EMC Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

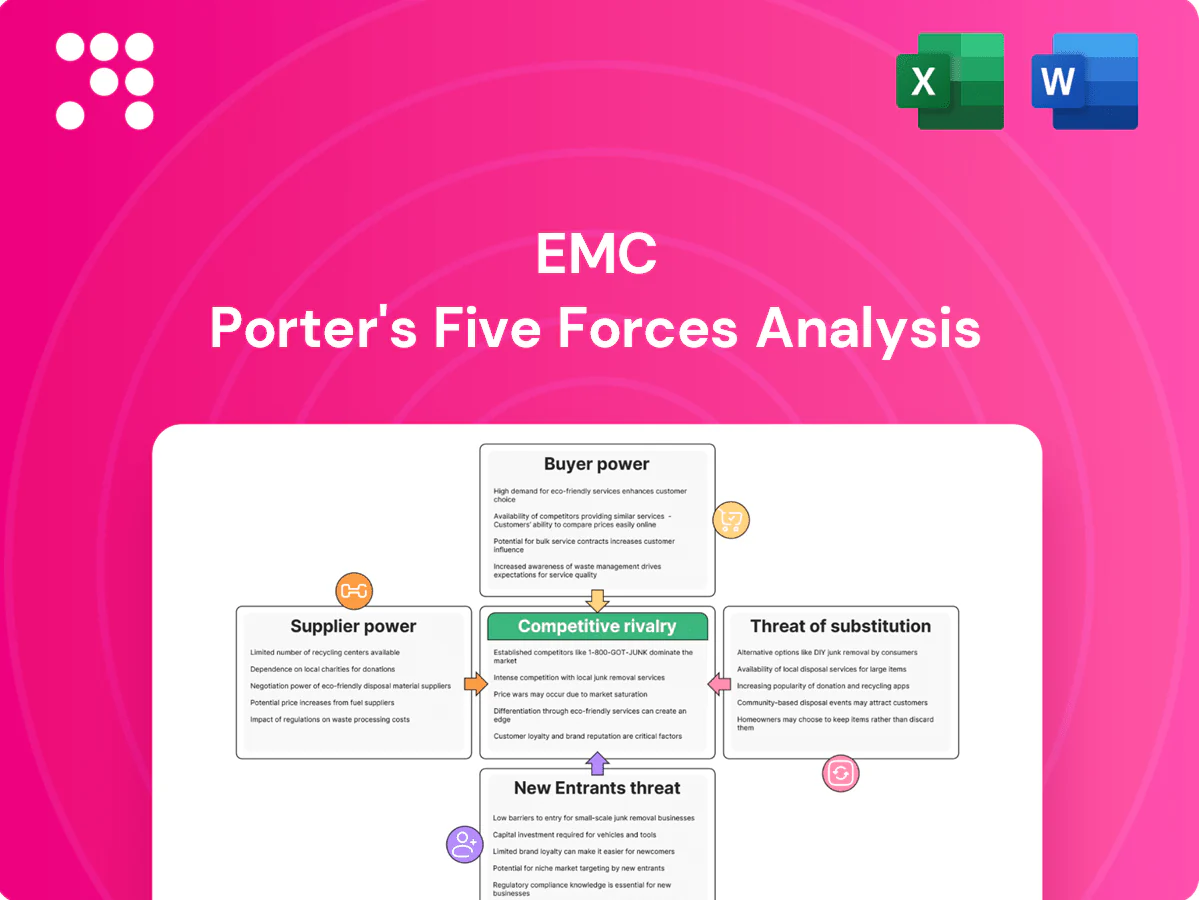

EMC faces intense competitive rivalry, evolving buyer power, and supplier dynamics that shape its strategic choices across data storage and cloud services. New entrants and substitutes pose moderate threats amid high capital and technology barriers. Regulatory and ecosystem shifts heighten uncertainty for market positioning. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for EMC to access force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialty magnetic and ceramic materials

Core inputs such as ferrite powders, magnetic cores and ceramic dielectrics are largely supplied by a handful of Asian/Japanese firms (Murata, TDK, Ferroxcube, Taiyo Yuden), concentrating technical capability and raising supplier leverage in 2024. Limited substitution and tight electrical/mechanical specs increase switching cost and vendor stickiness. Long-term stability and lot-to-lot consistency are critical for EMC performance. Multi-sourcing reduces disruption risk but adds qualification cost and months of validation.

