EMCOR Group Boston Consulting Group Matrix

Actionable Strategy Starts Here

Quick snapshot: EMCOR’s BCG Matrix preview shows where key business lines sit — some are fueling growth, others just treading water. Want the full picture with quadrant-by-quadrant data, tactical recommendations, and an editable Word + Excel pack? Purchase the complete BCG Matrix for a practical roadmap to reallocate capital, prune underperformers, and double down on true stars. Get instant access and skip the guesswork.

Stars

Data center MEP

Data center MEP sits in EMCORs BCG matrix as a star: explosive cloud and AI demand is driving complex, high-ticket projects that EMCOR executes well. The company reported 2024 revenue of $12.5 billion and shows strong repeat wins in mission-critical builds. Growth is hot and margins in data center MEP justify continued investment. Keep feeding capacity and specialized talent to lock in share.

Healthcare & life sciences

Hospital upgrades, labs, and cleanrooms demand precision mechanical and electrical work that EMCOR has delivered in high-complexity projects, supporting 24/7 uptime and regulatory compliance across healthcare facilities.

Regulatory complexity and mission-critical continuity favor experienced leaders; in 2024 EMCOR’s healthcare pipeline remained robust driven by facility modernization and biopharma expansion.

Maintaining share now captures modernization projects that tend to convert into steady annuity-style MRO and facilities contracts as installations mature.

Energy efficiency retrofits

ESCO-style upgrades, electrification and decarbonization mandates are accelerating as buildings and construction account for about 37% of global energy‑related CO2 emissions (IEA); EMCOR, with revenue over $12 billion, can design‑build and operate savings‑backed projects, a distinct edge. Cash in equals cash out now because demand growth is rapid and paybacks compress. Continue investing in robust measurement & verification and in financing partnerships to scale.

Mission-critical facilities services

Operate-and-maintain for high-stakes sites (data centers, pharma, defense) is booming; EMCOR reported 2024 revenue of about $12.2 billion and a service backlog near $6.3 billion, giving its performance history and national coverage a competitive lead. Growth demands added headcount, advanced tooling and tech enablement to keep SLAs tight; done right, pilots become durable contracts.

- Market: rapid demand for mission-critical O&M

- Edge: EMCOR scale + 2024 backlog advantage

- Needs: hiring, tooling, SaaS/IoT enablement

- Outcome: higher retention, long-term contracts

EV charging infrastructure

Fleet and depot electrification is accelerating in logistics and municipalities; federal NEVI funding of about 5 billion USD underpins public charging and grid upgrades, and EMCOR’s electrical depth and utility coordination are distinct competitive advantages. Market growth is strong but rollout is capital- and labor-intensive, so prioritize multi-site fleet programs and trusted network partners to scale efficiently.

- Position: Question mark — high growth, mixed share

- Advantage: electrical scope + utility coordination

- Risk: capital and skilled-labor constraints

- Recommendation: selective multi-site + network partnerships

AI, biopharma, decarb lift data center, healthcare & ESCO O&M; rev $12.5B

Data center MEP, healthcare modernization and ESCO O&M are Stars: cloud/AI, biopharma expansion and decarbonization drive high-growth, high-margin projects. EMCOR reported 2024 revenue $12.5 billion with service backlog ~$6.3 billion; NEVI ~$5B accelerates fleet electrification. Prioritize capacity, specialized talent, M&V and financing to lock share.

| Segment | 2024 Rev | Backlog | Drivers | Priority |

|---|---|---|---|---|

| Data center/Healthcare/ESCO | $12.5B corporate | $6.3B service | AI, biopharma, decarb | Hire, M&V, finance |

