Emami Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

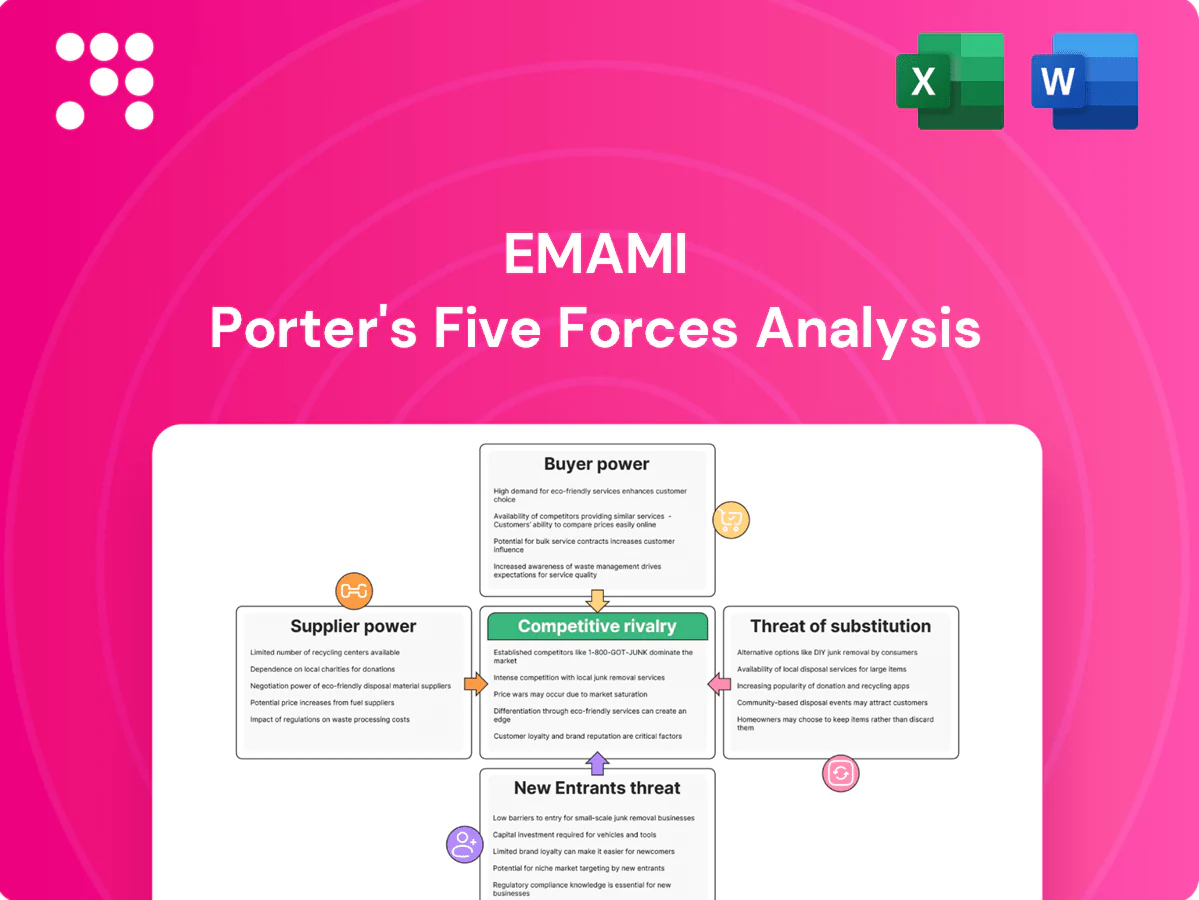

Emami’s Porter's Five Forces snapshot highlights moderate buyer power, intense rivalry in FMCG, manageable supplier influence, low threat of new entrants but rising substitute risks from niche naturals. The full report reveals force-by-force ratings, market data and strategic implications to pinpoint vulnerabilities and growth levers. Ready for a consultant-grade breakdown? Unlock the complete analysis for actionable insights.

