Elekta Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Elekta faces moderate supplier power, high buyer scrutiny, regulatory-driven barriers to entry, intense rivalry among oncology-tech players, and evolving substitute threats from emerging therapies; this snapshot highlights key pressure points shaping margins and innovation. The full Porter's Five Forces Analysis unpacks force-by-force ratings, data and strategic implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized component suppliers concentration

Linear accelerator tubes, beam-shaping devices, high-precision bearings and rare-earth magnets come from a small set of qualified vendors, giving suppliers clear leverage on price and lead times. Dual-sourcing is constrained by lengthy qualification and regulatory validation, raising switching costs and inventory needs. Major rare-earth magnet capacity is concentrated in China, increasing geopolitical supply risk. Any supplier disruption can postpone Elekta system deliveries and service SLAs.

Radioisotope and dosimetry dependencies

Brachytherapy sources (Ir-192 half-life 73.83 days; Co-60 half-life 5.27 years), dosimeters and QA phantoms depend on tightly regulated isotope and measurement suppliers subject to IAEA and national certification, limiting vendor switching. Certification and handling constraints raise switching costs and make price hikes hard to offset without product redesign. Strategic inventory management and long-term contracts are vital to mitigate supply and cost risk.

Advanced electronics and semiconductor exposure

Elekta relies on high-spec semiconductors, GPUs and FPGAs for control systems and imaging, and cyclical shortages have previously increased lead times and component costs, forcing production delays; substituting parts typically requires engineering changes and regulatory re-approval, making swaps costly and slow. Close supplier collaboration and design-for-availability strategies materially reduce this supplier power and operational risk.

Software stack and cloud infrastructure

Treatment planning, oncology information systems and AI modules rely on third-party toolkits and cloud providers; 2024 market shares concentrate with AWS ~31%, Azure ~24% and GCP ~11%, raising licensing and interoperability switching costs. Security and certifications (ISO 27001, HIPAA, GDPR) increase vendor stickiness; negotiation power improves with Elekta scale but is bounded by compliance-driven dependency.

- Dependency: third-party SDKs, cloud APIs

- Switching cost: licensing + integration

- Stickiness: security/compliance certifications

- Leverage: scale helps but compliance caps bargaining

Service parts and field logistics

- Limited substitutes: strict QA/traceability raises supplier power

- Logistics impact: regional partners determine 24–72h response and costs

- SLAs drive inventory: elevated buffer stocks increase OPEX/working capital

- Calibration suppliers: concentrated tech suppliers can exert price pressure

- Market scale 2024: global aftermarket >$100bn

Supply risk: China ~80% rare-earths; cloud 31%/24%/11%

Suppliers hold significant leverage across linac components, rare-earth magnets (China ~80% processing share 2024) and calibrated spares, raising prices and lead times. Dual-sourcing is limited by regulatory requalification and isotope handling (Ir-192 half-life 73.83 days), increasing switching costs and inventory. Cloud/toolkit concentration (AWS ~31%, Azure ~24%, GCP ~11% 2024) and semiconductors add stickiness and cost risk.

| Category | Concentration | 2024 Impact |

|---|---|---|

| Rare-earths | China ~80% | High geopolitical supply risk |

| Cloud | AWS 31%/Azure 24%/GCP 11% | Licensing/switch costs |

| Aftermarket | Fragmented but large | Market >$100bn |

What is included in the product

Combines analysis of competitive rivalry, buyer and supplier power, substitution and entry threats to assess Elekta's strategic position in radiotherapy and oncology equipment markets, highlighting disruptive technologies, pricing pressures, and barriers that shape its profitability and growth prospects.

A clear, one-sheet Porter's Five Forces analysis for Elekta—perfect for quick strategic decisions; customize pressure levels and swap in current data to assess supplier, buyer, rivalry, substitutes, and new entrant threats.

Customers Bargaining Power

Consolidated hospital systems and GPOs

Consolidated IDNs and GPOs, which serve over 90% of US hospitals, push Elekta for aggressive pricing and contract terms, intensifying margin pressure.

Multi-year tenders and blanket agreements create repeated competitive auctions, often driving supplier discounts in the 10–25% range.

Buyers routinely demand bundled service and software concessions, and fleet refresh cycles every 7–10 years create clear switching windows.

