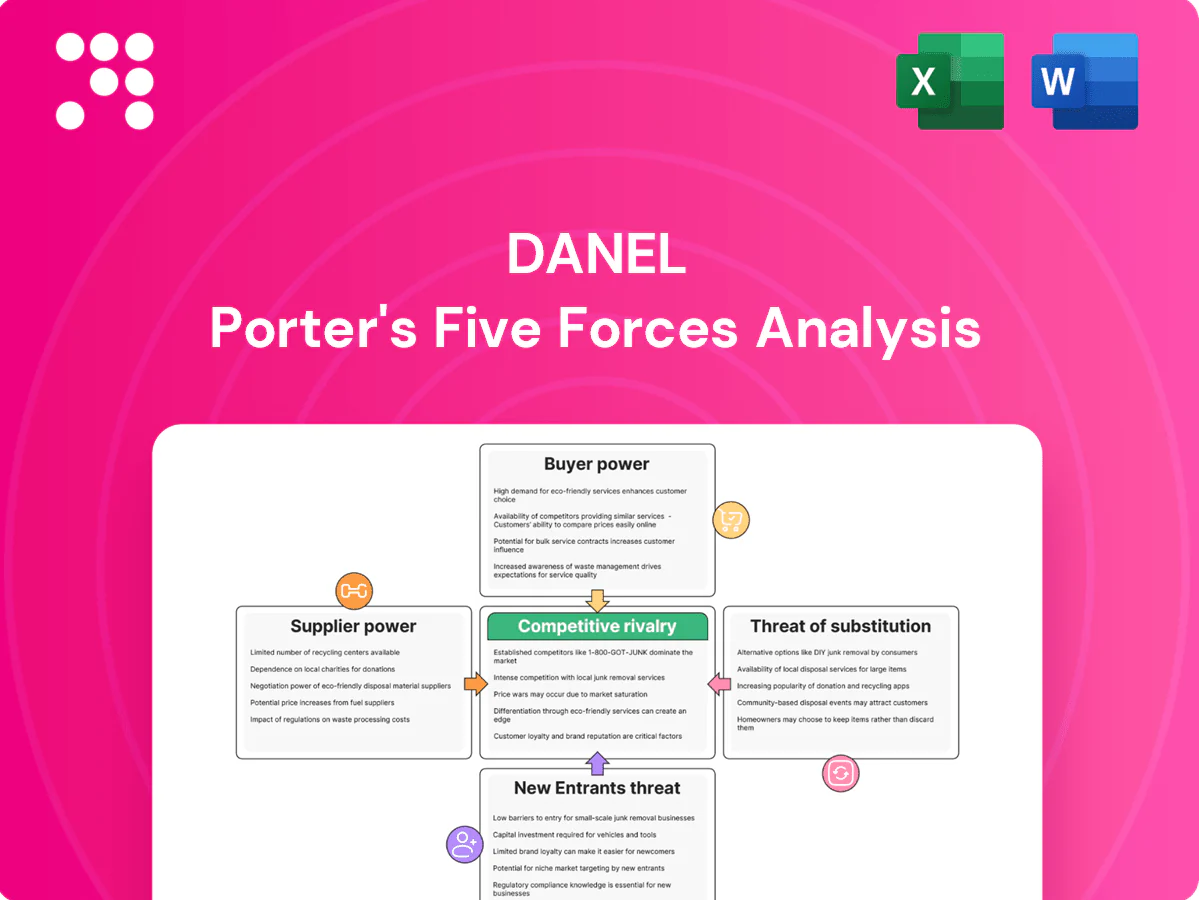

Danel ’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, and risks from new entrants and substitutes to show where margins and market share are most vulnerable. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Danel ’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Tight talent in key verticals

In Israel, scarce high-tech engineers and licensed healthcare staff command premium terms; over 60% of employers reported hiring difficulties in 2024, pushing average tech starting salaries up and shortening time-to-hire windows. Candidate scarcity forces agencies to offer higher wages and faster placements, elevating suppliers’ leverage on rates and assignment conditions. This tight market also increases risks of ghosting or late-stage renegotiation, raising contingency costs for firms.