Suppliers Bargaining Power

Diverse raw inputs and commodities

Emami sources herbal extracts, essential oils, menthol, petrochemicals and packaging, spreading supplier dependency across many inputs. Commodity volatility in items like palm and menthol can squeeze margins when exposures are unhedged. Global supply shocks or erratic monsoon patterns periodically tighten availability and raise procurement costs. Scale contracts and multi-sourcing mitigate but do not eliminate spike risk.

Specialized Ayurvedic and herbal inputs

Certain botanicals and standardized extracts have few qualified suppliers, and quality, traceability and AYUSH compliance raise switching costs. This concentration grants niche suppliers moderate bargaining power versus Emami. Long-term vertical partnerships and targeted backward integration can reduce dependence. Emami’s procurement emphasizes supplier audits, contract farming and certification to mitigate risks.

Packaging and contract manufacturing

Packaging suppliers in India remain numerous (India packaging market ~USD 38 billion in 2024), keeping supplier power low for Emami, though bespoke molds and sustainability specs cause temporary lock‑in. Contract manufacturers with niche formulations gain leverage during capacity constraints, as seen in 2023–24 feedstock tightness. Emami’s dual‑vendor sourcing reduces concentration risk.

Regulatory and quality compliance burden

High documentation standards and CDSCO oversight for cosmetics in 2024 shift leverage to suppliers with robust audit trails and certifications.

Any compliance lapse risks product approvals and Emami’s brand equity, tightening reliance on vetted suppliers and narrowing real substitution options.

Approved vendor lists, especially for sensitive inputs, institutionalize supplier power and raise switching costs for Emami.

- Regulatory oversight: CDSCO (2024)

- Audited suppliers hold leverage

- Noncompliance jeopardizes approvals

- Approved vendor lists increase switching costs

Cross-portfolio scale benefits

Emami’s cross-portfolio volumes strengthen supplier negotiations by enabling multi-year contracts and preferential pricing across personal care, healthcare and food segments, reducing per-unit input costs.

Aggregated demand and centralized procurement coupled with freight optimization compress supplier margins and improve inventory turns, though 2024 global commodity cycles—especially vegetable oil and packaging resin volatility—can temporarily negate scale benefits.

- Diversified volumes => better long-term terms

- Centralized procurement + freight optimization => lower supplier leverage

- Aggregated demand improves bargaining across inputs

- 2024 commodity cycle volatility can override scale

Moderate supplier power: packaging scale offsets niche botanicals and menthol risks

Emami faces moderate supplier power: diversified inputs and scale lower leverage, but niche botanicals, menthol and unhedged commodities can spike costs. Packaging market in India was ~USD 38 billion in 2024, keeping many suppliers competitive, while CDSCO compliance and approved vendor lists raise switching costs. Centralized procurement, multi‑sourcing and contract farming mitigate but do not eliminate supply shocks.

| Factor | Impact | 2024 indicator |

|---|---|---|

| Packaging market | Low supplier power | ~USD 38B |

| Botanicals/menthol | Moderate power | Few qualified suppliers |

| Regulation | Raises switching costs | CDSCO oversight 2024 |

What is included in the product

Concise Porter's Five Forces analysis for Emami uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting disruptive trends, pricing pressures, and entry barriers shaping its profitability and strategic positioning.

A concise, one-sheet Porter's Five Forces for Emami—instantly clarifies competitive pressures and strategic levers for faster decisions, with customizable pressure levels and a ready-to-copy layout for decks or reports.

Customers Bargaining Power

Fragmented end-consumers with price sensitivity

Retail consumers in India number about 1.428 billion, which fragments individual bargaining power for Emami despite strong aggregate demand.

Mass-market price sensitivity—driven by a largely rural base (~65%) and an FMCG market of roughly $110 billion—raises elasticity, making promotions and grammage pivotal.

Promotional offers, value packs and sachets drive trial and defend share; sachets remain critical for reach in lower-income segments and trade-up conversion.

Modern trade and e-commerce platforms

Large modern-trade chains and e-commerce platforms exert strong bargaining power over Emami, negotiating margins, visibility and access to consumer data; platform commissions typically range from 10–25% and global e-commerce reached 22.3% of retail sales in 2024 (Statista). Control of shelf space and search algorithms makes switching easy for shoppers, while compliance fees and liberal return policies compress margins. Brands must adopt joint business plans and co-marketing investments to secure prominence.

