Eiffage PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Eiffage faces shifting political regulations, infrastructure spending cycles and rising sustainability pressures that reshape project economics. Our PESTLE distills these external forces into clear risks and opportunities—ideal for investors, consultants and strategists. Download the full, ready-to-use analysis now to inform decisions and gain a competitive edge.

Political factors

EU infrastructure funding

Access to EU funds—cohesion policy €392.8bn (2021–27) and NextGenerationEU/RRF components within the €806.9bn package—shapes Eiffage’s project pipeline and margins. Shifts in allocations accelerate transport, energy and urban renewal projects; CEF’s €33.7bn focus on TEN-T and rail electrification benefits civil engineering units. Budget tightening delays awards and stretches tender timelines, squeezing cashflows and bid windows.

PPP policy direction

Government appetite for public–private partnerships shapes concession pipelines and directly affects Eiffage’s tender flow; stable frameworks unlock lifecycle revenues from design through operation, supporting its reported €20.3bn 2023 revenue base. Policy reversals or stricter value-for-money tests can sharply reduce greenfield PPP volumes, while political scrutiny of user fees or availability payments shifts risk sharing and compresses expected returns.

Public procurement rules

EU directives (2014/24/EU) and national laws govern procurement across a c.€2 trillion EU market (~14% of GDP), enforcing competition, transparency and local-content rules. Shift from lowest-price to MEAT award criteria boosts innovation incentives and life-cycle pricing. Faster permitting and streamlined approvals cut backlog-related delays and de-risk projects. Anti-corruption enforcement (OECD estimates 10–25% procurement loss to corruption) raises compliance costs but protects reputational capital.

Energy transition priorities

EU political decarbonization targets (‑55% GHG by 2030) drive demand for rail electrification, EV charging infrastructure and renewables-backed grids, while auctions and subsidies (eg. REPowerEU funding) shape near-term pipeline visibility. Industrial policy and CBAM, together with EU ETS carbon pricing at roughly €90–110/t in 2024–mid‑2025, push steel and cement costs higher. Policy stability remains critical to de‑risk investment in low‑carbon construction methods.

- Demand: rail, EV charging, grid expansion

- Finance: auctions/subsidies = pipeline visibility

- Supply costs: CBAM + EU ETS ~€90–110/t

- Investment: policy stability required for low‑carbon construction

Regional planning and decentralization

- Deal origination: regional/municipal first

- Public investment: ~70% local (INSEE 2021)

- Risk: delays from local political turnover

- Advantage: stakeholder management differentiator

EU funds and CEF steer pipeline to transport/energy; PPP/MEAT lift margins ETS raises costs

EU funding packages (€392.8bn cohesion; €806.9bn NextGenerationEU) and CEF €33.7bn tilt Eiffage’s pipeline to transport/energy projects, while PPP policy and MEAT procurement boost lifecycle margins supporting €20.3bn 2023 revenue. EU ETS ~€90–110/t (2024–mid‑2025) and CBAM raise steel/cement costs. Local governments supply ~70% of French public investment, increasing regional deal risk from political turnover.

