E-mart SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

E-mart’s market leadership, robust omnichannel footprint, and private-label strength are tempered by intense competition, thin margins, and rapid digital disruption. Want the full strategic picture with actionable insights and financial context? Purchase the complete SWOT analysis—editable Word and Excel deliverables for planning, pitching, and investing.

Strengths

Market leadership

E-Mart, founded in 1993, is one of South Korea’s largest discount and hypermarket chains, anchoring strong brand recognition and consumer trust. Its national footprint of over 140 stores sustains top-of-mind awareness and draws high foot traffic. Market leadership attracts prime suppliers and favorable terms, while scale amplifies bargaining power and marketing efficiency.

Broad assortment

E-mart’s one-stop portfolio across groceries, household goods, apparel and electronics—backed by over 160 hypermarkets and roughly 5,000 Emart24 convenience stores—lifts average basket size and visit frequency. Cross-category promotions drive trade-up and impulse purchases, increasing per-trip spend. Offering multiple mission fulfilments in one visit reduces churn by improving convenience and loyalty.

Omnichannel reach

E-mart leverages its 160+ physical hypermarkets alongside robust online platforms and delivery networks to drive omnichannel reach. Click-and-collect and same-day delivery in major metros increase convenience and basket frequency. A unified inventory system improves stock availability across channels. Rich omnichannel data enables sharper personalization and dynamic pricing to lift conversion and margins.

Private labels

E-mart’s private labels raise gross margins versus national brands, reflecting industry uplifts of about 3–7 percentage points through lower procurement and marketing costs; they create clear price-value differentiation and increase customer stickiness by offering exclusive SKUs and tailored assortments. Sourcing control under owned brands enhances quality oversight and supply continuity, reducing stockouts and margin volatility.

- Margin uplift: 3–7pp

- Customer loyalty: exclusive ranges

- Supply control: quality & continuity

Supply chain scale

E-mart's centralized procurement and integrated logistics drive lower unit costs and higher margin resilience, while high throughput across its network ensures rapid distribution and frequent fresh replenishment. Close vendor collaboration boosts fill rates and shelf availability, and scale funds continuous investment in automation and expanded cold-chain capacity.

- Centralized procurement reduces unit cost

- High throughput enables fresh replenishment

- Vendor collaboration improves fill rates

- Scale funds automation and cold chain

Nationwide retailer: 140+ stores, ~5,000 conv. outlets, omnichannel, 3–7pp margin lift

E-mart, founded in 1993, is a market leader with nationwide reach (140+ large stores, 160+ hypermarkets, ~5,000 Emart24) driving high footfall and supplier leverage. Omnichannel integration and unified inventory boost convenience, same-day delivery and personalized pricing. Private labels lift gross margins ~3–7pp and improve loyalty and supply control.

| Metric | Value |

|---|---|

| Large stores | 140+ |

| Hypermarkets | 160+ |

| Convenience stores | ~5,000 |

| Private label margin uplift | 3–7pp |

What is included in the product

Delivers a strategic overview of E-mart’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects; highlights core capabilities, market opportunities, operational gaps, and risks to inform strategic decisions.

Provides a concise, visual SWOT matrix for E-mart to quickly identify strengths, weaknesses, opportunities and threats, speeding strategy alignment and simplifying stakeholder communication.

Weaknesses

Thin margins

Discount retail is structurally low-margin; global peers like Walmart report gross margins near 24%, leaving limited buffer for E-mart when local price wars shave several percentage points off gross profit.

Domestic concentration

Revenue is heavily tied to the South Korean market, leaving Emart exposed to domestic macroeconomic and demographic headwinds that can disproportionately dent sales and margins. Limited currency and geographic diversification constrain hedging options and growth levers outside Korea. If household consumption or population declines in Korea, Emart’s top-line growth and retail footprint could stall. Domestic retail dominance concentrates business risk.

Store saturation

Urban markets offer limited room for new large-format stores in South Korea, where urbanization reached 81.9% in 2023 (World Bank) and Seoul density is about 16,000 people/km2 (Seoul Statistics, 2023). Cannibalization risks rise as incremental openings create overlap with existing Emart locations, compressing same-store growth. Zoning and community constraints slow approval cycles and increase development costs. ROI on new boxes trends lower amid these constraints and shifting consumer spend toward online channels.