Multi-channel sourcing dependence

Danel relies on job boards, LinkedIn and niche communities to source talent, concentrating supply through a few upstream platforms. Platform algorithm shifts and pricing changes can materially raise candidate acquisition costs and time-to-hire. LinkedIn surpassed 930 million members in 2024, increasing its leverage as preferred access or featured listings often become paid necessities. This dependence strengthens upstream platforms' bargaining power.

Credentialing and compliance gatekeepers

Background checks, medical licensing bodies, and training vendors act as gatekeepers—CAQH data in 2024 showed credentialing delays averaged about 90 days for many clinicians—slowing placements and adding administrative costs often exceeding $1,500 per candidate. Vendors can impose verification price hikes that agencies must absorb or lose candidates, increasing supplier leverage in regulated roles and compressing agency margins.

Talent brand and referral networks

Candidates with strong reputations or niche certifications can choose among multiple agencies; in 2024 surveys ~70% received multiple offers and many firms conceded 5–10% margins or added perks to win them, preferring agencies with better benefits, schedules, or payroll terms, which raises individual supplier power in hot segments.

- 70% multiple-offer rate (2024)

- 5–10% margin concessions

- Perks and payroll flexibility drive wins

Technology stack lock-in

ATS, CRM and payroll systems embed deeply into hiring, sales and payroll workflows, making wholesale switches costly and operationally risky, so vendors gain leverage at renewal time.

Many enterprise contracts include annual price escalators typically in the 3–5% range and module bundling that can raise spend by roughly 10–30%, pressuring margins.

Service quality lapses can disrupt HR/payroll operations yet are hard to contest once data and processes are entrenched.

- Key risk: vendor leverage on renewals

- Typical escalators: 3–5%

- Bundling uplift: ~10–30%

Supplier squeeze: 60% hiring difficulty, 70% multiple-offer surge

Supplier power is high: 60% of employers reported 2024 hiring difficulties and niche candidates saw ~70% multiple-offer rates, forcing 5–10% margin concessions. Dependence on platforms like LinkedIn (930M members in 2024) and slow credentialing (~90-day delays) raises acquisition and admin costs. Contractual escalators (3–5%) and bundling uplifts (10–30%) further compress agency margins.

| Metric | 2024 Value |

|---|---|

| Hiring difficulty | 60% |

| Multiple-offer rate | 70% |

| LinkedIn size | 930M |

| Credentialing delay | ~90 days |

| Escalators | 3–5% |

| Bundling uplift | 10–30% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Danel, uncovering competitive drivers, supplier and buyer power, substitutes and new-entry risks, and identifying disruptive threats and protective market dynamics.

A clear one-sheet summary of Danel Porter’s Five Forces that instantly highlights competitive pain points and relieves decision paralysis—ready to drop into decks, customize with current data, and share across teams.

Customers Bargaining Power

Large clients use MSPs and RFPs

Enterprises in healthcare, finance and tech increasingly centralize procurement through MSPs and RFPs; in 2024 roughly 65% of large firms used centralized contingent labor buying. Volume commitments commonly secure discounts of 10–25% and stringent SLAs. Widespread VMS adoption (about 60% of large buyers in 2024) compresses supplier margins 5–15%. The net effect is pronounced buyer leverage over pricing and contract terms.

Low switching costs across agencies

Clients commonly multi-source similar roles from several providers, with 2024 industry surveys indicating ≈55% of employers use multiple agencies, compressing supplier margins. Comparable candidate pools reduce differentiation, so agencies compete on speed, pricing and niche expertise. If quality or time-to-fill slips, requisitions shift quickly between vendors. This dynamic keeps pricing keen and response times tight.