| Factor | Key Figure |

|---|---|

| EU funding | €392.8bn / €806.9bn |

| CEF | €33.7bn |

| Revenue (Eiffage) | €20.3bn (2023) |

| EU ETS | €90–110/t (2024–mid‑2025) |

| Local investment (France) | ~70% (INSEE 2021) |

What is included in the product

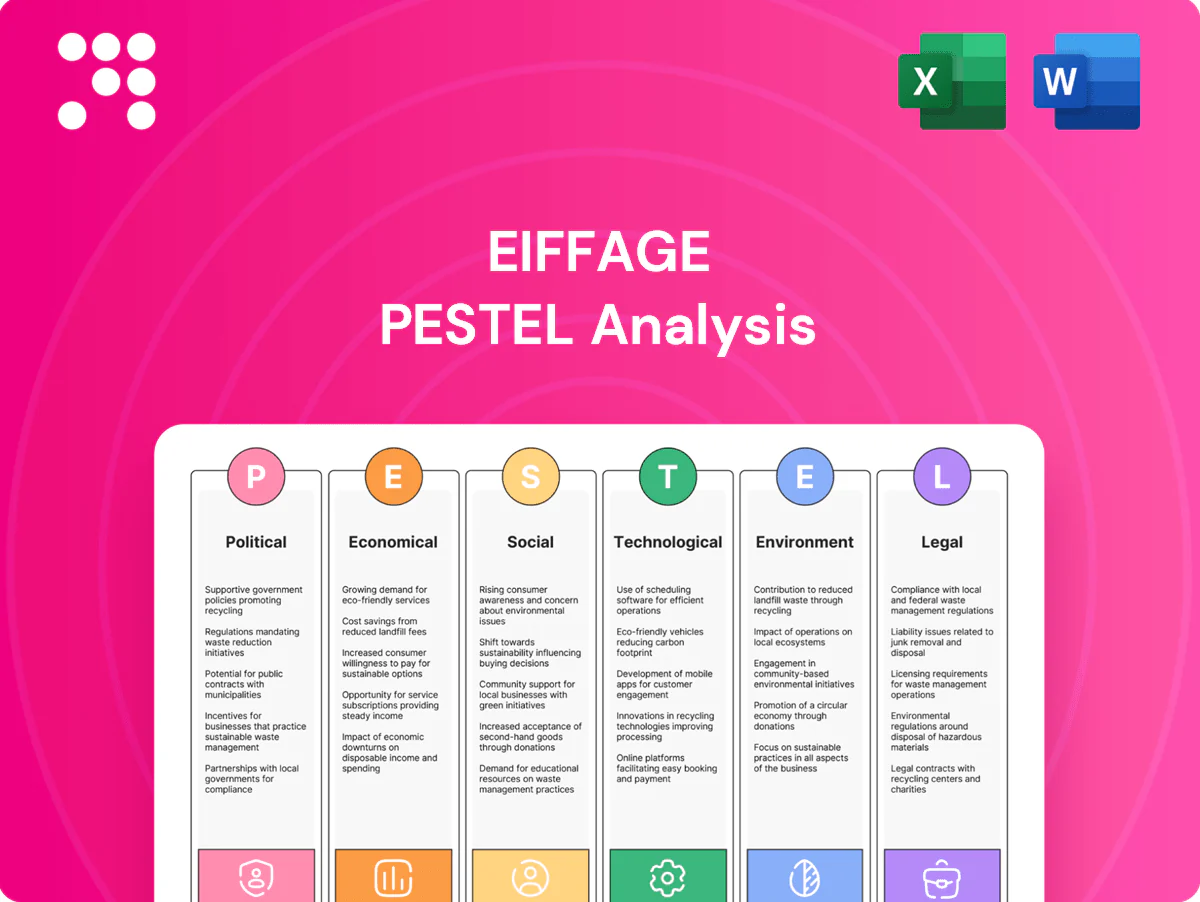

Provides a concise PESTLE evaluation of Eiffage, detailing Political, Economic, Social, Technological, Environmental and Legal drivers with data-backed trends and region-specific regulatory context; designed to help executives, advisors and investors identify risks, opportunities and forward-looking strategic actions.

A concise, visually segmented PESTLE summary of Eiffage that’s easily editable and shareable for presentations, workshops, and client reports, enabling quick alignment across teams and streamlined discussion of external risks and market positioning.

Economic factors

Interest rates and financing

Higher borrowing costs—ECB policy rate at 4.00% (July 2024)—raise WACC for Eiffage concessions and EPC bids, squeezing returns and necessitating higher bid margins. Debt market tightness limits competitive bidding and reduces refinancing gains versus past low-rate cycles. Inflation-linked contracts help protect margins but indexation lags can still erode real returns. Active treasury management is critical for long-duration assets.