Complex operations

- Operational scope: multi-format (~150 hypermarkets, ~4,000 smaller outlets in 2024)

- Category complexity: fresh, GM, electronics need separate capabilities

- Inventory risk: cross-channel visibility lags

- Cost impact: higher SG&A and execution risk

Legacy systems

Legacy IT at E-mart, part of Shinsegae Group, limits real-time analytics and slows omnichannel agility; store-online integration remains imperfect, hampering stock visibility and unified customer journeys. Major upgrades need significant capex and change management, and slow data pipelines dilute personalization and targeted promotions.

- IT fragmentation

- High upgrade capex

- Poor omnichannel sync

- Weak personalization

Low margins, urban concentration and legacy IT threaten discount retailer growth

Discount retail is low-margin; global peer Walmart posts ~24% gross margin, leaving little buffer. Revenue concentrated in South Korea, with urbanization 81.9% (2023), raising domestic demand risk. Store expansion is constrained—~150 hypermarkets and ~4,000 smaller outlets (2024), increasing cannibalization. Legacy IT and weak omnichannel raise SG&A and capex needs.

| Metric | Value |

|---|---|

| Walmart gross margin | ~24% (2023) |

| South Korea urbanization | 81.9% (2023) |

| Emart formats | ~150 hypermarkets; ~4,000 smaller outlets (2024) |

| IT/omnichannel | Legacy systems; high upgrade capex |

Same Document Delivered

E-mart SWOT Analysis

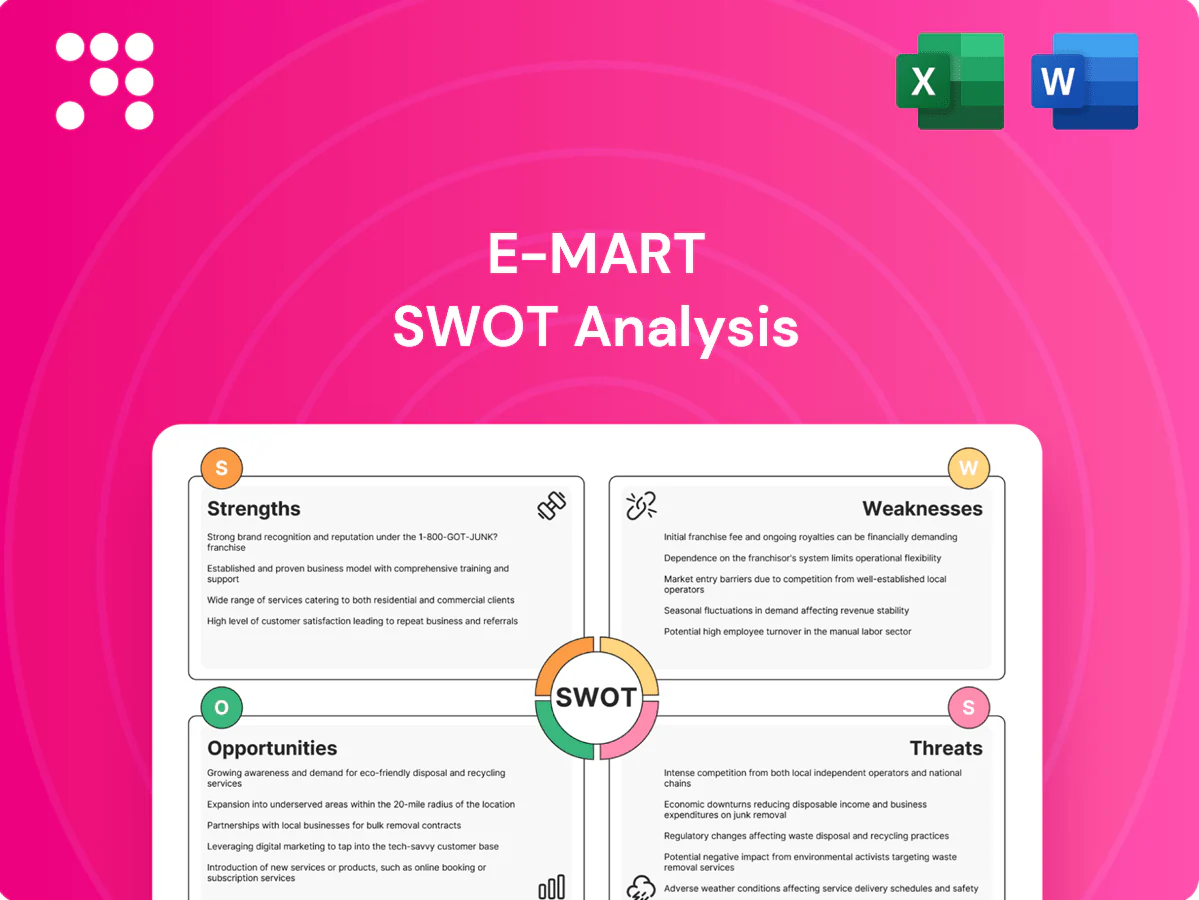

This is the actual E-mart SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities, and threats clearly outlined. Purchase unlocks the complete, editable version ready for use.

Elevate Your Analysis with the Complete SWOT Report

E-mart’s market leadership, robust omnichannel footprint, and private-label strength are tempered by intense competition, thin margins, and rapid digital disruption. Want the full strategic picture with actionable insights and financial context? Purchase the complete SWOT analysis—editable Word and Excel deliverables for planning, pitching, and investing.

Strengths

Market leadership

E-Mart, founded in 1993, is one of South Korea’s largest discount and hypermarket chains, anchoring strong brand recognition and consumer trust. Its national footprint of over 140 stores sustains top-of-mind awareness and draws high foot traffic. Market leadership attracts prime suppliers and favorable terms, while scale amplifies bargaining power and marketing efficiency.

Broad assortment

E-mart’s one-stop portfolio across groceries, household goods, apparel and electronics—backed by over 160 hypermarkets and roughly 5,000 Emart24 convenience stores—lifts average basket size and visit frequency. Cross-category promotions drive trade-up and impulse purchases, increasing per-trip spend. Offering multiple mission fulfilments in one visit reduces churn by improving convenience and loyalty.