What is included in the product

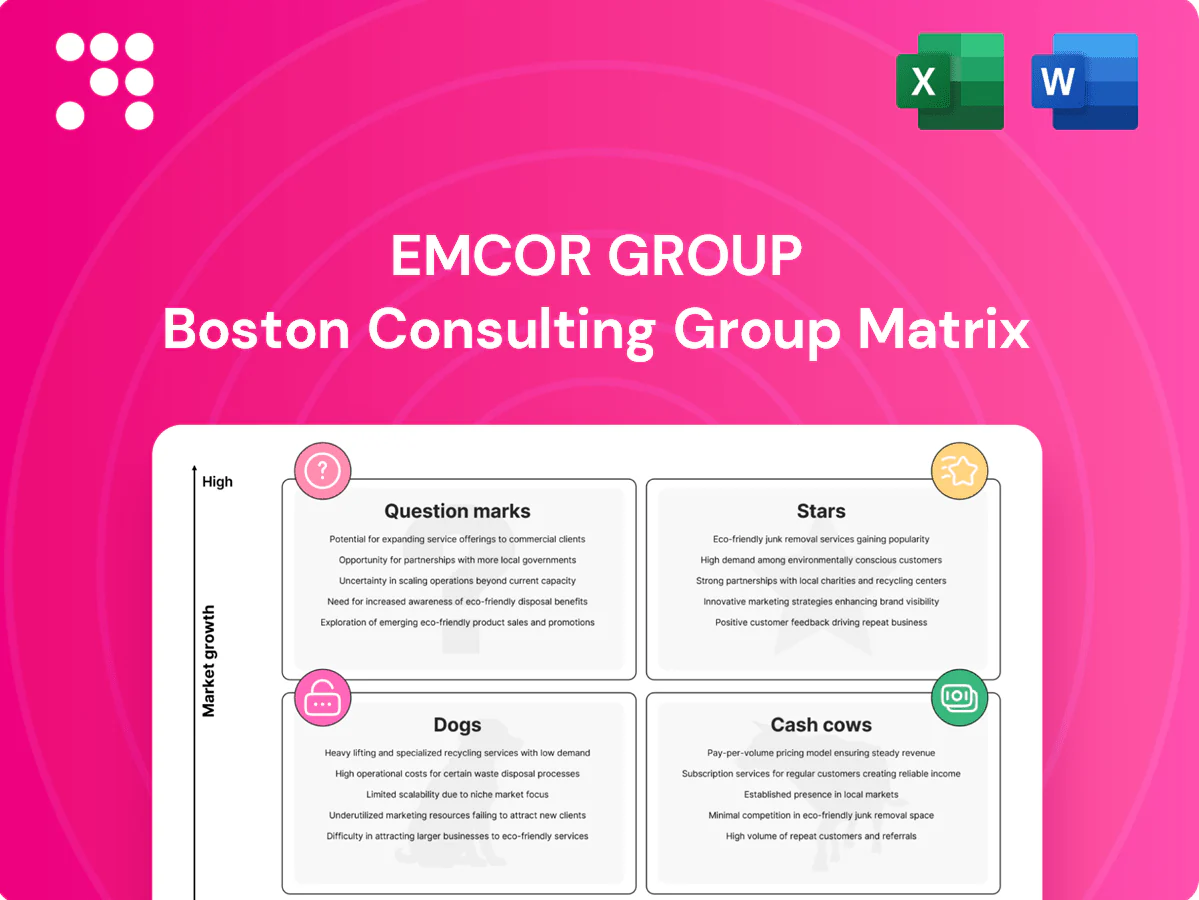

BCG Matrix for EMCOR Group: maps Stars, Cash Cows, Question Marks and Dogs, with targeted invest, hold or divest recommendations.

One-page EMCOR BCG Matrix relieves portfolio confusion by placing each business unit in a clear quadrant

Cash Cows

Facility maintenance contracts

Long-running O&M facility maintenance contracts underpin EMCORs cash-cow segment, representing stable, high-share recurring revenue (EMCOR reported approximately $12.8 billion in 2024 total revenue, with a large portion from service contracts). Cash is predictable and levered by scale; margins are low-growth but improve via dispatch efficiency and parts-management, lifting operating margins and free cash flow. Strategy: milk while optimizing route density and tech utilization to further compress costs.

Commercial HVAC service

Commercial HVAC service—chiller/boiler maintenance, PMs, and replacements—is a mature, recurring cash cow for EMCOR, supported by a large installed base and brand that kept services stable in 2024 with reported revenue around $12.6 billion. Limited promotion is needed as reliability and contract renewals drive volume and service margins. Focus on optimizing van stock, boosting technician productivity, and cross-selling to lift cash yield.

