Elbit Systems PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our PESTLE analysis for Elbit Systems reveals how political, economic, technological, social, legal and environmental forces shape its strategic risks and opportunities. Ideal for investors, consultants and strategists seeking concise, actionable intelligence. Purchase the full report to download the complete, editable analysis instantly.

Political factors

Defense-budget dependence

Elbit’s revenue—reported at $5.7 billion in FY2024—remains tightly linked to geopolitical priorities and government appropriations in Israel, the U.S. and key NATO and APAC markets. Election cycles and coalition shifts in buyer countries often accelerate or delay multi-year procurement programs and FMS approvals. Heightened regional tensions can spur urgent orders and backlog growth but also disrupt production, supply chains and on-time delivery.

Export controls/sanctions

Arms-export licenses and ITAR/EAR classification govern Elbit Systems’ market access, with US export approvals commonly adding 1–4 months to delivery timelines; tightening regimes have in recent years required product redesigns to de-scope controlled content. Destination-country sanctions can outright block deals or force rerouting of supply chains. Elbit’s compliance posture and licensing agility thus serve as clear competitive differentiators.

Offsets/industrial policy

Many buyers mandate local production, tech transfer or industrial participation, with offset rates typically ranging from 10–100% of contract value and countries like India enforcing roughly 30% offsets on large defense deals above $200m. Navigating offset obligations compresses margins and can dilute IP, often requiring Elbit to absorb CAPEX and local-content costs that can cut operating margins by mid-single-digit percentage points. National defense-industrial policies increasingly favor domestic champions, forcing JVs or localization strategies that reshape partner selection and long-term revenue mix.

Alliances and FMF flows

U.S. Foreign Military Financing and alliance frameworks materially influence Elbit Systems' addressable market, with U.S. FMF allocations about 6.9 billion USD in FY2024 shaping procurement in the Middle East and NATO partners. NATO interoperability standards (STANAG/EN) force open-architecture designs and affect R&D/integration timelines. Policy shifts in aid packages, including 2023–24 surge funding, can reprioritize Elbit’s production pipeline within months.

- FMF FY2024 ~6.9 billion USD

- NATO defense spend >1.2 trillion USD (2024)

- High pipeline sensitivity to rapid aid-policy changes

Political risk/geography

Operating from Israel exposes Elbit Systems to elevated security risks and logistical constraints near active conflict zones; Israel accounted for 3.8% of global arms exports in 2019–23 (SIPRI), shaping export sensitivities. Diplomatic relations and export controls limit tender eligibility in several regions, while diversifying production reduces country risk but raises supply-chain and compliance complexity.

- Home-country risk: Israel security volatility

- SIPRI 2019–23: Israel 3.8% of global arms exports

- Market access: diplomacy affects tenders

- Mitigation: diversify production — higher complexity

Defense supplier: $5.7B revenue vulnerable to budgets, sanctions, offsets

Elbit’s $5.7B FY2024 revenue is tightly tied to defense budgets, FMF flows and export licenses; political cycles and sanctions can speed or stall multi-year procurements. US ITAR/EAR and destination sanctions add 1–4 months or block deals; offsets and localization (often 10–30%+) compress margins. Home-country risk (Israel 3.8% of global arms exports 2019–23) raises supply-chain and tender constraints.

| Metric | Value |

|---|---|

| FY2024 Revenue | $5.7B |

| US FMF FY2024 | $6.9B |

| NATO Spend 2024 | >$1.2T |

| Israel SIPRI 2019–23 | 3.8% |

What is included in the product

Explores how macro-environmental factors impact Elbit Systems across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed for executives and investors to identify strategic risks, opportunities and forward-looking scenarios.

A concise, visually segmented PESTLE summary for Elbit Systems that relieves briefing pain points—easy to drop into presentations, annotate for regional context, and share across teams to align on external risks and strategic positioning.

Economic factors

Cyclicality/defense outlays

Macro cycles compress tax revenues and fiscal space for defense budgets; SIPRI reports global military spending at USD 2.24 trillion in 2023, constraining some modernization plans. In downturns procurement can slow, while crises trigger sharp spikes in spending. Multi-year programs grant Elbit visibility via secured backlog but remain exposed to deferrals and reprioritisations.