Omnichannel reach

E-mart leverages its 160+ physical hypermarkets alongside robust online platforms and delivery networks to drive omnichannel reach. Click-and-collect and same-day delivery in major metros increase convenience and basket frequency. A unified inventory system improves stock availability across channels. Rich omnichannel data enables sharper personalization and dynamic pricing to lift conversion and margins.

Private labels

E-mart’s private labels raise gross margins versus national brands, reflecting industry uplifts of about 3–7 percentage points through lower procurement and marketing costs; they create clear price-value differentiation and increase customer stickiness by offering exclusive SKUs and tailored assortments. Sourcing control under owned brands enhances quality oversight and supply continuity, reducing stockouts and margin volatility.

- Margin uplift: 3–7pp

- Customer loyalty: exclusive ranges

- Supply control: quality & continuity

Supply chain scale

E-mart's centralized procurement and integrated logistics drive lower unit costs and higher margin resilience, while high throughput across its network ensures rapid distribution and frequent fresh replenishment. Close vendor collaboration boosts fill rates and shelf availability, and scale funds continuous investment in automation and expanded cold-chain capacity.

- Centralized procurement reduces unit cost

- High throughput enables fresh replenishment

- Vendor collaboration improves fill rates

- Scale funds automation and cold chain

Nationwide retailer: 140+ stores, ~5,000 conv. outlets, omnichannel, 3–7pp margin lift

E-mart, founded in 1993, is a market leader with nationwide reach (140+ large stores, 160+ hypermarkets, ~5,000 Emart24) driving high footfall and supplier leverage. Omnichannel integration and unified inventory boost convenience, same-day delivery and personalized pricing. Private labels lift gross margins ~3–7pp and improve loyalty and supply control.

| Metric | Value |

|---|---|

| Large stores | 140+ |

| Hypermarkets | 160+ |

| Convenience stores | ~5,000 |

| Private label margin uplift | 3–7pp |

What is included in the product

Delivers a strategic overview of E-mart’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects; highlights core capabilities, market opportunities, operational gaps, and risks to inform strategic decisions.

Provides a concise, visual SWOT matrix for E-mart to quickly identify strengths, weaknesses, opportunities and threats, speeding strategy alignment and simplifying stakeholder communication.

