Elia Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Elia Group faces regulated monopolistic characteristics, rising supplier leverage for grid tech, moderate buyer power from utilities and large corporates, and growing pressure from decentralised renewables and storage as substitutes. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Concentrated OEM base

As of 2024 only a few global OEMs—Siemens Energy, Hitachi Energy, GE Grid Solutions and NKT—dominate high‑voltage cables, transformers and switchgear markets. Limited alternatives push lead times to roughly 12–24 months and give suppliers pricing power. Dual‑sourcing is feasible but constrained by technical standards and certifications. Framework agreements reduce supply risk but do not prevent price spikes or shortages at peak demand.

Specialized HVDC tech

Converter stations and subsea HVDC systems depend on a handful of vendors—Siemens Energy, Hitachi Energy, GE Grid Solutions—creating concentrated supplier power; large projects like NordLink (1,400 MW, ~€1.5bn) illustrate scale. Project complexity, certification and interface risk force TSOs such as Elia to accept vendor terms, while qualification cycles commonly exceed 18–24 months, reinforcing supplier leverage.

EPC and skilled labor scarcity

Large grid builds demand scarce EPC and skilled labor, concentrating supplier power as experienced transmission engineers and construction teams are limited. Tight European markets and wage inflation (around 4–5% recent wage growth) raise contractor pricing and scarcity premiums. Specialized safety, permitting and HV expertise further narrows providers, and schedule risk often shifts margin pressure onto contractors.

IT/OT and cybersecurity vendors

Right-of-way and materials volatility

Concentrated HV suppliers create 12–24 month lead times, pricing power and copper/steel exposure

As of 2024 a few OEMs (Siemens Energy, Hitachi Energy, GE, NKT) concentrate high‑voltage supply, producing 12–24 month lead times and pricing power. HVDC vendors control large projects; qualification cycles exceed 18–24 months. 2024 capex ~€2.2bn raises exposure to copper/steel volatility despite hedging.