Currency/FX exposure

Elbit Systems earns revenue in USD, EUR, ILS and other currencies, with over 70% of sales generated from international markets, exposing margins to FX swings. Costs are incurred locally across production sites, creating natural currency offsets but leaving residual exposure on long-dated contracts. FX volatility has materially affected margins in recent years, so active hedging programs and contract-indexation are critical to protect pricing on multi-year deals.

Supply-chain inflation

Input-cost volatility in semiconductors, optics, composites and rare earths has pressured Elbit Systems program economics, with procurement-driven cost increases noted through 2024. Long-lead components have extended delivery schedules by roughly 6–12 months on complex subsystems. Active should-costing, multi-sourcing and strategic inventory helped preserve gross margins during 2024 supply disruptions. Ongoing supplier diversification remains critical into 2025.

Working-capital intensity

Working-capital intensity is elevated at Elbit due to milestone-based payments and inventory for bespoke systems that tie up cash, but advance payments and progress billing used in 2024 eased liquidity pressures; reported backlog of about $11.3bn at end-2024 supports conversion into free cash flow, with 2024 free cash flow turning positive after higher collections and progress-billing terms.

- Milestones: tie-up of cash

- Advance payments: improve liquidity

- Backlog ~$11.3bn (end-2024): underpins FCF

Market diversification

Market diversification across land, air, sea and training spreads program and platform risk; Elbit reported FY2023 revenue of about $5.6bn with an order backlog above $10bn, underpinned by broad product lines. Civil and security adjacencies (homeland, border, cyber) act as countercyclical buffers during defense spending swings. Deeper penetration in India, wider Asia and Eastern Europe supports higher volumes and pricing power.

- Multi-domain exposure: lowers concentration risk

- Adjacencies: provide demand resilience

- Growth markets: India/Asia/Eastern Europe lift volume/pricing

Defense supplier: $5.7B revenue vulnerable to budgets, sanctions, offsets

Macro cycles compress defense budgets; SIPRI reports global military spending $2.24tn (2023), causing procurement variability. Elbit's >70% international sales and revenues in USD/EUR/ILS expose margins to FX; backlog ~$11.3bn (end‑2024) and FY2023 revenue ~$5.6bn underpin liquidity; 2024 FCF turned positive.

