Elopak Porter's Five Forces Analysis

Don't Miss the Bigger Picture

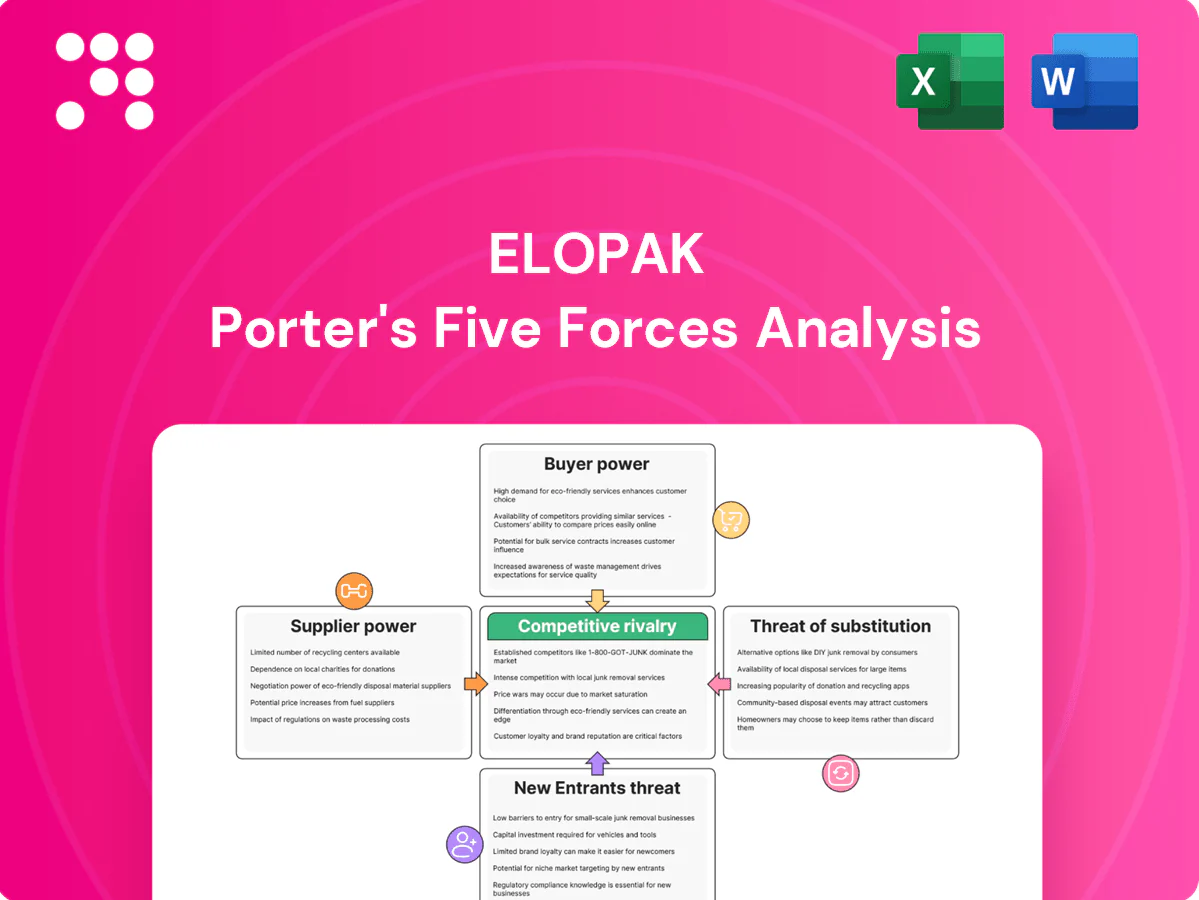

Elopak faces moderate supplier power, strong buyer pressure for sustainable and cost-efficient cartons, rising substitute threats, and intense rivalry among global packagers. Barriers to entry are moderate given capital requirements and regulation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elopak’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated paperboard sources

Elopak depends on a limited set of large cartonboard mills for high-spec food-grade material, creating supplier concentration that raises dependency and supplier pricing power. Stringent certifications such as FSC and PEFC plus barrier-grade specifications further limit the pool of qualified suppliers. Elopak’s long-term contracts and dual-sourcing reduce exposure but do not eliminate supply and price risk.