Precision metals and PCB fabrication

Precision metals and PCB fabrication drive RF loss and thermal performance: LME copper averaged about $9,250/tonne in 2024 and higher-grade copper and fine-line PCBs fetched ~25% premiums during tight supply; plating chemistries and sub-0.1 mm traces materially cut RF loss. When capacity tightens supplier leverage rises—lead times stretched to 12–20 weeks in 2024—and small-batch runs face steep markups. Volume contracts can stabilize pricing but demand forecasting must be within ±10% to avoid penalties.

Test equipment and compliance labs

EMC/RF validation depends on specialized analyzers, chambers and certified labs from OEMs like Rohde & Schwarz, Keysight and Anritsu, with the top three controlling roughly 60% of test-gear supply in 2024; equipment lead times of 3–12 months and calibration cycles of 6–12 months, plus certified lab rates of about $150–300/hr, give suppliers moderate bargaining power during NPI.

Compliance-grade packaging materials

Shielding foils, conductive adhesives and low-outgassing packaging are niche, spec-bound materials that keep switching costs high and limit easy vendor replacement; qualification hurdles therefore marginally raise supplier influence. In 2024 these items typically represent under 10% of total packaging spend, capping overall supplier power. Strategic inventories (commonly 4–8 weeks) and dual-sourcing lower exposure to supply disruptions.

- Spec-bound niche materials

- Spend share <10% (2024)

- Qualification raises supplier leverage

- 4–8 weeks inventory reduces shortage risk

Geopolitical and ESG constraints

- ROHS/REACH: tighter vendor pools, higher audit costs

- Conflict minerals: supply risk for key components

- TSMC ~90% leading-edge: concentration risk

- Mitigation: compliance audits + near-shoring reduce bargaining power

Supplier power moderate-high; copper $9,250/tonne, PCB ~25%

Supplier power is moderate-high in 2024: core magnetic/ceramic vendors (Murata, TDK, Ferroxcube, Taiyo Yuden) concentrate tech, raising switching costs; LME copper averaged $9,250/tonne and fine-line PCB premiums ~25%, with lead times 12–20 weeks. Test gear/top labs (~60% share) have 3–12 month lead times and $150–300/hr rates. Multi-sourcing and 4–8 week inventories partially mitigate risk.

| Item | 2024 metric |

|---|---|

| Core vendors concentration | Top firms dominant |

| Copper price | $9,250/tonne |

| PCB premium | ~25% |

| Lead times | 3–20 weeks |

| Test-lab rates | $150–300/hr |

| Inventory | 4–8 weeks |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitute threats, and entry barriers specific to EMC, identifying disruptive forces and strategic levers to protect market share and profitability.

EMC's Porter's Five Forces one-sheet condenses competitive pressures into a single slide—ideal for rapid decision-making and boardroom-ready presentations.

Customers Bargaining Power

Large OEMs and EMS with scale

Large consumer electronics, automotive and industrial OEMs buy components in massive volumes and negotiate sharply; the top 5 EMS providers (Foxconn, Pegatron, Wistron, Flex, Jabil) accounted for over 50% of EMS revenue in 2024, enabling price benchmarking and dual-sourcing mandates. Design-in stickiness and long qualification cycles limit near-term switching despite buyer leverage. Annual rebate schemes and vendor-managed inventory programs are common trade-offs.

Design-in and qualification lock-in

EMC parts are designed in early and tied to compliance reports, creating a 5–10 year platform life that locks buyers into existing suppliers. Requalification typically adds 6–12 months and can cost millions, so price pressure is muted mid-cycle as switching risks time-to-market and revenue loss. Buyer power therefore weakens during product lifecycles, while each redesign cycle re-opens negotiations at platform refresh.