Demand cyclicality and budget controls

Demand cyclicality and tighter budget controls sharply increase customer leverage: IMF projected global GDP growth of about 3.1% in 2024, and hiring freezes or project delays instantaneously cut requisition flow for providers. Buyers routinely renegotiate rates during downturns and favor variable staffing to flex spend without long-term penalties. Cycles thus amplify buyer power over both rates and volume, compressing margins for suppliers.

Data and compliance expectations

Clients demand strict GDPR and Israeli privacy plus payroll and tax compliance; 2024 enforcement intensified, raising penalty risk and supplier delisting. Audit rights and expanded reporting routinely add 5–12% to delivery costs, and buyers increasingly wield compliance failures as a negotiation lever.

- Compliance-driven delisting risk: >10% reported in 2024

- Delivery cost uplift: 5–12%

- Audit/reporting duties: mandatory contract clauses

Preference for outcome KPIs

Preference for outcome KPIs like time-to-fill, quality-of-hire and retention guarantees shifts risk from buyers to agencies, forcing agencies to absorb costs when SLAs are missed. Penalties or free replacements directly erode agency margins and cashflow, while more clients in 2024 pushed for performance-based fees tied to hires and retention, strengthening buyer leverage. This trend compresses pricing power and increases negotiation pressure on agencies.

- Time-to-fill linked to SLAs increases agency risk

- Quality-of-hire metrics drive replacement penalties

- Retention guarantees shorten payback on placements

- Performance fees boost buyer bargaining power

Buyers have leverage: ~65% central buying, 10–25% discounts

Buyers hold strong leverage: in 2024 ~65% of large firms used centralized contingent labor buying and ~60% used VMS, driving 10–25% volume discounts and compressing supplier margins 5–15%. About 55% multi-source vendors, forcing competition on price and speed. Compliance and audits add 5–12% delivery cost and >10% delisting risk. Performance-based fees and SLAs shift risk to agencies, tightening pricing power.

| Metric | 2024 Value |

|---|---|

| Centralized buying | ~65% |

| VMS adoption | ~60% |

| Multi-sourcing | ~55% |

| Volume discounts | 10–25% |

| Margin compression | 5–15% |

| Compliance cost uplift | 5–12% |

| Delisting risk | >10% |

What You See Is What You Get

Danel Porter's Five Forces Analysis

This preview shows the exact Danel Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready for use. The file displayed here is the complete, professional report with no placeholders, mockups, or samples. Once you buy, you'll get instant access to this identical document for download and application.

Go Beyond the Preview—Access the Full Strategic Report

Danel ’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, and risks from new entrants and substitutes to show where margins and market share are most vulnerable. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Danel ’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Tight talent in key verticals

In Israel, scarce high-tech engineers and licensed healthcare staff command premium terms; over 60% of employers reported hiring difficulties in 2024, pushing average tech starting salaries up and shortening time-to-hire windows. Candidate scarcity forces agencies to offer higher wages and faster placements, elevating suppliers’ leverage on rates and assignment conditions. This tight market also increases risks of ghosting or late-stage renegotiation, raising contingency costs for firms.

Multi-channel sourcing dependence

Danel relies on job boards, LinkedIn and niche communities to source talent, concentrating supply through a few upstream platforms. Platform algorithm shifts and pricing changes can materially raise candidate acquisition costs and time-to-hire. LinkedIn surpassed 930 million members in 2024, increasing its leverage as preferred access or featured listings often become paid necessities. This dependence strengthens upstream platforms' bargaining power.

Credentialing and compliance gatekeepers

Background checks, medical licensing bodies, and training vendors act as gatekeepers—CAQH data in 2024 showed credentialing delays averaged about 90 days for many clinicians—slowing placements and adding administrative costs often exceeding $1,500 per candidate. Vendors can impose verification price hikes that agencies must absorb or lose candidates, increasing supplier leverage in regulated roles and compressing agency margins.

Talent brand and referral networks

Candidates with strong reputations or niche certifications can choose among multiple agencies; in 2024 surveys ~70% received multiple offers and many firms conceded 5–10% margins or added perks to win them, preferring agencies with better benefits, schedules, or payroll terms, which raises individual supplier power in hot segments.