Specialized barrier materials

Polyethylene, biopolymers and aluminum/ALD coatings are central to aseptic integrity and shelf-life, with global polyethylene supply around 110 million tonnes in 2024. Few suppliers meet strict food-contact and sustainability standards, concentrating supplier power. Volatility in resin and LME aluminum markets transmits to packaging costs, and long qualification cycles (months to >1 year) limit rapid switching.

Proprietary machine components

Aseptic filling lines rely on precision parts, electronics and validated consumables whose approved vendors create high qualification barriers, giving suppliers leverage over pricing and delivery. Disruptions to these proprietary components directly threaten uptime targets—service SLAs commonly demand >98% availability—and can trigger penalty exposure. Framework agreements and multi-month inventory buffers mitigate but do not eliminate supplier concentration risk.

Logistics and energy sensitivity

Transport, energy, and pulp costs materially shape carton economics for Elopak; pulp can represent roughly 30-40% of carton raw-material cost and EU industrial electricity spikes (peaking near €200/MWh in 2023–24 episodes) and freight disruptions raised logistics premiums by an estimated 10–25% in 2024, tightening supplier leverage. Suppliers can prioritize larger, nearer customers during bottlenecks, but nearshoring and multimodal logistics reduced exposure and shortened lead times by ~15–20% in 2024.

- pulp share ~30–40% of raw-material cost

- EU industrial electricity spikes near €200/MWh (peak episodes)

- logistics premiums up ~10–25% in 2024; nearshoring cut lead times ~15–20%

Sustainability spec tightening

Sustainability spec tightening reduces supplier pool as demand for recyclable, low-carbon and plastic-reduced structures forces Elopak to source specialized cartonboard, barrier coatings and mono-material caps that meet recyclability standards and tethered-cap requirements under evolving EU/UK rules.

Suppliers of certified recycled or low-carbon inputs command pricing power and premiums, while co-development agreements for barrier tech or recycled-content formulations deepen dependence on a few qualified vendors.

- Supplier scarcity: fewer certified recyclable/low-carbon input providers

- Regulatory squeeze: tethered-cap and recyclability rules raise qualification barriers

- Price pressure: greener inputs often carry premiums

- Dependency: co-development increases vendor lock-in

30-40% pulp; 110Mt PE; logistics +10-25%

Supplier concentration for high-spec cartonboard and barrier materials gives vendors meaningful pricing power; pulp is ~30–40% of carton raw cost. Polyethylene global supply ~110Mt (2024) and resin/aluminum volatility plus logistics premiums +10–25% (2024) transmit cost risk. Sustainability specs shrink qualified suppliers and prolong qualification (months–>1 year).

| Factor | 2024 Metric | Impact |

|---|---|---|

| Pulp share | 30–40% of raw cost | High price sensitivity |

| PE supply | ~110 Mt | Concentrated suppliers |

| Logistics | +10–25% premiums | Higher procurement cost |

What is included in the product

Tailored exclusively for Elopak, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitutes and entry barriers, and identifies disruptive threats and strategic levers affecting pricing, profitability and market position.

A clear one-sheet Porter's Five Forces for Elopak that maps competitive pressures on a spider chart and is fully customizable to new data or scenarios for rapid strategic decisions, with a clean layout ready for pitch decks and seamless integration into broader dashboards.

Customers Bargaining Power

Highly concentrated buyers

Dairy and beverage multinationals and large retailers account for the bulk of Elopak's volumes, giving buyers strong leverage to press for lower prices and tougher terms. Their scale forces suppliers into fierce competition, especially as multi-year tenders commonly run 3–5 years and lock in preferred partners. Losing a single major account can materially dent plant utilization and margins. This concentrated buyer base thus amplifies price sensitivity and contract risk.

Installed base switching costs

Filling lines, staff training, and bespoke formats create strong installed-base switching costs that lock in customers and suppliers, often making conversion projects take 3–9 months. Customers can still leverage competing vendors offering compatible formats, keeping negotiating leverage. Total cost of ownership and service quality dominate the switching calculus, especially for high-volume dairy and beverage clients. Line conversion incentives and payback offers frequently tip decisions in practice.

Private label and cost focus

Retailer private-label focus—European grocery private-label penetration around 40% in 2023—pushes unit economics and speed-to-shelf, forcing demands for price breaks, lightweighting and promotional support.

