Eigenmann & Veronelli SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

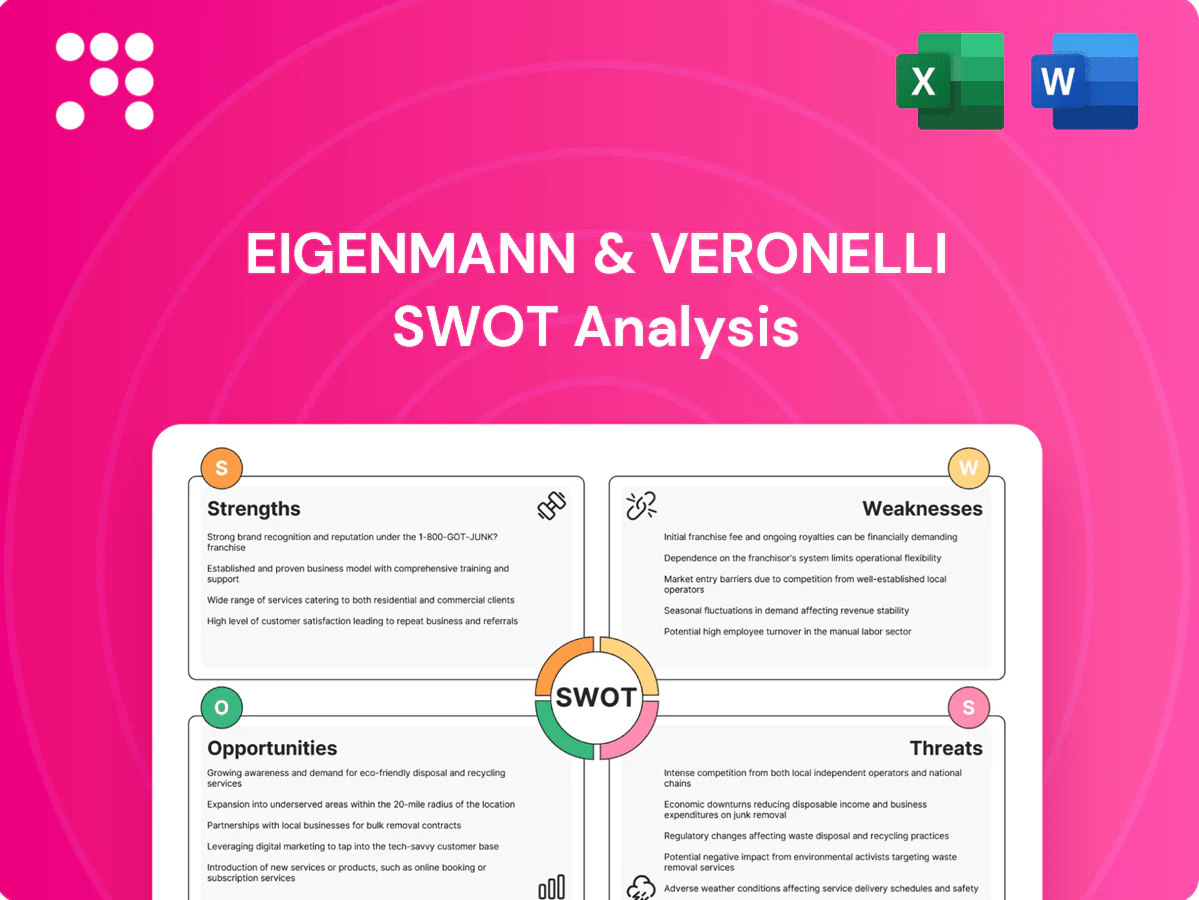

Eigenmann & Veronelli’s SWOT reveals core strengths, market risks, and growth drivers across its branded portfolio and distribution network; the preview highlights strategic issues and opportunity areas. Want the full picture—actionable recommendations, financial context, and editable Word + Excel deliverables? Purchase the complete SWOT to strategize, pitch, or invest with confidence.

Strengths

Diversified end-market exposure

Eigenmann & Veronelli serves food, pharma, cosmetics and industrial clients, spreading exposure across four end markets and reducing cyclicality and customer concentration. Cross-sector know-how lets the company balance demand when one vertical softens, enhancing resilience and upsell potential. This breadth supports cross-selling and portfolio synergies. The company is listed on B3 as EIGR3.

Strong supplier network

Deep relationships with global chemical producers secure Eigenmann & Veronelli access to specialty portfolios and innovation pipelines, aligning with a 2024 specialty chemicals market estimated at about USD 747 billion. Preferential supply agreements improve product availability and service levels for industrial clients. Co-development projects with principals increase customer stickiness and enhance credibility with regulated customers.

