eismann PESTLE Analysis

Skip the Research. Get the Strategy.

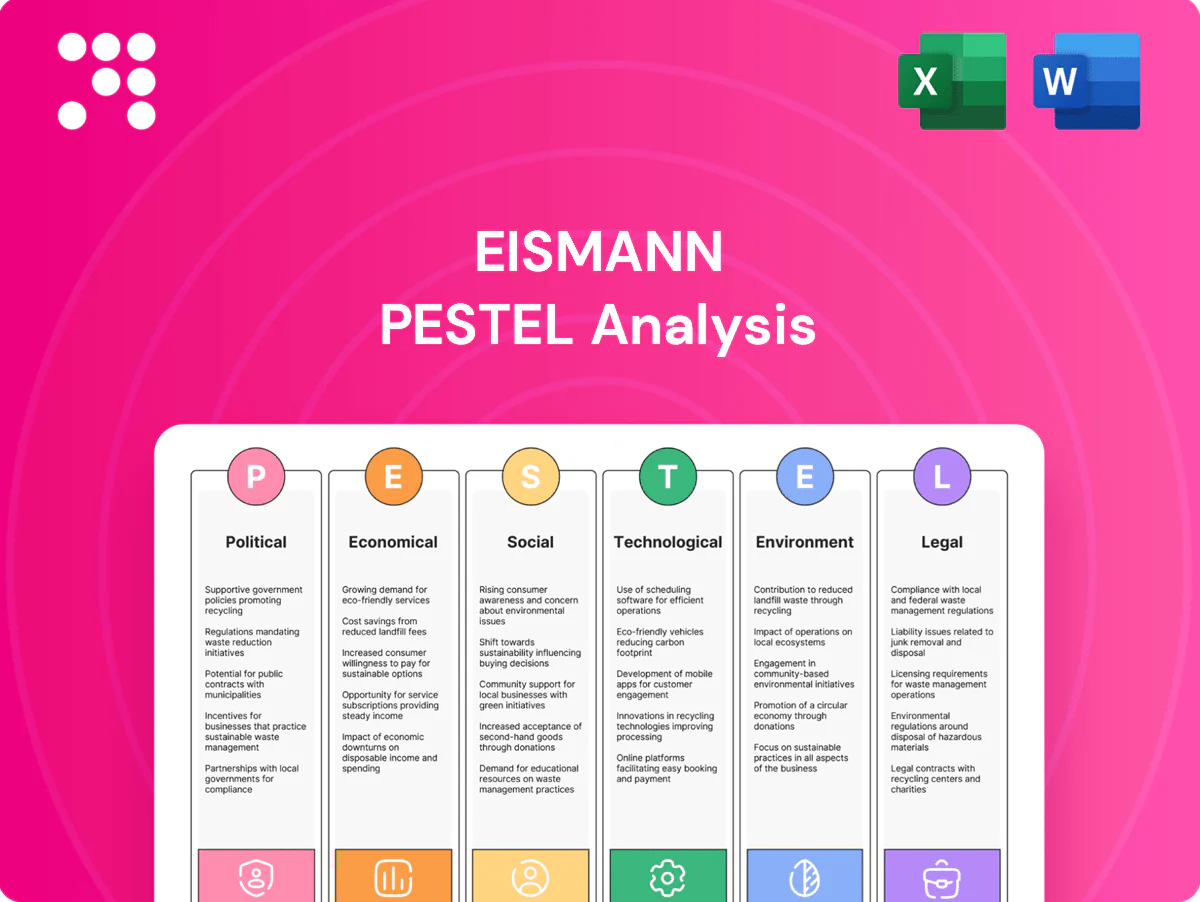

Unlock strategic clarity with our focused PESTLE Analysis of eismann. Explore how political, economic, social, technological, legal, and environmental forces are shaping its prospects. Ideal for investors and strategists seeking actionable context. Purchase the full report for the complete, ready-to-use intelligence and immediate download.