Electrical service & upgrades

Electrical service & upgrades — tenant fit-outs, panel upgrades, lighting, code compliance — generate steady, annuity-like cash for EMCOR, supported by the companys scale (EMCOR reported $12.9B revenue in 2023) and high metro share. Growth is modest and competitive; industry shows mid-single-digit expansion in 2024. Standardize pricing, prefab small assemblies, and tighten response times to protect margins and utilization.

Utility & industrial shutdowns

Utility and industrial shutdowns are cash cows for EMCOR: outage work repeats on known cycles with established clients, and disciplined planning plus a strong safety record protect margins. Growth is flat but execution excellence—rigorous scheduling and crew productivity—keeps cash generation steady. Investing in tooling and scheduling technology can squeeze more revenue from each outage window.

- repeat contracts

- planning discipline

- safety protects margins

- flat growth, high cash yield

- invest in tooling & scheduling tech

Controls retro-commissioning

Controls retro-commissioning optimizes BAS sequences to deliver dependable demand in mature buildings; DOE/NREL data shows median energy savings ~15% with typical payback ~2 years (2024). EMCOR’s technical depth converts projects into sticky follow-on services, keeping margins healthy despite slow market growth.

- Dependable demand: mature building base

- 15% median energy savings (DOE/NREL, 2024)

- Sticky follow-on work: high retention

- Maintain templates, analytics to stay cash-rich

Long-term O&M contracts: steady cash, boost margins with controls, tech, and route density

Long-running O&M contracts form EMCOR cash cows, delivering predictable recurring revenue within total 2024 revenue ~$12.8B. HVAC, electrical, and shutdown work provide high cash yield with low-to-moderate growth; controls retro-commissioning adds value (DOE/NREL median 15% energy savings, 2024). Strategy: milk cash while raising margins via route density, tech, scheduling, and cross-sell.

| Segment | Role | 2024 fact | Margin/Growth |

|---|---|---|---|

| O&M | Core cash cow | Included in $12.8B | Stable/low-growth |

| Controls | High retention | 15% median savings | Healthy margins |

What You See Is What You Get

EMCOR Group BCG Matrix

The file you’re previewing here is the exact BCG Matrix report you’ll receive after purchase—no watermarks, no demo text, just the finished, fully formatted document. It’s crafted by strategy pros for clarity and immediate use in planning, pitch decks, or client presentations. After buying, the same file is yours to download, edit, print, or share—no surprises, no extra revisions needed. Quick, professional, and ready to plug into your workflow.

Actionable Strategy Starts Here

Quick snapshot: EMCOR’s BCG Matrix preview shows where key business lines sit — some are fueling growth, others just treading water. Want the full picture with quadrant-by-quadrant data, tactical recommendations, and an editable Word + Excel pack? Purchase the complete BCG Matrix for a practical roadmap to reallocate capital, prune underperformers, and double down on true stars. Get instant access and skip the guesswork.

Stars

Data center MEP

Data center MEP sits in EMCORs BCG matrix as a star: explosive cloud and AI demand is driving complex, high-ticket projects that EMCOR executes well. The company reported 2024 revenue of $12.5 billion and shows strong repeat wins in mission-critical builds. Growth is hot and margins in data center MEP justify continued investment. Keep feeding capacity and specialized talent to lock in share.

Healthcare & life sciences

Hospital upgrades, labs, and cleanrooms demand precision mechanical and electrical work that EMCOR has delivered in high-complexity projects, supporting 24/7 uptime and regulatory compliance across healthcare facilities.

Regulatory complexity and mission-critical continuity favor experienced leaders; in 2024 EMCOR’s healthcare pipeline remained robust driven by facility modernization and biopharma expansion.

Maintaining share now captures modernization projects that tend to convert into steady annuity-style MRO and facilities contracts as installations mature.

Energy efficiency retrofits

ESCO-style upgrades, electrification and decarbonization mandates are accelerating as buildings and construction account for about 37% of global energy‑related CO2 emissions (IEA); EMCOR, with revenue over $12 billion, can design‑build and operate savings‑backed projects, a distinct edge. Cash in equals cash out now because demand growth is rapid and paybacks compress. Continue investing in robust measurement & verification and in financing partnerships to scale.

