Elektroimportøren Porter's Five Forces Analysis

Don't Miss the Bigger Picture

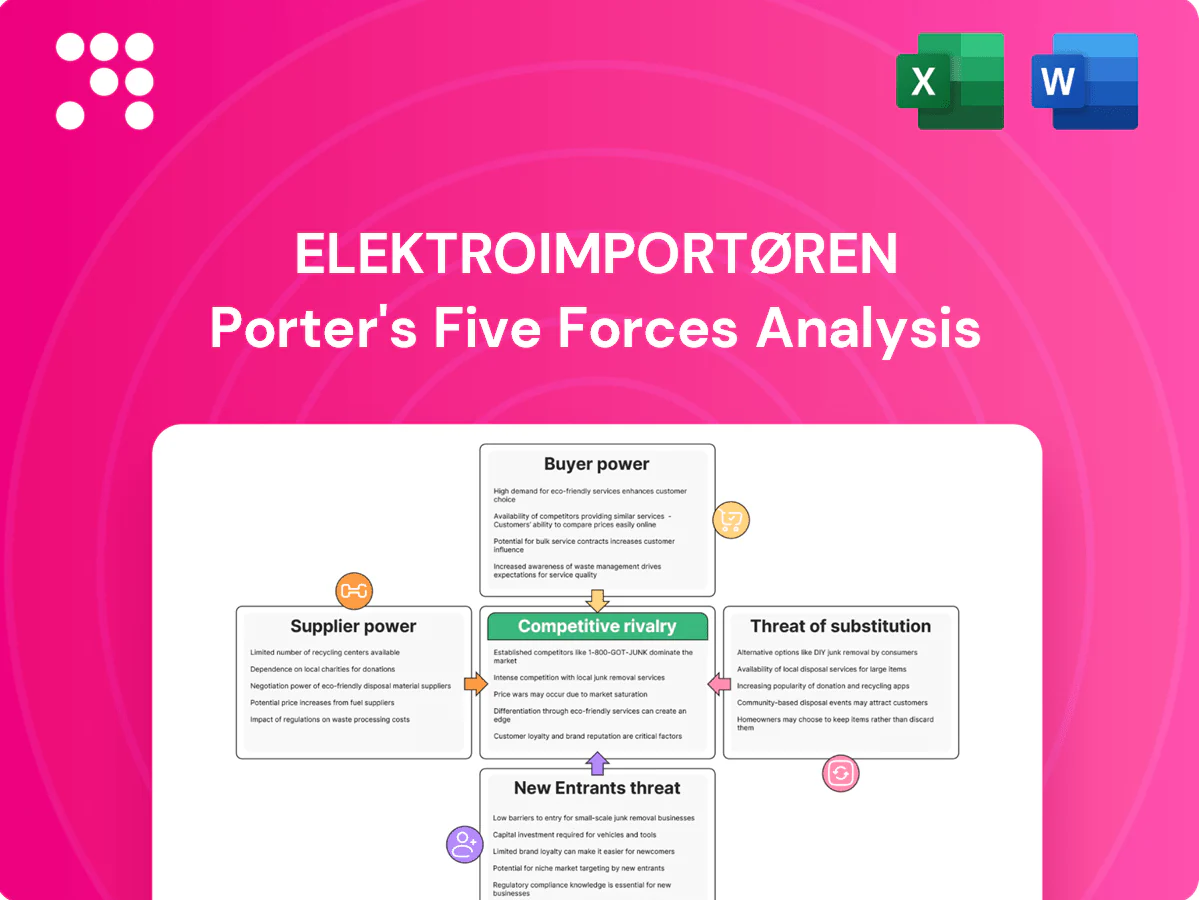

Elektroimportøren faces moderate supplier power, strong buyer expectations, and rising online competition that intensifies rivalry; barriers to entry are mixed and substitutes present targeted threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elektroimportøren’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global brand concentration

Leading manufacturers such as ABB (2024 rev ~29bn USD), Schneider Electric (2024 rev ~40bn EUR), Eaton (2024 rev ~24bn USD), Signify (2024 rev ~7bn EUR) and Nexans (2024 rev ~9.5bn EUR) hold strong brands and compliance pedigrees, limiting interchangeable supply. Their concentration tightens commercial terms and can dictate product availability. Elektroimportøren mitigates risk via multi-sourcing but must stock key brands for pro customers, raising supplier leverage in negotiations and assortment decisions.