Political factors

EU food policy alignment

EU and German rules on food safety, labeling and nutrition—including the EU Commission's 2022 proposal for a single front-of-pack nutrition label and the Farm to Fork targets (50% reduction in pesticide use by 2030)—directly shape eismann’s sourcing and product development. The 2023–27 Common Agricultural Policy budget of about €387.6 billion and shifting trade/import controls can alter input availability and costs. Close monitoring of Brussels’ agendas enables preemptive portfolio and process adjustments, and proactive compliance reduces operational disruption risk for home-delivery services.

Energy and transport incentives

Government incentives for low-emission vehicles and refrigeration efficiency (EU targets for zero-emission new cars by 2035) can lower fleet TCO, with BloombergNEF noting electric vans reach TCO parity in Europe by 2025. Conversely, higher fuel taxes and an EU ETS price near €100/t in 2024 increased diesel-related delivery costs. Accessing EU and national grants (KfW, Recovery funds) accelerates cold-chain modernization. Policy volatility mandates scenario budgeting for route-based operations.

Trade and supply security

Geopolitical tensions and sanctions increasingly disrupt eismann’s fish, meat and ingredient imports, driving higher compliance and rerouting costs. Customs checks and non-tariff barriers slow frozen supply flows and raise lead times. Diversified sourcing across multiple countries reduces exposure to single-source shocks. Strategic regional depot stocks preserve service levels during border or logistics interruptions.

Local governance and zoning

Public health priorities

Government nutrition and food-safety campaigns shape consumer expectations and demand healthier options; EU laws on allergen labeling (Reg. 1169/2011) and traceability (Reg. 178/2002) mandate rigorous documentation. Aligning product ranges with WHO targets (salt <5 g/day, sugar reduction policies) aids market acceptance, while transparent controls under Reg. 2017/625 strengthen trust in direct sales channels.

- Reg. 1169/2011: mandatory allergen labeling

- Reg. 178/2002: traceability requirements

- WHO salt target: <5 g/day

- Reg. 2017/625: official controls boost trust

EU rules, CAP and LEZs reshape sourcing; EV vans parity ~2025

EU/German food-safety, labeling and Farm to Fork targets (50% pesticide cut by 2030) shape sourcing and SKUs; CAP budget ~€387.6bn (2023–27) affects input costs. EV fleet incentives and 300+ LEZs by 2024 lower long-term TCO (electric vans parity ~2025) but raise short-term CAPEX; sanctions and customs hikes increase lead times and compliance spend.

| Factor | Key 2024–25 Data |

|---|---|

| CAP | €387.6bn (2023–27) |

| EU ETS | ~€100/t (2024) |

| LEZs | 300+ cities (2024) |

What is included in the product

Provides a concise PESTLE evaluation of eismann across Political, Economic, Social, Technological, Environmental and Legal dimensions, grounded in current market and regulatory data and expanded into actionable sub-points; designed for executives and investors, region- and industry-specific, forward-looking, and formatted for direct use in plans, decks, or reports.

A concise, visually segmented PESTLE summary of eismann that’s easily editable and shareable for presentations, planning sessions, and client reports—helps align teams and surface external risks quickly.

Economic factors

Consumer spending elasticity

Euro area inflation eased to about 2.4% in 2024 (Eurostat) while German real wages rose roughly 0.9% (Destatis), moderating pressure on premium frozen purchase frequency. Frozen products deliver value through reduced waste and portion control, supporting retention. Flexible pricing and pack-size tiers limit downtrading, and loyalty incentives cushion volume swings by boosting repeat orders.

Energy and cold-chain costs

Electricity (German industrial rates ~€0.20/kWh in 2024, Eurostat) and refrigerants are major drivers of eismann’s storage and transport costs, with European gas/Ttf volatility (front-month ~€40/MWh average in 2024) pressuring margins for freezing‑intensive ops. Targeted efficiency investments and fuel/energy hedges have been used to stabilize costs, while higher route density materially improves unit economics in last‑mile frozen delivery.

