Elemaster SpA Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

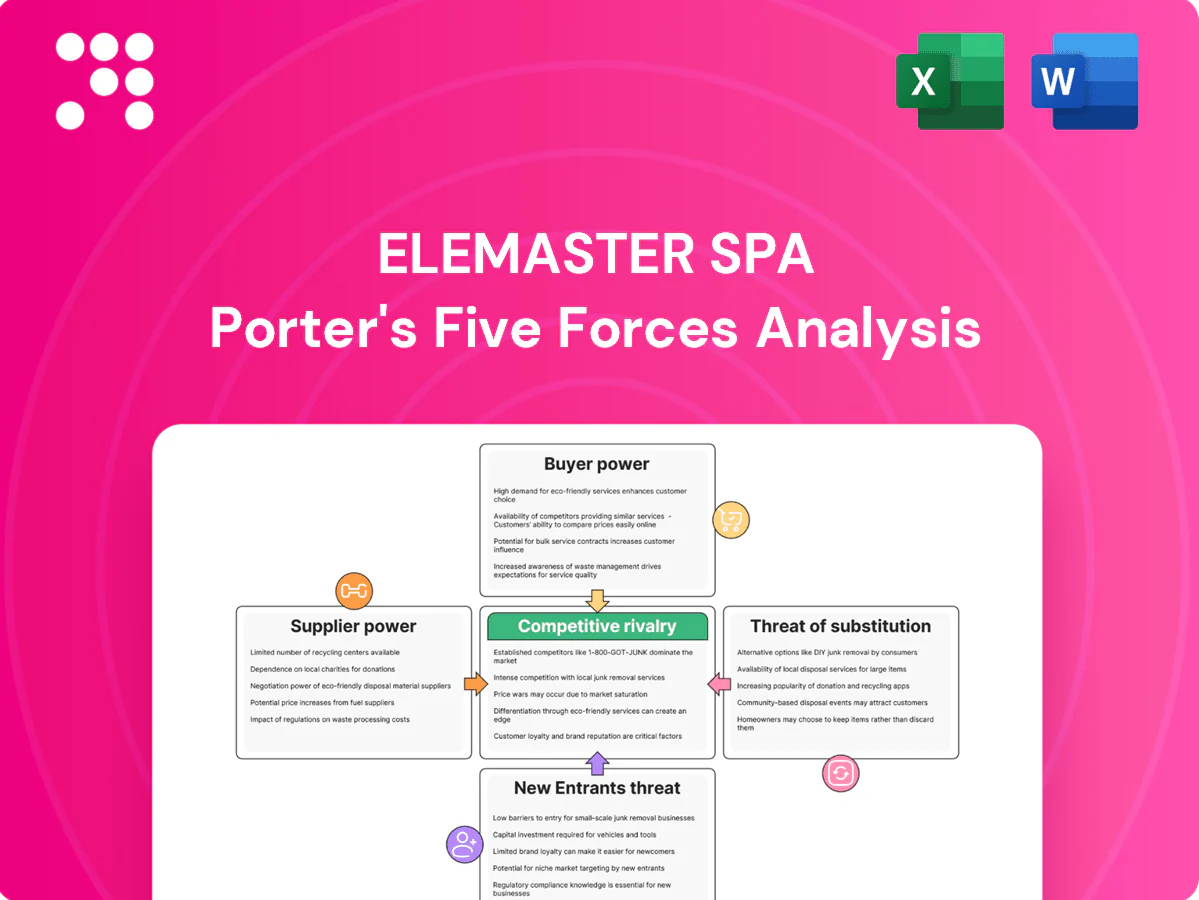

Elemaster SpA faces moderate supplier leverage, rising buyer expectations, and pressure from agile contract manufacturers, while differentiation and scale buffer competitive rivalry; emerging technologies and new entrants pose watchable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elemaster SpA’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Specialized component dependence

Elemaster depends on semiconductors, PCBs, connectors and test gear from niche suppliers with long lead times, often 12–24 weeks, concentrating supply and raising switching costs that give suppliers pricing and allocation leverage. Dual-sourcing and design-for-availability reduce but do not eliminate this exposure. Strategic supplier agreements and buffer inventories remain key to dampen 2024 volatility.