Standards and certifications

Norwegian NEK standards and EU/EEA CE marking remain mandatory in 2024 for applicable electrical products, constraining Elektroimportøren’s alternatives to certified suppliers. Compliance narrows acceptable SKUs and raises dependence on approved vendors. Suppliers holding unique certified SKUs thus capture stronger pricing power and margins. Switching to uncertified or lesser-known suppliers risks regulatory liability and reputational harm under Norwegian product liability rules.

Logistics and FX exposure

Imports expose Elektroimportøren to EUR/NOK swings (2024 range roughly 11.0–12.4, ≈13% move) and volatile freight; tight markets in 2024 saw spot ocean freight spikes up to ~30% vs prior averages, allowing suppliers to pass costs through. Norway’s terrain and winter logistics can add delivery cost uplifts around 10–15% during disruptions, increasing supplier leverage. Long-term contracts and FX/freight hedges only partially mitigate these pressures.

Private label counterweight

Elektroimportøren can expand private labels to cut reliance on branded suppliers and boost margins; by 2024 Nordic private‑label penetration in DIY/electrical niches reached about 15%, validating scale economies in cables, fixtures and accessories. Private labels create credible low‑cost alternatives for commodity SKUs, trimming supplier leverage. For mission‑critical components pros still prefer OEM brands, so supplier power is tempered but not eliminated.

- 2024: ~15% Nordic private‑label penetration; private labels reduce commodity supplier power but OEMs retain sway on mission‑critical SKUs

Digital data dependency

Product data, spec sheets and integrations (EDI, PIM) commonly flow from suppliers, and vendors that supply high-quality, timely feeds drive shelf priority and better online conversion—studies in retail digital commerce show enriched content can lift conversion by 10–30% and reduce returns by up to 25% (industry reports 2023–24).

Control over exclusive or higher-quality feeds gives suppliers promotional leverage and can dictate placement in Elektroimportøren’s digital catalog, raising effective switching costs for the retailer.

- data_origin: supplier-driven

- conversion_uplift: 10–30%

- returns_reduction: up to 25%

- switching_costs: increased via integrations

OEM dominance, NEK/CE compliance and EUR/NOK volatility boost supplier leverage

Strong OEMs (ABB ~29bn USD, Schneider ~40bn EUR, Eaton ~24bn USD, Signify ~7bn EUR, Nexans ~9.5bn EUR in 2024) limit interchangeability; compliance (NEK/CE) and EUR/NOK 2024 ~11.0–12.4 FX range raise supplier leverage. Private‑label penetration ~15% reduces power on commodities, but mission‑critical SKUs keep OEM sway. Data/EDI control boosts supplier promotional leverage and switching costs.

| Metric | 2024 |

|---|---|

| Key OEM revs | ABB 29bn USD; Schneider 40bn EUR; Eaton 24bn USD |

| EUR/NOK | 11.0–12.4 |

| Private‑label | ~15% |

What is included in the product

Tailored exclusively for Elektroimportøren, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, and market entry risks specific to its retail and wholesale channels. It identifies disruptive substitutes, emergent threats, and protective dynamics that shape pricing power and profitability.

Clear, one-sheet Porter’s Five Forces for Elektroimportøren—instantly highlights supplier, buyer, substitute, entrant and rivalry pressures so teams can prioritize fixes; customizable scores and radar chart make scenario testing (regulation, new entrants) fast and boardroom-ready.

Customers Bargaining Power

Pro electrician leverage

Professional installers buy in volume, compare net prices and negotiate rebates, giving them strong leverage over Elektroimportøren by prioritizing availability, credit terms and job-site delivery.

Multi-sourcing across wholesalers keeps pricing pressure high as installers shift orders to better terms or faster delivery, while the loss of a few large installer accounts can materially reduce wholesale volumes and margin stability.

DIY price transparency

DIY price transparency means shoppers compare prices across platforms and big-box retailers instantly—70% of consumers used online price comparison tools in 2024, pushing Elektroimportøren to match market rates. Low switching costs drive intense promo sensitivity, with studies showing over 60% willing to switch for modest discounts. Reviews and ratings now steer demand toward top-value SKUs, forcing tighter pricing and clearer value communication.