Supply chain volatility

Protein and vegetable inputs can swing 10–30% seasonally, driven by harvests and feed markets; FAO indices and local feed barley trends showed heightened variability through 2023–24. Lead times and freight rates—container rates down roughly 60% from 2021 peaks by 2024—shrink freshness windows. Dual sourcing and 6–12 month supply contracts smooth variability, while 4–12 week safety stocks protect delivery reliability.

Labor market dynamics

Independent sales reps for eismann operate in tight German labor markets (unemployment ~3.6% in 2024), driving rising earnings expectations and higher recruitment/training costs; retention directly affects route coverage and service levels. Performance-based incentives mitigate peak-demand gaps, while digital sales and route-planning tools lift rep productivity and reduce missed deliveries.

- Labor tightness: unemployment ~3.6% (2024)

- Recruitment/training: higher OPEX per rep

- Incentives: align effort with peaks

- Digital tools: improve productivity & coverage

Interest rates and capex

Rising rates (ECB deposit rate 4.00% in mid‑2025; German 10y bund ~2.6%) increase financing costs for eismann’s fleet, depots and IT, extending payback thresholds for refrigeration upgrades and often pushing paybacks from ~4 to 6–8 years. Phased investments and leasing preserve cash and capex flexibility; prioritizing ROI‑positive efficiency projects is essential.

- Higher borrowing costs: ECB 4.00%

- Longer paybacks: ~4 → 6–8 yrs

- Mitigation: phased capex, leasing

- Focus: ROI‑positive efficiency

EU rules, CAP and LEZs reshape sourcing; EV vans parity ~2025

Euro‑area inflation ~2.4% (2024) and German wages +0.9% ease price pressure; unemployment ~3.6% tightens rep costs. Energy €0.20/kWh (2024) and gas volatility (~€40/MWh 2024) raise freezing OPEX; ECB rate 4.00% (mid‑2025) and 10y bund ~2.6% lengthen capex paybacks. Supply swings (protein/veg 10–30%) and container rates down ~60% vs 2021 affect input and freight costs; density and hedges protect margins.

| Metric | Value |

|---|---|

| Inflation (EA 2024) | 2.4% |

| Unemployment (DE 2024) | 3.6% |

| Industrial electricity (DE 2024) | €0.20/kWh |

| Gas (Ttf 2024 avg) | €40/MWh |

| ECB deposit (mid‑2025) | 4.00% |

| DE 10y bund | ~2.6% |

| Input volatility | 10–30% |

| Container rates vs 2021 | −60% |

Preview Before You Purchase

eismann PESTLE Analysis

The preview shown here is the exact Eismann PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the finished file.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our focused PESTLE Analysis of eismann. Explore how political, economic, social, technological, legal, and environmental forces are shaping its prospects. Ideal for investors and strategists seeking actionable context. Purchase the full report for the complete, ready-to-use intelligence and immediate download.

Political factors

EU food policy alignment

EU and German rules on food safety, labeling and nutrition—including the EU Commission's 2022 proposal for a single front-of-pack nutrition label and the Farm to Fork targets (50% reduction in pesticide use by 2030)—directly shape eismann’s sourcing and product development. The 2023–27 Common Agricultural Policy budget of about €387.6 billion and shifting trade/import controls can alter input availability and costs. Close monitoring of Brussels’ agendas enables preemptive portfolio and process adjustments, and proactive compliance reduces operational disruption risk for home-delivery services.

Energy and transport incentives

Government incentives for low-emission vehicles and refrigeration efficiency (EU targets for zero-emission new cars by 2035) can lower fleet TCO, with BloombergNEF noting electric vans reach TCO parity in Europe by 2025. Conversely, higher fuel taxes and an EU ETS price near €100/t in 2024 increased diesel-related delivery costs. Accessing EU and national grants (KfW, Recovery funds) accelerates cold-chain modernization. Policy volatility mandates scenario budgeting for route-based operations.

Trade and supply security

Geopolitical tensions and sanctions increasingly disrupt eismann’s fish, meat and ingredient imports, driving higher compliance and rerouting costs. Customs checks and non-tariff barriers slow frozen supply flows and raise lead times. Diversified sourcing across multiple countries reduces exposure to single-source shocks. Strategic regional depot stocks preserve service levels during border or logistics interruptions.