Public tenders and reimbursement constraints

National health systems award many radiotherapy contracts via price-centric tenders, where price often counts for 30–70% of scoring; reimbursement caps in 2024 continue to constrain achievable ASPs, depressing device prices by mid-single digits annually in several EU markets. Lengthy budget cycles extend negotiations and favor lowest total cost of ownership, while proven cost-effectiveness (QALY gains, lower retreatment rates) materially influences award decisions.

High switching costs but evaluative power

Installed-base integration with workflows, QA and training creates strong inertia—Elekta’s global installed base exceeds 5,000 systems, driving high switching costs—yet buyers use cross-vendor pilots and head-to-head trials to extract concessions. Contracts now hinge on uptime (industry target ~98–99%), dose-accuracy tolerances (~±2%) and adaptive-RT capabilities (adoption ~10% in 2024), and performance-based clauses appear in over 30% of recent procurements.

Demand for comprehensive solutions

In 2024 customers increasingly demand end-to-end ecosystems covering hardware, treatment planning and oncology IT, using that leverage to seek package discounts and unified SLAs; interoperability with existing systems is frequently a condition of sale, and demonstrated outcomes data plus usability carry high decision weight.

- End-to-end ecosystems drive bundled pricing and SLA demands

- Interoperability often a formal sales requirement

- Outcomes evidence and usability are primary purchase criteria

Aftermarket service leverage

Aftermarket service leverage is central for Elekta because service contracts and upgrades drive recurring revenue and lifetime value, and Elekta's 2024 reports emphasize services as a strategic recurring segment. Buyers use competitive service bids to push down fees, making uptime guarantees (commonly 99% SLAs) and remote diagnostics table stakes. Transparent TCO and predictable lifecycle costs are decisive for renewal and upgrade timing.

- Service-driven recurring revenue: highlighted in Elekta 2024 disclosures

- Competitive bids compress margins, buyers seek 99%+ uptime

- Remote diagnostics standard; TCO transparency influences renewals

IDN/GPO leverage: >90% coverage, 10–25% discounts

Consolidated IDNs/GPOs (covering >90% of US hospitals) and price-focused tenders (price weight 30–70%) give customers strong leverage, pushing discounts often 10–25% and compressing ASPs. Multi-year contracts, bundled service/software demands and 5,000+ installed base create switching windows but high inertia; uptime SLAs (~99%) and adaptive-RT adoption (~10% in 2024) shape negotiations.

