Elevance Health Porter's Five Forces Analysis

Don't Miss the Bigger Picture

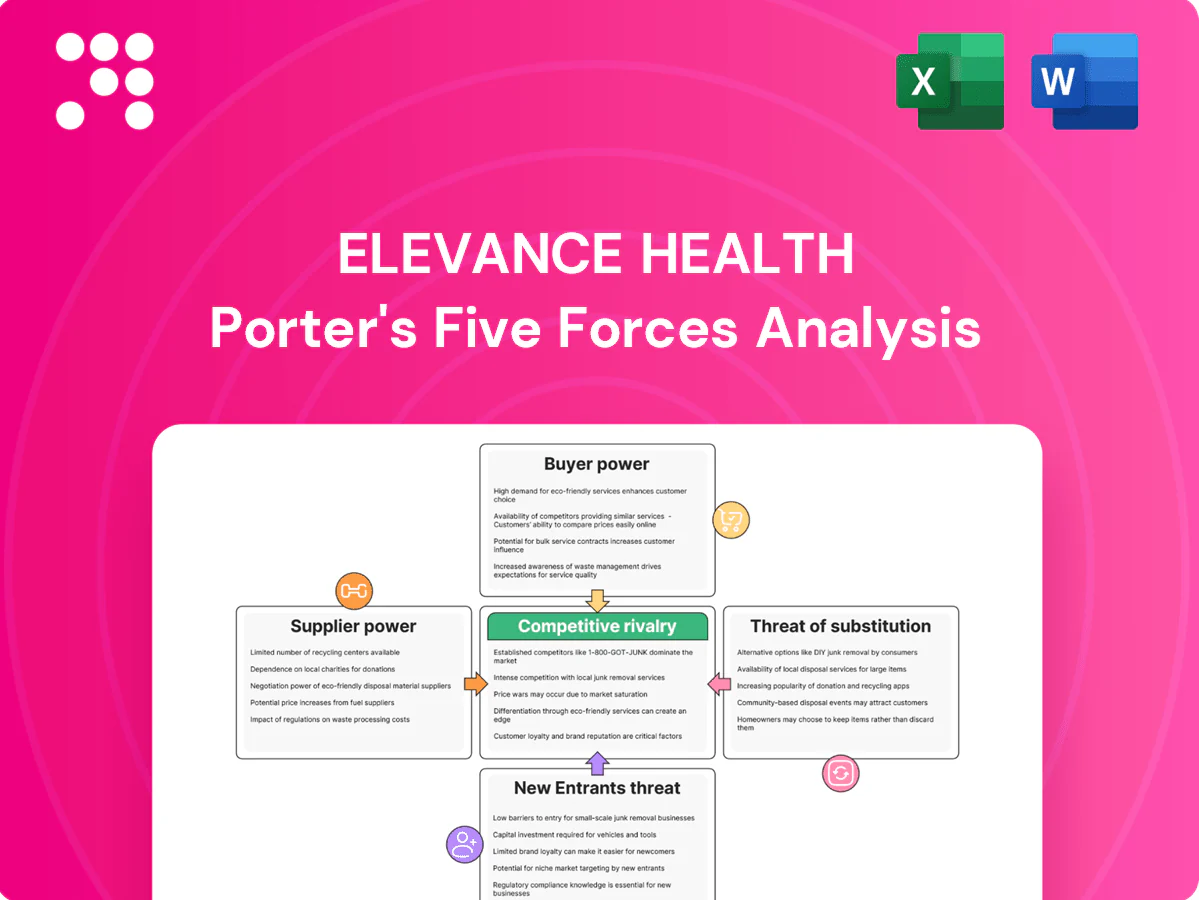

Elevance Health faces intense buyer bargaining, regulatory pressure, and competitive rivalry from insurers and tech-enabled entrants, while supplier leverage and substitute care models shape margins and growth. This snapshot highlights key tensions but omits force-by-force ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to get a consultant-grade breakdown for strategy or investment decisions.

Suppliers Bargaining Power

Consolidated hospital systems

Large consolidated hospital systems extract leverage over Elevance—which serves about 46 million members in 2024—by owning must-have facilities and branded centers of excellence, prompting Elevance to pursue multi-year contracts and steerage to control costs; in concentrated metros hospital unit prices can be 10–30% higher. Narrow and tiered networks help rebalance power but access standards and member expectations limit exclusions, while rate disputes risk network disruption and mutual concessions.