Construction cost inflation

Volatile input costs — e.g., European hot‑rolled coil ranged roughly €600–1,000/ton in 2022–24 — squeeze margins on fixed‑price contracts and raise bid risk for Eiffage. Supply‑chain hedging and multi‑year framework agreements have helped stabilize procurement and limit short‑term shocks. Design‑to‑cost, modular construction and prefabrication protect margins by reducing on‑site material exposure. Budget pressure can prompt clients to defer projects, slowing revenue recognition.

Public investment cycles

Public investment volumes for Eiffage are driven by fiscal space and stimulus: EU NextGenerationEU mobilises €806.9bn and France’s 2020 Relance was €100bn, shaping civil works demand. Election cycles (next French presidential vote 2027) and deficit rules influence award timing and contractor risk. EU multiyear transport and cohesion budgets (circa €330bn 2021–27) give planning visibility. Recurrent delays in budget execution squeeze working capital and cashflow.

Labor market dynamics

- Workforce: ~74,000 (2024)

- Skills gap: raises wages and delays

- Solutions: apprenticeships, EU mobility, prefabrication

- Risk: industrial relations affect schedules

Traffic and demand elasticity

Concession revenues for Eiffage closely track macro growth and mobility patterns, so shifts toward rail, micromobility or remote work change traffic mixes and reduce peak toll volumes, pressuring yields. Implementing dynamic pricing and higher service standards can partially stabilize cash flows and improve elasticity management. During downturns, increased demand risk prompts renegotiations with grantors and greater use of revenue-sharing mechanisms.

- Concession sensitivity

- Mode shift impact

- Dynamic pricing stabilises cash flow

- Downturn → renegotiation

EU funds and CEF steer pipeline to transport/energy; PPP/MEAT lift margins ETS raises costs

Higher ECB rate 4.00% (Jul 2024) raises WACC, tightening bids and refinancing; inflation indexation helps but lags. Volatile inputs (HRC ~€600–1,000/t in 2022–24) and supply shocks raise fixed‑price risk; prefabrication and hedging reduce exposure. Public investment (NextGenerationEU €806.9bn; EU transport/cohesion ~€330bn 2021–27) supports visibility; execution delays strain cashflow and working capital.

| Metric | Value |

|---|---|

| ECB rate (Jul 2024) | 4.00% |

| Workforce (2024) | ~74,000 |

| NextGenerationEU | €806.9bn |

Same Document Delivered

Eiffage PESTLE Analysis

The Eiffage PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors shaping the company’s operating environment. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The document is fully formatted and ready to download and use after purchase.

Your Shortcut to Market Insight Starts Here

Eiffage faces shifting political regulations, infrastructure spending cycles and rising sustainability pressures that reshape project economics. Our PESTLE distills these external forces into clear risks and opportunities—ideal for investors, consultants and strategists. Download the full, ready-to-use analysis now to inform decisions and gain a competitive edge.

Political factors

EU infrastructure funding

Access to EU funds—cohesion policy €392.8bn (2021–27) and NextGenerationEU/RRF components within the €806.9bn package—shapes Eiffage’s project pipeline and margins. Shifts in allocations accelerate transport, energy and urban renewal projects; CEF’s €33.7bn focus on TEN-T and rail electrification benefits civil engineering units. Budget tightening delays awards and stretches tender timelines, squeezing cashflows and bid windows.

PPP policy direction

Government appetite for public–private partnerships shapes concession pipelines and directly affects Eiffage’s tender flow; stable frameworks unlock lifecycle revenues from design through operation, supporting its reported €20.3bn 2023 revenue base. Policy reversals or stricter value-for-money tests can sharply reduce greenfield PPP volumes, while political scrutiny of user fees or availability payments shifts risk sharing and compresses expected returns.

Public procurement rules

EU directives (2014/24/EU) and national laws govern procurement across a c.€2 trillion EU market (~14% of GDP), enforcing competition, transparency and local-content rules. Shift from lowest-price to MEAT award criteria boosts innovation incentives and life-cycle pricing. Faster permitting and streamlined approvals cut backlog-related delays and de-risk projects. Anti-corruption enforcement (OECD estimates 10–25% procurement loss to corruption) raises compliance costs but protects reputational capital.