Performance and footprint sensitivity

Buyers in 2024 pushed for smaller, lower-loss, higher-current EMC components while demanding tight costs, driving design wins toward specialty parts that reduce substitutability and curb buyer leverage.

Commoditized SKUs still face relentless price erosion—commonly reported in the industry at roughly 5–15% annual decline—eroding margins for volume items.

Total cost of ownership arguments (service, efficiency, reliability) enable premium parts to sustain price premia, often exceeding 2x versus commodity equivalents in supplier negotiations.

Compliance risk transfer

Customers expect suppliers to meet global EMC standards and deliver test reports and certifications; liability for EMC failures pushes buyers in safety-critical automotive and medical segments to prefer proven vendors over lowest-cost options, reducing pure price bargaining, while consumer segments still exert stronger price pressure.

- Compliance docs required: CE/UL/IEC

- Liability shifts buying toward reliability

- Less price sensitivity in auto/medical

- Consumer electronics remain price-driven

Supply assurance and lead-time

Short product cycles force dependable delivery and second-source strategies, letting buyers demand tighter lead-times and penalties; approved vendor lists and QBRs concentrate purchasing power and secure better price and payment terms, though acute shortages flip allocation power to suppliers; buffer stock and long-term agreements (LTAs) are widely used to stabilize supply and lead-time risk.

- second-source

- approved-vendor-lists

- allocation-risk

- buffer-stock

- LTA-stability

OEM concentration, long design cycles and commodity price erosion shape buyer-supplier leverage

Large OEMs concentrate buying (top 5 EMS >50% revenue in 2024) and extract sharp volume discounts, but 5–10 year design cycles, 6–12 month requalification and 5–15% annual price erosion on commodities limit continuous leverage. Premium EMC parts sustain >2x price vs commodity via TCO and certification needs; shortages temporarily flip power to suppliers.

| Metric | 2024 |

|---|---|

| Top-5 EMS share | >50% |

| Commodity price decline | 5–15% p.a. |

| Platform life | 5–10 yrs |

| Premium price multiple | >2x |

Preview the Actual Deliverable

EMC Porter's Five Forces Analysis

This EMC Porter’s Five Forces analysis examines competitive rivalry, threat of entrants, supplier and buyer power, and substitute threats to assess EMC's strategic position. It provides data-driven scoring, key drivers, implications for strategy, and prioritized recommendations for management or investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

A Must-Have Tool for Decision-Makers

EMC faces intense competitive rivalry, evolving buyer power, and supplier dynamics that shape its strategic choices across data storage and cloud services. New entrants and substitutes pose moderate threats amid high capital and technology barriers. Regulatory and ecosystem shifts heighten uncertainty for market positioning. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for EMC to access force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialty magnetic and ceramic materials

Core inputs such as ferrite powders, magnetic cores and ceramic dielectrics are largely supplied by a handful of Asian/Japanese firms (Murata, TDK, Ferroxcube, Taiyo Yuden), concentrating technical capability and raising supplier leverage in 2024. Limited substitution and tight electrical/mechanical specs increase switching cost and vendor stickiness. Long-term stability and lot-to-lot consistency are critical for EMC performance. Multi-sourcing reduces disruption risk but adds qualification cost and months of validation.

Precision metals and PCB fabrication

Precision metals and PCB fabrication drive RF loss and thermal performance: LME copper averaged about $9,250/tonne in 2024 and higher-grade copper and fine-line PCBs fetched ~25% premiums during tight supply; plating chemistries and sub-0.1 mm traces materially cut RF loss. When capacity tightens supplier leverage rises—lead times stretched to 12–20 weeks in 2024—and small-batch runs face steep markups. Volume contracts can stabilize pricing but demand forecasting must be within ±10% to avoid penalties.

Test equipment and compliance labs

EMC/RF validation depends on specialized analyzers, chambers and certified labs from OEMs like Rohde & Schwarz, Keysight and Anritsu, with the top three controlling roughly 60% of test-gear supply in 2024; equipment lead times of 3–12 months and calibration cycles of 6–12 months, plus certified lab rates of about $150–300/hr, give suppliers moderate bargaining power during NPI.