| Metric | Value |

|---|---|

| Global military spend (2023) | $2.24tn |

| FY2023 revenue | $5.6bn |

| Backlog (end‑2024) | $11.3bn |

| International sales | >70% |

Preview the Actual Deliverable

Elbit Systems PESTLE Analysis

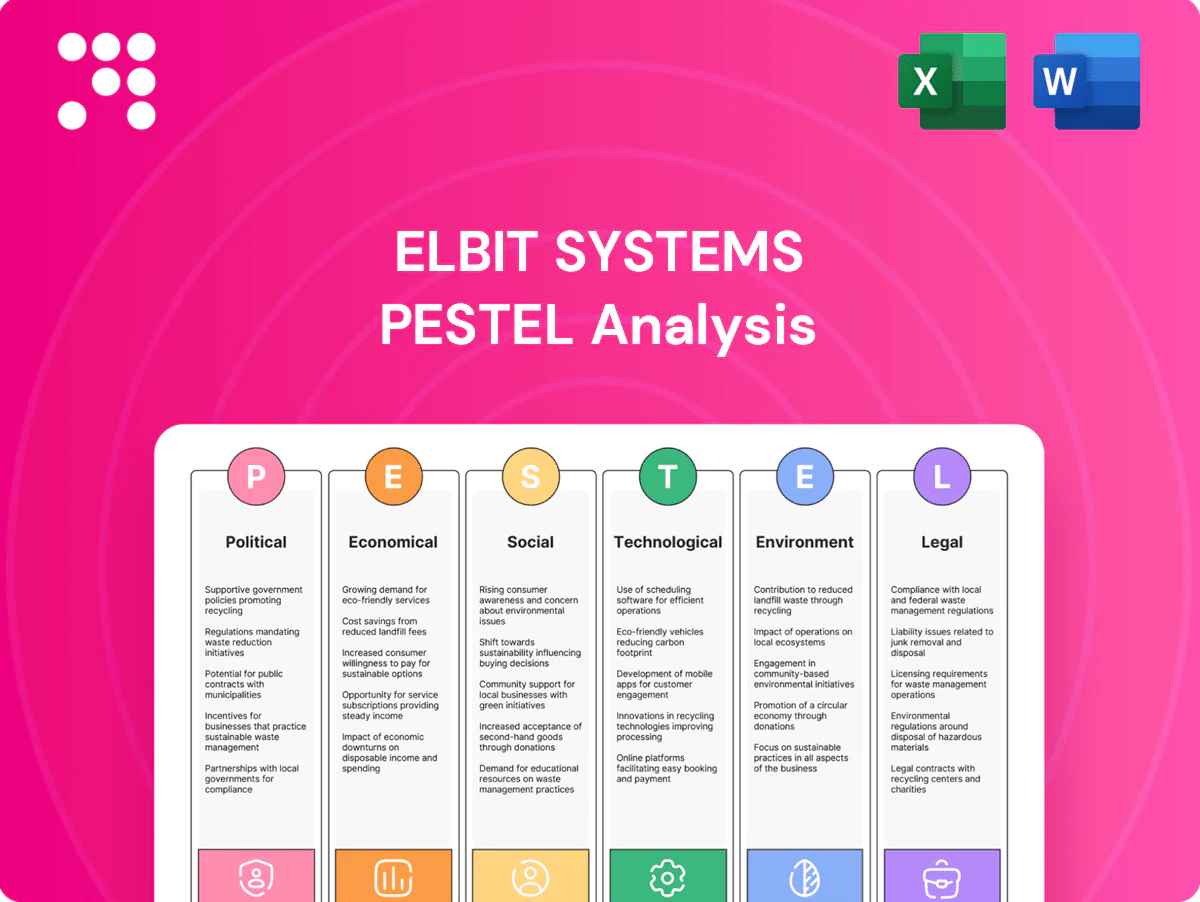

The Elbit Systems PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and the content and structure are identical to the downloadable file. No placeholders or teasers—what you see is the final, professionally structured report.

Your Competitive Advantage Starts with This Report

Our PESTLE analysis for Elbit Systems reveals how political, economic, technological, social, legal and environmental forces shape its strategic risks and opportunities. Ideal for investors, consultants and strategists seeking concise, actionable intelligence. Purchase the full report to download the complete, editable analysis instantly.

Political factors

Defense-budget dependence

Elbit’s revenue—reported at $5.7 billion in FY2024—remains tightly linked to geopolitical priorities and government appropriations in Israel, the U.S. and key NATO and APAC markets. Election cycles and coalition shifts in buyer countries often accelerate or delay multi-year procurement programs and FMS approvals. Heightened regional tensions can spur urgent orders and backlog growth but also disrupt production, supply chains and on-time delivery.

Export controls/sanctions

Arms-export licenses and ITAR/EAR classification govern Elbit Systems’ market access, with US export approvals commonly adding 1–4 months to delivery timelines; tightening regimes have in recent years required product redesigns to de-scope controlled content. Destination-country sanctions can outright block deals or force rerouting of supply chains. Elbit’s compliance posture and licensing agility thus serve as clear competitive differentiators.

Offsets/industrial policy

Many buyers mandate local production, tech transfer or industrial participation, with offset rates typically ranging from 10–100% of contract value and countries like India enforcing roughly 30% offsets on large defense deals above $200m. Navigating offset obligations compresses margins and can dilute IP, often requiring Elbit to absorb CAPEX and local-content costs that can cut operating margins by mid-single-digit percentage points. National defense-industrial policies increasingly favor domestic champions, forcing JVs or localization strategies that reshape partner selection and long-term revenue mix.