Local governance and zoning

Public health priorities

Government nutrition and food-safety campaigns shape consumer expectations and demand healthier options; EU laws on allergen labeling (Reg. 1169/2011) and traceability (Reg. 178/2002) mandate rigorous documentation. Aligning product ranges with WHO targets (salt <5 g/day, sugar reduction policies) aids market acceptance, while transparent controls under Reg. 2017/625 strengthen trust in direct sales channels.

- Reg. 1169/2011: mandatory allergen labeling

- Reg. 178/2002: traceability requirements

- WHO salt target: <5 g/day

- Reg. 2017/625: official controls boost trust

EU rules, CAP and LEZs reshape sourcing; EV vans parity ~2025

EU/German food-safety, labeling and Farm to Fork targets (50% pesticide cut by 2030) shape sourcing and SKUs; CAP budget ~€387.6bn (2023–27) affects input costs. EV fleet incentives and 300+ LEZs by 2024 lower long-term TCO (electric vans parity ~2025) but raise short-term CAPEX; sanctions and customs hikes increase lead times and compliance spend.

| Factor | Key 2024–25 Data |

|---|---|

| CAP | €387.6bn (2023–27) |

| EU ETS | ~€100/t (2024) |

| LEZs | 300+ cities (2024) |

What is included in the product

Provides a concise PESTLE evaluation of eismann across Political, Economic, Social, Technological, Environmental and Legal dimensions, grounded in current market and regulatory data and expanded into actionable sub-points; designed for executives and investors, region- and industry-specific, forward-looking, and formatted for direct use in plans, decks, or reports.

A concise, visually segmented PESTLE summary of eismann that’s easily editable and shareable for presentations, planning sessions, and client reports—helps align teams and surface external risks quickly.

Economic factors

Consumer spending elasticity

Euro area inflation eased to about 2.4% in 2024 (Eurostat) while German real wages rose roughly 0.9% (Destatis), moderating pressure on premium frozen purchase frequency. Frozen products deliver value through reduced waste and portion control, supporting retention. Flexible pricing and pack-size tiers limit downtrading, and loyalty incentives cushion volume swings by boosting repeat orders.

Energy and cold-chain costs

Electricity (German industrial rates ~€0.20/kWh in 2024, Eurostat) and refrigerants are major drivers of eismann’s storage and transport costs, with European gas/Ttf volatility (front-month ~€40/MWh average in 2024) pressuring margins for freezing‑intensive ops. Targeted efficiency investments and fuel/energy hedges have been used to stabilize costs, while higher route density materially improves unit economics in last‑mile frozen delivery.

Supply chain volatility

Protein and vegetable inputs can swing 10–30% seasonally, driven by harvests and feed markets; FAO indices and local feed barley trends showed heightened variability through 2023–24. Lead times and freight rates—container rates down roughly 60% from 2021 peaks by 2024—shrink freshness windows. Dual sourcing and 6–12 month supply contracts smooth variability, while 4–12 week safety stocks protect delivery reliability.

Labor market dynamics

Independent sales reps for eismann operate in tight German labor markets (unemployment ~3.6% in 2024), driving rising earnings expectations and higher recruitment/training costs; retention directly affects route coverage and service levels. Performance-based incentives mitigate peak-demand gaps, while digital sales and route-planning tools lift rep productivity and reduce missed deliveries.

- Labor tightness: unemployment ~3.6% (2024)

- Recruitment/training: higher OPEX per rep

- Incentives: align effort with peaks

- Digital tools: improve productivity & coverage

Interest rates and capex

Rising rates (ECB deposit rate 4.00% in mid‑2025; German 10y bund ~2.6%) increase financing costs for eismann’s fleet, depots and IT, extending payback thresholds for refrigeration upgrades and often pushing paybacks from ~4 to 6–8 years. Phased investments and leasing preserve cash and capex flexibility; prioritizing ROI‑positive efficiency projects is essential.