| Metric | Value (2024) |

|---|---|

| Lead times | 12–24 months |

| Qualification cycle | >18–24 months |

| Elia capex | ~€2.2bn |

What is included in the product

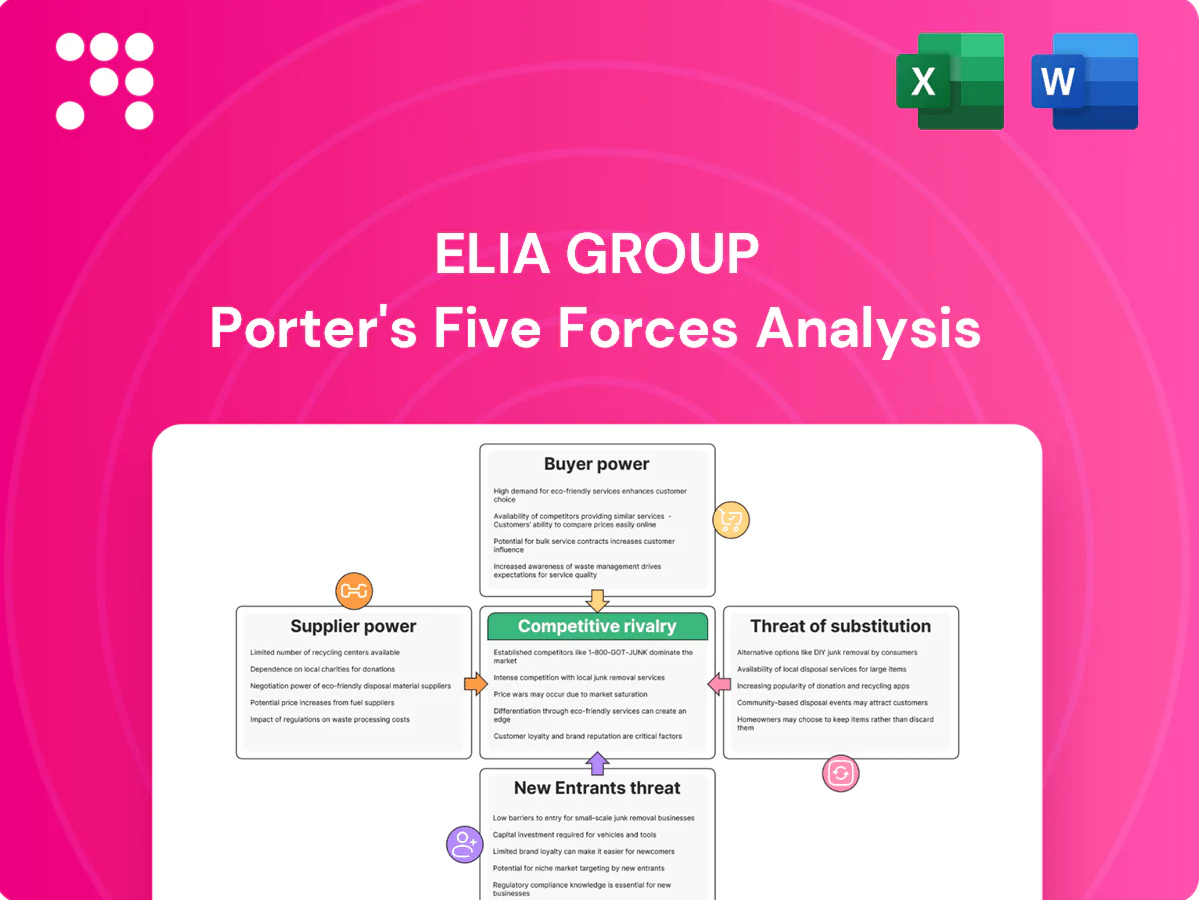

Tailored Porter's Five Forces analysis of Elia Group highlighting competitive rivalry in transmission networks, buyer and supplier bargaining power, barriers deterring new grid entrants, and threats from substitutes and regulatory shifts that could reshape profitability and strategic positioning.

Clear, one-sheet Porter's Five Forces for Elia Group that translates regulatory, supplier and entrant pressures into actionable scores—perfect for fast boardroom decisions. Customize inputs and export charts for decks.

Customers Bargaining Power

Regulated captive users

Grid users—DSOs, generators and large industry—are captive to Elia as the sole TSO for cross-area transmission; Belgian annual consumption was about 78 TWh in 2024, reinforcing dependency. Tariffs are largely set by regulator CREG, capping direct buyer power; within a control area switching is infeasible and short-term demand elasticity remains very low.

Regulatory oversight as proxy power

Customers influence regulatory frameworks through formal consultations, and in 2024 stakeholder feedback helped shape Belgium’s transmission tariff review that adjusted allowed revenues by about 5%, demonstrating downstream bargaining leverage. Regulators can alter allowed revenues and incentive schemes, shifting Elia’s investment timing and service levels. This indirect channel ties compliance and revenue to performance metrics, with up to 20% of variable remuneration linked to reliability targets in recent frameworks.

Large industrials’ negotiation

Large industrials push for tailored connections and timelines, leveraging projects of up to several hundred MW and representing significant shares of Elia’s peak load (~18 GW in 2024). Their scale lets them lobby for cost allocation and curtailment rules, shaping tariffs and queue priorities. Technical standards restrict deep customization, keeping solutions within grid codes. Payment risk is low but schedule pressure remains high.

Market participants’ service demands

Cross-border stakeholders

Neighboring TSOs and interconnector users, notably Nemo Link (1,000 MW), shape Elia Group operational choices via flow management and congestion allocation.

Joint planning through ENTSO-E mechanisms forces negotiation on cost sharing and capacity allocation; Elia’s majority stake in 50Hertz (serving ~18 million customers) raises cross-border stakes, while physical grid and HVDC limits cap customer leverage.