Alliances and FMF flows

U.S. Foreign Military Financing and alliance frameworks materially influence Elbit Systems' addressable market, with U.S. FMF allocations about 6.9 billion USD in FY2024 shaping procurement in the Middle East and NATO partners. NATO interoperability standards (STANAG/EN) force open-architecture designs and affect R&D/integration timelines. Policy shifts in aid packages, including 2023–24 surge funding, can reprioritize Elbit’s production pipeline within months.

- FMF FY2024 ~6.9 billion USD

- NATO defense spend >1.2 trillion USD (2024)

- High pipeline sensitivity to rapid aid-policy changes

Political risk/geography

Operating from Israel exposes Elbit Systems to elevated security risks and logistical constraints near active conflict zones; Israel accounted for 3.8% of global arms exports in 2019–23 (SIPRI), shaping export sensitivities. Diplomatic relations and export controls limit tender eligibility in several regions, while diversifying production reduces country risk but raises supply-chain and compliance complexity.

- Home-country risk: Israel security volatility

- SIPRI 2019–23: Israel 3.8% of global arms exports

- Market access: diplomacy affects tenders

- Mitigation: diversify production — higher complexity

Defense supplier: $5.7B revenue vulnerable to budgets, sanctions, offsets

Elbit’s $5.7B FY2024 revenue is tightly tied to defense budgets, FMF flows and export licenses; political cycles and sanctions can speed or stall multi-year procurements. US ITAR/EAR and destination sanctions add 1–4 months or block deals; offsets and localization (often 10–30%+) compress margins. Home-country risk (Israel 3.8% of global arms exports 2019–23) raises supply-chain and tender constraints.

| Metric | Value |

|---|---|

| FY2024 Revenue | $5.7B |

| US FMF FY2024 | $6.9B |

| NATO Spend 2024 | >$1.2T |

| Israel SIPRI 2019–23 | 3.8% |

What is included in the product

Explores how macro-environmental factors impact Elbit Systems across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed for executives and investors to identify strategic risks, opportunities and forward-looking scenarios.

A concise, visually segmented PESTLE summary for Elbit Systems that relieves briefing pain points—easy to drop into presentations, annotate for regional context, and share across teams to align on external risks and strategic positioning.

Economic factors

Cyclicality/defense outlays

Macro cycles compress tax revenues and fiscal space for defense budgets; SIPRI reports global military spending at USD 2.24 trillion in 2023, constraining some modernization plans. In downturns procurement can slow, while crises trigger sharp spikes in spending. Multi-year programs grant Elbit visibility via secured backlog but remain exposed to deferrals and reprioritisations.

Currency/FX exposure

Elbit Systems earns revenue in USD, EUR, ILS and other currencies, with over 70% of sales generated from international markets, exposing margins to FX swings. Costs are incurred locally across production sites, creating natural currency offsets but leaving residual exposure on long-dated contracts. FX volatility has materially affected margins in recent years, so active hedging programs and contract-indexation are critical to protect pricing on multi-year deals.

Supply-chain inflation

Input-cost volatility in semiconductors, optics, composites and rare earths has pressured Elbit Systems program economics, with procurement-driven cost increases noted through 2024. Long-lead components have extended delivery schedules by roughly 6–12 months on complex subsystems. Active should-costing, multi-sourcing and strategic inventory helped preserve gross margins during 2024 supply disruptions. Ongoing supplier diversification remains critical into 2025.

Working-capital intensity

Working-capital intensity is elevated at Elbit due to milestone-based payments and inventory for bespoke systems that tie up cash, but advance payments and progress billing used in 2024 eased liquidity pressures; reported backlog of about $11.3bn at end-2024 supports conversion into free cash flow, with 2024 free cash flow turning positive after higher collections and progress-billing terms.

- Milestones: tie-up of cash

- Advance payments: improve liquidity

- Backlog ~$11.3bn (end-2024): underpins FCF

Market diversification

Market diversification across land, air, sea and training spreads program and platform risk; Elbit reported FY2023 revenue of about $5.6bn with an order backlog above $10bn, underpinned by broad product lines. Civil and security adjacencies (homeland, border, cyber) act as countercyclical buffers during defense spending swings. Deeper penetration in India, wider Asia and Eastern Europe supports higher volumes and pricing power.