Supply chain cyclicality

Component cycles and capacity constraints shift leverage to suppliers during shortages; following 2020–22 disruptions chip lead times peaked over 20 weeks and in 2024 commonly exceeded 12 weeks, allowing OEMs priority allocation and squeezing EMS gross margins by several hundred basis points in boom phases. Elemaster’s diversified end-markets smooth demand volatility but cannot offset systemic tightness; long-term forecasts and vendor-managed inventory mitigate risk.

Regulated, high-reliability inputs

Regulated, high-reliability inputs for aerospace, defense, rail and medical require certifications such as AS9100/EN 9100, EN 15085 and ISO 13485, which constrain approved vendor lists and shrink the supplier pool. Fewer compliant suppliers increase vendor bargaining power, raising prices and leverage on lead times. Any supplier requalification triggers extended timelines and added costs. Early supplier involvement and multi-approved BOMs reduce dependence and procurement risk.

Geopolitical and trade exposure

Tariffs, export controls and regionalization have tightened component availability and pricing; US CHIPS Act funding of 52.7 billion USD and concentration in foundries (TSMC ~53% share) increase supplier leverage in advanced nodes. Suppliers in sensitive nodes can enforce compliance-led restrictions, forcing Elemaster to engineer around restricted parts or redesign products. Localizing supply lowers geopolitical risk but typically raises procurement and manufacturing costs.

- Tariffs impact cost pass-through

- Export controls enable supplier leverage

- Redesign or second-sourcing required

- Localization reduces risk, increases unit cost

Equipment and test platform lock-in

Equipment vendors for SMT, AOI and ICT enforce lock-in via proprietary software, fixtures and spare parts, with service and consumable contracts often representing 8–12% of original equipment cost annually in 2024, entrenching supplier leverage over lifecycle terms.

- Vendor lock-in: proprietary SW/fixtures

- Opex impact: service/consumables ~8–12% p.a. (2024)

- Lifecycle leverage: limited bargaining on upgrades

- Mitigation: standardize platforms, negotiate bundled SLAs

12–24 week lead times and supplier concentration squeeze EMS margins

Elemaster relies on niche semiconductor, PCB and test suppliers with typical lead times 12–24 weeks, giving suppliers allocation and pricing leverage. Shortages have squeezed EMS gross margins ~200–400 bps in tight cycles; certified aerospace/medical vendors are few, raising switching costs. Equipment service/consumables run ~8–12% of OEM cost (2024), so long-term contracts and dual-sourcing remain key.

| Metric | 2024 value |

|---|---|

| Avg lead time | 12–24 weeks |

| EMS margin hit (shortage) | 200–400 bps |

| Equipment opex | 8–12% p.a. |

| TSMC market share | ~53% |

| US CHIPS funding | 52.7 billion USD |

What is included in the product

Tailored Porter's Five Forces analysis for Elemaster SpA uncovering key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position.

A concise one-sheet Porter's Five Forces for Elemaster SpA—instantly clarifies supplier, buyer, entrant and substitute pressures to streamline strategic choices and reduce research time.

Customers Bargaining Power

Large, sophisticated OEMs

Customers in aerospace, defense, medical and rail are few but highly technical, with procurement and design cycles typically spanning 3–7 years in 2024, giving OEMs strong negotiating leverage. They demand price transparency, strict SLAs and single-digit to low-double-digit penalty clauses. Large OEM orders drive volume, so trusted partnerships often trade margin for multi-year contracts and stable backlog.

Qualification lock-ins

Once a product is qualified, switching EMS providers is costly and slow, which tempers buyer power mid-program and preserves incumbent margins. At rebid or redesign—typically every 3–5 years—buyers regain leverage to benchmark suppliers globally and can reduce TCO by roughly 10–20% using aggressive sourcing. Elemaster must defend win-rates with granular performance KPIs, real-time quality data and rigorous TCO analytics to retain programs.