Compliance-grade packaging materials

Shielding foils, conductive adhesives and low-outgassing packaging are niche, spec-bound materials that keep switching costs high and limit easy vendor replacement; qualification hurdles therefore marginally raise supplier influence. In 2024 these items typically represent under 10% of total packaging spend, capping overall supplier power. Strategic inventories (commonly 4–8 weeks) and dual-sourcing lower exposure to supply disruptions.

- Spec-bound niche materials

- Spend share <10% (2024)

- Qualification raises supplier leverage

- 4–8 weeks inventory reduces shortage risk

Geopolitical and ESG constraints

- ROHS/REACH: tighter vendor pools, higher audit costs

- Conflict minerals: supply risk for key components

- TSMC ~90% leading-edge: concentration risk

- Mitigation: compliance audits + near-shoring reduce bargaining power

Supplier power moderate-high; copper $9,250/tonne, PCB ~25%

Supplier power is moderate-high in 2024: core magnetic/ceramic vendors (Murata, TDK, Ferroxcube, Taiyo Yuden) concentrate tech, raising switching costs; LME copper averaged $9,250/tonne and fine-line PCB premiums ~25%, with lead times 12–20 weeks. Test gear/top labs (~60% share) have 3–12 month lead times and $150–300/hr rates. Multi-sourcing and 4–8 week inventories partially mitigate risk.

| Item | 2024 metric |

|---|---|

| Core vendors concentration | Top firms dominant |

| Copper price | $9,250/tonne |

| PCB premium | ~25% |

| Lead times | 3–20 weeks |

| Test-lab rates | $150–300/hr |

| Inventory | 4–8 weeks |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitute threats, and entry barriers specific to EMC, identifying disruptive forces and strategic levers to protect market share and profitability.

EMC's Porter's Five Forces one-sheet condenses competitive pressures into a single slide—ideal for rapid decision-making and boardroom-ready presentations.

Customers Bargaining Power

Large OEMs and EMS with scale

Large consumer electronics, automotive and industrial OEMs buy components in massive volumes and negotiate sharply; the top 5 EMS providers (Foxconn, Pegatron, Wistron, Flex, Jabil) accounted for over 50% of EMS revenue in 2024, enabling price benchmarking and dual-sourcing mandates. Design-in stickiness and long qualification cycles limit near-term switching despite buyer leverage. Annual rebate schemes and vendor-managed inventory programs are common trade-offs.

Design-in and qualification lock-in

EMC parts are designed in early and tied to compliance reports, creating a 5–10 year platform life that locks buyers into existing suppliers. Requalification typically adds 6–12 months and can cost millions, so price pressure is muted mid-cycle as switching risks time-to-market and revenue loss. Buyer power therefore weakens during product lifecycles, while each redesign cycle re-opens negotiations at platform refresh.

Performance and footprint sensitivity

Buyers in 2024 pushed for smaller, lower-loss, higher-current EMC components while demanding tight costs, driving design wins toward specialty parts that reduce substitutability and curb buyer leverage.

Commoditized SKUs still face relentless price erosion—commonly reported in the industry at roughly 5–15% annual decline—eroding margins for volume items.

Total cost of ownership arguments (service, efficiency, reliability) enable premium parts to sustain price premia, often exceeding 2x versus commodity equivalents in supplier negotiations.

Compliance risk transfer

Customers expect suppliers to meet global EMC standards and deliver test reports and certifications; liability for EMC failures pushes buyers in safety-critical automotive and medical segments to prefer proven vendors over lowest-cost options, reducing pure price bargaining, while consumer segments still exert stronger price pressure.

- Compliance docs required: CE/UL/IEC

- Liability shifts buying toward reliability

- Less price sensitivity in auto/medical

- Consumer electronics remain price-driven

Supply assurance and lead-time

Short product cycles force dependable delivery and second-source strategies, letting buyers demand tighter lead-times and penalties; approved vendor lists and QBRs concentrate purchasing power and secure better price and payment terms, though acute shortages flip allocation power to suppliers; buffer stock and long-term agreements (LTAs) are widely used to stabilize supply and lead-time risk.