Weaknesses

Thin margins

Discount retail is structurally low-margin; global peers like Walmart report gross margins near 24%, leaving limited buffer for E-mart when local price wars shave several percentage points off gross profit.

Domestic concentration

Revenue is heavily tied to the South Korean market, leaving Emart exposed to domestic macroeconomic and demographic headwinds that can disproportionately dent sales and margins. Limited currency and geographic diversification constrain hedging options and growth levers outside Korea. If household consumption or population declines in Korea, Emart’s top-line growth and retail footprint could stall. Domestic retail dominance concentrates business risk.

Store saturation

Urban markets offer limited room for new large-format stores in South Korea, where urbanization reached 81.9% in 2023 (World Bank) and Seoul density is about 16,000 people/km2 (Seoul Statistics, 2023). Cannibalization risks rise as incremental openings create overlap with existing Emart locations, compressing same-store growth. Zoning and community constraints slow approval cycles and increase development costs. ROI on new boxes trends lower amid these constraints and shifting consumer spend toward online channels.

Complex operations

- Operational scope: multi-format (~150 hypermarkets, ~4,000 smaller outlets in 2024)

- Category complexity: fresh, GM, electronics need separate capabilities

- Inventory risk: cross-channel visibility lags

- Cost impact: higher SG&A and execution risk

Legacy systems

Legacy IT at E-mart, part of Shinsegae Group, limits real-time analytics and slows omnichannel agility; store-online integration remains imperfect, hampering stock visibility and unified customer journeys. Major upgrades need significant capex and change management, and slow data pipelines dilute personalization and targeted promotions.

- IT fragmentation

- High upgrade capex

- Poor omnichannel sync

- Weak personalization

Low margins, urban concentration and legacy IT threaten discount retailer growth

Discount retail is low-margin; global peer Walmart posts ~24% gross margin, leaving little buffer. Revenue concentrated in South Korea, with urbanization 81.9% (2023), raising domestic demand risk. Store expansion is constrained—~150 hypermarkets and ~4,000 smaller outlets (2024), increasing cannibalization. Legacy IT and weak omnichannel raise SG&A and capex needs.

| Metric | Value |

|---|---|

| Walmart gross margin | ~24% (2023) |

| South Korea urbanization | 81.9% (2023) |

| Emart formats | ~150 hypermarkets; ~4,000 smaller outlets (2024) |

| IT/omnichannel | Legacy systems; high upgrade capex |

Same Document Delivered

E-mart SWOT Analysis

This is the actual E-mart SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities, and threats clearly outlined. Purchase unlocks the complete, editable version ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

E-mart’s market leadership, robust omnichannel footprint, and private-label strength are tempered by intense competition, thin margins, and rapid digital disruption. Want the full strategic picture with actionable insights and financial context? Purchase the complete SWOT analysis—editable Word and Excel deliverables for planning, pitching, and investing.

Strengths

Market leadership

E-Mart, founded in 1993, is one of South Korea’s largest discount and hypermarket chains, anchoring strong brand recognition and consumer trust. Its national footprint of over 140 stores sustains top-of-mind awareness and draws high foot traffic. Market leadership attracts prime suppliers and favorable terms, while scale amplifies bargaining power and marketing efficiency.

Broad assortment

E-mart’s one-stop portfolio across groceries, household goods, apparel and electronics—backed by over 160 hypermarkets and roughly 5,000 Emart24 convenience stores—lifts average basket size and visit frequency. Cross-category promotions drive trade-up and impulse purchases, increasing per-trip spend. Offering multiple mission fulfilments in one visit reduces churn by improving convenience and loyalty.

Omnichannel reach

E-mart leverages its 160+ physical hypermarkets alongside robust online platforms and delivery networks to drive omnichannel reach. Click-and-collect and same-day delivery in major metros increase convenience and basket frequency. A unified inventory system improves stock availability across channels. Rich omnichannel data enables sharper personalization and dynamic pricing to lift conversion and margins.

Private labels

E-mart’s private labels raise gross margins versus national brands, reflecting industry uplifts of about 3–7 percentage points through lower procurement and marketing costs; they create clear price-value differentiation and increase customer stickiness by offering exclusive SKUs and tailored assortments. Sourcing control under owned brands enhances quality oversight and supply continuity, reducing stockouts and margin volatility.