- 70% multiple-offer rate (2024)

- 5–10% margin concessions

- Perks and payroll flexibility drive wins

Technology stack lock-in

ATS, CRM and payroll systems embed deeply into hiring, sales and payroll workflows, making wholesale switches costly and operationally risky, so vendors gain leverage at renewal time.

Many enterprise contracts include annual price escalators typically in the 3–5% range and module bundling that can raise spend by roughly 10–30%, pressuring margins.

Service quality lapses can disrupt HR/payroll operations yet are hard to contest once data and processes are entrenched.

- Key risk: vendor leverage on renewals

- Typical escalators: 3–5%

- Bundling uplift: ~10–30%

Supplier squeeze: 60% hiring difficulty, 70% multiple-offer surge

Supplier power is high: 60% of employers reported 2024 hiring difficulties and niche candidates saw ~70% multiple-offer rates, forcing 5–10% margin concessions. Dependence on platforms like LinkedIn (930M members in 2024) and slow credentialing (~90-day delays) raises acquisition and admin costs. Contractual escalators (3–5%) and bundling uplifts (10–30%) further compress agency margins.

| Metric | 2024 Value |

|---|---|

| Hiring difficulty | 60% |

| Multiple-offer rate | 70% |

| LinkedIn size | 930M |

| Credentialing delay | ~90 days |

| Escalators | 3–5% |

| Bundling uplift | 10–30% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Danel, uncovering competitive drivers, supplier and buyer power, substitutes and new-entry risks, and identifying disruptive threats and protective market dynamics.

A clear one-sheet summary of Danel Porter’s Five Forces that instantly highlights competitive pain points and relieves decision paralysis—ready to drop into decks, customize with current data, and share across teams.

Customers Bargaining Power

Large clients use MSPs and RFPs

Enterprises in healthcare, finance and tech increasingly centralize procurement through MSPs and RFPs; in 2024 roughly 65% of large firms used centralized contingent labor buying. Volume commitments commonly secure discounts of 10–25% and stringent SLAs. Widespread VMS adoption (about 60% of large buyers in 2024) compresses supplier margins 5–15%. The net effect is pronounced buyer leverage over pricing and contract terms.

Low switching costs across agencies

Clients commonly multi-source similar roles from several providers, with 2024 industry surveys indicating ≈55% of employers use multiple agencies, compressing supplier margins. Comparable candidate pools reduce differentiation, so agencies compete on speed, pricing and niche expertise. If quality or time-to-fill slips, requisitions shift quickly between vendors. This dynamic keeps pricing keen and response times tight.

Demand cyclicality and budget controls

Demand cyclicality and tighter budget controls sharply increase customer leverage: IMF projected global GDP growth of about 3.1% in 2024, and hiring freezes or project delays instantaneously cut requisition flow for providers. Buyers routinely renegotiate rates during downturns and favor variable staffing to flex spend without long-term penalties. Cycles thus amplify buyer power over both rates and volume, compressing margins for suppliers.

Data and compliance expectations

Clients demand strict GDPR and Israeli privacy plus payroll and tax compliance; 2024 enforcement intensified, raising penalty risk and supplier delisting. Audit rights and expanded reporting routinely add 5–12% to delivery costs, and buyers increasingly wield compliance failures as a negotiation lever.

- Compliance-driven delisting risk: >10% reported in 2024

- Delivery cost uplift: 5–12%

- Audit/reporting duties: mandatory contract clauses

Preference for outcome KPIs

Preference for outcome KPIs like time-to-fill, quality-of-hire and retention guarantees shifts risk from buyers to agencies, forcing agencies to absorb costs when SLAs are missed. Penalties or free replacements directly erode agency margins and cashflow, while more clients in 2024 pushed for performance-based fees tied to hires and retention, strengthening buyer leverage. This trend compresses pricing power and increases negotiation pressure on agencies.