Demand volatility and forecast risk

Project-based, lumpy pull-ins shift inventory risk onto Elemaster as customers push volatility — industry EMS demand swings rose ~±18% in 2024, stressing cash and working capital. Buyers increasingly request consignment and flexible payment terms, pressuring margins; strong S&OP and NCNR clauses help rebalance risk and reduced inventory write-offs. Offering value-added planning services allows Elemaster to justify premium pricing and stabilize throughput.

Design ownership and IP

When customers retain design ownership, Elemaster’s differentiation shifts to cost, quality and delivery, enabling buyers to dual-source and exert pricing pressure. Providing co-design and test development embeds Elemaster deeper into product workflows, reducing pure price competition. Lifecycle engineering and aftersales services increase switching costs and customer stickiness.

- Design ownership narrows EMS differentiation

- Dual-sourcing increases pricing pressure

- Co-design/test development embeds supplier

- Lifecycle engineering raises switching costs

Compliance and penalty regimes

Regulated customers impose strict quality, traceability and on-time delivery penalties, and commonly leverage these clauses to demand credits or remediation; Elemaster’s ISO and sector-specific certifications plus zero-defect manufacturing and SPC lines are key defenses. Proactive publication of quality KPIs and on-time rates reduces dispute frequency and strengthens bargaining power.

- Certifications: core defense

- Zero-defect processes: penalty mitigation

- Quality KPIs: preempt penalties

OEM cycles, rebids shave TCO; EMS ±18% demand swings raise inventory risk

Customers in aerospace, defense, medical and rail are few, highly technical and give OEMs strong leverage with 3–7 year procurement cycles in 2024. Rebid cycles (3–5 years) let buyers cut TCO ~10–20%; incumbent switching costs and certifications limit mid-program pressure. 2024 EMS demand volatility ±18% shifts inventory risk and fuels consignment/payment requests.

| Metric | 2024 Value |

|---|---|

| Procurement cycle | 3–7 years |

| Rebid interval | 3–5 years |

| TCO reduction on rebid | 10–20% |

| EMS demand volatility | ±18% |

Preview Before You Purchase

Elemaster SpA Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Elemaster SpA you'll receive after purchase—no surprises, fully formatted and ready to use. The report assesses industry rivalry, bargaining power of suppliers and customers, threats of new entrants and substitutes, and strategic implications for Elemaster's competitive positioning. Instant access to this identical document follows your purchase.

Go Beyond the Preview—Access the Full Strategic Report

Elemaster SpA faces moderate supplier leverage, rising buyer expectations, and pressure from agile contract manufacturers, while differentiation and scale buffer competitive rivalry; emerging technologies and new entrants pose watchable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elemaster SpA’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Specialized component dependence

Elemaster depends on semiconductors, PCBs, connectors and test gear from niche suppliers with long lead times, often 12–24 weeks, concentrating supply and raising switching costs that give suppliers pricing and allocation leverage. Dual-sourcing and design-for-availability reduce but do not eliminate this exposure. Strategic supplier agreements and buffer inventories remain key to dampen 2024 volatility.

Supply chain cyclicality

Component cycles and capacity constraints shift leverage to suppliers during shortages; following 2020–22 disruptions chip lead times peaked over 20 weeks and in 2024 commonly exceeded 12 weeks, allowing OEMs priority allocation and squeezing EMS gross margins by several hundred basis points in boom phases. Elemaster’s diversified end-markets smooth demand volatility but cannot offset systemic tightness; long-term forecasts and vendor-managed inventory mitigate risk.

Regulated, high-reliability inputs

Regulated, high-reliability inputs for aerospace, defense, rail and medical require certifications such as AS9100/EN 9100, EN 15085 and ISO 13485, which constrain approved vendor lists and shrink the supplier pool. Fewer compliant suppliers increase vendor bargaining power, raising prices and leverage on lead times. Any supplier requalification triggers extended timelines and added costs. Early supplier involvement and multi-approved BOMs reduce dependence and procurement risk.