| Metric | 2024 value |

|---|---|

| IDN/GPO coverage | >90% US hospitals |

| Typical supplier discounts | 10–25% |

| Price weight in tenders | 30–70% |

| Installed base | >5,000 systems |

| Uptime SLAs | ~99% |

| Adaptive-RT adoption | ~10% |

What You See Is What You Get

Elekta Porter's Five Forces Analysis

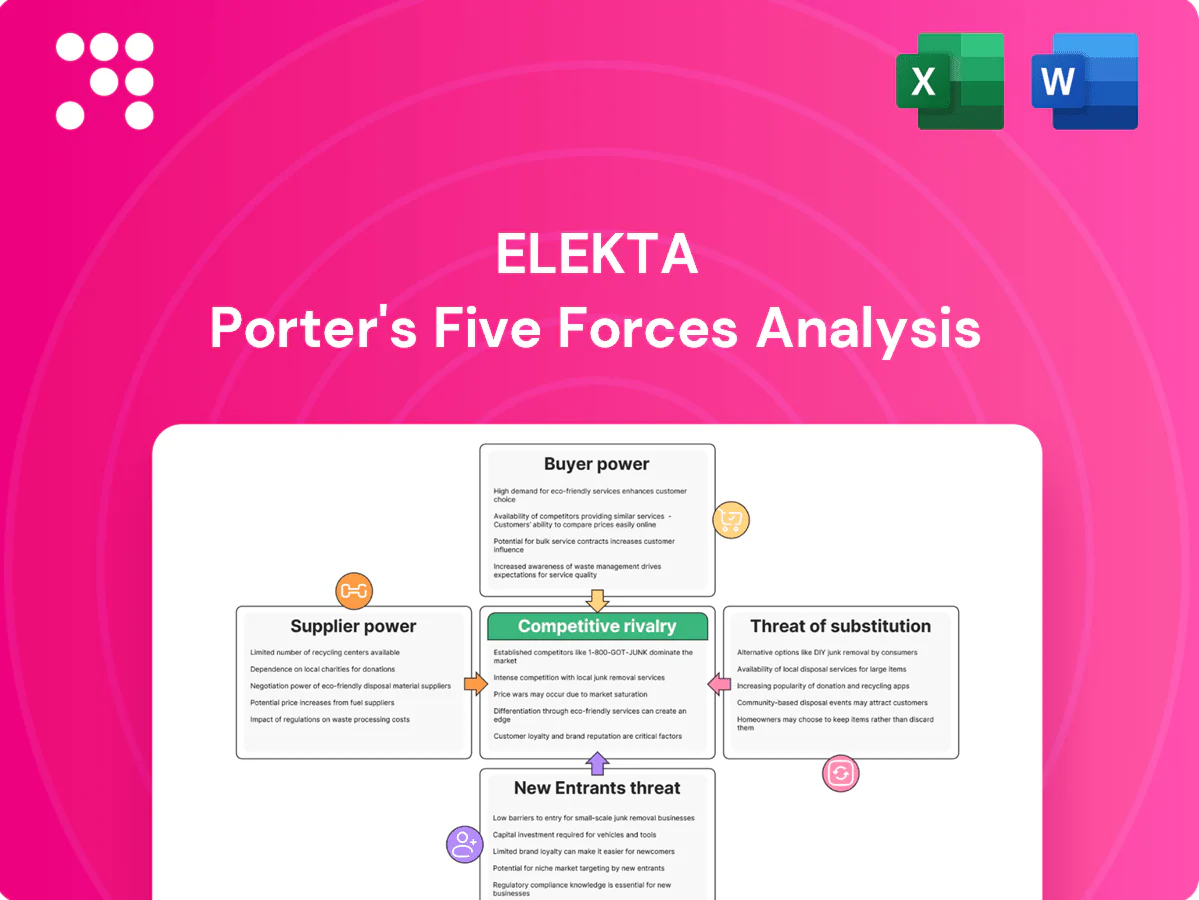

This preview shows the exact Elekta Porter’s Five Forces analysis you'll receive after purchase—fully formatted and ready for use. It covers supplier power, buyer power, threat of entrants, threat of substitutes, and competitive rivalry specific to Elekta. No placeholders or samples—instant download upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Elekta faces moderate supplier power, high buyer scrutiny, regulatory-driven barriers to entry, intense rivalry among oncology-tech players, and evolving substitute threats from emerging therapies; this snapshot highlights key pressure points shaping margins and innovation. The full Porter's Five Forces Analysis unpacks force-by-force ratings, data and strategic implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized component suppliers concentration

Linear accelerator tubes, beam-shaping devices, high-precision bearings and rare-earth magnets come from a small set of qualified vendors, giving suppliers clear leverage on price and lead times. Dual-sourcing is constrained by lengthy qualification and regulatory validation, raising switching costs and inventory needs. Major rare-earth magnet capacity is concentrated in China, increasing geopolitical supply risk. Any supplier disruption can postpone Elekta system deliveries and service SLAs.

Radioisotope and dosimetry dependencies

Brachytherapy sources (Ir-192 half-life 73.83 days; Co-60 half-life 5.27 years), dosimeters and QA phantoms depend on tightly regulated isotope and measurement suppliers subject to IAEA and national certification, limiting vendor switching. Certification and handling constraints raise switching costs and make price hikes hard to offset without product redesign. Strategic inventory management and long-term contracts are vital to mitigate supply and cost risk.

Advanced electronics and semiconductor exposure

Elekta relies on high-spec semiconductors, GPUs and FPGAs for control systems and imaging, and cyclical shortages have previously increased lead times and component costs, forcing production delays; substituting parts typically requires engineering changes and regulatory re-approval, making swaps costly and slow. Close supplier collaboration and design-for-availability strategies materially reduce this supplier power and operational risk.

Software stack and cloud infrastructure

Treatment planning, oncology information systems and AI modules rely on third-party toolkits and cloud providers; 2024 market shares concentrate with AWS ~31%, Azure ~24% and GCP ~11%, raising licensing and interoperability switching costs. Security and certifications (ISO 27001, HIPAA, GDPR) increase vendor stickiness; negotiation power improves with Elekta scale but is bounded by compliance-driven dependency.