- Time-to-fill linked to SLAs increases agency risk

- Quality-of-hire metrics drive replacement penalties

- Retention guarantees shorten payback on placements

- Performance fees boost buyer bargaining power

Buyers have leverage: ~65% central buying, 10–25% discounts

Buyers hold strong leverage: in 2024 ~65% of large firms used centralized contingent labor buying and ~60% used VMS, driving 10–25% volume discounts and compressing supplier margins 5–15%. About 55% multi-source vendors, forcing competition on price and speed. Compliance and audits add 5–12% delivery cost and >10% delisting risk. Performance-based fees and SLAs shift risk to agencies, tightening pricing power.

| Metric | 2024 Value |

|---|---|

| Centralized buying | ~65% |

| VMS adoption | ~60% |

| Multi-sourcing | ~55% |

| Volume discounts | 10–25% |

| Margin compression | 5–15% |

| Compliance cost uplift | 5–12% |

| Delisting risk | >10% |

What You See Is What You Get

Danel Porter's Five Forces Analysis

This preview shows the exact Danel Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready for use. The file displayed here is the complete, professional report with no placeholders, mockups, or samples. Once you buy, you'll get instant access to this identical document for download and application.

Description

Go Beyond the Preview—Access the Full Strategic Report

Danel ’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, and risks from new entrants and substitutes to show where margins and market share are most vulnerable. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Danel ’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Tight talent in key verticals

In Israel, scarce high-tech engineers and licensed healthcare staff command premium terms; over 60% of employers reported hiring difficulties in 2024, pushing average tech starting salaries up and shortening time-to-hire windows. Candidate scarcity forces agencies to offer higher wages and faster placements, elevating suppliers’ leverage on rates and assignment conditions. This tight market also increases risks of ghosting or late-stage renegotiation, raising contingency costs for firms.

Multi-channel sourcing dependence

Danel relies on job boards, LinkedIn and niche communities to source talent, concentrating supply through a few upstream platforms. Platform algorithm shifts and pricing changes can materially raise candidate acquisition costs and time-to-hire. LinkedIn surpassed 930 million members in 2024, increasing its leverage as preferred access or featured listings often become paid necessities. This dependence strengthens upstream platforms' bargaining power.

Credentialing and compliance gatekeepers

Background checks, medical licensing bodies, and training vendors act as gatekeepers—CAQH data in 2024 showed credentialing delays averaged about 90 days for many clinicians—slowing placements and adding administrative costs often exceeding $1,500 per candidate. Vendors can impose verification price hikes that agencies must absorb or lose candidates, increasing supplier leverage in regulated roles and compressing agency margins.

Talent brand and referral networks

Candidates with strong reputations or niche certifications can choose among multiple agencies; in 2024 surveys ~70% received multiple offers and many firms conceded 5–10% margins or added perks to win them, preferring agencies with better benefits, schedules, or payroll terms, which raises individual supplier power in hot segments.

- 70% multiple-offer rate (2024)

- 5–10% margin concessions

- Perks and payroll flexibility drive wins

Technology stack lock-in

ATS, CRM and payroll systems embed deeply into hiring, sales and payroll workflows, making wholesale switches costly and operationally risky, so vendors gain leverage at renewal time.

Many enterprise contracts include annual price escalators typically in the 3–5% range and module bundling that can raise spend by roughly 10–30%, pressuring margins.

Service quality lapses can disrupt HR/payroll operations yet are hard to contest once data and processes are entrenched.

- Key risk: vendor leverage on renewals

- Typical escalators: 3–5%

- Bundling uplift: ~10–30%

Supplier squeeze: 60% hiring difficulty, 70% multiple-offer surge

Supplier power is high: 60% of employers reported 2024 hiring difficulties and niche candidates saw ~70% multiple-offer rates, forcing 5–10% margin concessions. Dependence on platforms like LinkedIn (930M members in 2024) and slow credentialing (~90-day delays) raises acquisition and admin costs. Contractual escalators (3–5%) and bundling uplifts (10–30%) further compress agency margins.

| Metric | 2024 Value |

|---|---|

| Hiring difficulty | 60% |

| Multiple-offer rate | 70% |

| LinkedIn size | 930M |

| Credentialing delay | ~90 days |

| Escalators | 3–5% |

| Bundling uplift | 10–30% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Danel, uncovering competitive drivers, supplier and buyer power, substitutes and new-entry risks, and identifying disruptive threats and protective market dynamics.