- Margin uplift: 3–7pp

- Customer loyalty: exclusive ranges

- Supply control: quality & continuity

Supply chain scale

E-mart's centralized procurement and integrated logistics drive lower unit costs and higher margin resilience, while high throughput across its network ensures rapid distribution and frequent fresh replenishment. Close vendor collaboration boosts fill rates and shelf availability, and scale funds continuous investment in automation and expanded cold-chain capacity.

- Centralized procurement reduces unit cost

- High throughput enables fresh replenishment

- Vendor collaboration improves fill rates

- Scale funds automation and cold chain

Nationwide retailer: 140+ stores, ~5,000 conv. outlets, omnichannel, 3–7pp margin lift

E-mart, founded in 1993, is a market leader with nationwide reach (140+ large stores, 160+ hypermarkets, ~5,000 Emart24) driving high footfall and supplier leverage. Omnichannel integration and unified inventory boost convenience, same-day delivery and personalized pricing. Private labels lift gross margins ~3–7pp and improve loyalty and supply control.

| Metric | Value |

|---|---|

| Large stores | 140+ |

| Hypermarkets | 160+ |

| Convenience stores | ~5,000 |

| Private label margin uplift | 3–7pp |

What is included in the product

Delivers a strategic overview of E-mart’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects; highlights core capabilities, market opportunities, operational gaps, and risks to inform strategic decisions.

Provides a concise, visual SWOT matrix for E-mart to quickly identify strengths, weaknesses, opportunities and threats, speeding strategy alignment and simplifying stakeholder communication.

Weaknesses

Thin margins

Discount retail is structurally low-margin; global peers like Walmart report gross margins near 24%, leaving limited buffer for E-mart when local price wars shave several percentage points off gross profit.

Domestic concentration

Revenue is heavily tied to the South Korean market, leaving Emart exposed to domestic macroeconomic and demographic headwinds that can disproportionately dent sales and margins. Limited currency and geographic diversification constrain hedging options and growth levers outside Korea. If household consumption or population declines in Korea, Emart’s top-line growth and retail footprint could stall. Domestic retail dominance concentrates business risk.

Store saturation

Urban markets offer limited room for new large-format stores in South Korea, where urbanization reached 81.9% in 2023 (World Bank) and Seoul density is about 16,000 people/km2 (Seoul Statistics, 2023). Cannibalization risks rise as incremental openings create overlap with existing Emart locations, compressing same-store growth. Zoning and community constraints slow approval cycles and increase development costs. ROI on new boxes trends lower amid these constraints and shifting consumer spend toward online channels.

Complex operations

- Operational scope: multi-format (~150 hypermarkets, ~4,000 smaller outlets in 2024)

- Category complexity: fresh, GM, electronics need separate capabilities

- Inventory risk: cross-channel visibility lags

- Cost impact: higher SG&A and execution risk

Legacy systems

Legacy IT at E-mart, part of Shinsegae Group, limits real-time analytics and slows omnichannel agility; store-online integration remains imperfect, hampering stock visibility and unified customer journeys. Major upgrades need significant capex and change management, and slow data pipelines dilute personalization and targeted promotions.

- IT fragmentation

- High upgrade capex

- Poor omnichannel sync

- Weak personalization

Low margins, urban concentration and legacy IT threaten discount retailer growth

Discount retail is low-margin; global peer Walmart posts ~24% gross margin, leaving little buffer. Revenue concentrated in South Korea, with urbanization 81.9% (2023), raising domestic demand risk. Store expansion is constrained—~150 hypermarkets and ~4,000 smaller outlets (2024), increasing cannibalization. Legacy IT and weak omnichannel raise SG&A and capex needs.

| Metric | Value |

|---|---|

| Walmart gross margin | ~24% (2023) |

| South Korea urbanization | 81.9% (2023) |

| Emart formats | ~150 hypermarkets; ~4,000 smaller outlets (2024) |

| IT/omnichannel | Legacy systems; high upgrade capex |

Same Document Delivered

E-mart SWOT Analysis

This is the actual E-mart SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities, and threats clearly outlined. Purchase unlocks the complete, editable version ready for use.