Energy transition priorities

EU political decarbonization targets (‑55% GHG by 2030) drive demand for rail electrification, EV charging infrastructure and renewables-backed grids, while auctions and subsidies (eg. REPowerEU funding) shape near-term pipeline visibility. Industrial policy and CBAM, together with EU ETS carbon pricing at roughly €90–110/t in 2024–mid‑2025, push steel and cement costs higher. Policy stability remains critical to de‑risk investment in low‑carbon construction methods.

- Demand: rail, EV charging, grid expansion

- Finance: auctions/subsidies = pipeline visibility

- Supply costs: CBAM + EU ETS ~€90–110/t

- Investment: policy stability required for low‑carbon construction

Regional planning and decentralization

- Deal origination: regional/municipal first

- Public investment: ~70% local (INSEE 2021)

- Risk: delays from local political turnover

- Advantage: stakeholder management differentiator

EU funds and CEF steer pipeline to transport/energy; PPP/MEAT lift margins ETS raises costs

EU funding packages (€392.8bn cohesion; €806.9bn NextGenerationEU) and CEF €33.7bn tilt Eiffage’s pipeline to transport/energy projects, while PPP policy and MEAT procurement boost lifecycle margins supporting €20.3bn 2023 revenue. EU ETS ~€90–110/t (2024–mid‑2025) and CBAM raise steel/cement costs. Local governments supply ~70% of French public investment, increasing regional deal risk from political turnover.

| Factor | Key Figure |

|---|---|

| EU funding | €392.8bn / €806.9bn |

| CEF | €33.7bn |

| Revenue (Eiffage) | €20.3bn (2023) |

| EU ETS | €90–110/t (2024–mid‑2025) |

| Local investment (France) | ~70% (INSEE 2021) |

What is included in the product

Provides a concise PESTLE evaluation of Eiffage, detailing Political, Economic, Social, Technological, Environmental and Legal drivers with data-backed trends and region-specific regulatory context; designed to help executives, advisors and investors identify risks, opportunities and forward-looking strategic actions.

A concise, visually segmented PESTLE summary of Eiffage that’s easily editable and shareable for presentations, workshops, and client reports, enabling quick alignment across teams and streamlined discussion of external risks and market positioning.

Economic factors

Interest rates and financing

Higher borrowing costs—ECB policy rate at 4.00% (July 2024)—raise WACC for Eiffage concessions and EPC bids, squeezing returns and necessitating higher bid margins. Debt market tightness limits competitive bidding and reduces refinancing gains versus past low-rate cycles. Inflation-linked contracts help protect margins but indexation lags can still erode real returns. Active treasury management is critical for long-duration assets.

Construction cost inflation

Volatile input costs — e.g., European hot‑rolled coil ranged roughly €600–1,000/ton in 2022–24 — squeeze margins on fixed‑price contracts and raise bid risk for Eiffage. Supply‑chain hedging and multi‑year framework agreements have helped stabilize procurement and limit short‑term shocks. Design‑to‑cost, modular construction and prefabrication protect margins by reducing on‑site material exposure. Budget pressure can prompt clients to defer projects, slowing revenue recognition.

Public investment cycles

Public investment volumes for Eiffage are driven by fiscal space and stimulus: EU NextGenerationEU mobilises €806.9bn and France’s 2020 Relance was €100bn, shaping civil works demand. Election cycles (next French presidential vote 2027) and deficit rules influence award timing and contractor risk. EU multiyear transport and cohesion budgets (circa €330bn 2021–27) give planning visibility. Recurrent delays in budget execution squeeze working capital and cashflow.

Labor market dynamics

- Workforce: ~74,000 (2024)

- Skills gap: raises wages and delays

- Solutions: apprenticeships, EU mobility, prefabrication

- Risk: industrial relations affect schedules

Traffic and demand elasticity

Concession revenues for Eiffage closely track macro growth and mobility patterns, so shifts toward rail, micromobility or remote work change traffic mixes and reduce peak toll volumes, pressuring yields. Implementing dynamic pricing and higher service standards can partially stabilize cash flows and improve elasticity management. During downturns, increased demand risk prompts renegotiations with grantors and greater use of revenue-sharing mechanisms.