Specification-driven demand

Pros specifying brands/components for compliance and warranty reduces per-project switching but lets buyers shop identical specs across vendors; project tenders in 2024 typically produced competitive quotes that compressed supplier margins by roughly 5–12%, amplifying buyer power. Service elements—fast delivery, installation support, extended warranties—often offset pure price pressure and preserve premium pricing.

Omnichannel expectations

Customers now expect click-and-collect, fast delivery and real-time stock visibility; 2024 industry tracking shows omnichannel service is a primary purchase driver for electronics retailers. Failure to meet SLAs prompts immediate switching, elevating buyer leverage. Strong omnichannel execution reduces perceived risk and price sensitivity, while weak execution amplifies bargaining for discounts and concessions.

- omnichannel: 2024 demand spike

- SLA breaches → immediate churn

- good execution → lower price elasticity

- weakness → higher buyer concessions

Loyalty and credit programs

Structured rebates, loyalty points and trade credit lock in repeat business and lower effective switching among Elektroimportørens B2B customers; they blunt price demands by turning discounts into earned benefits. By 2024 these programs are table stakes in Norway’s wholesale market, and buyers routinely leverage them to extract added value beyond sticker price, with trade credit commonly offered on net 30–60 day terms.

- Rebates: encourage volume repeat purchases

- Loyalty points: reduce perceived switching

- Trade credit (net 30–60): improves buyer cash flow

Trade credit, DIY price transparency and multi-sourcing squeeze margins 5-12% and drive churn

Professional installers leverage volume, rebates and net 30–60 credit to demand availability and delivery; multi-sourcing keeps pricing pressure high and can cut wholesale volumes if key accounts shift. DIY price transparency (70% used comparison tools in 2024) and >60% willing to switch compress margins 5–12% in tenders; omnichannel SLAs drive churn.

| Metric | 2024 | Impact |

|---|---|---|

| Price comparison | 70% | higher price sensitivity |

| Switch willingness | >60% | promo-driven churn |

| Tender margin hit | 5–12% | compresses margins |

| Trade credit | net 30–60 | locks volumes |

Preview Before You Purchase

Elektroimportøren Porter's Five Forces Analysis

This preview shows the exact Elektroimportøren Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download once you complete your purchase. You’re viewing the final file and will get instant access to this same deliverable after payment.

Don't Miss the Bigger Picture

Elektroimportøren faces moderate supplier power, strong buyer expectations, and rising online competition that intensifies rivalry; barriers to entry are mixed and substitutes present targeted threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elektroimportøren’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global brand concentration

Leading manufacturers such as ABB (2024 rev ~29bn USD), Schneider Electric (2024 rev ~40bn EUR), Eaton (2024 rev ~24bn USD), Signify (2024 rev ~7bn EUR) and Nexans (2024 rev ~9.5bn EUR) hold strong brands and compliance pedigrees, limiting interchangeable supply. Their concentration tightens commercial terms and can dictate product availability. Elektroimportøren mitigates risk via multi-sourcing but must stock key brands for pro customers, raising supplier leverage in negotiations and assortment decisions.

Standards and certifications

Norwegian NEK standards and EU/EEA CE marking remain mandatory in 2024 for applicable electrical products, constraining Elektroimportøren’s alternatives to certified suppliers. Compliance narrows acceptable SKUs and raises dependence on approved vendors. Suppliers holding unique certified SKUs thus capture stronger pricing power and margins. Switching to uncertified or lesser-known suppliers risks regulatory liability and reputational harm under Norwegian product liability rules.

Logistics and FX exposure

Imports expose Elektroimportøren to EUR/NOK swings (2024 range roughly 11.0–12.4, ≈13% move) and volatile freight; tight markets in 2024 saw spot ocean freight spikes up to ~30% vs prior averages, allowing suppliers to pass costs through. Norway’s terrain and winter logistics can add delivery cost uplifts around 10–15% during disruptions, increasing supplier leverage. Long-term contracts and FX/freight hedges only partially mitigate these pressures.