- Multi-domain exposure: lowers concentration risk

- Adjacencies: provide demand resilience

- Growth markets: India/Asia/Eastern Europe lift volume/pricing

Defense supplier: $5.7B revenue vulnerable to budgets, sanctions, offsets

Macro cycles compress defense budgets; SIPRI reports global military spending $2.24tn (2023), causing procurement variability. Elbit's >70% international sales and revenues in USD/EUR/ILS expose margins to FX; backlog ~$11.3bn (end‑2024) and FY2023 revenue ~$5.6bn underpin liquidity; 2024 FCF turned positive.

| Metric | Value |

|---|---|

| Global military spend (2023) | $2.24tn |

| FY2023 revenue | $5.6bn |

| Backlog (end‑2024) | $11.3bn |

| International sales | >70% |

Preview the Actual Deliverable

Elbit Systems PESTLE Analysis

The Elbit Systems PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and the content and structure are identical to the downloadable file. No placeholders or teasers—what you see is the final, professionally structured report.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Our PESTLE analysis for Elbit Systems reveals how political, economic, technological, social, legal and environmental forces shape its strategic risks and opportunities. Ideal for investors, consultants and strategists seeking concise, actionable intelligence. Purchase the full report to download the complete, editable analysis instantly.

Political factors

Defense-budget dependence

Elbit’s revenue—reported at $5.7 billion in FY2024—remains tightly linked to geopolitical priorities and government appropriations in Israel, the U.S. and key NATO and APAC markets. Election cycles and coalition shifts in buyer countries often accelerate or delay multi-year procurement programs and FMS approvals. Heightened regional tensions can spur urgent orders and backlog growth but also disrupt production, supply chains and on-time delivery.

Export controls/sanctions

Arms-export licenses and ITAR/EAR classification govern Elbit Systems’ market access, with US export approvals commonly adding 1–4 months to delivery timelines; tightening regimes have in recent years required product redesigns to de-scope controlled content. Destination-country sanctions can outright block deals or force rerouting of supply chains. Elbit’s compliance posture and licensing agility thus serve as clear competitive differentiators.

Offsets/industrial policy

Many buyers mandate local production, tech transfer or industrial participation, with offset rates typically ranging from 10–100% of contract value and countries like India enforcing roughly 30% offsets on large defense deals above $200m. Navigating offset obligations compresses margins and can dilute IP, often requiring Elbit to absorb CAPEX and local-content costs that can cut operating margins by mid-single-digit percentage points. National defense-industrial policies increasingly favor domestic champions, forcing JVs or localization strategies that reshape partner selection and long-term revenue mix.

Alliances and FMF flows

U.S. Foreign Military Financing and alliance frameworks materially influence Elbit Systems' addressable market, with U.S. FMF allocations about 6.9 billion USD in FY2024 shaping procurement in the Middle East and NATO partners. NATO interoperability standards (STANAG/EN) force open-architecture designs and affect R&D/integration timelines. Policy shifts in aid packages, including 2023–24 surge funding, can reprioritize Elbit’s production pipeline within months.

- FMF FY2024 ~6.9 billion USD

- NATO defense spend >1.2 trillion USD (2024)

- High pipeline sensitivity to rapid aid-policy changes

Political risk/geography

Operating from Israel exposes Elbit Systems to elevated security risks and logistical constraints near active conflict zones; Israel accounted for 3.8% of global arms exports in 2019–23 (SIPRI), shaping export sensitivities. Diplomatic relations and export controls limit tender eligibility in several regions, while diversifying production reduces country risk but raises supply-chain and compliance complexity.