- Concession sensitivity

- Mode shift impact

- Dynamic pricing stabilises cash flow

- Downturn → renegotiation

EU funds and CEF steer pipeline to transport/energy; PPP/MEAT lift margins ETS raises costs

Higher ECB rate 4.00% (Jul 2024) raises WACC, tightening bids and refinancing; inflation indexation helps but lags. Volatile inputs (HRC ~€600–1,000/t in 2022–24) and supply shocks raise fixed‑price risk; prefabrication and hedging reduce exposure. Public investment (NextGenerationEU €806.9bn; EU transport/cohesion ~€330bn 2021–27) supports visibility; execution delays strain cashflow and working capital.

| Metric | Value |

|---|---|

| ECB rate (Jul 2024) | 4.00% |

| Workforce (2024) | ~74,000 |

| NextGenerationEU | €806.9bn |

Same Document Delivered

Eiffage PESTLE Analysis

The Eiffage PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors shaping the company’s operating environment. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The document is fully formatted and ready to download and use after purchase.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Eiffage faces shifting political regulations, infrastructure spending cycles and rising sustainability pressures that reshape project economics. Our PESTLE distills these external forces into clear risks and opportunities—ideal for investors, consultants and strategists. Download the full, ready-to-use analysis now to inform decisions and gain a competitive edge.

Political factors

EU infrastructure funding

Access to EU funds—cohesion policy €392.8bn (2021–27) and NextGenerationEU/RRF components within the €806.9bn package—shapes Eiffage’s project pipeline and margins. Shifts in allocations accelerate transport, energy and urban renewal projects; CEF’s €33.7bn focus on TEN-T and rail electrification benefits civil engineering units. Budget tightening delays awards and stretches tender timelines, squeezing cashflows and bid windows.

PPP policy direction

Government appetite for public–private partnerships shapes concession pipelines and directly affects Eiffage’s tender flow; stable frameworks unlock lifecycle revenues from design through operation, supporting its reported €20.3bn 2023 revenue base. Policy reversals or stricter value-for-money tests can sharply reduce greenfield PPP volumes, while political scrutiny of user fees or availability payments shifts risk sharing and compresses expected returns.

Public procurement rules

EU directives (2014/24/EU) and national laws govern procurement across a c.€2 trillion EU market (~14% of GDP), enforcing competition, transparency and local-content rules. Shift from lowest-price to MEAT award criteria boosts innovation incentives and life-cycle pricing. Faster permitting and streamlined approvals cut backlog-related delays and de-risk projects. Anti-corruption enforcement (OECD estimates 10–25% procurement loss to corruption) raises compliance costs but protects reputational capital.

Energy transition priorities

EU political decarbonization targets (‑55% GHG by 2030) drive demand for rail electrification, EV charging infrastructure and renewables-backed grids, while auctions and subsidies (eg. REPowerEU funding) shape near-term pipeline visibility. Industrial policy and CBAM, together with EU ETS carbon pricing at roughly €90–110/t in 2024–mid‑2025, push steel and cement costs higher. Policy stability remains critical to de‑risk investment in low‑carbon construction methods.

- Demand: rail, EV charging, grid expansion

- Finance: auctions/subsidies = pipeline visibility

- Supply costs: CBAM + EU ETS ~€90–110/t

- Investment: policy stability required for low‑carbon construction

Regional planning and decentralization

- Deal origination: regional/municipal first

- Public investment: ~70% local (INSEE 2021)

- Risk: delays from local political turnover

- Advantage: stakeholder management differentiator

EU funds and CEF steer pipeline to transport/energy; PPP/MEAT lift margins ETS raises costs