Geopolitical and trade exposure

Tariffs, export controls and regionalization have tightened component availability and pricing; US CHIPS Act funding of 52.7 billion USD and concentration in foundries (TSMC ~53% share) increase supplier leverage in advanced nodes. Suppliers in sensitive nodes can enforce compliance-led restrictions, forcing Elemaster to engineer around restricted parts or redesign products. Localizing supply lowers geopolitical risk but typically raises procurement and manufacturing costs.

- Tariffs impact cost pass-through

- Export controls enable supplier leverage

- Redesign or second-sourcing required

- Localization reduces risk, increases unit cost

Equipment and test platform lock-in

Equipment vendors for SMT, AOI and ICT enforce lock-in via proprietary software, fixtures and spare parts, with service and consumable contracts often representing 8–12% of original equipment cost annually in 2024, entrenching supplier leverage over lifecycle terms.

- Vendor lock-in: proprietary SW/fixtures

- Opex impact: service/consumables ~8–12% p.a. (2024)

- Lifecycle leverage: limited bargaining on upgrades

- Mitigation: standardize platforms, negotiate bundled SLAs

12–24 week lead times and supplier concentration squeeze EMS margins

Elemaster relies on niche semiconductor, PCB and test suppliers with typical lead times 12–24 weeks, giving suppliers allocation and pricing leverage. Shortages have squeezed EMS gross margins ~200–400 bps in tight cycles; certified aerospace/medical vendors are few, raising switching costs. Equipment service/consumables run ~8–12% of OEM cost (2024), so long-term contracts and dual-sourcing remain key.

| Metric | 2024 value |

|---|---|

| Avg lead time | 12–24 weeks |

| EMS margin hit (shortage) | 200–400 bps |

| Equipment opex | 8–12% p.a. |

| TSMC market share | ~53% |

| US CHIPS funding | 52.7 billion USD |

What is included in the product

Tailored Porter's Five Forces analysis for Elemaster SpA uncovering key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position.

A concise one-sheet Porter's Five Forces for Elemaster SpA—instantly clarifies supplier, buyer, entrant and substitute pressures to streamline strategic choices and reduce research time.

Customers Bargaining Power

Large, sophisticated OEMs

Customers in aerospace, defense, medical and rail are few but highly technical, with procurement and design cycles typically spanning 3–7 years in 2024, giving OEMs strong negotiating leverage. They demand price transparency, strict SLAs and single-digit to low-double-digit penalty clauses. Large OEM orders drive volume, so trusted partnerships often trade margin for multi-year contracts and stable backlog.

Qualification lock-ins

Once a product is qualified, switching EMS providers is costly and slow, which tempers buyer power mid-program and preserves incumbent margins. At rebid or redesign—typically every 3–5 years—buyers regain leverage to benchmark suppliers globally and can reduce TCO by roughly 10–20% using aggressive sourcing. Elemaster must defend win-rates with granular performance KPIs, real-time quality data and rigorous TCO analytics to retain programs.

Demand volatility and forecast risk

Project-based, lumpy pull-ins shift inventory risk onto Elemaster as customers push volatility — industry EMS demand swings rose ~±18% in 2024, stressing cash and working capital. Buyers increasingly request consignment and flexible payment terms, pressuring margins; strong S&OP and NCNR clauses help rebalance risk and reduced inventory write-offs. Offering value-added planning services allows Elemaster to justify premium pricing and stabilize throughput.

Design ownership and IP

When customers retain design ownership, Elemaster’s differentiation shifts to cost, quality and delivery, enabling buyers to dual-source and exert pricing pressure. Providing co-design and test development embeds Elemaster deeper into product workflows, reducing pure price competition. Lifecycle engineering and aftersales services increase switching costs and customer stickiness.

- Design ownership narrows EMS differentiation

- Dual-sourcing increases pricing pressure

- Co-design/test development embeds supplier

- Lifecycle engineering raises switching costs

Compliance and penalty regimes

Regulated customers impose strict quality, traceability and on-time delivery penalties, and commonly leverage these clauses to demand credits or remediation; Elemaster’s ISO and sector-specific certifications plus zero-defect manufacturing and SPC lines are key defenses. Proactive publication of quality KPIs and on-time rates reduces dispute frequency and strengthens bargaining power.