- Interconnector: Nemo Link 1,000 MW

- Platform: ENTSO-E harmonization pressure

- Cross-border asset: 50Hertz ~18M customers

- Constraint: finite HVDC/grid capacity

Sole Belgian TSO traps users; 78 TWh consumption, 18 GW peak

Grid users (DSOs, generators, large industry) are captive to Elia as sole Belgian TSO; national consumption ~78 TWh and peak ~18 GW in 2024 limit switching. Regulator CREG sets tariffs (2024 tariff review adjusted allowed revenues ~5%) reducing direct buyer price power, but stakeholder inputs can shift incentives (up to 20% variable pay tied to reliability). Large industrials and interconnector users (Nemo Link 1,000 MW) press for bespoke connections and transparency; alternatives are limited.

| Metric | 2024 value |

|---|---|

| Belgian consumption | ~78 TWh |

| Peak load | ~18 GW |

| Nemo Link | 1,000 MW |

| Tariff review impact | ~+5% allowed rev |

Preview the Actual Deliverable

Elia Group Porter's Five Forces Analysis

This preview shows the exact Elia Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the full, professionally formatted analysis, ready for download and use the moment you buy. It includes a detailed assessment of competitive rivalry, supplier and buyer power, and threats of substitutes and new entry, with clear strategic implications.

A Must-Have Tool for Decision-Makers

Elia Group faces regulated monopolistic characteristics, rising supplier leverage for grid tech, moderate buyer power from utilities and large corporates, and growing pressure from decentralised renewables and storage as substitutes. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Concentrated OEM base

As of 2024 only a few global OEMs—Siemens Energy, Hitachi Energy, GE Grid Solutions and NKT—dominate high‑voltage cables, transformers and switchgear markets. Limited alternatives push lead times to roughly 12–24 months and give suppliers pricing power. Dual‑sourcing is feasible but constrained by technical standards and certifications. Framework agreements reduce supply risk but do not prevent price spikes or shortages at peak demand.

Specialized HVDC tech

Converter stations and subsea HVDC systems depend on a handful of vendors—Siemens Energy, Hitachi Energy, GE Grid Solutions—creating concentrated supplier power; large projects like NordLink (1,400 MW, ~€1.5bn) illustrate scale. Project complexity, certification and interface risk force TSOs such as Elia to accept vendor terms, while qualification cycles commonly exceed 18–24 months, reinforcing supplier leverage.

EPC and skilled labor scarcity

Large grid builds demand scarce EPC and skilled labor, concentrating supplier power as experienced transmission engineers and construction teams are limited. Tight European markets and wage inflation (around 4–5% recent wage growth) raise contractor pricing and scarcity premiums. Specialized safety, permitting and HV expertise further narrows providers, and schedule risk often shifts margin pressure onto contractors.

IT/OT and cybersecurity vendors

Right-of-way and materials volatility

Concentrated HV suppliers create 12–24 month lead times, pricing power and copper/steel exposure

As of 2024 a few OEMs (Siemens Energy, Hitachi Energy, GE, NKT) concentrate high‑voltage supply, producing 12–24 month lead times and pricing power. HVDC vendors control large projects; qualification cycles exceed 18–24 months. 2024 capex ~€2.2bn raises exposure to copper/steel volatility despite hedging.

| Metric | Value (2024) |

|---|---|

| Lead times | 12–24 months |

| Qualification cycle | >18–24 months |

| Elia capex | ~€2.2bn |

What is included in the product

Tailored Porter's Five Forces analysis of Elia Group highlighting competitive rivalry in transmission networks, buyer and supplier bargaining power, barriers deterring new grid entrants, and threats from substitutes and regulatory shifts that could reshape profitability and strategic positioning.

Clear, one-sheet Porter's Five Forces for Elia Group that translates regulatory, supplier and entrant pressures into actionable scores—perfect for fast boardroom decisions. Customize inputs and export charts for decks.

Customers Bargaining Power

Regulated captive users

Grid users—DSOs, generators and large industry—are captive to Elia as the sole TSO for cross-area transmission; Belgian annual consumption was about 78 TWh in 2024, reinforcing dependency. Tariffs are largely set by regulator CREG, capping direct buyer power; within a control area switching is infeasible and short-term demand elasticity remains very low.