- second-source

- approved-vendor-lists

- allocation-risk

- buffer-stock

- LTA-stability

OEM concentration, long design cycles and commodity price erosion shape buyer-supplier leverage

Large OEMs concentrate buying (top 5 EMS >50% revenue in 2024) and extract sharp volume discounts, but 5–10 year design cycles, 6–12 month requalification and 5–15% annual price erosion on commodities limit continuous leverage. Premium EMC parts sustain >2x price vs commodity via TCO and certification needs; shortages temporarily flip power to suppliers.

| Metric | 2024 |

|---|---|

| Top-5 EMS share | >50% |

| Commodity price decline | 5–15% p.a. |

| Platform life | 5–10 yrs |

| Premium price multiple | >2x |

Preview the Actual Deliverable

EMC Porter's Five Forces Analysis

This EMC Porter’s Five Forces analysis examines competitive rivalry, threat of entrants, supplier and buyer power, and substitute threats to assess EMC's strategic position. It provides data-driven scoring, key drivers, implications for strategy, and prioritized recommendations for management or investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

EMC faces intense competitive rivalry, evolving buyer power, and supplier dynamics that shape its strategic choices across data storage and cloud services. New entrants and substitutes pose moderate threats amid high capital and technology barriers. Regulatory and ecosystem shifts heighten uncertainty for market positioning. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for EMC to access force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialty magnetic and ceramic materials

Core inputs such as ferrite powders, magnetic cores and ceramic dielectrics are largely supplied by a handful of Asian/Japanese firms (Murata, TDK, Ferroxcube, Taiyo Yuden), concentrating technical capability and raising supplier leverage in 2024. Limited substitution and tight electrical/mechanical specs increase switching cost and vendor stickiness. Long-term stability and lot-to-lot consistency are critical for EMC performance. Multi-sourcing reduces disruption risk but adds qualification cost and months of validation.

Precision metals and PCB fabrication

Precision metals and PCB fabrication drive RF loss and thermal performance: LME copper averaged about $9,250/tonne in 2024 and higher-grade copper and fine-line PCBs fetched ~25% premiums during tight supply; plating chemistries and sub-0.1 mm traces materially cut RF loss. When capacity tightens supplier leverage rises—lead times stretched to 12–20 weeks in 2024—and small-batch runs face steep markups. Volume contracts can stabilize pricing but demand forecasting must be within ±10% to avoid penalties.

Test equipment and compliance labs

EMC/RF validation depends on specialized analyzers, chambers and certified labs from OEMs like Rohde & Schwarz, Keysight and Anritsu, with the top three controlling roughly 60% of test-gear supply in 2024; equipment lead times of 3–12 months and calibration cycles of 6–12 months, plus certified lab rates of about $150–300/hr, give suppliers moderate bargaining power during NPI.

Compliance-grade packaging materials

Shielding foils, conductive adhesives and low-outgassing packaging are niche, spec-bound materials that keep switching costs high and limit easy vendor replacement; qualification hurdles therefore marginally raise supplier influence. In 2024 these items typically represent under 10% of total packaging spend, capping overall supplier power. Strategic inventories (commonly 4–8 weeks) and dual-sourcing lower exposure to supply disruptions.

- Spec-bound niche materials

- Spend share <10% (2024)

- Qualification raises supplier leverage

- 4–8 weeks inventory reduces shortage risk

Geopolitical and ESG constraints

- ROHS/REACH: tighter vendor pools, higher audit costs

- Conflict minerals: supply risk for key components

- TSMC ~90% leading-edge: concentration risk

- Mitigation: compliance audits + near-shoring reduce bargaining power

Supplier power moderate-high; copper $9,250/tonne, PCB ~25%

Supplier power is moderate-high in 2024: core magnetic/ceramic vendors (Murata, TDK, Ferroxcube, Taiyo Yuden) concentrate tech, raising switching costs; LME copper averaged $9,250/tonne and fine-line PCB premiums ~25%, with lead times 12–20 weeks. Test gear/top labs (~60% share) have 3–12 month lead times and $150–300/hr rates. Multi-sourcing and 4–8 week inventories partially mitigate risk.