Specialist and primary care shortages

Provider scarcity in behavioral health, oncology and select PCP markets raises fee pressure; in 2024 roughly 40% of US counties lack a psychiatrist and average new‑patient PCP waits are about 24 days. Elevance leans on value‑based contracts and a ~30% lift in virtual visits versus 2020 to expand supply, but credentialing and quality guardrails slow scaling. Extended waits erode payer leverage on utilization controls; incentives and care management mitigate but do not eliminate supplier power.

Pharma manufacturers and specialty drugs

High-cost biologics and limited‑competition therapies push supplier power higher, with specialty drugs accounting for roughly 50% of US drug spending as of 2024 and single-dose gene therapies like Zolgensma priced at about $2.1M maintaining manufacturer leverage.

Formulary design, prior authorization and rising biosimilar uptake contain costs but face clinical and regulatory limits that slow savings realization.

Elevance’s integrated pharmacy services, serving ~48 million members, strengthen rebate capture and data‑driven management, yet orphan drugs and novel gene therapies keep pricing power skewed to manufacturers.

PBM, data, and tech vendors

Interoperability, claims platforms, analytics and cybersecurity are mission-critical for Elevance, creating high switching frictions; Elevance reported about $150B revenue in 2024, enabling strong in-house build and bargaining leverage. Niche PBM, data and tech vendors retain pricing power for specialized tools and data sets. Long implementation cycles (18–36 months) and compliance needs further entrench suppliers. Co-development deals often trade margin for faster innovation.

- Switching friction: high

- In-house build: reduces dependence

- Implementation: 18–36 months

- Co-dev: margin for speed

Reinsurance and ancillary services

Reinsurance and stop-loss markets materially affect Elevance Health’s capital efficiency and risk appetite; tightened capacity and hard market pricing since 2023 have raised ceded costs and shifted leverage toward reinsurers. Ancillary networks (dental, vision, behavioral) can exert local bargaining power where options are scarce, though Elevance’s scale and multi-line bundling mitigate single-supplier pressure. Elevance served about 48 million members in 2024, enhancing bundling leverage.

- Reinsurance hardening → higher ceded cost, lower capital efficiency

- Ancillary networks strong in limited local markets

- Multi-line bundling with ~48M members offsets supplier power

Supplier power squeezes margins despite scale; 46M medical, 48M pharmacy, $150B revenue

Supplier power is elevated: hospital concentration, specialty drug pricing and provider scarcity constrain Elevance’s margins despite scale; Elevance served ~46M medical and ~48M pharmacy members in 2024 and reported ~$150B revenue. Value‑based contracts and in‑house tech reduce dependence but long vendor cycles (18–36 months) and orphan drugs keep leverage with suppliers. Reinsurance hardening since 2023 raised ceded costs.

| Metric | 2024 value |

|---|---|

| Members (medical) | ~46M |

| Pharmacy reach | ~48M |

| Revenue | ~$150B |

| Specialty drug share | ~50% of drug spend |

| Counties w/o psychiatrist | ~40% |

What is included in the product

Tailored Porter’s Five Forces analysis of Elevance Health assessing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and regulatory barriers that shape pricing, margins and strategic positioning.

Clear one-sheet Porter's Five Forces for Elevance Health—instantly visualizes competitive pressure with a spider chart and customizable intensity levels, ready to drop into decks or Excel dashboards to relieve analysis bottlenecks.

Customers Bargaining Power

Large employer groups

Large national and jumbo employer groups negotiate aggressively on premiums, ASO fees and performance guarantees, leveraging multi-carrier bids and broker benchmarking while favoring custom networks and stop-loss to shift risk. In 2024 Elevance served about 47 million members and reported roughly $169 billion in revenue, countering with integrated benefits, advanced analytics and value-based outcome commitments to retain large accounts.

Government programs

Medicaid and Medicare Advantage buyers are highly price sensitive and tightly regulated, with Medicaid/CHIP covering ~82 million people and MA enrollment ~31.5 million in 2024, intensifying procurement pressure on margins. States' competitive solicitations and network rules compress rates, while CMS links MA payments to star ratings and risk scores, giving regulators indirect control over plan design. Loss of a state contract or a star downgrade can shift millions of members rapidly, hitting revenue and margins.