- Higher borrowing costs: ECB 4.00%

- Longer paybacks: ~4 → 6–8 yrs

- Mitigation: phased capex, leasing

- Focus: ROI‑positive efficiency

EU rules, CAP and LEZs reshape sourcing; EV vans parity ~2025

Euro‑area inflation ~2.4% (2024) and German wages +0.9% ease price pressure; unemployment ~3.6% tightens rep costs. Energy €0.20/kWh (2024) and gas volatility (~€40/MWh 2024) raise freezing OPEX; ECB rate 4.00% (mid‑2025) and 10y bund ~2.6% lengthen capex paybacks. Supply swings (protein/veg 10–30%) and container rates down ~60% vs 2021 affect input and freight costs; density and hedges protect margins.

| Metric | Value |

|---|---|

| Inflation (EA 2024) | 2.4% |

| Unemployment (DE 2024) | 3.6% |

| Industrial electricity (DE 2024) | €0.20/kWh |

| Gas (Ttf 2024 avg) | €40/MWh |

| ECB deposit (mid‑2025) | 4.00% |

| DE 10y bund | ~2.6% |

| Input volatility | 10–30% |

| Container rates vs 2021 | −60% |

Preview Before You Purchase

eismann PESTLE Analysis

The preview shown here is the exact Eismann PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the finished file.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our focused PESTLE Analysis of eismann. Explore how political, economic, social, technological, legal, and environmental forces are shaping its prospects. Ideal for investors and strategists seeking actionable context. Purchase the full report for the complete, ready-to-use intelligence and immediate download.

Political factors

EU food policy alignment

EU and German rules on food safety, labeling and nutrition—including the EU Commission's 2022 proposal for a single front-of-pack nutrition label and the Farm to Fork targets (50% reduction in pesticide use by 2030)—directly shape eismann’s sourcing and product development. The 2023–27 Common Agricultural Policy budget of about €387.6 billion and shifting trade/import controls can alter input availability and costs. Close monitoring of Brussels’ agendas enables preemptive portfolio and process adjustments, and proactive compliance reduces operational disruption risk for home-delivery services.

Energy and transport incentives

Government incentives for low-emission vehicles and refrigeration efficiency (EU targets for zero-emission new cars by 2035) can lower fleet TCO, with BloombergNEF noting electric vans reach TCO parity in Europe by 2025. Conversely, higher fuel taxes and an EU ETS price near €100/t in 2024 increased diesel-related delivery costs. Accessing EU and national grants (KfW, Recovery funds) accelerates cold-chain modernization. Policy volatility mandates scenario budgeting for route-based operations.

Trade and supply security

Geopolitical tensions and sanctions increasingly disrupt eismann’s fish, meat and ingredient imports, driving higher compliance and rerouting costs. Customs checks and non-tariff barriers slow frozen supply flows and raise lead times. Diversified sourcing across multiple countries reduces exposure to single-source shocks. Strategic regional depot stocks preserve service levels during border or logistics interruptions.

Local governance and zoning

Public health priorities

Government nutrition and food-safety campaigns shape consumer expectations and demand healthier options; EU laws on allergen labeling (Reg. 1169/2011) and traceability (Reg. 178/2002) mandate rigorous documentation. Aligning product ranges with WHO targets (salt <5 g/day, sugar reduction policies) aids market acceptance, while transparent controls under Reg. 2017/625 strengthen trust in direct sales channels.

- Reg. 1169/2011: mandatory allergen labeling

- Reg. 178/2002: traceability requirements

- WHO salt target: <5 g/day

- Reg. 2017/625: official controls boost trust

EU rules, CAP and LEZs reshape sourcing; EV vans parity ~2025

EU/German food-safety, labeling and Farm to Fork targets (50% pesticide cut by 2030) shape sourcing and SKUs; CAP budget ~€387.6bn (2023–27) affects input costs. EV fleet incentives and 300+ LEZs by 2024 lower long-term TCO (electric vans parity ~2025) but raise short-term CAPEX; sanctions and customs hikes increase lead times and compliance spend.

| Factor | Key 2024–25 Data |

|---|---|

| CAP | €387.6bn (2023–27) |

| EU ETS | ~€100/t (2024) |

| LEZs | 300+ cities (2024) |

What is included in the product

Provides a concise PESTLE evaluation of eismann across Political, Economic, Social, Technological, Environmental and Legal dimensions, grounded in current market and regulatory data and expanded into actionable sub-points; designed for executives and investors, region- and industry-specific, forward-looking, and formatted for direct use in plans, decks, or reports.