Distributor and wholesaler leverage

Route-to-market distributors and wholesalers shape Emami’s assortment and secondary placements, directly affecting in-store visibility and SKU mix. Credit terms and inventory expectations from channel partners tighten working capital cycles, forcing trade receivable and stocking pressures. In regions where Emami’s share is lower, distributor leverage and promotional demands increase, while incentive structures and selective exclusivity reduce churn risk.

Brand equity dampens buyer power

Emami’s strong franchises like Zandu Balm and BoroPlus create habitual demand and limit customer bargaining power by shifting competition from price to efficacy and trust.

Perceived Ayurvedic effectiveness and repeat purchase behavior give Emami pricing headroom, while loyalty programs and celebrity endorsements reinforce stickiness and reduce churn.

- Brand-led habitual demand

- Trust reduces pure price comparisons

- Repeat purchases enable premium pricing

- Loyalty programs and endorsements boost retention

Information transparency and reviews

2024 surveys show 73% of buyers consult online reviews and price-comparison tools, amplifying buyer knowledge and lowering search costs; quicker discovery of alternatives raises buyers' indirect negotiation power. Content-led education shifts decisions from price to benefits, while D2C channels let Emami capture first-party data to tailor offers and improve conversion and margins.

- 73% buyers consult online reviews (2024)

- Price-comparison tools speed alternative discovery

- D2C first-party data enables targeted offers

Fragmented 1.428B consumers, $110B FMCG, 22.3% online

Retail fragmentation (1.428B) limits individual leverage, but mass price sensitivity in a ~$110B FMCG market and 65% rural base raise elasticity; modern trade/e‑commerce (22.3% of retail 2024) and distributors increase buyer negotiating power; strong brands (Zandu, BoroPlus) and D2C data reduce churn and permit premiuming.

| Metric | Value | Impact |

|---|---|---|

| Consumers | 1.428B | Fragmented power |

| FMCG market | $110B | High price sensitivity |

| E‑commerce (2024) | 22.3% | Platform leverage |

| Online reviews | 73% | Higher buyer knowledge |

Preview Before You Purchase

Emami Porter's Five Forces Analysis

This Emami Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive—no placeholders or samples. It offers complete evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitutes. Purchase grants instant download of this same file, ready for use.

A Must-Have Tool for Decision-Makers

Emami’s Porter's Five Forces snapshot highlights moderate buyer power, intense rivalry in FMCG, manageable supplier influence, low threat of new entrants but rising substitute risks from niche naturals. The full report reveals force-by-force ratings, market data and strategic implications to pinpoint vulnerabilities and growth levers. Ready for a consultant-grade breakdown? Unlock the complete analysis for actionable insights.

Suppliers Bargaining Power

Diverse raw inputs and commodities

Emami sources herbal extracts, essential oils, menthol, petrochemicals and packaging, spreading supplier dependency across many inputs. Commodity volatility in items like palm and menthol can squeeze margins when exposures are unhedged. Global supply shocks or erratic monsoon patterns periodically tighten availability and raise procurement costs. Scale contracts and multi-sourcing mitigate but do not eliminate spike risk.

Specialized Ayurvedic and herbal inputs

Certain botanicals and standardized extracts have few qualified suppliers, and quality, traceability and AYUSH compliance raise switching costs. This concentration grants niche suppliers moderate bargaining power versus Emami. Long-term vertical partnerships and targeted backward integration can reduce dependence. Emami’s procurement emphasizes supplier audits, contract farming and certification to mitigate risks.

Packaging and contract manufacturing

Packaging suppliers in India remain numerous (India packaging market ~USD 38 billion in 2024), keeping supplier power low for Emami, though bespoke molds and sustainability specs cause temporary lock‑in. Contract manufacturers with niche formulations gain leverage during capacity constraints, as seen in 2023–24 feedstock tightness. Emami’s dual‑vendor sourcing reduces concentration risk.

Regulatory and quality compliance burden

High documentation standards and CDSCO oversight for cosmetics in 2024 shift leverage to suppliers with robust audit trails and certifications.