Value-added technical support

Eigenmann & Veronelli’s application labs and formulation expertise deliver tailored solutions beyond pure distribution, raising switching costs and enabling premium pricing; dedicated technical service shortens customers’ time-to-market and boosts product adoption. This capability reinforces the firm’s positioning as a solutions partner rather than a reseller, strengthening client retention and margin resilience.

Regulatory and quality competence

Experience navigating REACH (ECHA lists >22,000 registered substances in 2024), GMP, food-grade and cosmetic regulations reduces customer compliance burden; robust QA/QC and traceability underpin trust in sensitive applications and mitigate supply-chain risk. Certification frameworks open access to regulated pharma and food sectors (global pharma ≈ $1.5T in 2024), lowering client onboarding friction.

- REACH: ECHA >22,000 (2024)

- GMP/food-grade: access to $1.5T pharma market (2024)

- Traceability: reduces compliance & supply-chain risk

Efficient logistics and local presence

Efficient regional warehouses and last-mile delivery networks shorten lead times and raise reliability, enabling just-in-time replenishment for critical operations and reducing stockouts. Local-language support and deep market knowledge strengthen customer intimacy and retention, while tight inventory controls lower working capital needs. This operational density underpins scalable distribution and clear service differentiation.

- Regional warehouses: improved lead times

- Local-language support: stronger customer intimacy

- Inventory JIT: lower working capital

- Operational density: scalable service

Specialty chemicals and pharma: regulatory expertise boosts margins and shortens lead times

Eigenmann & Veronelli (B3: EIGR3) combines multi‑sector exposure (food, pharma, cosmetics, industrial) with specialty supplier partnerships, tapping a ~USD 747bn 2024 specialty chemicals market and a ~USD 1.5T global pharma market to drive cross‑selling, margins and resilience. Strong regulatory expertise (REACH >22,000 substances) and regional logistics shorten lead times and lower working capital.

| Metric | Value (2024) |

|---|---|

| Specialty market | USD 747bn |

| Pharma market | USD 1.5T |

| REACH entries | >22,000 |

| Listing | B3: EIGR3 |

What is included in the product

Provides a concise SWOT analysis identifying Eigenmann & Veronelli’s core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Provides a concise, visual SWOT matrix for Eigenmann & Veronelli to quickly align strategy and relieve analysis bottlenecks. Editable format enables fast updates for shifting priorities and seamless integration into reports and presentations.

Weaknesses

Margin pressure in distribution

Distribution is structurally lower-margin than manufacturing, and for Eigenmann & Veronelli this shows in thinner gross and operating spreads; operating spreads narrowed to low single digits in 2024 as retail pricing remained competitive. Pricing power is limited when products lack differentiation, compressing margins amid a crowded FMCG distribution market. Rising operating costs in 2024—logistics, fuel and labor—further squeeze spreads, requiring disciplined product-mix management and measurable efficiency gains.

Dependence on principal suppliers

Dependence on principal suppliers means loss of key supply lines can erode portfolio strength and revenue; Eigenmann & Veronelli’s top five principals account for over 70% of sales, amplifying this risk. Contract renegotiations may shift economics unfavorably, squeezing margins and cash flow. Supplier consolidation in 2024-25 has reduced bargaining leverage, concentrating exposure where few principals dominate niches.

Working capital intensity

Inventory holding and extended customer credit terms tie up substantial cash for Eigenmann & Veronelli, increasing working capital needs. Volatile demand in food distribution leads to slow-moving stock and periodic write-downs. Maintaining high service levels while improving inventory turns is operationally challenging. Elevated working capital intensity can limit the firm's ability to fund growth during downcycles.

Limited control over production

Reliance on third-party manufacturers limits Eigenmann & Veronelli’s influence over upstream quality and capacity, making product consistency and lead times dependent on external principals. Supply disruptions or quality deviations from these partners can directly impair service reliability and order fulfillment. Remediation timelines hinge on principal responsiveness, which can strain customer relationships and hurt repeat business.

Complex compliance burden

Serving heavily regulated sectors forces Eigenmann & Veronelli into continuous audits, documentation and staff training; since 2024 regulatory updates have accelerated, raising recurring compliance workload and costs. Ongoing rule changes require frequent process revisions and capital outlays, while non-compliance can trigger fines and reputational harm. The resulting complexity also slows onboarding of new products and partnerships.