Private label counterweight

Elektroimportøren can expand private labels to cut reliance on branded suppliers and boost margins; by 2024 Nordic private‑label penetration in DIY/electrical niches reached about 15%, validating scale economies in cables, fixtures and accessories. Private labels create credible low‑cost alternatives for commodity SKUs, trimming supplier leverage. For mission‑critical components pros still prefer OEM brands, so supplier power is tempered but not eliminated.

- 2024: ~15% Nordic private‑label penetration; private labels reduce commodity supplier power but OEMs retain sway on mission‑critical SKUs

Digital data dependency

Product data, spec sheets and integrations (EDI, PIM) commonly flow from suppliers, and vendors that supply high-quality, timely feeds drive shelf priority and better online conversion—studies in retail digital commerce show enriched content can lift conversion by 10–30% and reduce returns by up to 25% (industry reports 2023–24).

Control over exclusive or higher-quality feeds gives suppliers promotional leverage and can dictate placement in Elektroimportøren’s digital catalog, raising effective switching costs for the retailer.

- data_origin: supplier-driven

- conversion_uplift: 10–30%

- returns_reduction: up to 25%

- switching_costs: increased via integrations

OEM dominance, NEK/CE compliance and EUR/NOK volatility boost supplier leverage

Strong OEMs (ABB ~29bn USD, Schneider ~40bn EUR, Eaton ~24bn USD, Signify ~7bn EUR, Nexans ~9.5bn EUR in 2024) limit interchangeability; compliance (NEK/CE) and EUR/NOK 2024 ~11.0–12.4 FX range raise supplier leverage. Private‑label penetration ~15% reduces power on commodities, but mission‑critical SKUs keep OEM sway. Data/EDI control boosts supplier promotional leverage and switching costs.

| Metric | 2024 |

|---|---|

| Key OEM revs | ABB 29bn USD; Schneider 40bn EUR; Eaton 24bn USD |

| EUR/NOK | 11.0–12.4 |

| Private‑label | ~15% |

What is included in the product

Tailored exclusively for Elektroimportøren, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, and market entry risks specific to its retail and wholesale channels. It identifies disruptive substitutes, emergent threats, and protective dynamics that shape pricing power and profitability.

Clear, one-sheet Porter’s Five Forces for Elektroimportøren—instantly highlights supplier, buyer, substitute, entrant and rivalry pressures so teams can prioritize fixes; customizable scores and radar chart make scenario testing (regulation, new entrants) fast and boardroom-ready.

Customers Bargaining Power

Pro electrician leverage

Professional installers buy in volume, compare net prices and negotiate rebates, giving them strong leverage over Elektroimportøren by prioritizing availability, credit terms and job-site delivery.

Multi-sourcing across wholesalers keeps pricing pressure high as installers shift orders to better terms or faster delivery, while the loss of a few large installer accounts can materially reduce wholesale volumes and margin stability.

DIY price transparency

DIY price transparency means shoppers compare prices across platforms and big-box retailers instantly—70% of consumers used online price comparison tools in 2024, pushing Elektroimportøren to match market rates. Low switching costs drive intense promo sensitivity, with studies showing over 60% willing to switch for modest discounts. Reviews and ratings now steer demand toward top-value SKUs, forcing tighter pricing and clearer value communication.

Specification-driven demand

Pros specifying brands/components for compliance and warranty reduces per-project switching but lets buyers shop identical specs across vendors; project tenders in 2024 typically produced competitive quotes that compressed supplier margins by roughly 5–12%, amplifying buyer power. Service elements—fast delivery, installation support, extended warranties—often offset pure price pressure and preserve premium pricing.

Omnichannel expectations

Customers now expect click-and-collect, fast delivery and real-time stock visibility; 2024 industry tracking shows omnichannel service is a primary purchase driver for electronics retailers. Failure to meet SLAs prompts immediate switching, elevating buyer leverage. Strong omnichannel execution reduces perceived risk and price sensitivity, while weak execution amplifies bargaining for discounts and concessions.

- omnichannel: 2024 demand spike

- SLA breaches → immediate churn

- good execution → lower price elasticity

- weakness → higher buyer concessions

Loyalty and credit programs

Structured rebates, loyalty points and trade credit lock in repeat business and lower effective switching among Elektroimportørens B2B customers; they blunt price demands by turning discounts into earned benefits. By 2024 these programs are table stakes in Norway’s wholesale market, and buyers routinely leverage them to extract added value beyond sticker price, with trade credit commonly offered on net 30–60 day terms.