- Dependency: third-party SDKs, cloud APIs

- Switching cost: licensing + integration

- Stickiness: security/compliance certifications

- Leverage: scale helps but compliance caps bargaining

Service parts and field logistics

- Limited substitutes: strict QA/traceability raises supplier power

- Logistics impact: regional partners determine 24–72h response and costs

- SLAs drive inventory: elevated buffer stocks increase OPEX/working capital

- Calibration suppliers: concentrated tech suppliers can exert price pressure

- Market scale 2024: global aftermarket >$100bn

Supply risk: China ~80% rare-earths; cloud 31%/24%/11%

Suppliers hold significant leverage across linac components, rare-earth magnets (China ~80% processing share 2024) and calibrated spares, raising prices and lead times. Dual-sourcing is limited by regulatory requalification and isotope handling (Ir-192 half-life 73.83 days), increasing switching costs and inventory. Cloud/toolkit concentration (AWS ~31%, Azure ~24%, GCP ~11% 2024) and semiconductors add stickiness and cost risk.

| Category | Concentration | 2024 Impact |

|---|---|---|

| Rare-earths | China ~80% | High geopolitical supply risk |

| Cloud | AWS 31%/Azure 24%/GCP 11% | Licensing/switch costs |

| Aftermarket | Fragmented but large | Market >$100bn |

What is included in the product

Combines analysis of competitive rivalry, buyer and supplier power, substitution and entry threats to assess Elekta's strategic position in radiotherapy and oncology equipment markets, highlighting disruptive technologies, pricing pressures, and barriers that shape its profitability and growth prospects.

A clear, one-sheet Porter's Five Forces analysis for Elekta—perfect for quick strategic decisions; customize pressure levels and swap in current data to assess supplier, buyer, rivalry, substitutes, and new entrant threats.

Customers Bargaining Power

Consolidated hospital systems and GPOs

Consolidated IDNs and GPOs, which serve over 90% of US hospitals, push Elekta for aggressive pricing and contract terms, intensifying margin pressure.

Multi-year tenders and blanket agreements create repeated competitive auctions, often driving supplier discounts in the 10–25% range.

Buyers routinely demand bundled service and software concessions, and fleet refresh cycles every 7–10 years create clear switching windows.

Public tenders and reimbursement constraints

National health systems award many radiotherapy contracts via price-centric tenders, where price often counts for 30–70% of scoring; reimbursement caps in 2024 continue to constrain achievable ASPs, depressing device prices by mid-single digits annually in several EU markets. Lengthy budget cycles extend negotiations and favor lowest total cost of ownership, while proven cost-effectiveness (QALY gains, lower retreatment rates) materially influences award decisions.

High switching costs but evaluative power

Installed-base integration with workflows, QA and training creates strong inertia—Elekta’s global installed base exceeds 5,000 systems, driving high switching costs—yet buyers use cross-vendor pilots and head-to-head trials to extract concessions. Contracts now hinge on uptime (industry target ~98–99%), dose-accuracy tolerances (~±2%) and adaptive-RT capabilities (adoption ~10% in 2024), and performance-based clauses appear in over 30% of recent procurements.

Demand for comprehensive solutions

In 2024 customers increasingly demand end-to-end ecosystems covering hardware, treatment planning and oncology IT, using that leverage to seek package discounts and unified SLAs; interoperability with existing systems is frequently a condition of sale, and demonstrated outcomes data plus usability carry high decision weight.

- End-to-end ecosystems drive bundled pricing and SLA demands

- Interoperability often a formal sales requirement

- Outcomes evidence and usability are primary purchase criteria

Aftermarket service leverage

Aftermarket service leverage is central for Elekta because service contracts and upgrades drive recurring revenue and lifetime value, and Elekta's 2024 reports emphasize services as a strategic recurring segment. Buyers use competitive service bids to push down fees, making uptime guarantees (commonly 99% SLAs) and remote diagnostics table stakes. Transparent TCO and predictable lifecycle costs are decisive for renewal and upgrade timing.