A clear one-sheet summary of Danel Porter’s Five Forces that instantly highlights competitive pain points and relieves decision paralysis—ready to drop into decks, customize with current data, and share across teams.

Customers Bargaining Power

Large clients use MSPs and RFPs

Enterprises in healthcare, finance and tech increasingly centralize procurement through MSPs and RFPs; in 2024 roughly 65% of large firms used centralized contingent labor buying. Volume commitments commonly secure discounts of 10–25% and stringent SLAs. Widespread VMS adoption (about 60% of large buyers in 2024) compresses supplier margins 5–15%. The net effect is pronounced buyer leverage over pricing and contract terms.

Low switching costs across agencies

Clients commonly multi-source similar roles from several providers, with 2024 industry surveys indicating ≈55% of employers use multiple agencies, compressing supplier margins. Comparable candidate pools reduce differentiation, so agencies compete on speed, pricing and niche expertise. If quality or time-to-fill slips, requisitions shift quickly between vendors. This dynamic keeps pricing keen and response times tight.

Demand cyclicality and budget controls

Demand cyclicality and tighter budget controls sharply increase customer leverage: IMF projected global GDP growth of about 3.1% in 2024, and hiring freezes or project delays instantaneously cut requisition flow for providers. Buyers routinely renegotiate rates during downturns and favor variable staffing to flex spend without long-term penalties. Cycles thus amplify buyer power over both rates and volume, compressing margins for suppliers.

Data and compliance expectations

Clients demand strict GDPR and Israeli privacy plus payroll and tax compliance; 2024 enforcement intensified, raising penalty risk and supplier delisting. Audit rights and expanded reporting routinely add 5–12% to delivery costs, and buyers increasingly wield compliance failures as a negotiation lever.

- Compliance-driven delisting risk: >10% reported in 2024

- Delivery cost uplift: 5–12%

- Audit/reporting duties: mandatory contract clauses

Preference for outcome KPIs

Preference for outcome KPIs like time-to-fill, quality-of-hire and retention guarantees shifts risk from buyers to agencies, forcing agencies to absorb costs when SLAs are missed. Penalties or free replacements directly erode agency margins and cashflow, while more clients in 2024 pushed for performance-based fees tied to hires and retention, strengthening buyer leverage. This trend compresses pricing power and increases negotiation pressure on agencies.

- Time-to-fill linked to SLAs increases agency risk

- Quality-of-hire metrics drive replacement penalties

- Retention guarantees shorten payback on placements

- Performance fees boost buyer bargaining power

Buyers have leverage: ~65% central buying, 10–25% discounts

Buyers hold strong leverage: in 2024 ~65% of large firms used centralized contingent labor buying and ~60% used VMS, driving 10–25% volume discounts and compressing supplier margins 5–15%. About 55% multi-source vendors, forcing competition on price and speed. Compliance and audits add 5–12% delivery cost and >10% delisting risk. Performance-based fees and SLAs shift risk to agencies, tightening pricing power.

| Metric | 2024 Value |

|---|---|

| Centralized buying | ~65% |

| VMS adoption | ~60% |

| Multi-sourcing | ~55% |

| Volume discounts | 10–25% |

| Margin compression | 5–15% |

| Compliance cost uplift | 5–12% |

| Delisting risk | >10% |

What You See Is What You Get

Danel Porter's Five Forces Analysis

This preview shows the exact Danel Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted and ready for use. The file displayed here is the complete, professional report with no placeholders, mockups, or samples. Once you buy, you'll get instant access to this identical document for download and application.