Any compliance lapse risks product approvals and Emami’s brand equity, tightening reliance on vetted suppliers and narrowing real substitution options.

Approved vendor lists, especially for sensitive inputs, institutionalize supplier power and raise switching costs for Emami.

- Regulatory oversight: CDSCO (2024)

- Audited suppliers hold leverage

- Noncompliance jeopardizes approvals

- Approved vendor lists increase switching costs

Cross-portfolio scale benefits

Emami’s cross-portfolio volumes strengthen supplier negotiations by enabling multi-year contracts and preferential pricing across personal care, healthcare and food segments, reducing per-unit input costs.

Aggregated demand and centralized procurement coupled with freight optimization compress supplier margins and improve inventory turns, though 2024 global commodity cycles—especially vegetable oil and packaging resin volatility—can temporarily negate scale benefits.

- Diversified volumes => better long-term terms

- Centralized procurement + freight optimization => lower supplier leverage

- Aggregated demand improves bargaining across inputs

- 2024 commodity cycle volatility can override scale

Moderate supplier power: packaging scale offsets niche botanicals and menthol risks

Emami faces moderate supplier power: diversified inputs and scale lower leverage, but niche botanicals, menthol and unhedged commodities can spike costs. Packaging market in India was ~USD 38 billion in 2024, keeping many suppliers competitive, while CDSCO compliance and approved vendor lists raise switching costs. Centralized procurement, multi‑sourcing and contract farming mitigate but do not eliminate supply shocks.

| Factor | Impact | 2024 indicator |

|---|---|---|

| Packaging market | Low supplier power | ~USD 38B |

| Botanicals/menthol | Moderate power | Few qualified suppliers |

| Regulation | Raises switching costs | CDSCO oversight 2024 |

What is included in the product

Concise Porter's Five Forces analysis for Emami uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting disruptive trends, pricing pressures, and entry barriers shaping its profitability and strategic positioning.

A concise, one-sheet Porter's Five Forces for Emami—instantly clarifies competitive pressures and strategic levers for faster decisions, with customizable pressure levels and a ready-to-copy layout for decks or reports.

Customers Bargaining Power

Fragmented end-consumers with price sensitivity

Retail consumers in India number about 1.428 billion, which fragments individual bargaining power for Emami despite strong aggregate demand.

Mass-market price sensitivity—driven by a largely rural base (~65%) and an FMCG market of roughly $110 billion—raises elasticity, making promotions and grammage pivotal.

Promotional offers, value packs and sachets drive trial and defend share; sachets remain critical for reach in lower-income segments and trade-up conversion.

Modern trade and e-commerce platforms

Large modern-trade chains and e-commerce platforms exert strong bargaining power over Emami, negotiating margins, visibility and access to consumer data; platform commissions typically range from 10–25% and global e-commerce reached 22.3% of retail sales in 2024 (Statista). Control of shelf space and search algorithms makes switching easy for shoppers, while compliance fees and liberal return policies compress margins. Brands must adopt joint business plans and co-marketing investments to secure prominence.

Distributor and wholesaler leverage

Route-to-market distributors and wholesalers shape Emami’s assortment and secondary placements, directly affecting in-store visibility and SKU mix. Credit terms and inventory expectations from channel partners tighten working capital cycles, forcing trade receivable and stocking pressures. In regions where Emami’s share is lower, distributor leverage and promotional demands increase, while incentive structures and selective exclusivity reduce churn risk.

Brand equity dampens buyer power

Emami’s strong franchises like Zandu Balm and BoroPlus create habitual demand and limit customer bargaining power by shifting competition from price to efficacy and trust.

Perceived Ayurvedic effectiveness and repeat purchase behavior give Emami pricing headroom, while loyalty programs and celebrity endorsements reinforce stickiness and reduce churn.

- Brand-led habitual demand

- Trust reduces pure price comparisons

- Repeat purchases enable premium pricing

- Loyalty programs and endorsements boost retention

Information transparency and reviews

2024 surveys show 73% of buyers consult online reviews and price-comparison tools, amplifying buyer knowledge and lowering search costs; quicker discovery of alternatives raises buyers' indirect negotiation power. Content-led education shifts decisions from price to benefits, while D2C channels let Emami capture first-party data to tailor offers and improve conversion and margins.