Customers press packaging vendors to demonstrate total system savings (logistics, fill-speed, waste), not just per-package price, raising evidence requirements in contracts.

Ongoing margin compression risk for Elopak is acute as retailers extract cost concessions while expecting investment in lightweight R&D and shelf-ready innovations.

Sustainability and innovation demands

Buyers increasingly demand lower carbon footprints, higher recyclability and reduced plastic content; failure to meet 2024 ESG expectations — driven by CSRD roll-out for EU suppliers in 2024 — prompts retailer re-evaluation and contract risk. Co-development roadmaps and transparent LCA datasets are now table stakes, with major retailers requiring LCA evidence during sourcing.

- CSRD 2024: expanded ESG reporting for large EU suppliers

- Co-development roadmaps expected by major retailers

- Transparent LCA data mandatory in RFQs

- ESG shortfalls trigger supplier re-evaluation

Multi-sourcing strategies

Large customers often dual-source to manage risk and keep pricing competitive; in 2024 roughly 60% of major beverage and dairy buyers reported dual-sourcing packaging suppliers, reducing single-vendor exposure. Qualification of alternate formats lowers vendor dependence while annual scorecards (with penalties) drive continuous improvement; deep service relationships and >99.5% uptime can blunt buyer leverage.

- Dual-sourcing ~60% (2024)

- Alternate-format qualification reduces dependency

- Annual scorecards + penalties enforce performance

- Service depth >99.5% uptime reduces buyer power

Retailer leverage, tenders and ESG/private-label pressure squeeze dairy/beverage margins

Large dairy/beverage customers and retailers wield high leverage — losing one client can cut utilization and margins, while multi-year tenders (3–5 yrs) intensify price pressure. Switching costs (lines, training) take 3–9 months, but ~60% dual-source (2024), keeping vendor competition. ESG/LCA demands (CSRD 2024) and private-label pressure (~40% PL in EU 2023) heighten price and innovation demands.

| Metric | Value |

|---|---|

| Dual-sourcing (2024) | ~60% |

| EU private-label (2023) | ~40% |

| Tender length | 3–5 yrs |

| Line conversion | 3–9 months |

| Uptime | >99.5% |

What You See Is What You Get

Elopak Porter's Five Forces Analysis

This preview shows the exact Elopak Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, comprehensive and ready for download and use the moment you buy. No surprises, instant access.

Don't Miss the Bigger Picture

Elopak faces moderate supplier power, strong buyer pressure for sustainable and cost-efficient cartons, rising substitute threats, and intense rivalry among global packagers. Barriers to entry are moderate given capital requirements and regulation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elopak’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated paperboard sources

Elopak depends on a limited set of large cartonboard mills for high-spec food-grade material, creating supplier concentration that raises dependency and supplier pricing power. Stringent certifications such as FSC and PEFC plus barrier-grade specifications further limit the pool of qualified suppliers. Elopak’s long-term contracts and dual-sourcing reduce exposure but do not eliminate supply and price risk.

Specialized barrier materials

Polyethylene, biopolymers and aluminum/ALD coatings are central to aseptic integrity and shelf-life, with global polyethylene supply around 110 million tonnes in 2024. Few suppliers meet strict food-contact and sustainability standards, concentrating supplier power. Volatility in resin and LME aluminum markets transmits to packaging costs, and long qualification cycles (months to >1 year) limit rapid switching.

Proprietary machine components

Aseptic filling lines rely on precision parts, electronics and validated consumables whose approved vendors create high qualification barriers, giving suppliers leverage over pricing and delivery. Disruptions to these proprietary components directly threaten uptime targets—service SLAs commonly demand >98% availability—and can trigger penalty exposure. Framework agreements and multi-month inventory buffers mitigate but do not eliminate supplier concentration risk.

Logistics and energy sensitivity

Transport, energy, and pulp costs materially shape carton economics for Elopak; pulp can represent roughly 30-40% of carton raw-material cost and EU industrial electricity spikes (peaking near €200/MWh in 2023–24 episodes) and freight disruptions raised logistics premiums by an estimated 10–25% in 2024, tightening supplier leverage. Suppliers can prioritize larger, nearer customers during bottlenecks, but nearshoring and multimodal logistics reduced exposure and shortened lead times by ~15–20% in 2024.