- Home-country risk: Israel security volatility

- SIPRI 2019–23: Israel 3.8% of global arms exports

- Market access: diplomacy affects tenders

- Mitigation: diversify production — higher complexity

Defense supplier: $5.7B revenue vulnerable to budgets, sanctions, offsets

Elbit’s $5.7B FY2024 revenue is tightly tied to defense budgets, FMF flows and export licenses; political cycles and sanctions can speed or stall multi-year procurements. US ITAR/EAR and destination sanctions add 1–4 months or block deals; offsets and localization (often 10–30%+) compress margins. Home-country risk (Israel 3.8% of global arms exports 2019–23) raises supply-chain and tender constraints.

| Metric | Value |

|---|---|

| FY2024 Revenue | $5.7B |

| US FMF FY2024 | $6.9B |

| NATO Spend 2024 | >$1.2T |

| Israel SIPRI 2019–23 | 3.8% |

What is included in the product

Explores how macro-environmental factors impact Elbit Systems across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed for executives and investors to identify strategic risks, opportunities and forward-looking scenarios.

A concise, visually segmented PESTLE summary for Elbit Systems that relieves briefing pain points—easy to drop into presentations, annotate for regional context, and share across teams to align on external risks and strategic positioning.

Economic factors

Cyclicality/defense outlays

Macro cycles compress tax revenues and fiscal space for defense budgets; SIPRI reports global military spending at USD 2.24 trillion in 2023, constraining some modernization plans. In downturns procurement can slow, while crises trigger sharp spikes in spending. Multi-year programs grant Elbit visibility via secured backlog but remain exposed to deferrals and reprioritisations.

Currency/FX exposure

Elbit Systems earns revenue in USD, EUR, ILS and other currencies, with over 70% of sales generated from international markets, exposing margins to FX swings. Costs are incurred locally across production sites, creating natural currency offsets but leaving residual exposure on long-dated contracts. FX volatility has materially affected margins in recent years, so active hedging programs and contract-indexation are critical to protect pricing on multi-year deals.

Supply-chain inflation

Input-cost volatility in semiconductors, optics, composites and rare earths has pressured Elbit Systems program economics, with procurement-driven cost increases noted through 2024. Long-lead components have extended delivery schedules by roughly 6–12 months on complex subsystems. Active should-costing, multi-sourcing and strategic inventory helped preserve gross margins during 2024 supply disruptions. Ongoing supplier diversification remains critical into 2025.

Working-capital intensity

Working-capital intensity is elevated at Elbit due to milestone-based payments and inventory for bespoke systems that tie up cash, but advance payments and progress billing used in 2024 eased liquidity pressures; reported backlog of about $11.3bn at end-2024 supports conversion into free cash flow, with 2024 free cash flow turning positive after higher collections and progress-billing terms.

- Milestones: tie-up of cash

- Advance payments: improve liquidity

- Backlog ~$11.3bn (end-2024): underpins FCF

Market diversification

Market diversification across land, air, sea and training spreads program and platform risk; Elbit reported FY2023 revenue of about $5.6bn with an order backlog above $10bn, underpinned by broad product lines. Civil and security adjacencies (homeland, border, cyber) act as countercyclical buffers during defense spending swings. Deeper penetration in India, wider Asia and Eastern Europe supports higher volumes and pricing power.

- Multi-domain exposure: lowers concentration risk

- Adjacencies: provide demand resilience

- Growth markets: India/Asia/Eastern Europe lift volume/pricing

Defense supplier: $5.7B revenue vulnerable to budgets, sanctions, offsets

Macro cycles compress defense budgets; SIPRI reports global military spending $2.24tn (2023), causing procurement variability. Elbit's >70% international sales and revenues in USD/EUR/ILS expose margins to FX; backlog ~$11.3bn (end‑2024) and FY2023 revenue ~$5.6bn underpin liquidity; 2024 FCF turned positive.

| Metric | Value |

|---|---|

| Global military spend (2023) | $2.24tn |

| FY2023 revenue | $5.6bn |

| Backlog (end‑2024) | $11.3bn |

| International sales | >70% |

Preview the Actual Deliverable

Elbit Systems PESTLE Analysis

The Elbit Systems PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and the content and structure are identical to the downloadable file. No placeholders or teasers—what you see is the final, professionally structured report.