- 73% buyers consult online reviews (2024)

- Price-comparison tools speed alternative discovery

- D2C first-party data enables targeted offers

Fragmented 1.428B consumers, $110B FMCG, 22.3% online

Retail fragmentation (1.428B) limits individual leverage, but mass price sensitivity in a ~$110B FMCG market and 65% rural base raise elasticity; modern trade/e‑commerce (22.3% of retail 2024) and distributors increase buyer negotiating power; strong brands (Zandu, BoroPlus) and D2C data reduce churn and permit premiuming.

| Metric | Value | Impact |

|---|---|---|

| Consumers | 1.428B | Fragmented power |

| FMCG market | $110B | High price sensitivity |

| E‑commerce (2024) | 22.3% | Platform leverage |

| Online reviews | 73% | Higher buyer knowledge |

Preview Before You Purchase

Emami Porter's Five Forces Analysis

This Emami Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive—no placeholders or samples. It offers complete evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitutes. Purchase grants instant download of this same file, ready for use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Emami’s Porter's Five Forces snapshot highlights moderate buyer power, intense rivalry in FMCG, manageable supplier influence, low threat of new entrants but rising substitute risks from niche naturals. The full report reveals force-by-force ratings, market data and strategic implications to pinpoint vulnerabilities and growth levers. Ready for a consultant-grade breakdown? Unlock the complete analysis for actionable insights.

Suppliers Bargaining Power

Diverse raw inputs and commodities

Emami sources herbal extracts, essential oils, menthol, petrochemicals and packaging, spreading supplier dependency across many inputs. Commodity volatility in items like palm and menthol can squeeze margins when exposures are unhedged. Global supply shocks or erratic monsoon patterns periodically tighten availability and raise procurement costs. Scale contracts and multi-sourcing mitigate but do not eliminate spike risk.

Specialized Ayurvedic and herbal inputs

Certain botanicals and standardized extracts have few qualified suppliers, and quality, traceability and AYUSH compliance raise switching costs. This concentration grants niche suppliers moderate bargaining power versus Emami. Long-term vertical partnerships and targeted backward integration can reduce dependence. Emami’s procurement emphasizes supplier audits, contract farming and certification to mitigate risks.

Packaging and contract manufacturing

Packaging suppliers in India remain numerous (India packaging market ~USD 38 billion in 2024), keeping supplier power low for Emami, though bespoke molds and sustainability specs cause temporary lock‑in. Contract manufacturers with niche formulations gain leverage during capacity constraints, as seen in 2023–24 feedstock tightness. Emami’s dual‑vendor sourcing reduces concentration risk.

Regulatory and quality compliance burden

High documentation standards and CDSCO oversight for cosmetics in 2024 shift leverage to suppliers with robust audit trails and certifications.

Any compliance lapse risks product approvals and Emami’s brand equity, tightening reliance on vetted suppliers and narrowing real substitution options.

Approved vendor lists, especially for sensitive inputs, institutionalize supplier power and raise switching costs for Emami.

- Regulatory oversight: CDSCO (2024)

- Audited suppliers hold leverage

- Noncompliance jeopardizes approvals

- Approved vendor lists increase switching costs

Cross-portfolio scale benefits

Emami’s cross-portfolio volumes strengthen supplier negotiations by enabling multi-year contracts and preferential pricing across personal care, healthcare and food segments, reducing per-unit input costs.

Aggregated demand and centralized procurement coupled with freight optimization compress supplier margins and improve inventory turns, though 2024 global commodity cycles—especially vegetable oil and packaging resin volatility—can temporarily negate scale benefits.