- pulp share ~30–40% of raw-material cost

- EU industrial electricity spikes near €200/MWh (peak episodes)

- logistics premiums up ~10–25% in 2024; nearshoring cut lead times ~15–20%

Sustainability spec tightening

Sustainability spec tightening reduces supplier pool as demand for recyclable, low-carbon and plastic-reduced structures forces Elopak to source specialized cartonboard, barrier coatings and mono-material caps that meet recyclability standards and tethered-cap requirements under evolving EU/UK rules.

Suppliers of certified recycled or low-carbon inputs command pricing power and premiums, while co-development agreements for barrier tech or recycled-content formulations deepen dependence on a few qualified vendors.

- Supplier scarcity: fewer certified recyclable/low-carbon input providers

- Regulatory squeeze: tethered-cap and recyclability rules raise qualification barriers

- Price pressure: greener inputs often carry premiums

- Dependency: co-development increases vendor lock-in

30-40% pulp; 110Mt PE; logistics +10-25%

Supplier concentration for high-spec cartonboard and barrier materials gives vendors meaningful pricing power; pulp is ~30–40% of carton raw cost. Polyethylene global supply ~110Mt (2024) and resin/aluminum volatility plus logistics premiums +10–25% (2024) transmit cost risk. Sustainability specs shrink qualified suppliers and prolong qualification (months–>1 year).

| Factor | 2024 Metric | Impact |

|---|---|---|

| Pulp share | 30–40% of raw cost | High price sensitivity |

| PE supply | ~110 Mt | Concentrated suppliers |

| Logistics | +10–25% premiums | Higher procurement cost |

What is included in the product

Tailored exclusively for Elopak, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitutes and entry barriers, and identifies disruptive threats and strategic levers affecting pricing, profitability and market position.

A clear one-sheet Porter's Five Forces for Elopak that maps competitive pressures on a spider chart and is fully customizable to new data or scenarios for rapid strategic decisions, with a clean layout ready for pitch decks and seamless integration into broader dashboards.

Customers Bargaining Power

Highly concentrated buyers

Dairy and beverage multinationals and large retailers account for the bulk of Elopak's volumes, giving buyers strong leverage to press for lower prices and tougher terms. Their scale forces suppliers into fierce competition, especially as multi-year tenders commonly run 3–5 years and lock in preferred partners. Losing a single major account can materially dent plant utilization and margins. This concentrated buyer base thus amplifies price sensitivity and contract risk.

Installed base switching costs

Filling lines, staff training, and bespoke formats create strong installed-base switching costs that lock in customers and suppliers, often making conversion projects take 3–9 months. Customers can still leverage competing vendors offering compatible formats, keeping negotiating leverage. Total cost of ownership and service quality dominate the switching calculus, especially for high-volume dairy and beverage clients. Line conversion incentives and payback offers frequently tip decisions in practice.

Private label and cost focus

Retailer private-label focus—European grocery private-label penetration around 40% in 2023—pushes unit economics and speed-to-shelf, forcing demands for price breaks, lightweighting and promotional support.

Customers press packaging vendors to demonstrate total system savings (logistics, fill-speed, waste), not just per-package price, raising evidence requirements in contracts.

Ongoing margin compression risk for Elopak is acute as retailers extract cost concessions while expecting investment in lightweight R&D and shelf-ready innovations.

Sustainability and innovation demands

Buyers increasingly demand lower carbon footprints, higher recyclability and reduced plastic content; failure to meet 2024 ESG expectations — driven by CSRD roll-out for EU suppliers in 2024 — prompts retailer re-evaluation and contract risk. Co-development roadmaps and transparent LCA datasets are now table stakes, with major retailers requiring LCA evidence during sourcing.

- CSRD 2024: expanded ESG reporting for large EU suppliers

- Co-development roadmaps expected by major retailers

- Transparent LCA data mandatory in RFQs

- ESG shortfalls trigger supplier re-evaluation

Multi-sourcing strategies

Large customers often dual-source to manage risk and keep pricing competitive; in 2024 roughly 60% of major beverage and dairy buyers reported dual-sourcing packaging suppliers, reducing single-vendor exposure. Qualification of alternate formats lowers vendor dependence while annual scorecards (with penalties) drive continuous improvement; deep service relationships and >99.5% uptime can blunt buyer leverage.