Mission-critical facilities services

Operate-and-maintain for high-stakes sites (data centers, pharma, defense) is booming; EMCOR reported 2024 revenue of about $12.2 billion and a service backlog near $6.3 billion, giving its performance history and national coverage a competitive lead. Growth demands added headcount, advanced tooling and tech enablement to keep SLAs tight; done right, pilots become durable contracts.

- Market: rapid demand for mission-critical O&M

- Edge: EMCOR scale + 2024 backlog advantage

- Needs: hiring, tooling, SaaS/IoT enablement

- Outcome: higher retention, long-term contracts

EV charging infrastructure

Fleet and depot electrification is accelerating in logistics and municipalities; federal NEVI funding of about 5 billion USD underpins public charging and grid upgrades, and EMCOR’s electrical depth and utility coordination are distinct competitive advantages. Market growth is strong but rollout is capital- and labor-intensive, so prioritize multi-site fleet programs and trusted network partners to scale efficiently.

- Position: Question mark — high growth, mixed share

- Advantage: electrical scope + utility coordination

- Risk: capital and skilled-labor constraints

- Recommendation: selective multi-site + network partnerships

AI, biopharma, decarb lift data center, healthcare & ESCO O&M; rev $12.5B

Data center MEP, healthcare modernization and ESCO O&M are Stars: cloud/AI, biopharma expansion and decarbonization drive high-growth, high-margin projects. EMCOR reported 2024 revenue $12.5 billion with service backlog ~$6.3 billion; NEVI ~$5B accelerates fleet electrification. Prioritize capacity, specialized talent, M&V and financing to lock share.

| Segment | 2024 Rev | Backlog | Drivers | Priority |

|---|---|---|---|---|

| Data center/Healthcare/ESCO | $12.5B corporate | $6.3B service | AI, biopharma, decarb | Hire, M&V, finance |

What is included in the product

BCG Matrix for EMCOR Group: maps Stars, Cash Cows, Question Marks and Dogs, with targeted invest, hold or divest recommendations.

One-page EMCOR BCG Matrix relieves portfolio confusion by placing each business unit in a clear quadrant

Cash Cows

Facility maintenance contracts

Long-running O&M facility maintenance contracts underpin EMCORs cash-cow segment, representing stable, high-share recurring revenue (EMCOR reported approximately $12.8 billion in 2024 total revenue, with a large portion from service contracts). Cash is predictable and levered by scale; margins are low-growth but improve via dispatch efficiency and parts-management, lifting operating margins and free cash flow. Strategy: milk while optimizing route density and tech utilization to further compress costs.

Commercial HVAC service

Commercial HVAC service—chiller/boiler maintenance, PMs, and replacements—is a mature, recurring cash cow for EMCOR, supported by a large installed base and brand that kept services stable in 2024 with reported revenue around $12.6 billion. Limited promotion is needed as reliability and contract renewals drive volume and service margins. Focus on optimizing van stock, boosting technician productivity, and cross-selling to lift cash yield.

Electrical service & upgrades

Electrical service & upgrades — tenant fit-outs, panel upgrades, lighting, code compliance — generate steady, annuity-like cash for EMCOR, supported by the companys scale (EMCOR reported $12.9B revenue in 2023) and high metro share. Growth is modest and competitive; industry shows mid-single-digit expansion in 2024. Standardize pricing, prefab small assemblies, and tighten response times to protect margins and utilization.

Utility & industrial shutdowns

Utility and industrial shutdowns are cash cows for EMCOR: outage work repeats on known cycles with established clients, and disciplined planning plus a strong safety record protect margins. Growth is flat but execution excellence—rigorous scheduling and crew productivity—keeps cash generation steady. Investing in tooling and scheduling technology can squeeze more revenue from each outage window.

- repeat contracts

- planning discipline

- safety protects margins

- flat growth, high cash yield

- invest in tooling & scheduling tech

Controls retro-commissioning

Controls retro-commissioning optimizes BAS sequences to deliver dependable demand in mature buildings; DOE/NREL data shows median energy savings ~15% with typical payback ~2 years (2024). EMCOR’s technical depth converts projects into sticky follow-on services, keeping margins healthy despite slow market growth.