- Rebates: encourage volume repeat purchases

- Loyalty points: reduce perceived switching

- Trade credit (net 30–60): improves buyer cash flow

Trade credit, DIY price transparency and multi-sourcing squeeze margins 5-12% and drive churn

Professional installers leverage volume, rebates and net 30–60 credit to demand availability and delivery; multi-sourcing keeps pricing pressure high and can cut wholesale volumes if key accounts shift. DIY price transparency (70% used comparison tools in 2024) and >60% willing to switch compress margins 5–12% in tenders; omnichannel SLAs drive churn.

| Metric | 2024 | Impact |

|---|---|---|

| Price comparison | 70% | higher price sensitivity |

| Switch willingness | >60% | promo-driven churn |

| Tender margin hit | 5–12% | compresses margins |

| Trade credit | net 30–60 | locks volumes |

Preview Before You Purchase

Elektroimportøren Porter's Five Forces Analysis

This preview shows the exact Elektroimportøren Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download once you complete your purchase. You’re viewing the final file and will get instant access to this same deliverable after payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Elektroimportøren faces moderate supplier power, strong buyer expectations, and rising online competition that intensifies rivalry; barriers to entry are mixed and substitutes present targeted threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elektroimportøren’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global brand concentration

Leading manufacturers such as ABB (2024 rev ~29bn USD), Schneider Electric (2024 rev ~40bn EUR), Eaton (2024 rev ~24bn USD), Signify (2024 rev ~7bn EUR) and Nexans (2024 rev ~9.5bn EUR) hold strong brands and compliance pedigrees, limiting interchangeable supply. Their concentration tightens commercial terms and can dictate product availability. Elektroimportøren mitigates risk via multi-sourcing but must stock key brands for pro customers, raising supplier leverage in negotiations and assortment decisions.

Standards and certifications

Norwegian NEK standards and EU/EEA CE marking remain mandatory in 2024 for applicable electrical products, constraining Elektroimportøren’s alternatives to certified suppliers. Compliance narrows acceptable SKUs and raises dependence on approved vendors. Suppliers holding unique certified SKUs thus capture stronger pricing power and margins. Switching to uncertified or lesser-known suppliers risks regulatory liability and reputational harm under Norwegian product liability rules.

Logistics and FX exposure

Imports expose Elektroimportøren to EUR/NOK swings (2024 range roughly 11.0–12.4, ≈13% move) and volatile freight; tight markets in 2024 saw spot ocean freight spikes up to ~30% vs prior averages, allowing suppliers to pass costs through. Norway’s terrain and winter logistics can add delivery cost uplifts around 10–15% during disruptions, increasing supplier leverage. Long-term contracts and FX/freight hedges only partially mitigate these pressures.

Private label counterweight

Elektroimportøren can expand private labels to cut reliance on branded suppliers and boost margins; by 2024 Nordic private‑label penetration in DIY/electrical niches reached about 15%, validating scale economies in cables, fixtures and accessories. Private labels create credible low‑cost alternatives for commodity SKUs, trimming supplier leverage. For mission‑critical components pros still prefer OEM brands, so supplier power is tempered but not eliminated.

- 2024: ~15% Nordic private‑label penetration; private labels reduce commodity supplier power but OEMs retain sway on mission‑critical SKUs

Digital data dependency

Product data, spec sheets and integrations (EDI, PIM) commonly flow from suppliers, and vendors that supply high-quality, timely feeds drive shelf priority and better online conversion—studies in retail digital commerce show enriched content can lift conversion by 10–30% and reduce returns by up to 25% (industry reports 2023–24).

Control over exclusive or higher-quality feeds gives suppliers promotional leverage and can dictate placement in Elektroimportøren’s digital catalog, raising effective switching costs for the retailer.