- Diversified volumes => better long-term terms

- Centralized procurement + freight optimization => lower supplier leverage

- Aggregated demand improves bargaining across inputs

- 2024 commodity cycle volatility can override scale

Moderate supplier power: packaging scale offsets niche botanicals and menthol risks

Emami faces moderate supplier power: diversified inputs and scale lower leverage, but niche botanicals, menthol and unhedged commodities can spike costs. Packaging market in India was ~USD 38 billion in 2024, keeping many suppliers competitive, while CDSCO compliance and approved vendor lists raise switching costs. Centralized procurement, multi‑sourcing and contract farming mitigate but do not eliminate supply shocks.

| Factor | Impact | 2024 indicator |

|---|---|---|

| Packaging market | Low supplier power | ~USD 38B |

| Botanicals/menthol | Moderate power | Few qualified suppliers |

| Regulation | Raises switching costs | CDSCO oversight 2024 |

What is included in the product

Concise Porter's Five Forces analysis for Emami uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting disruptive trends, pricing pressures, and entry barriers shaping its profitability and strategic positioning.

A concise, one-sheet Porter's Five Forces for Emami—instantly clarifies competitive pressures and strategic levers for faster decisions, with customizable pressure levels and a ready-to-copy layout for decks or reports.

Customers Bargaining Power

Fragmented end-consumers with price sensitivity

Retail consumers in India number about 1.428 billion, which fragments individual bargaining power for Emami despite strong aggregate demand.

Mass-market price sensitivity—driven by a largely rural base (~65%) and an FMCG market of roughly $110 billion—raises elasticity, making promotions and grammage pivotal.

Promotional offers, value packs and sachets drive trial and defend share; sachets remain critical for reach in lower-income segments and trade-up conversion.

Modern trade and e-commerce platforms

Large modern-trade chains and e-commerce platforms exert strong bargaining power over Emami, negotiating margins, visibility and access to consumer data; platform commissions typically range from 10–25% and global e-commerce reached 22.3% of retail sales in 2024 (Statista). Control of shelf space and search algorithms makes switching easy for shoppers, while compliance fees and liberal return policies compress margins. Brands must adopt joint business plans and co-marketing investments to secure prominence.

Distributor and wholesaler leverage

Route-to-market distributors and wholesalers shape Emami’s assortment and secondary placements, directly affecting in-store visibility and SKU mix. Credit terms and inventory expectations from channel partners tighten working capital cycles, forcing trade receivable and stocking pressures. In regions where Emami’s share is lower, distributor leverage and promotional demands increase, while incentive structures and selective exclusivity reduce churn risk.

Brand equity dampens buyer power

Emami’s strong franchises like Zandu Balm and BoroPlus create habitual demand and limit customer bargaining power by shifting competition from price to efficacy and trust.

Perceived Ayurvedic effectiveness and repeat purchase behavior give Emami pricing headroom, while loyalty programs and celebrity endorsements reinforce stickiness and reduce churn.

- Brand-led habitual demand

- Trust reduces pure price comparisons

- Repeat purchases enable premium pricing

- Loyalty programs and endorsements boost retention

Information transparency and reviews

2024 surveys show 73% of buyers consult online reviews and price-comparison tools, amplifying buyer knowledge and lowering search costs; quicker discovery of alternatives raises buyers' indirect negotiation power. Content-led education shifts decisions from price to benefits, while D2C channels let Emami capture first-party data to tailor offers and improve conversion and margins.

- 73% buyers consult online reviews (2024)

- Price-comparison tools speed alternative discovery

- D2C first-party data enables targeted offers

Fragmented 1.428B consumers, $110B FMCG, 22.3% online

Retail fragmentation (1.428B) limits individual leverage, but mass price sensitivity in a ~$110B FMCG market and 65% rural base raise elasticity; modern trade/e‑commerce (22.3% of retail 2024) and distributors increase buyer negotiating power; strong brands (Zandu, BoroPlus) and D2C data reduce churn and permit premiuming.

| Metric | Value | Impact |

|---|---|---|

| Consumers | 1.428B | Fragmented power |

| FMCG market | $110B | High price sensitivity |

| E‑commerce (2024) | 22.3% | Platform leverage |

| Online reviews | 73% | Higher buyer knowledge |

Preview Before You Purchase

Emami Porter's Five Forces Analysis

This Emami Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive—no placeholders or samples. It offers complete evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitutes. Purchase grants instant download of this same file, ready for use.