ACA individual members

ACA individual members show high price elasticity: roughly 15 million marketplace enrollees in 2024 and about 80% receiving premium subsidies drive sensitivity to premium changes. Annual open enrollment and plan switching, especially in counties with multiple carriers, increase buyer leverage. Network breadth and deductible levels are primary differentiators, and comparison tools/aggregators accelerate switching, compressing industry margins.

Brokers and consultants

Brokers and consultants significantly shape employer plan selection, demanding fee concessions, custom reporting and performance guarantees to secure placements. Their market-wide visibility and access to multiple carriers strengthens negotiating positions, forcing Elevance to offer clinical program commitments and outcomes-based terms. Elevance offsets this by investing in distribution enablement to maintain shelf space and broker loyalty.

- Intermediary leverage: fee concessions, reporting

- Negotiation power: market visibility, multi-carrier access

- Win criteria: performance guarantees, clinical programs

- Elevance response: distribution enablement investments

Switching costs and experience

While member disruption and provider continuity create switching frictions for Elevance Health, annual renewal cycles reopen choices; Elevance served about 48 million members in 2024, so even small churn shifts large volumes. Poor service or narrow network changes have historically triggered spikes in attrition, while improved digital engagement and care management programs lift loyalty and reduce buyer power. Competitive parity in benefits and networks erodes differentiation if not continuously refreshed.

- 48 million members in 2024 — scale magnifies churn impact

- Renewals = recurring choice points

- Digital/care mgmt reduces churn

- Network/service shifts can trigger churn

Buyers wield leverage: employers, brokers and public programs squeeze premiums

Buyers exert strong leverage: large employers demand lower premiums, ASO concessions and guarantees; brokers amplify this through multi-carrier bids. Medicaid/MA and marketplace programs (82M Medicaid/CHIP, 31.5M MA, 15M marketplace in 2024) press pricing via regulation and subsidies. Elevance (≈48M members, $169B revenue in 2024) counters with integrated benefits, analytics and value-based contracts.

| Metric | 2024 |

|---|---|

| Members | ≈48M |

| Revenue | $169B |

| Medicaid/CHIP | ≈82M |

| Medicare Advantage | ≈31.5M |

| Marketplace enrollees | ≈15M |

What You See Is What You Get

Elevance Health Porter's Five Forces Analysis

This preview shows the exact Elevance Health Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The file is the complete, professionally formatted report, ready for download and immediate use. It comprehensively covers competitive rivalry, supplier and buyer power, threat of entry, and substitutes.

Don't Miss the Bigger Picture

Elevance Health faces intense buyer bargaining, regulatory pressure, and competitive rivalry from insurers and tech-enabled entrants, while supplier leverage and substitute care models shape margins and growth. This snapshot highlights key tensions but omits force-by-force ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to get a consultant-grade breakdown for strategy or investment decisions.

Suppliers Bargaining Power

Consolidated hospital systems

Large consolidated hospital systems extract leverage over Elevance—which serves about 46 million members in 2024—by owning must-have facilities and branded centers of excellence, prompting Elevance to pursue multi-year contracts and steerage to control costs; in concentrated metros hospital unit prices can be 10–30% higher. Narrow and tiered networks help rebalance power but access standards and member expectations limit exclusions, while rate disputes risk network disruption and mutual concessions.

Specialist and primary care shortages

Provider scarcity in behavioral health, oncology and select PCP markets raises fee pressure; in 2024 roughly 40% of US counties lack a psychiatrist and average new‑patient PCP waits are about 24 days. Elevance leans on value‑based contracts and a ~30% lift in virtual visits versus 2020 to expand supply, but credentialing and quality guardrails slow scaling. Extended waits erode payer leverage on utilization controls; incentives and care management mitigate but do not eliminate supplier power.

Pharma manufacturers and specialty drugs

High-cost biologics and limited‑competition therapies push supplier power higher, with specialty drugs accounting for roughly 50% of US drug spending as of 2024 and single-dose gene therapies like Zolgensma priced at about $2.1M maintaining manufacturer leverage.

Formulary design, prior authorization and rising biosimilar uptake contain costs but face clinical and regulatory limits that slow savings realization.

Elevance’s integrated pharmacy services, serving ~48 million members, strengthen rebate capture and data‑driven management, yet orphan drugs and novel gene therapies keep pricing power skewed to manufacturers.