- data_origin: supplier-driven

- conversion_uplift: 10–30%

- returns_reduction: up to 25%

- switching_costs: increased via integrations

OEM dominance, NEK/CE compliance and EUR/NOK volatility boost supplier leverage

Strong OEMs (ABB ~29bn USD, Schneider ~40bn EUR, Eaton ~24bn USD, Signify ~7bn EUR, Nexans ~9.5bn EUR in 2024) limit interchangeability; compliance (NEK/CE) and EUR/NOK 2024 ~11.0–12.4 FX range raise supplier leverage. Private‑label penetration ~15% reduces power on commodities, but mission‑critical SKUs keep OEM sway. Data/EDI control boosts supplier promotional leverage and switching costs.

| Metric | 2024 |

|---|---|

| Key OEM revs | ABB 29bn USD; Schneider 40bn EUR; Eaton 24bn USD |

| EUR/NOK | 11.0–12.4 |

| Private‑label | ~15% |

What is included in the product

Tailored exclusively for Elektroimportøren, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, and market entry risks specific to its retail and wholesale channels. It identifies disruptive substitutes, emergent threats, and protective dynamics that shape pricing power and profitability.

Clear, one-sheet Porter’s Five Forces for Elektroimportøren—instantly highlights supplier, buyer, substitute, entrant and rivalry pressures so teams can prioritize fixes; customizable scores and radar chart make scenario testing (regulation, new entrants) fast and boardroom-ready.

Customers Bargaining Power

Pro electrician leverage

Professional installers buy in volume, compare net prices and negotiate rebates, giving them strong leverage over Elektroimportøren by prioritizing availability, credit terms and job-site delivery.

Multi-sourcing across wholesalers keeps pricing pressure high as installers shift orders to better terms or faster delivery, while the loss of a few large installer accounts can materially reduce wholesale volumes and margin stability.

DIY price transparency

DIY price transparency means shoppers compare prices across platforms and big-box retailers instantly—70% of consumers used online price comparison tools in 2024, pushing Elektroimportøren to match market rates. Low switching costs drive intense promo sensitivity, with studies showing over 60% willing to switch for modest discounts. Reviews and ratings now steer demand toward top-value SKUs, forcing tighter pricing and clearer value communication.

Specification-driven demand

Pros specifying brands/components for compliance and warranty reduces per-project switching but lets buyers shop identical specs across vendors; project tenders in 2024 typically produced competitive quotes that compressed supplier margins by roughly 5–12%, amplifying buyer power. Service elements—fast delivery, installation support, extended warranties—often offset pure price pressure and preserve premium pricing.

Omnichannel expectations

Customers now expect click-and-collect, fast delivery and real-time stock visibility; 2024 industry tracking shows omnichannel service is a primary purchase driver for electronics retailers. Failure to meet SLAs prompts immediate switching, elevating buyer leverage. Strong omnichannel execution reduces perceived risk and price sensitivity, while weak execution amplifies bargaining for discounts and concessions.

- omnichannel: 2024 demand spike

- SLA breaches → immediate churn

- good execution → lower price elasticity

- weakness → higher buyer concessions

Loyalty and credit programs

Structured rebates, loyalty points and trade credit lock in repeat business and lower effective switching among Elektroimportørens B2B customers; they blunt price demands by turning discounts into earned benefits. By 2024 these programs are table stakes in Norway’s wholesale market, and buyers routinely leverage them to extract added value beyond sticker price, with trade credit commonly offered on net 30–60 day terms.

- Rebates: encourage volume repeat purchases

- Loyalty points: reduce perceived switching

- Trade credit (net 30–60): improves buyer cash flow

Trade credit, DIY price transparency and multi-sourcing squeeze margins 5-12% and drive churn

Professional installers leverage volume, rebates and net 30–60 credit to demand availability and delivery; multi-sourcing keeps pricing pressure high and can cut wholesale volumes if key accounts shift. DIY price transparency (70% used comparison tools in 2024) and >60% willing to switch compress margins 5–12% in tenders; omnichannel SLAs drive churn.

| Metric | 2024 | Impact |

|---|---|---|

| Price comparison | 70% | higher price sensitivity |

| Switch willingness | >60% | promo-driven churn |

| Tender margin hit | 5–12% | compresses margins |

| Trade credit | net 30–60 | locks volumes |

Preview Before You Purchase

Elektroimportøren Porter's Five Forces Analysis

This preview shows the exact Elektroimportøren Porter’s Five Forces analysis you’ll receive—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download once you complete your purchase. You’re viewing the final file and will get instant access to this same deliverable after payment.