| Item | 2024 metric |

|---|---|

| Core vendors concentration | Top firms dominant |

| Copper price | $9,250/tonne |

| PCB premium | ~25% |

| Lead times | 3–20 weeks |

| Test-lab rates | $150–300/hr |

| Inventory | 4–8 weeks |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitute threats, and entry barriers specific to EMC, identifying disruptive forces and strategic levers to protect market share and profitability.

EMC's Porter's Five Forces one-sheet condenses competitive pressures into a single slide—ideal for rapid decision-making and boardroom-ready presentations.

Customers Bargaining Power

Large OEMs and EMS with scale

Large consumer electronics, automotive and industrial OEMs buy components in massive volumes and negotiate sharply; the top 5 EMS providers (Foxconn, Pegatron, Wistron, Flex, Jabil) accounted for over 50% of EMS revenue in 2024, enabling price benchmarking and dual-sourcing mandates. Design-in stickiness and long qualification cycles limit near-term switching despite buyer leverage. Annual rebate schemes and vendor-managed inventory programs are common trade-offs.

Design-in and qualification lock-in

EMC parts are designed in early and tied to compliance reports, creating a 5–10 year platform life that locks buyers into existing suppliers. Requalification typically adds 6–12 months and can cost millions, so price pressure is muted mid-cycle as switching risks time-to-market and revenue loss. Buyer power therefore weakens during product lifecycles, while each redesign cycle re-opens negotiations at platform refresh.

Performance and footprint sensitivity

Buyers in 2024 pushed for smaller, lower-loss, higher-current EMC components while demanding tight costs, driving design wins toward specialty parts that reduce substitutability and curb buyer leverage.

Commoditized SKUs still face relentless price erosion—commonly reported in the industry at roughly 5–15% annual decline—eroding margins for volume items.

Total cost of ownership arguments (service, efficiency, reliability) enable premium parts to sustain price premia, often exceeding 2x versus commodity equivalents in supplier negotiations.

Compliance risk transfer

Customers expect suppliers to meet global EMC standards and deliver test reports and certifications; liability for EMC failures pushes buyers in safety-critical automotive and medical segments to prefer proven vendors over lowest-cost options, reducing pure price bargaining, while consumer segments still exert stronger price pressure.

- Compliance docs required: CE/UL/IEC

- Liability shifts buying toward reliability

- Less price sensitivity in auto/medical

- Consumer electronics remain price-driven

Supply assurance and lead-time

Short product cycles force dependable delivery and second-source strategies, letting buyers demand tighter lead-times and penalties; approved vendor lists and QBRs concentrate purchasing power and secure better price and payment terms, though acute shortages flip allocation power to suppliers; buffer stock and long-term agreements (LTAs) are widely used to stabilize supply and lead-time risk.

- second-source

- approved-vendor-lists

- allocation-risk

- buffer-stock

- LTA-stability

OEM concentration, long design cycles and commodity price erosion shape buyer-supplier leverage

Large OEMs concentrate buying (top 5 EMS >50% revenue in 2024) and extract sharp volume discounts, but 5–10 year design cycles, 6–12 month requalification and 5–15% annual price erosion on commodities limit continuous leverage. Premium EMC parts sustain >2x price vs commodity via TCO and certification needs; shortages temporarily flip power to suppliers.

| Metric | 2024 |

|---|---|

| Top-5 EMS share | >50% |

| Commodity price decline | 5–15% p.a. |

| Platform life | 5–10 yrs |

| Premium price multiple | >2x |

Preview the Actual Deliverable

EMC Porter's Five Forces Analysis

This EMC Porter’s Five Forces analysis examines competitive rivalry, threat of entrants, supplier and buyer power, and substitute threats to assess EMC's strategic position. It provides data-driven scoring, key drivers, implications for strategy, and prioritized recommendations for management or investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.