- Audits, documentation, training required

- 2024 regulatory updates increased workload

- Non-compliance risks fines and reputation

- Complexity slows product onboarding

Margins at low single digits; top-5 > 70%; 2024 regs up

Distribution margins compressed—operating spreads narrowed to low single digits in 2024—while pricing power is limited and margin sensitivity remains high. Top five principals drive over 70% of sales, concentrating supplier risk and weakening bargaining leverage. Elevated working capital intensity ties cash to inventory and receivables; 2024 regulatory updates raised compliance costs and complexity.

| Metric | 2024 |

|---|---|

| Operating spread | Low single digits |

| Top-5 principals share | >70% |

| Regulatory burden | Increased (2024) |

What You See Is What You Get

Eigenmann & Veronelli SWOT Analysis

This is the actual Eigenmann & Veronelli SWOT analysis document you’re previewing—no sample, no surprises. The content below is taken directly from the full, editable report you’ll download after purchase. Buy now to unlock the complete, professionally formatted analysis for immediate use.

Go Beyond the Preview—Access the Full Strategic Report

Eigenmann & Veronelli’s SWOT reveals core strengths, market risks, and growth drivers across its branded portfolio and distribution network; the preview highlights strategic issues and opportunity areas. Want the full picture—actionable recommendations, financial context, and editable Word + Excel deliverables? Purchase the complete SWOT to strategize, pitch, or invest with confidence.

Strengths

Diversified end-market exposure

Eigenmann & Veronelli serves food, pharma, cosmetics and industrial clients, spreading exposure across four end markets and reducing cyclicality and customer concentration. Cross-sector know-how lets the company balance demand when one vertical softens, enhancing resilience and upsell potential. This breadth supports cross-selling and portfolio synergies. The company is listed on B3 as EIGR3.

Strong supplier network

Deep relationships with global chemical producers secure Eigenmann & Veronelli access to specialty portfolios and innovation pipelines, aligning with a 2024 specialty chemicals market estimated at about USD 747 billion. Preferential supply agreements improve product availability and service levels for industrial clients. Co-development projects with principals increase customer stickiness and enhance credibility with regulated customers.

Value-added technical support

Eigenmann & Veronelli’s application labs and formulation expertise deliver tailored solutions beyond pure distribution, raising switching costs and enabling premium pricing; dedicated technical service shortens customers’ time-to-market and boosts product adoption. This capability reinforces the firm’s positioning as a solutions partner rather than a reseller, strengthening client retention and margin resilience.

Regulatory and quality competence

Experience navigating REACH (ECHA lists >22,000 registered substances in 2024), GMP, food-grade and cosmetic regulations reduces customer compliance burden; robust QA/QC and traceability underpin trust in sensitive applications and mitigate supply-chain risk. Certification frameworks open access to regulated pharma and food sectors (global pharma ≈ $1.5T in 2024), lowering client onboarding friction.

- REACH: ECHA >22,000 (2024)

- GMP/food-grade: access to $1.5T pharma market (2024)

- Traceability: reduces compliance & supply-chain risk

Efficient logistics and local presence

Efficient regional warehouses and last-mile delivery networks shorten lead times and raise reliability, enabling just-in-time replenishment for critical operations and reducing stockouts. Local-language support and deep market knowledge strengthen customer intimacy and retention, while tight inventory controls lower working capital needs. This operational density underpins scalable distribution and clear service differentiation.

- Regional warehouses: improved lead times

- Local-language support: stronger customer intimacy

- Inventory JIT: lower working capital

- Operational density: scalable service

Specialty chemicals and pharma: regulatory expertise boosts margins and shortens lead times

Eigenmann & Veronelli (B3: EIGR3) combines multi‑sector exposure (food, pharma, cosmetics, industrial) with specialty supplier partnerships, tapping a ~USD 747bn 2024 specialty chemicals market and a ~USD 1.5T global pharma market to drive cross‑selling, margins and resilience. Strong regulatory expertise (REACH >22,000 substances) and regional logistics shorten lead times and lower working capital.

| Metric | Value (2024) |

|---|---|

| Specialty market | USD 747bn |

| Pharma market | USD 1.5T |

| REACH entries | >22,000 |

| Listing | B3: EIGR3 |

What is included in the product

Provides a concise SWOT analysis identifying Eigenmann & Veronelli’s core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Provides a concise, visual SWOT matrix for Eigenmann & Veronelli to quickly align strategy and relieve analysis bottlenecks. Editable format enables fast updates for shifting priorities and seamless integration into reports and presentations.