Regulatory oversight as proxy power

Customers influence regulatory frameworks through formal consultations, and in 2024 stakeholder feedback helped shape Belgium’s transmission tariff review that adjusted allowed revenues by about 5%, demonstrating downstream bargaining leverage. Regulators can alter allowed revenues and incentive schemes, shifting Elia’s investment timing and service levels. This indirect channel ties compliance and revenue to performance metrics, with up to 20% of variable remuneration linked to reliability targets in recent frameworks.

Large industrials’ negotiation

Large industrials push for tailored connections and timelines, leveraging projects of up to several hundred MW and representing significant shares of Elia’s peak load (~18 GW in 2024). Their scale lets them lobby for cost allocation and curtailment rules, shaping tariffs and queue priorities. Technical standards restrict deep customization, keeping solutions within grid codes. Payment risk is low but schedule pressure remains high.

Market participants’ service demands

Cross-border stakeholders

Neighboring TSOs and interconnector users, notably Nemo Link (1,000 MW), shape Elia Group operational choices via flow management and congestion allocation.

Joint planning through ENTSO-E mechanisms forces negotiation on cost sharing and capacity allocation; Elia’s majority stake in 50Hertz (serving ~18 million customers) raises cross-border stakes, while physical grid and HVDC limits cap customer leverage.

- Interconnector: Nemo Link 1,000 MW

- Platform: ENTSO-E harmonization pressure

- Cross-border asset: 50Hertz ~18M customers

- Constraint: finite HVDC/grid capacity

Sole Belgian TSO traps users; 78 TWh consumption, 18 GW peak

Grid users (DSOs, generators, large industry) are captive to Elia as sole Belgian TSO; national consumption ~78 TWh and peak ~18 GW in 2024 limit switching. Regulator CREG sets tariffs (2024 tariff review adjusted allowed revenues ~5%) reducing direct buyer price power, but stakeholder inputs can shift incentives (up to 20% variable pay tied to reliability). Large industrials and interconnector users (Nemo Link 1,000 MW) press for bespoke connections and transparency; alternatives are limited.

| Metric | 2024 value |

|---|---|

| Belgian consumption | ~78 TWh |

| Peak load | ~18 GW |

| Nemo Link | 1,000 MW |

| Tariff review impact | ~+5% allowed rev |

Preview the Actual Deliverable

Elia Group Porter's Five Forces Analysis

This preview shows the exact Elia Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the full, professionally formatted analysis, ready for download and use the moment you buy. It includes a detailed assessment of competitive rivalry, supplier and buyer power, and threats of substitutes and new entry, with clear strategic implications.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Elia Group faces regulated monopolistic characteristics, rising supplier leverage for grid tech, moderate buyer power from utilities and large corporates, and growing pressure from decentralised renewables and storage as substitutes. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis for a force-by-force strategic breakdown and actionable insights.

Suppliers Bargaining Power

Concentrated OEM base

As of 2024 only a few global OEMs—Siemens Energy, Hitachi Energy, GE Grid Solutions and NKT—dominate high‑voltage cables, transformers and switchgear markets. Limited alternatives push lead times to roughly 12–24 months and give suppliers pricing power. Dual‑sourcing is feasible but constrained by technical standards and certifications. Framework agreements reduce supply risk but do not prevent price spikes or shortages at peak demand.

Specialized HVDC tech

Converter stations and subsea HVDC systems depend on a handful of vendors—Siemens Energy, Hitachi Energy, GE Grid Solutions—creating concentrated supplier power; large projects like NordLink (1,400 MW, ~€1.5bn) illustrate scale. Project complexity, certification and interface risk force TSOs such as Elia to accept vendor terms, while qualification cycles commonly exceed 18–24 months, reinforcing supplier leverage.

EPC and skilled labor scarcity

Large grid builds demand scarce EPC and skilled labor, concentrating supplier power as experienced transmission engineers and construction teams are limited. Tight European markets and wage inflation (around 4–5% recent wage growth) raise contractor pricing and scarcity premiums. Specialized safety, permitting and HV expertise further narrows providers, and schedule risk often shifts margin pressure onto contractors.