A concise, visually segmented PESTLE summary of eismann that’s easily editable and shareable for presentations, planning sessions, and client reports—helps align teams and surface external risks quickly.

Economic factors

Consumer spending elasticity

Euro area inflation eased to about 2.4% in 2024 (Eurostat) while German real wages rose roughly 0.9% (Destatis), moderating pressure on premium frozen purchase frequency. Frozen products deliver value through reduced waste and portion control, supporting retention. Flexible pricing and pack-size tiers limit downtrading, and loyalty incentives cushion volume swings by boosting repeat orders.

Energy and cold-chain costs

Electricity (German industrial rates ~€0.20/kWh in 2024, Eurostat) and refrigerants are major drivers of eismann’s storage and transport costs, with European gas/Ttf volatility (front-month ~€40/MWh average in 2024) pressuring margins for freezing‑intensive ops. Targeted efficiency investments and fuel/energy hedges have been used to stabilize costs, while higher route density materially improves unit economics in last‑mile frozen delivery.

Supply chain volatility

Protein and vegetable inputs can swing 10–30% seasonally, driven by harvests and feed markets; FAO indices and local feed barley trends showed heightened variability through 2023–24. Lead times and freight rates—container rates down roughly 60% from 2021 peaks by 2024—shrink freshness windows. Dual sourcing and 6–12 month supply contracts smooth variability, while 4–12 week safety stocks protect delivery reliability.

Labor market dynamics

Independent sales reps for eismann operate in tight German labor markets (unemployment ~3.6% in 2024), driving rising earnings expectations and higher recruitment/training costs; retention directly affects route coverage and service levels. Performance-based incentives mitigate peak-demand gaps, while digital sales and route-planning tools lift rep productivity and reduce missed deliveries.

- Labor tightness: unemployment ~3.6% (2024)

- Recruitment/training: higher OPEX per rep

- Incentives: align effort with peaks

- Digital tools: improve productivity & coverage

Interest rates and capex

Rising rates (ECB deposit rate 4.00% in mid‑2025; German 10y bund ~2.6%) increase financing costs for eismann’s fleet, depots and IT, extending payback thresholds for refrigeration upgrades and often pushing paybacks from ~4 to 6–8 years. Phased investments and leasing preserve cash and capex flexibility; prioritizing ROI‑positive efficiency projects is essential.

- Higher borrowing costs: ECB 4.00%

- Longer paybacks: ~4 → 6–8 yrs

- Mitigation: phased capex, leasing

- Focus: ROI‑positive efficiency

EU rules, CAP and LEZs reshape sourcing; EV vans parity ~2025

Euro‑area inflation ~2.4% (2024) and German wages +0.9% ease price pressure; unemployment ~3.6% tightens rep costs. Energy €0.20/kWh (2024) and gas volatility (~€40/MWh 2024) raise freezing OPEX; ECB rate 4.00% (mid‑2025) and 10y bund ~2.6% lengthen capex paybacks. Supply swings (protein/veg 10–30%) and container rates down ~60% vs 2021 affect input and freight costs; density and hedges protect margins.

| Metric | Value |

|---|---|

| Inflation (EA 2024) | 2.4% |

| Unemployment (DE 2024) | 3.6% |

| Industrial electricity (DE 2024) | €0.20/kWh |

| Gas (Ttf 2024 avg) | €40/MWh |

| ECB deposit (mid‑2025) | 4.00% |

| DE 10y bund | ~2.6% |

| Input volatility | 10–30% |

| Container rates vs 2021 | −60% |

Preview Before You Purchase

eismann PESTLE Analysis

The preview shown here is the exact Eismann PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the finished file.