EU funding packages (€392.8bn cohesion; €806.9bn NextGenerationEU) and CEF €33.7bn tilt Eiffage’s pipeline to transport/energy projects, while PPP policy and MEAT procurement boost lifecycle margins supporting €20.3bn 2023 revenue. EU ETS ~€90–110/t (2024–mid‑2025) and CBAM raise steel/cement costs. Local governments supply ~70% of French public investment, increasing regional deal risk from political turnover.

| Factor | Key Figure |

|---|---|

| EU funding | €392.8bn / €806.9bn |

| CEF | €33.7bn |

| Revenue (Eiffage) | €20.3bn (2023) |

| EU ETS | €90–110/t (2024–mid‑2025) |

| Local investment (France) | ~70% (INSEE 2021) |

What is included in the product

Provides a concise PESTLE evaluation of Eiffage, detailing Political, Economic, Social, Technological, Environmental and Legal drivers with data-backed trends and region-specific regulatory context; designed to help executives, advisors and investors identify risks, opportunities and forward-looking strategic actions.

A concise, visually segmented PESTLE summary of Eiffage that’s easily editable and shareable for presentations, workshops, and client reports, enabling quick alignment across teams and streamlined discussion of external risks and market positioning.

Economic factors

Interest rates and financing

Higher borrowing costs—ECB policy rate at 4.00% (July 2024)—raise WACC for Eiffage concessions and EPC bids, squeezing returns and necessitating higher bid margins. Debt market tightness limits competitive bidding and reduces refinancing gains versus past low-rate cycles. Inflation-linked contracts help protect margins but indexation lags can still erode real returns. Active treasury management is critical for long-duration assets.

Construction cost inflation

Volatile input costs — e.g., European hot‑rolled coil ranged roughly €600–1,000/ton in 2022–24 — squeeze margins on fixed‑price contracts and raise bid risk for Eiffage. Supply‑chain hedging and multi‑year framework agreements have helped stabilize procurement and limit short‑term shocks. Design‑to‑cost, modular construction and prefabrication protect margins by reducing on‑site material exposure. Budget pressure can prompt clients to defer projects, slowing revenue recognition.

Public investment cycles

Public investment volumes for Eiffage are driven by fiscal space and stimulus: EU NextGenerationEU mobilises €806.9bn and France’s 2020 Relance was €100bn, shaping civil works demand. Election cycles (next French presidential vote 2027) and deficit rules influence award timing and contractor risk. EU multiyear transport and cohesion budgets (circa €330bn 2021–27) give planning visibility. Recurrent delays in budget execution squeeze working capital and cashflow.

Labor market dynamics

- Workforce: ~74,000 (2024)

- Skills gap: raises wages and delays

- Solutions: apprenticeships, EU mobility, prefabrication

- Risk: industrial relations affect schedules

Traffic and demand elasticity

Concession revenues for Eiffage closely track macro growth and mobility patterns, so shifts toward rail, micromobility or remote work change traffic mixes and reduce peak toll volumes, pressuring yields. Implementing dynamic pricing and higher service standards can partially stabilize cash flows and improve elasticity management. During downturns, increased demand risk prompts renegotiations with grantors and greater use of revenue-sharing mechanisms.

- Concession sensitivity

- Mode shift impact

- Dynamic pricing stabilises cash flow

- Downturn → renegotiation

EU funds and CEF steer pipeline to transport/energy; PPP/MEAT lift margins ETS raises costs

Higher ECB rate 4.00% (Jul 2024) raises WACC, tightening bids and refinancing; inflation indexation helps but lags. Volatile inputs (HRC ~€600–1,000/t in 2022–24) and supply shocks raise fixed‑price risk; prefabrication and hedging reduce exposure. Public investment (NextGenerationEU €806.9bn; EU transport/cohesion ~€330bn 2021–27) supports visibility; execution delays strain cashflow and working capital.

| Metric | Value |

|---|---|

| ECB rate (Jul 2024) | 4.00% |

| Workforce (2024) | ~74,000 |

| NextGenerationEU | €806.9bn |

Same Document Delivered

Eiffage PESTLE Analysis

The Eiffage PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors shaping the company’s operating environment. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The document is fully formatted and ready to download and use after purchase.