IT/OT and cybersecurity vendors

Right-of-way and materials volatility

Concentrated HV suppliers create 12–24 month lead times, pricing power and copper/steel exposure

As of 2024 a few OEMs (Siemens Energy, Hitachi Energy, GE, NKT) concentrate high‑voltage supply, producing 12–24 month lead times and pricing power. HVDC vendors control large projects; qualification cycles exceed 18–24 months. 2024 capex ~€2.2bn raises exposure to copper/steel volatility despite hedging.

| Metric | Value (2024) |

|---|---|

| Lead times | 12–24 months |

| Qualification cycle | >18–24 months |

| Elia capex | ~€2.2bn |

What is included in the product

Tailored Porter's Five Forces analysis of Elia Group highlighting competitive rivalry in transmission networks, buyer and supplier bargaining power, barriers deterring new grid entrants, and threats from substitutes and regulatory shifts that could reshape profitability and strategic positioning.

Clear, one-sheet Porter's Five Forces for Elia Group that translates regulatory, supplier and entrant pressures into actionable scores—perfect for fast boardroom decisions. Customize inputs and export charts for decks.

Customers Bargaining Power

Regulated captive users

Grid users—DSOs, generators and large industry—are captive to Elia as the sole TSO for cross-area transmission; Belgian annual consumption was about 78 TWh in 2024, reinforcing dependency. Tariffs are largely set by regulator CREG, capping direct buyer power; within a control area switching is infeasible and short-term demand elasticity remains very low.

Regulatory oversight as proxy power

Customers influence regulatory frameworks through formal consultations, and in 2024 stakeholder feedback helped shape Belgium’s transmission tariff review that adjusted allowed revenues by about 5%, demonstrating downstream bargaining leverage. Regulators can alter allowed revenues and incentive schemes, shifting Elia’s investment timing and service levels. This indirect channel ties compliance and revenue to performance metrics, with up to 20% of variable remuneration linked to reliability targets in recent frameworks.

Large industrials’ negotiation

Large industrials push for tailored connections and timelines, leveraging projects of up to several hundred MW and representing significant shares of Elia’s peak load (~18 GW in 2024). Their scale lets them lobby for cost allocation and curtailment rules, shaping tariffs and queue priorities. Technical standards restrict deep customization, keeping solutions within grid codes. Payment risk is low but schedule pressure remains high.

Market participants’ service demands

Cross-border stakeholders

Neighboring TSOs and interconnector users, notably Nemo Link (1,000 MW), shape Elia Group operational choices via flow management and congestion allocation.

Joint planning through ENTSO-E mechanisms forces negotiation on cost sharing and capacity allocation; Elia’s majority stake in 50Hertz (serving ~18 million customers) raises cross-border stakes, while physical grid and HVDC limits cap customer leverage.

- Interconnector: Nemo Link 1,000 MW

- Platform: ENTSO-E harmonization pressure

- Cross-border asset: 50Hertz ~18M customers

- Constraint: finite HVDC/grid capacity

Sole Belgian TSO traps users; 78 TWh consumption, 18 GW peak

Grid users (DSOs, generators, large industry) are captive to Elia as sole Belgian TSO; national consumption ~78 TWh and peak ~18 GW in 2024 limit switching. Regulator CREG sets tariffs (2024 tariff review adjusted allowed revenues ~5%) reducing direct buyer price power, but stakeholder inputs can shift incentives (up to 20% variable pay tied to reliability). Large industrials and interconnector users (Nemo Link 1,000 MW) press for bespoke connections and transparency; alternatives are limited.

| Metric | 2024 value |

|---|---|

| Belgian consumption | ~78 TWh |

| Peak load | ~18 GW |

| Nemo Link | 1,000 MW |

| Tariff review impact | ~+5% allowed rev |

Preview the Actual Deliverable

Elia Group Porter's Five Forces Analysis

This preview shows the exact Elia Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the full, professionally formatted analysis, ready for download and use the moment you buy. It includes a detailed assessment of competitive rivalry, supplier and buyer power, and threats of substitutes and new entry, with clear strategic implications.