PBM, data, and tech vendors

Interoperability, claims platforms, analytics and cybersecurity are mission-critical for Elevance, creating high switching frictions; Elevance reported about $150B revenue in 2024, enabling strong in-house build and bargaining leverage. Niche PBM, data and tech vendors retain pricing power for specialized tools and data sets. Long implementation cycles (18–36 months) and compliance needs further entrench suppliers. Co-development deals often trade margin for faster innovation.

- Switching friction: high

- In-house build: reduces dependence

- Implementation: 18–36 months

- Co-dev: margin for speed

Reinsurance and ancillary services

Reinsurance and stop-loss markets materially affect Elevance Health’s capital efficiency and risk appetite; tightened capacity and hard market pricing since 2023 have raised ceded costs and shifted leverage toward reinsurers. Ancillary networks (dental, vision, behavioral) can exert local bargaining power where options are scarce, though Elevance’s scale and multi-line bundling mitigate single-supplier pressure. Elevance served about 48 million members in 2024, enhancing bundling leverage.

- Reinsurance hardening → higher ceded cost, lower capital efficiency

- Ancillary networks strong in limited local markets

- Multi-line bundling with ~48M members offsets supplier power

Supplier power squeezes margins despite scale; 46M medical, 48M pharmacy, $150B revenue

Supplier power is elevated: hospital concentration, specialty drug pricing and provider scarcity constrain Elevance’s margins despite scale; Elevance served ~46M medical and ~48M pharmacy members in 2024 and reported ~$150B revenue. Value‑based contracts and in‑house tech reduce dependence but long vendor cycles (18–36 months) and orphan drugs keep leverage with suppliers. Reinsurance hardening since 2023 raised ceded costs.

| Metric | 2024 value |

|---|---|

| Members (medical) | ~46M |

| Pharmacy reach | ~48M |

| Revenue | ~$150B |

| Specialty drug share | ~50% of drug spend |

| Counties w/o psychiatrist | ~40% |

What is included in the product

Tailored Porter’s Five Forces analysis of Elevance Health assessing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and regulatory barriers that shape pricing, margins and strategic positioning.

Clear one-sheet Porter's Five Forces for Elevance Health—instantly visualizes competitive pressure with a spider chart and customizable intensity levels, ready to drop into decks or Excel dashboards to relieve analysis bottlenecks.

Customers Bargaining Power

Large employer groups

Large national and jumbo employer groups negotiate aggressively on premiums, ASO fees and performance guarantees, leveraging multi-carrier bids and broker benchmarking while favoring custom networks and stop-loss to shift risk. In 2024 Elevance served about 47 million members and reported roughly $169 billion in revenue, countering with integrated benefits, advanced analytics and value-based outcome commitments to retain large accounts.

Government programs

Medicaid and Medicare Advantage buyers are highly price sensitive and tightly regulated, with Medicaid/CHIP covering ~82 million people and MA enrollment ~31.5 million in 2024, intensifying procurement pressure on margins. States' competitive solicitations and network rules compress rates, while CMS links MA payments to star ratings and risk scores, giving regulators indirect control over plan design. Loss of a state contract or a star downgrade can shift millions of members rapidly, hitting revenue and margins.

ACA individual members

ACA individual members show high price elasticity: roughly 15 million marketplace enrollees in 2024 and about 80% receiving premium subsidies drive sensitivity to premium changes. Annual open enrollment and plan switching, especially in counties with multiple carriers, increase buyer leverage. Network breadth and deductible levels are primary differentiators, and comparison tools/aggregators accelerate switching, compressing industry margins.

Brokers and consultants

Brokers and consultants significantly shape employer plan selection, demanding fee concessions, custom reporting and performance guarantees to secure placements. Their market-wide visibility and access to multiple carriers strengthens negotiating positions, forcing Elevance to offer clinical program commitments and outcomes-based terms. Elevance offsets this by investing in distribution enablement to maintain shelf space and broker loyalty.

- Intermediary leverage: fee concessions, reporting

- Negotiation power: market visibility, multi-carrier access

- Win criteria: performance guarantees, clinical programs

- Elevance response: distribution enablement investments

Switching costs and experience

While member disruption and provider continuity create switching frictions for Elevance Health, annual renewal cycles reopen choices; Elevance served about 48 million members in 2024, so even small churn shifts large volumes. Poor service or narrow network changes have historically triggered spikes in attrition, while improved digital engagement and care management programs lift loyalty and reduce buyer power. Competitive parity in benefits and networks erodes differentiation if not continuously refreshed.