- Certifications: core defense

- Zero-defect processes: penalty mitigation

- Quality KPIs: preempt penalties

OEM cycles, rebids shave TCO; EMS ±18% demand swings raise inventory risk

Customers in aerospace, defense, medical and rail are few, highly technical and give OEMs strong leverage with 3–7 year procurement cycles in 2024. Rebid cycles (3–5 years) let buyers cut TCO ~10–20%; incumbent switching costs and certifications limit mid-program pressure. 2024 EMS demand volatility ±18% shifts inventory risk and fuels consignment/payment requests.

| Metric | 2024 Value |

|---|---|

| Procurement cycle | 3–7 years |

| Rebid interval | 3–5 years |

| TCO reduction on rebid | 10–20% |

| EMS demand volatility | ±18% |

Preview Before You Purchase

Elemaster SpA Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Elemaster SpA you'll receive after purchase—no surprises, fully formatted and ready to use. The report assesses industry rivalry, bargaining power of suppliers and customers, threats of new entrants and substitutes, and strategic implications for Elemaster's competitive positioning. Instant access to this identical document follows your purchase.

Description

Go Beyond the Preview—Access the Full Strategic Report

Elemaster SpA faces moderate supplier leverage, rising buyer expectations, and pressure from agile contract manufacturers, while differentiation and scale buffer competitive rivalry; emerging technologies and new entrants pose watchable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elemaster SpA’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Specialized component dependence

Elemaster depends on semiconductors, PCBs, connectors and test gear from niche suppliers with long lead times, often 12–24 weeks, concentrating supply and raising switching costs that give suppliers pricing and allocation leverage. Dual-sourcing and design-for-availability reduce but do not eliminate this exposure. Strategic supplier agreements and buffer inventories remain key to dampen 2024 volatility.

Supply chain cyclicality

Component cycles and capacity constraints shift leverage to suppliers during shortages; following 2020–22 disruptions chip lead times peaked over 20 weeks and in 2024 commonly exceeded 12 weeks, allowing OEMs priority allocation and squeezing EMS gross margins by several hundred basis points in boom phases. Elemaster’s diversified end-markets smooth demand volatility but cannot offset systemic tightness; long-term forecasts and vendor-managed inventory mitigate risk.

Regulated, high-reliability inputs

Regulated, high-reliability inputs for aerospace, defense, rail and medical require certifications such as AS9100/EN 9100, EN 15085 and ISO 13485, which constrain approved vendor lists and shrink the supplier pool. Fewer compliant suppliers increase vendor bargaining power, raising prices and leverage on lead times. Any supplier requalification triggers extended timelines and added costs. Early supplier involvement and multi-approved BOMs reduce dependence and procurement risk.

Geopolitical and trade exposure

Tariffs, export controls and regionalization have tightened component availability and pricing; US CHIPS Act funding of 52.7 billion USD and concentration in foundries (TSMC ~53% share) increase supplier leverage in advanced nodes. Suppliers in sensitive nodes can enforce compliance-led restrictions, forcing Elemaster to engineer around restricted parts or redesign products. Localizing supply lowers geopolitical risk but typically raises procurement and manufacturing costs.

- Tariffs impact cost pass-through

- Export controls enable supplier leverage

- Redesign or second-sourcing required

- Localization reduces risk, increases unit cost

Equipment and test platform lock-in

Equipment vendors for SMT, AOI and ICT enforce lock-in via proprietary software, fixtures and spare parts, with service and consumable contracts often representing 8–12% of original equipment cost annually in 2024, entrenching supplier leverage over lifecycle terms.