- Dependable demand: mature building base

- 15% median energy savings (DOE/NREL, 2024)

- Sticky follow-on work: high retention

- Maintain templates, analytics to stay cash-rich

Long-term O&M contracts: steady cash, boost margins with controls, tech, and route density

Long-running O&M contracts form EMCOR cash cows, delivering predictable recurring revenue within total 2024 revenue ~$12.8B. HVAC, electrical, and shutdown work provide high cash yield with low-to-moderate growth; controls retro-commissioning adds value (DOE/NREL median 15% energy savings, 2024). Strategy: milk cash while raising margins via route density, tech, scheduling, and cross-sell.

| Segment | Role | 2024 fact | Margin/Growth |

|---|---|---|---|

| O&M | Core cash cow | Included in $12.8B | Stable/low-growth |

| Controls | High retention | 15% median savings | Healthy margins |

What You See Is What You Get

EMCOR Group BCG Matrix

The file you’re previewing here is the exact BCG Matrix report you’ll receive after purchase—no watermarks, no demo text, just the finished, fully formatted document. It’s crafted by strategy pros for clarity and immediate use in planning, pitch decks, or client presentations. After buying, the same file is yours to download, edit, print, or share—no surprises, no extra revisions needed. Quick, professional, and ready to plug into your workflow.

Description

Actionable Strategy Starts Here

Quick snapshot: EMCOR’s BCG Matrix preview shows where key business lines sit — some are fueling growth, others just treading water. Want the full picture with quadrant-by-quadrant data, tactical recommendations, and an editable Word + Excel pack? Purchase the complete BCG Matrix for a practical roadmap to reallocate capital, prune underperformers, and double down on true stars. Get instant access and skip the guesswork.

Stars

Data center MEP

Data center MEP sits in EMCORs BCG matrix as a star: explosive cloud and AI demand is driving complex, high-ticket projects that EMCOR executes well. The company reported 2024 revenue of $12.5 billion and shows strong repeat wins in mission-critical builds. Growth is hot and margins in data center MEP justify continued investment. Keep feeding capacity and specialized talent to lock in share.

Healthcare & life sciences

Hospital upgrades, labs, and cleanrooms demand precision mechanical and electrical work that EMCOR has delivered in high-complexity projects, supporting 24/7 uptime and regulatory compliance across healthcare facilities.

Regulatory complexity and mission-critical continuity favor experienced leaders; in 2024 EMCOR’s healthcare pipeline remained robust driven by facility modernization and biopharma expansion.

Maintaining share now captures modernization projects that tend to convert into steady annuity-style MRO and facilities contracts as installations mature.

Energy efficiency retrofits

ESCO-style upgrades, electrification and decarbonization mandates are accelerating as buildings and construction account for about 37% of global energy‑related CO2 emissions (IEA); EMCOR, with revenue over $12 billion, can design‑build and operate savings‑backed projects, a distinct edge. Cash in equals cash out now because demand growth is rapid and paybacks compress. Continue investing in robust measurement & verification and in financing partnerships to scale.

Mission-critical facilities services

Operate-and-maintain for high-stakes sites (data centers, pharma, defense) is booming; EMCOR reported 2024 revenue of about $12.2 billion and a service backlog near $6.3 billion, giving its performance history and national coverage a competitive lead. Growth demands added headcount, advanced tooling and tech enablement to keep SLAs tight; done right, pilots become durable contracts.

- Market: rapid demand for mission-critical O&M

- Edge: EMCOR scale + 2024 backlog advantage

- Needs: hiring, tooling, SaaS/IoT enablement

- Outcome: higher retention, long-term contracts

EV charging infrastructure

Fleet and depot electrification is accelerating in logistics and municipalities; federal NEVI funding of about 5 billion USD underpins public charging and grid upgrades, and EMCOR’s electrical depth and utility coordination are distinct competitive advantages. Market growth is strong but rollout is capital- and labor-intensive, so prioritize multi-site fleet programs and trusted network partners to scale efficiently.