Weaknesses

Margin pressure in distribution

Distribution is structurally lower-margin than manufacturing, and for Eigenmann & Veronelli this shows in thinner gross and operating spreads; operating spreads narrowed to low single digits in 2024 as retail pricing remained competitive. Pricing power is limited when products lack differentiation, compressing margins amid a crowded FMCG distribution market. Rising operating costs in 2024—logistics, fuel and labor—further squeeze spreads, requiring disciplined product-mix management and measurable efficiency gains.

Dependence on principal suppliers

Dependence on principal suppliers means loss of key supply lines can erode portfolio strength and revenue; Eigenmann & Veronelli’s top five principals account for over 70% of sales, amplifying this risk. Contract renegotiations may shift economics unfavorably, squeezing margins and cash flow. Supplier consolidation in 2024-25 has reduced bargaining leverage, concentrating exposure where few principals dominate niches.

Working capital intensity

Inventory holding and extended customer credit terms tie up substantial cash for Eigenmann & Veronelli, increasing working capital needs. Volatile demand in food distribution leads to slow-moving stock and periodic write-downs. Maintaining high service levels while improving inventory turns is operationally challenging. Elevated working capital intensity can limit the firm's ability to fund growth during downcycles.

Limited control over production

Reliance on third-party manufacturers limits Eigenmann & Veronelli’s influence over upstream quality and capacity, making product consistency and lead times dependent on external principals. Supply disruptions or quality deviations from these partners can directly impair service reliability and order fulfillment. Remediation timelines hinge on principal responsiveness, which can strain customer relationships and hurt repeat business.

Complex compliance burden

Serving heavily regulated sectors forces Eigenmann & Veronelli into continuous audits, documentation and staff training; since 2024 regulatory updates have accelerated, raising recurring compliance workload and costs. Ongoing rule changes require frequent process revisions and capital outlays, while non-compliance can trigger fines and reputational harm. The resulting complexity also slows onboarding of new products and partnerships.

- Audits, documentation, training required

- 2024 regulatory updates increased workload

- Non-compliance risks fines and reputation

- Complexity slows product onboarding

Margins at low single digits; top-5 > 70%; 2024 regs up

Distribution margins compressed—operating spreads narrowed to low single digits in 2024—while pricing power is limited and margin sensitivity remains high. Top five principals drive over 70% of sales, concentrating supplier risk and weakening bargaining leverage. Elevated working capital intensity ties cash to inventory and receivables; 2024 regulatory updates raised compliance costs and complexity.

| Metric | 2024 |

|---|---|

| Operating spread | Low single digits |

| Top-5 principals share | >70% |

| Regulatory burden | Increased (2024) |

What You See Is What You Get

Eigenmann & Veronelli SWOT Analysis

This is the actual Eigenmann & Veronelli SWOT analysis document you’re previewing—no sample, no surprises. The content below is taken directly from the full, editable report you’ll download after purchase. Buy now to unlock the complete, professionally formatted analysis for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Eigenmann & Veronelli’s SWOT reveals core strengths, market risks, and growth drivers across its branded portfolio and distribution network; the preview highlights strategic issues and opportunity areas. Want the full picture—actionable recommendations, financial context, and editable Word + Excel deliverables? Purchase the complete SWOT to strategize, pitch, or invest with confidence.

Strengths

Diversified end-market exposure

Eigenmann & Veronelli serves food, pharma, cosmetics and industrial clients, spreading exposure across four end markets and reducing cyclicality and customer concentration. Cross-sector know-how lets the company balance demand when one vertical softens, enhancing resilience and upsell potential. This breadth supports cross-selling and portfolio synergies. The company is listed on B3 as EIGR3.

Strong supplier network

Deep relationships with global chemical producers secure Eigenmann & Veronelli access to specialty portfolios and innovation pipelines, aligning with a 2024 specialty chemicals market estimated at about USD 747 billion. Preferential supply agreements improve product availability and service levels for industrial clients. Co-development projects with principals increase customer stickiness and enhance credibility with regulated customers.

Value-added technical support

Eigenmann & Veronelli’s application labs and formulation expertise deliver tailored solutions beyond pure distribution, raising switching costs and enabling premium pricing; dedicated technical service shortens customers’ time-to-market and boosts product adoption. This capability reinforces the firm’s positioning as a solutions partner rather than a reseller, strengthening client retention and margin resilience.

Regulatory and quality competence

Experience navigating REACH (ECHA lists >22,000 registered substances in 2024), GMP, food-grade and cosmetic regulations reduces customer compliance burden; robust QA/QC and traceability underpin trust in sensitive applications and mitigate supply-chain risk. Certification frameworks open access to regulated pharma and food sectors (global pharma ≈ $1.5T in 2024), lowering client onboarding friction.