- Vendor lock-in: proprietary SW/fixtures

- Opex impact: service/consumables ~8–12% p.a. (2024)

- Lifecycle leverage: limited bargaining on upgrades

- Mitigation: standardize platforms, negotiate bundled SLAs

12–24 week lead times and supplier concentration squeeze EMS margins

Elemaster relies on niche semiconductor, PCB and test suppliers with typical lead times 12–24 weeks, giving suppliers allocation and pricing leverage. Shortages have squeezed EMS gross margins ~200–400 bps in tight cycles; certified aerospace/medical vendors are few, raising switching costs. Equipment service/consumables run ~8–12% of OEM cost (2024), so long-term contracts and dual-sourcing remain key.

| Metric | 2024 value |

|---|---|

| Avg lead time | 12–24 weeks |

| EMS margin hit (shortage) | 200–400 bps |

| Equipment opex | 8–12% p.a. |

| TSMC market share | ~53% |

| US CHIPS funding | 52.7 billion USD |

What is included in the product

Tailored Porter's Five Forces analysis for Elemaster SpA uncovering key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position.

A concise one-sheet Porter's Five Forces for Elemaster SpA—instantly clarifies supplier, buyer, entrant and substitute pressures to streamline strategic choices and reduce research time.

Customers Bargaining Power

Large, sophisticated OEMs

Customers in aerospace, defense, medical and rail are few but highly technical, with procurement and design cycles typically spanning 3–7 years in 2024, giving OEMs strong negotiating leverage. They demand price transparency, strict SLAs and single-digit to low-double-digit penalty clauses. Large OEM orders drive volume, so trusted partnerships often trade margin for multi-year contracts and stable backlog.

Qualification lock-ins

Once a product is qualified, switching EMS providers is costly and slow, which tempers buyer power mid-program and preserves incumbent margins. At rebid or redesign—typically every 3–5 years—buyers regain leverage to benchmark suppliers globally and can reduce TCO by roughly 10–20% using aggressive sourcing. Elemaster must defend win-rates with granular performance KPIs, real-time quality data and rigorous TCO analytics to retain programs.

Demand volatility and forecast risk

Project-based, lumpy pull-ins shift inventory risk onto Elemaster as customers push volatility — industry EMS demand swings rose ~±18% in 2024, stressing cash and working capital. Buyers increasingly request consignment and flexible payment terms, pressuring margins; strong S&OP and NCNR clauses help rebalance risk and reduced inventory write-offs. Offering value-added planning services allows Elemaster to justify premium pricing and stabilize throughput.

Design ownership and IP

When customers retain design ownership, Elemaster’s differentiation shifts to cost, quality and delivery, enabling buyers to dual-source and exert pricing pressure. Providing co-design and test development embeds Elemaster deeper into product workflows, reducing pure price competition. Lifecycle engineering and aftersales services increase switching costs and customer stickiness.

- Design ownership narrows EMS differentiation

- Dual-sourcing increases pricing pressure

- Co-design/test development embeds supplier

- Lifecycle engineering raises switching costs

Compliance and penalty regimes

Regulated customers impose strict quality, traceability and on-time delivery penalties, and commonly leverage these clauses to demand credits or remediation; Elemaster’s ISO and sector-specific certifications plus zero-defect manufacturing and SPC lines are key defenses. Proactive publication of quality KPIs and on-time rates reduces dispute frequency and strengthens bargaining power.

- Certifications: core defense

- Zero-defect processes: penalty mitigation

- Quality KPIs: preempt penalties

OEM cycles, rebids shave TCO; EMS ±18% demand swings raise inventory risk

Customers in aerospace, defense, medical and rail are few, highly technical and give OEMs strong leverage with 3–7 year procurement cycles in 2024. Rebid cycles (3–5 years) let buyers cut TCO ~10–20%; incumbent switching costs and certifications limit mid-program pressure. 2024 EMS demand volatility ±18% shifts inventory risk and fuels consignment/payment requests.

| Metric | 2024 Value |

|---|---|

| Procurement cycle | 3–7 years |

| Rebid interval | 3–5 years |

| TCO reduction on rebid | 10–20% |

| EMS demand volatility | ±18% |

Preview Before You Purchase

Elemaster SpA Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Elemaster SpA you'll receive after purchase—no surprises, fully formatted and ready to use. The report assesses industry rivalry, bargaining power of suppliers and customers, threats of new entrants and substitutes, and strategic implications for Elemaster's competitive positioning. Instant access to this identical document follows your purchase.