- Position: Question mark — high growth, mixed share

- Advantage: electrical scope + utility coordination

- Risk: capital and skilled-labor constraints

- Recommendation: selective multi-site + network partnerships

AI, biopharma, decarb lift data center, healthcare & ESCO O&M; rev $12.5B

Data center MEP, healthcare modernization and ESCO O&M are Stars: cloud/AI, biopharma expansion and decarbonization drive high-growth, high-margin projects. EMCOR reported 2024 revenue $12.5 billion with service backlog ~$6.3 billion; NEVI ~$5B accelerates fleet electrification. Prioritize capacity, specialized talent, M&V and financing to lock share.

| Segment | 2024 Rev | Backlog | Drivers | Priority |

|---|---|---|---|---|

| Data center/Healthcare/ESCO | $12.5B corporate | $6.3B service | AI, biopharma, decarb | Hire, M&V, finance |

What is included in the product

BCG Matrix for EMCOR Group: maps Stars, Cash Cows, Question Marks and Dogs, with targeted invest, hold or divest recommendations.

One-page EMCOR BCG Matrix relieves portfolio confusion by placing each business unit in a clear quadrant

Cash Cows

Facility maintenance contracts

Long-running O&M facility maintenance contracts underpin EMCORs cash-cow segment, representing stable, high-share recurring revenue (EMCOR reported approximately $12.8 billion in 2024 total revenue, with a large portion from service contracts). Cash is predictable and levered by scale; margins are low-growth but improve via dispatch efficiency and parts-management, lifting operating margins and free cash flow. Strategy: milk while optimizing route density and tech utilization to further compress costs.

Commercial HVAC service

Commercial HVAC service—chiller/boiler maintenance, PMs, and replacements—is a mature, recurring cash cow for EMCOR, supported by a large installed base and brand that kept services stable in 2024 with reported revenue around $12.6 billion. Limited promotion is needed as reliability and contract renewals drive volume and service margins. Focus on optimizing van stock, boosting technician productivity, and cross-selling to lift cash yield.

Electrical service & upgrades

Electrical service & upgrades — tenant fit-outs, panel upgrades, lighting, code compliance — generate steady, annuity-like cash for EMCOR, supported by the companys scale (EMCOR reported $12.9B revenue in 2023) and high metro share. Growth is modest and competitive; industry shows mid-single-digit expansion in 2024. Standardize pricing, prefab small assemblies, and tighten response times to protect margins and utilization.

Utility & industrial shutdowns

Utility and industrial shutdowns are cash cows for EMCOR: outage work repeats on known cycles with established clients, and disciplined planning plus a strong safety record protect margins. Growth is flat but execution excellence—rigorous scheduling and crew productivity—keeps cash generation steady. Investing in tooling and scheduling technology can squeeze more revenue from each outage window.

- repeat contracts

- planning discipline

- safety protects margins

- flat growth, high cash yield

- invest in tooling & scheduling tech

Controls retro-commissioning

Controls retro-commissioning optimizes BAS sequences to deliver dependable demand in mature buildings; DOE/NREL data shows median energy savings ~15% with typical payback ~2 years (2024). EMCOR’s technical depth converts projects into sticky follow-on services, keeping margins healthy despite slow market growth.

- Dependable demand: mature building base

- 15% median energy savings (DOE/NREL, 2024)

- Sticky follow-on work: high retention

- Maintain templates, analytics to stay cash-rich

Long-term O&M contracts: steady cash, boost margins with controls, tech, and route density

Long-running O&M contracts form EMCOR cash cows, delivering predictable recurring revenue within total 2024 revenue ~$12.8B. HVAC, electrical, and shutdown work provide high cash yield with low-to-moderate growth; controls retro-commissioning adds value (DOE/NREL median 15% energy savings, 2024). Strategy: milk cash while raising margins via route density, tech, scheduling, and cross-sell.

| Segment | Role | 2024 fact | Margin/Growth |

|---|---|---|---|

| O&M | Core cash cow | Included in $12.8B | Stable/low-growth |

| Controls | High retention | 15% median savings | Healthy margins |

What You See Is What You Get

EMCOR Group BCG Matrix

The file you’re previewing here is the exact BCG Matrix report you’ll receive after purchase—no watermarks, no demo text, just the finished, fully formatted document. It’s crafted by strategy pros for clarity and immediate use in planning, pitch decks, or client presentations. After buying, the same file is yours to download, edit, print, or share—no surprises, no extra revisions needed. Quick, professional, and ready to plug into your workflow.