- Service-driven recurring revenue: highlighted in Elekta 2024 disclosures

- Competitive bids compress margins, buyers seek 99%+ uptime

- Remote diagnostics standard; TCO transparency influences renewals

IDN/GPO leverage: >90% coverage, 10–25% discounts

Consolidated IDNs/GPOs (covering >90% of US hospitals) and price-focused tenders (price weight 30–70%) give customers strong leverage, pushing discounts often 10–25% and compressing ASPs. Multi-year contracts, bundled service/software demands and 5,000+ installed base create switching windows but high inertia; uptime SLAs (~99%) and adaptive-RT adoption (~10% in 2024) shape negotiations.

| Metric | 2024 value |

|---|---|

| IDN/GPO coverage | >90% US hospitals |

| Typical supplier discounts | 10–25% |

| Price weight in tenders | 30–70% |

| Installed base | >5,000 systems |

| Uptime SLAs | ~99% |

| Adaptive-RT adoption | ~10% |

What You See Is What You Get

Elekta Porter's Five Forces Analysis

This preview shows the exact Elekta Porter’s Five Forces analysis you'll receive after purchase—fully formatted and ready for use. It covers supplier power, buyer power, threat of entrants, threat of substitutes, and competitive rivalry specific to Elekta. No placeholders or samples—instant download upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Elekta faces moderate supplier power, high buyer scrutiny, regulatory-driven barriers to entry, intense rivalry among oncology-tech players, and evolving substitute threats from emerging therapies; this snapshot highlights key pressure points shaping margins and innovation. The full Porter's Five Forces Analysis unpacks force-by-force ratings, data and strategic implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized component suppliers concentration

Linear accelerator tubes, beam-shaping devices, high-precision bearings and rare-earth magnets come from a small set of qualified vendors, giving suppliers clear leverage on price and lead times. Dual-sourcing is constrained by lengthy qualification and regulatory validation, raising switching costs and inventory needs. Major rare-earth magnet capacity is concentrated in China, increasing geopolitical supply risk. Any supplier disruption can postpone Elekta system deliveries and service SLAs.

Radioisotope and dosimetry dependencies

Brachytherapy sources (Ir-192 half-life 73.83 days; Co-60 half-life 5.27 years), dosimeters and QA phantoms depend on tightly regulated isotope and measurement suppliers subject to IAEA and national certification, limiting vendor switching. Certification and handling constraints raise switching costs and make price hikes hard to offset without product redesign. Strategic inventory management and long-term contracts are vital to mitigate supply and cost risk.

Advanced electronics and semiconductor exposure

Elekta relies on high-spec semiconductors, GPUs and FPGAs for control systems and imaging, and cyclical shortages have previously increased lead times and component costs, forcing production delays; substituting parts typically requires engineering changes and regulatory re-approval, making swaps costly and slow. Close supplier collaboration and design-for-availability strategies materially reduce this supplier power and operational risk.

Software stack and cloud infrastructure

Treatment planning, oncology information systems and AI modules rely on third-party toolkits and cloud providers; 2024 market shares concentrate with AWS ~31%, Azure ~24% and GCP ~11%, raising licensing and interoperability switching costs. Security and certifications (ISO 27001, HIPAA, GDPR) increase vendor stickiness; negotiation power improves with Elekta scale but is bounded by compliance-driven dependency.

- Dependency: third-party SDKs, cloud APIs

- Switching cost: licensing + integration

- Stickiness: security/compliance certifications

- Leverage: scale helps but compliance caps bargaining

Service parts and field logistics

- Limited substitutes: strict QA/traceability raises supplier power

- Logistics impact: regional partners determine 24–72h response and costs

- SLAs drive inventory: elevated buffer stocks increase OPEX/working capital

- Calibration suppliers: concentrated tech suppliers can exert price pressure

- Market scale 2024: global aftermarket >$100bn

Supply risk: China ~80% rare-earths; cloud 31%/24%/11%

Suppliers hold significant leverage across linac components, rare-earth magnets (China ~80% processing share 2024) and calibrated spares, raising prices and lead times. Dual-sourcing is limited by regulatory requalification and isotope handling (Ir-192 half-life 73.83 days), increasing switching costs and inventory. Cloud/toolkit concentration (AWS ~31%, Azure ~24%, GCP ~11% 2024) and semiconductors add stickiness and cost risk.

| Category | Concentration | 2024 Impact |

|---|---|---|

| Rare-earths | China ~80% | High geopolitical supply risk |

| Cloud | AWS 31%/Azure 24%/GCP 11% | Licensing/switch costs |

| Aftermarket | Fragmented but large | Market >$100bn |

What is included in the product

Combines analysis of competitive rivalry, buyer and supplier power, substitution and entry threats to assess Elekta's strategic position in radiotherapy and oncology equipment markets, highlighting disruptive technologies, pricing pressures, and barriers that shape its profitability and growth prospects.