- 48 million members in 2024 — scale magnifies churn impact

- Renewals = recurring choice points

- Digital/care mgmt reduces churn

- Network/service shifts can trigger churn

Buyers wield leverage: employers, brokers and public programs squeeze premiums

Buyers exert strong leverage: large employers demand lower premiums, ASO concessions and guarantees; brokers amplify this through multi-carrier bids. Medicaid/MA and marketplace programs (82M Medicaid/CHIP, 31.5M MA, 15M marketplace in 2024) press pricing via regulation and subsidies. Elevance (≈48M members, $169B revenue in 2024) counters with integrated benefits, analytics and value-based contracts.

| Metric | 2024 |

|---|---|

| Members | ≈48M |

| Revenue | $169B |

| Medicaid/CHIP | ≈82M |

| Medicare Advantage | ≈31.5M |

| Marketplace enrollees | ≈15M |

What You See Is What You Get

Elevance Health Porter's Five Forces Analysis

This preview shows the exact Elevance Health Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The file is the complete, professionally formatted report, ready for download and immediate use. It comprehensively covers competitive rivalry, supplier and buyer power, threat of entry, and substitutes.

Description

Don't Miss the Bigger Picture

Elevance Health faces intense buyer bargaining, regulatory pressure, and competitive rivalry from insurers and tech-enabled entrants, while supplier leverage and substitute care models shape margins and growth. This snapshot highlights key tensions but omits force-by-force ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to get a consultant-grade breakdown for strategy or investment decisions.

Suppliers Bargaining Power

Consolidated hospital systems

Large consolidated hospital systems extract leverage over Elevance—which serves about 46 million members in 2024—by owning must-have facilities and branded centers of excellence, prompting Elevance to pursue multi-year contracts and steerage to control costs; in concentrated metros hospital unit prices can be 10–30% higher. Narrow and tiered networks help rebalance power but access standards and member expectations limit exclusions, while rate disputes risk network disruption and mutual concessions.

Specialist and primary care shortages

Provider scarcity in behavioral health, oncology and select PCP markets raises fee pressure; in 2024 roughly 40% of US counties lack a psychiatrist and average new‑patient PCP waits are about 24 days. Elevance leans on value‑based contracts and a ~30% lift in virtual visits versus 2020 to expand supply, but credentialing and quality guardrails slow scaling. Extended waits erode payer leverage on utilization controls; incentives and care management mitigate but do not eliminate supplier power.

Pharma manufacturers and specialty drugs

High-cost biologics and limited‑competition therapies push supplier power higher, with specialty drugs accounting for roughly 50% of US drug spending as of 2024 and single-dose gene therapies like Zolgensma priced at about $2.1M maintaining manufacturer leverage.

Formulary design, prior authorization and rising biosimilar uptake contain costs but face clinical and regulatory limits that slow savings realization.

Elevance’s integrated pharmacy services, serving ~48 million members, strengthen rebate capture and data‑driven management, yet orphan drugs and novel gene therapies keep pricing power skewed to manufacturers.

PBM, data, and tech vendors

Interoperability, claims platforms, analytics and cybersecurity are mission-critical for Elevance, creating high switching frictions; Elevance reported about $150B revenue in 2024, enabling strong in-house build and bargaining leverage. Niche PBM, data and tech vendors retain pricing power for specialized tools and data sets. Long implementation cycles (18–36 months) and compliance needs further entrench suppliers. Co-development deals often trade margin for faster innovation.

- Switching friction: high

- In-house build: reduces dependence

- Implementation: 18–36 months

- Co-dev: margin for speed

Reinsurance and ancillary services

Reinsurance and stop-loss markets materially affect Elevance Health’s capital efficiency and risk appetite; tightened capacity and hard market pricing since 2023 have raised ceded costs and shifted leverage toward reinsurers. Ancillary networks (dental, vision, behavioral) can exert local bargaining power where options are scarce, though Elevance’s scale and multi-line bundling mitigate single-supplier pressure. Elevance served about 48 million members in 2024, enhancing bundling leverage.