- REACH: ECHA >22,000 (2024)

- GMP/food-grade: access to $1.5T pharma market (2024)

- Traceability: reduces compliance & supply-chain risk

Efficient logistics and local presence

Efficient regional warehouses and last-mile delivery networks shorten lead times and raise reliability, enabling just-in-time replenishment for critical operations and reducing stockouts. Local-language support and deep market knowledge strengthen customer intimacy and retention, while tight inventory controls lower working capital needs. This operational density underpins scalable distribution and clear service differentiation.

- Regional warehouses: improved lead times

- Local-language support: stronger customer intimacy

- Inventory JIT: lower working capital

- Operational density: scalable service

Specialty chemicals and pharma: regulatory expertise boosts margins and shortens lead times

Eigenmann & Veronelli (B3: EIGR3) combines multi‑sector exposure (food, pharma, cosmetics, industrial) with specialty supplier partnerships, tapping a ~USD 747bn 2024 specialty chemicals market and a ~USD 1.5T global pharma market to drive cross‑selling, margins and resilience. Strong regulatory expertise (REACH >22,000 substances) and regional logistics shorten lead times and lower working capital.

| Metric | Value (2024) |

|---|---|

| Specialty market | USD 747bn |

| Pharma market | USD 1.5T |

| REACH entries | >22,000 |

| Listing | B3: EIGR3 |

What is included in the product

Provides a concise SWOT analysis identifying Eigenmann & Veronelli’s core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Provides a concise, visual SWOT matrix for Eigenmann & Veronelli to quickly align strategy and relieve analysis bottlenecks. Editable format enables fast updates for shifting priorities and seamless integration into reports and presentations.

Weaknesses

Margin pressure in distribution

Distribution is structurally lower-margin than manufacturing, and for Eigenmann & Veronelli this shows in thinner gross and operating spreads; operating spreads narrowed to low single digits in 2024 as retail pricing remained competitive. Pricing power is limited when products lack differentiation, compressing margins amid a crowded FMCG distribution market. Rising operating costs in 2024—logistics, fuel and labor—further squeeze spreads, requiring disciplined product-mix management and measurable efficiency gains.

Dependence on principal suppliers

Dependence on principal suppliers means loss of key supply lines can erode portfolio strength and revenue; Eigenmann & Veronelli’s top five principals account for over 70% of sales, amplifying this risk. Contract renegotiations may shift economics unfavorably, squeezing margins and cash flow. Supplier consolidation in 2024-25 has reduced bargaining leverage, concentrating exposure where few principals dominate niches.

Working capital intensity

Inventory holding and extended customer credit terms tie up substantial cash for Eigenmann & Veronelli, increasing working capital needs. Volatile demand in food distribution leads to slow-moving stock and periodic write-downs. Maintaining high service levels while improving inventory turns is operationally challenging. Elevated working capital intensity can limit the firm's ability to fund growth during downcycles.

Limited control over production

Reliance on third-party manufacturers limits Eigenmann & Veronelli’s influence over upstream quality and capacity, making product consistency and lead times dependent on external principals. Supply disruptions or quality deviations from these partners can directly impair service reliability and order fulfillment. Remediation timelines hinge on principal responsiveness, which can strain customer relationships and hurt repeat business.

Complex compliance burden

Serving heavily regulated sectors forces Eigenmann & Veronelli into continuous audits, documentation and staff training; since 2024 regulatory updates have accelerated, raising recurring compliance workload and costs. Ongoing rule changes require frequent process revisions and capital outlays, while non-compliance can trigger fines and reputational harm. The resulting complexity also slows onboarding of new products and partnerships.

- Audits, documentation, training required

- 2024 regulatory updates increased workload

- Non-compliance risks fines and reputation

- Complexity slows product onboarding

Margins at low single digits; top-5 > 70%; 2024 regs up

Distribution margins compressed—operating spreads narrowed to low single digits in 2024—while pricing power is limited and margin sensitivity remains high. Top five principals drive over 70% of sales, concentrating supplier risk and weakening bargaining leverage. Elevated working capital intensity ties cash to inventory and receivables; 2024 regulatory updates raised compliance costs and complexity.

| Metric | 2024 |

|---|---|

| Operating spread | Low single digits |

| Top-5 principals share | >70% |

| Regulatory burden | Increased (2024) |

What You See Is What You Get

Eigenmann & Veronelli SWOT Analysis

This is the actual Eigenmann & Veronelli SWOT analysis document you’re previewing—no sample, no surprises. The content below is taken directly from the full, editable report you’ll download after purchase. Buy now to unlock the complete, professionally formatted analysis for immediate use.