- Dual-sourcing ~60% (2024)

- Alternate-format qualification reduces dependency

- Annual scorecards + penalties enforce performance

- Service depth >99.5% uptime reduces buyer power

Retailer leverage, tenders and ESG/private-label pressure squeeze dairy/beverage margins

Large dairy/beverage customers and retailers wield high leverage — losing one client can cut utilization and margins, while multi-year tenders (3–5 yrs) intensify price pressure. Switching costs (lines, training) take 3–9 months, but ~60% dual-source (2024), keeping vendor competition. ESG/LCA demands (CSRD 2024) and private-label pressure (~40% PL in EU 2023) heighten price and innovation demands.

| Metric | Value |

|---|---|

| Dual-sourcing (2024) | ~60% |

| EU private-label (2023) | ~40% |

| Tender length | 3–5 yrs |

| Line conversion | 3–9 months |

| Uptime | >99.5% |

What You See Is What You Get

Elopak Porter's Five Forces Analysis

This preview shows the exact Elopak Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, comprehensive and ready for download and use the moment you buy. No surprises, instant access.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Elopak faces moderate supplier power, strong buyer pressure for sustainable and cost-efficient cartons, rising substitute threats, and intense rivalry among global packagers. Barriers to entry are moderate given capital requirements and regulation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Elopak’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated paperboard sources

Elopak depends on a limited set of large cartonboard mills for high-spec food-grade material, creating supplier concentration that raises dependency and supplier pricing power. Stringent certifications such as FSC and PEFC plus barrier-grade specifications further limit the pool of qualified suppliers. Elopak’s long-term contracts and dual-sourcing reduce exposure but do not eliminate supply and price risk.

Specialized barrier materials

Polyethylene, biopolymers and aluminum/ALD coatings are central to aseptic integrity and shelf-life, with global polyethylene supply around 110 million tonnes in 2024. Few suppliers meet strict food-contact and sustainability standards, concentrating supplier power. Volatility in resin and LME aluminum markets transmits to packaging costs, and long qualification cycles (months to >1 year) limit rapid switching.

Proprietary machine components

Aseptic filling lines rely on precision parts, electronics and validated consumables whose approved vendors create high qualification barriers, giving suppliers leverage over pricing and delivery. Disruptions to these proprietary components directly threaten uptime targets—service SLAs commonly demand >98% availability—and can trigger penalty exposure. Framework agreements and multi-month inventory buffers mitigate but do not eliminate supplier concentration risk.

Logistics and energy sensitivity

Transport, energy, and pulp costs materially shape carton economics for Elopak; pulp can represent roughly 30-40% of carton raw-material cost and EU industrial electricity spikes (peaking near €200/MWh in 2023–24 episodes) and freight disruptions raised logistics premiums by an estimated 10–25% in 2024, tightening supplier leverage. Suppliers can prioritize larger, nearer customers during bottlenecks, but nearshoring and multimodal logistics reduced exposure and shortened lead times by ~15–20% in 2024.

- pulp share ~30–40% of raw-material cost

- EU industrial electricity spikes near €200/MWh (peak episodes)

- logistics premiums up ~10–25% in 2024; nearshoring cut lead times ~15–20%

Sustainability spec tightening

Sustainability spec tightening reduces supplier pool as demand for recyclable, low-carbon and plastic-reduced structures forces Elopak to source specialized cartonboard, barrier coatings and mono-material caps that meet recyclability standards and tethered-cap requirements under evolving EU/UK rules.

Suppliers of certified recycled or low-carbon inputs command pricing power and premiums, while co-development agreements for barrier tech or recycled-content formulations deepen dependence on a few qualified vendors.