A clear, one-sheet Porter's Five Forces analysis for Elekta—perfect for quick strategic decisions; customize pressure levels and swap in current data to assess supplier, buyer, rivalry, substitutes, and new entrant threats.

Customers Bargaining Power

Consolidated hospital systems and GPOs

Consolidated IDNs and GPOs, which serve over 90% of US hospitals, push Elekta for aggressive pricing and contract terms, intensifying margin pressure.

Multi-year tenders and blanket agreements create repeated competitive auctions, often driving supplier discounts in the 10–25% range.

Buyers routinely demand bundled service and software concessions, and fleet refresh cycles every 7–10 years create clear switching windows.

Public tenders and reimbursement constraints

National health systems award many radiotherapy contracts via price-centric tenders, where price often counts for 30–70% of scoring; reimbursement caps in 2024 continue to constrain achievable ASPs, depressing device prices by mid-single digits annually in several EU markets. Lengthy budget cycles extend negotiations and favor lowest total cost of ownership, while proven cost-effectiveness (QALY gains, lower retreatment rates) materially influences award decisions.

High switching costs but evaluative power

Installed-base integration with workflows, QA and training creates strong inertia—Elekta’s global installed base exceeds 5,000 systems, driving high switching costs—yet buyers use cross-vendor pilots and head-to-head trials to extract concessions. Contracts now hinge on uptime (industry target ~98–99%), dose-accuracy tolerances (~±2%) and adaptive-RT capabilities (adoption ~10% in 2024), and performance-based clauses appear in over 30% of recent procurements.

Demand for comprehensive solutions

In 2024 customers increasingly demand end-to-end ecosystems covering hardware, treatment planning and oncology IT, using that leverage to seek package discounts and unified SLAs; interoperability with existing systems is frequently a condition of sale, and demonstrated outcomes data plus usability carry high decision weight.

- End-to-end ecosystems drive bundled pricing and SLA demands

- Interoperability often a formal sales requirement

- Outcomes evidence and usability are primary purchase criteria

Aftermarket service leverage

Aftermarket service leverage is central for Elekta because service contracts and upgrades drive recurring revenue and lifetime value, and Elekta's 2024 reports emphasize services as a strategic recurring segment. Buyers use competitive service bids to push down fees, making uptime guarantees (commonly 99% SLAs) and remote diagnostics table stakes. Transparent TCO and predictable lifecycle costs are decisive for renewal and upgrade timing.

- Service-driven recurring revenue: highlighted in Elekta 2024 disclosures

- Competitive bids compress margins, buyers seek 99%+ uptime

- Remote diagnostics standard; TCO transparency influences renewals

IDN/GPO leverage: >90% coverage, 10–25% discounts

Consolidated IDNs/GPOs (covering >90% of US hospitals) and price-focused tenders (price weight 30–70%) give customers strong leverage, pushing discounts often 10–25% and compressing ASPs. Multi-year contracts, bundled service/software demands and 5,000+ installed base create switching windows but high inertia; uptime SLAs (~99%) and adaptive-RT adoption (~10% in 2024) shape negotiations.

| Metric | 2024 value |

|---|---|

| IDN/GPO coverage | >90% US hospitals |

| Typical supplier discounts | 10–25% |

| Price weight in tenders | 30–70% |

| Installed base | >5,000 systems |

| Uptime SLAs | ~99% |

| Adaptive-RT adoption | ~10% |

What You See Is What You Get

Elekta Porter's Five Forces Analysis

This preview shows the exact Elekta Porter’s Five Forces analysis you'll receive after purchase—fully formatted and ready for use. It covers supplier power, buyer power, threat of entrants, threat of substitutes, and competitive rivalry specific to Elekta. No placeholders or samples—instant download upon payment.