- Reinsurance hardening → higher ceded cost, lower capital efficiency

- Ancillary networks strong in limited local markets

- Multi-line bundling with ~48M members offsets supplier power

Supplier power squeezes margins despite scale; 46M medical, 48M pharmacy, $150B revenue

Supplier power is elevated: hospital concentration, specialty drug pricing and provider scarcity constrain Elevance’s margins despite scale; Elevance served ~46M medical and ~48M pharmacy members in 2024 and reported ~$150B revenue. Value‑based contracts and in‑house tech reduce dependence but long vendor cycles (18–36 months) and orphan drugs keep leverage with suppliers. Reinsurance hardening since 2023 raised ceded costs.

| Metric | 2024 value |

|---|---|

| Members (medical) | ~46M |

| Pharmacy reach | ~48M |

| Revenue | ~$150B |

| Specialty drug share | ~50% of drug spend |

| Counties w/o psychiatrist | ~40% |

What is included in the product

Tailored Porter’s Five Forces analysis of Elevance Health assessing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and regulatory barriers that shape pricing, margins and strategic positioning.

Clear one-sheet Porter's Five Forces for Elevance Health—instantly visualizes competitive pressure with a spider chart and customizable intensity levels, ready to drop into decks or Excel dashboards to relieve analysis bottlenecks.

Customers Bargaining Power

Large employer groups

Large national and jumbo employer groups negotiate aggressively on premiums, ASO fees and performance guarantees, leveraging multi-carrier bids and broker benchmarking while favoring custom networks and stop-loss to shift risk. In 2024 Elevance served about 47 million members and reported roughly $169 billion in revenue, countering with integrated benefits, advanced analytics and value-based outcome commitments to retain large accounts.

Government programs

Medicaid and Medicare Advantage buyers are highly price sensitive and tightly regulated, with Medicaid/CHIP covering ~82 million people and MA enrollment ~31.5 million in 2024, intensifying procurement pressure on margins. States' competitive solicitations and network rules compress rates, while CMS links MA payments to star ratings and risk scores, giving regulators indirect control over plan design. Loss of a state contract or a star downgrade can shift millions of members rapidly, hitting revenue and margins.

ACA individual members

ACA individual members show high price elasticity: roughly 15 million marketplace enrollees in 2024 and about 80% receiving premium subsidies drive sensitivity to premium changes. Annual open enrollment and plan switching, especially in counties with multiple carriers, increase buyer leverage. Network breadth and deductible levels are primary differentiators, and comparison tools/aggregators accelerate switching, compressing industry margins.

Brokers and consultants

Brokers and consultants significantly shape employer plan selection, demanding fee concessions, custom reporting and performance guarantees to secure placements. Their market-wide visibility and access to multiple carriers strengthens negotiating positions, forcing Elevance to offer clinical program commitments and outcomes-based terms. Elevance offsets this by investing in distribution enablement to maintain shelf space and broker loyalty.

- Intermediary leverage: fee concessions, reporting

- Negotiation power: market visibility, multi-carrier access

- Win criteria: performance guarantees, clinical programs

- Elevance response: distribution enablement investments

Switching costs and experience

While member disruption and provider continuity create switching frictions for Elevance Health, annual renewal cycles reopen choices; Elevance served about 48 million members in 2024, so even small churn shifts large volumes. Poor service or narrow network changes have historically triggered spikes in attrition, while improved digital engagement and care management programs lift loyalty and reduce buyer power. Competitive parity in benefits and networks erodes differentiation if not continuously refreshed.

- 48 million members in 2024 — scale magnifies churn impact

- Renewals = recurring choice points

- Digital/care mgmt reduces churn

- Network/service shifts can trigger churn

Buyers wield leverage: employers, brokers and public programs squeeze premiums

Buyers exert strong leverage: large employers demand lower premiums, ASO concessions and guarantees; brokers amplify this through multi-carrier bids. Medicaid/MA and marketplace programs (82M Medicaid/CHIP, 31.5M MA, 15M marketplace in 2024) press pricing via regulation and subsidies. Elevance (≈48M members, $169B revenue in 2024) counters with integrated benefits, analytics and value-based contracts.

| Metric | 2024 |

|---|---|

| Members | ≈48M |

| Revenue | $169B |

| Medicaid/CHIP | ≈82M |

| Medicare Advantage | ≈31.5M |

| Marketplace enrollees | ≈15M |

What You See Is What You Get

Elevance Health Porter's Five Forces Analysis

This preview shows the exact Elevance Health Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The file is the complete, professionally formatted report, ready for download and immediate use. It comprehensively covers competitive rivalry, supplier and buyer power, threat of entry, and substitutes.