- Supplier scarcity: fewer certified recyclable/low-carbon input providers

- Regulatory squeeze: tethered-cap and recyclability rules raise qualification barriers

- Price pressure: greener inputs often carry premiums

- Dependency: co-development increases vendor lock-in

30-40% pulp; 110Mt PE; logistics +10-25%

Supplier concentration for high-spec cartonboard and barrier materials gives vendors meaningful pricing power; pulp is ~30–40% of carton raw cost. Polyethylene global supply ~110Mt (2024) and resin/aluminum volatility plus logistics premiums +10–25% (2024) transmit cost risk. Sustainability specs shrink qualified suppliers and prolong qualification (months–>1 year).

| Factor | 2024 Metric | Impact |

|---|---|---|

| Pulp share | 30–40% of raw cost | High price sensitivity |

| PE supply | ~110 Mt | Concentrated suppliers |

| Logistics | +10–25% premiums | Higher procurement cost |

What is included in the product

Tailored exclusively for Elopak, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitutes and entry barriers, and identifies disruptive threats and strategic levers affecting pricing, profitability and market position.

A clear one-sheet Porter's Five Forces for Elopak that maps competitive pressures on a spider chart and is fully customizable to new data or scenarios for rapid strategic decisions, with a clean layout ready for pitch decks and seamless integration into broader dashboards.

Customers Bargaining Power

Highly concentrated buyers

Dairy and beverage multinationals and large retailers account for the bulk of Elopak's volumes, giving buyers strong leverage to press for lower prices and tougher terms. Their scale forces suppliers into fierce competition, especially as multi-year tenders commonly run 3–5 years and lock in preferred partners. Losing a single major account can materially dent plant utilization and margins. This concentrated buyer base thus amplifies price sensitivity and contract risk.

Installed base switching costs

Filling lines, staff training, and bespoke formats create strong installed-base switching costs that lock in customers and suppliers, often making conversion projects take 3–9 months. Customers can still leverage competing vendors offering compatible formats, keeping negotiating leverage. Total cost of ownership and service quality dominate the switching calculus, especially for high-volume dairy and beverage clients. Line conversion incentives and payback offers frequently tip decisions in practice.

Private label and cost focus

Retailer private-label focus—European grocery private-label penetration around 40% in 2023—pushes unit economics and speed-to-shelf, forcing demands for price breaks, lightweighting and promotional support.

Customers press packaging vendors to demonstrate total system savings (logistics, fill-speed, waste), not just per-package price, raising evidence requirements in contracts.

Ongoing margin compression risk for Elopak is acute as retailers extract cost concessions while expecting investment in lightweight R&D and shelf-ready innovations.

Sustainability and innovation demands

Buyers increasingly demand lower carbon footprints, higher recyclability and reduced plastic content; failure to meet 2024 ESG expectations — driven by CSRD roll-out for EU suppliers in 2024 — prompts retailer re-evaluation and contract risk. Co-development roadmaps and transparent LCA datasets are now table stakes, with major retailers requiring LCA evidence during sourcing.

- CSRD 2024: expanded ESG reporting for large EU suppliers

- Co-development roadmaps expected by major retailers

- Transparent LCA data mandatory in RFQs

- ESG shortfalls trigger supplier re-evaluation

Multi-sourcing strategies

Large customers often dual-source to manage risk and keep pricing competitive; in 2024 roughly 60% of major beverage and dairy buyers reported dual-sourcing packaging suppliers, reducing single-vendor exposure. Qualification of alternate formats lowers vendor dependence while annual scorecards (with penalties) drive continuous improvement; deep service relationships and >99.5% uptime can blunt buyer leverage.

- Dual-sourcing ~60% (2024)

- Alternate-format qualification reduces dependency

- Annual scorecards + penalties enforce performance

- Service depth >99.5% uptime reduces buyer power

Retailer leverage, tenders and ESG/private-label pressure squeeze dairy/beverage margins

Large dairy/beverage customers and retailers wield high leverage — losing one client can cut utilization and margins, while multi-year tenders (3–5 yrs) intensify price pressure. Switching costs (lines, training) take 3–9 months, but ~60% dual-source (2024), keeping vendor competition. ESG/LCA demands (CSRD 2024) and private-label pressure (~40% PL in EU 2023) heighten price and innovation demands.

| Metric | Value |

|---|---|

| Dual-sourcing (2024) | ~60% |

| EU private-label (2023) | ~40% |

| Tender length | 3–5 yrs |

| Line conversion | 3–9 months |

| Uptime | >99.5% |

What You See Is What You Get

Elopak Porter's Five Forces Analysis

This preview shows the exact Elopak Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, comprehensive and ready for download and use the moment you buy. No surprises, instant access.