Emeco PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are shaping Emeco’s strategic outlook in our concise PESTLE snapshot—designed for investors and strategists. This ready-to-use analysis highlights risks and opportunities you can act on immediately. Purchase the full PESTLE to access detailed, editable insights and make confident decisions.

Political factors

Resource royalties and mining policy shifts

Changes in federal and state royalty regimes can widen miners’ cost bases and shift rental appetite, reducing fleet utilization visibility for Emeco; policy moves that enable or delay new mine approvals directly affect near-term demand for heavy-equipment hire.

Infrastructure and regional development priorities

Government spend on roads, ports and energy reliability directly shapes mine uptime and equipment utilization; for example Port Hedland handled about 561 million tonnes in 2023-24, so port and road improvements materially affect fleet loading and turnarounds. Improved haul roads can reduce cycle times, shifting fleet mix and extending maintenance intervals. Delays in public works elevate downtime and logistics costs, so Emeco can co-plan deployment with regional capital programs to align asset timing and reduce idle rates.

Trade relations and equipment import tariffs

Shifts in tariffs or trade tensions raise the landed cost of heavy machinery and parts, increasing maintenance and capex per unit and pressuring margins. Variable lead-times from customs or export controls disrupt fleet availability and project scheduling. Emeco’s diversified sourcing and dealer network reduce political supply risk, while forward hedging on freight/currency and inventory buffers protect service levels and uptime.

Indigenous affairs and local stakeholder expectations

Policies on Indigenous engagement, anchored by the federal Indigenous Procurement Policy target of 3% for government contracts, guide hiring, training and procurement pathways for Emeco near mine sites. Strong compliance boosts social licence to operate and supports awarding of long-tenor service contracts; mining projects commonly set local Indigenous employment targets of 10–20%. Misalignment risks project delays, fines or contract loss.

- Compliance: aligns with IPP 3% procurement target

- Revenue impact: secures long-tenor contracts

- Risk: misalignment can cause delays or contract termination

Geopolitical commodity security and critical minerals

National critical-minerals strategies (Australia’s A$2.3bn package announced in 2023) are speeding approvals and permitting, accelerating mine and processing projects; rising demand for lithium, nickel and rare earths is reshaping fleet allocation toward battery- and magnet-metal plays. Emeco can prioritise growth basins aligned with these policy tailwinds and use scenario planning to balance commodity exposure and operational risk.

- Policy tailwinds: A$2.3bn (Australia)

- Commodity shift: lithium, nickel, rare earths

- Strategy: focus on aligned basins

- Risk control: scenario planning to diversify exposure

Royalties, permits and A$2.3bn spend drive fleet demand; Port Hedland 561mt and IPP 3%

Royalty, tariff and permitting changes plus public infrastructure spend drive Emeco fleet utilisation and capex; Port Hedland handled ~561mt in 2023–24 and Australia announced A$2.3bn for critical minerals in 2023. Indigenous Procurement Policy 3% and common local hiring targets (10–20%) influence contract access and social licence.

| Factor | 2023–24 datapoint | Impact |

|---|---|---|

| Port throughput | Port Hedland ~561mt | fleet loading/turnarounds |

| Policy funding | A$2.3bn | permits, demand for equipment |

| Indigenous policy | IPP 3%; targets 10–20% | contract eligibility |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely affect Emeco, combining data-driven trends and region-specific regulatory context to identify risks and opportunities for executives, investors and strategists in concise, actionable form.

Emeco's PESTLE analysis condenses external risk insights into a clean, visually segmented summary for quick interpretation and seamless inclusion in presentations. Editable notes and shareable formatting make it ideal for team alignment and client-ready strategy packs.

Economic factors

Commodity price cycles and miners’ capex/opex mix

In commodity downcycles miners shift from capex to renting, lifting Emeco fleet utilisation to near 70% in 2024 as reflected in higher rental days; in upcycles capex returns but short-term rentals still bridge supply gaps with spot rates rising ~25% during 2023–24 spikes. Emeco’s flexible terms capture both phases and contract diversity—daily, medium and long-term—underpins revenue resilience and reduced cyclicality.

Interest rates and financing costs

Higher policy rates in 2024–25 and elevated 10-year Treasury yields around 4–4.5% raise Emeco’s cost to acquire and refinance heavy fleet, boosting financing expense and CAPEX hurdle rates. Clients’ WACC shifts increase rental duration and price sensitivity, reducing utilisation risk for short-term hires. Emeco must optimise leverage and tenor and use rate hedges to stabilise cash flows and protect margins.

Currency volatility (AUD/USD) on parts and assets

Imported equipment and components expose Emeco’s COGS to AUD/USD swings; AUD/USD was around 0.65 in mid‑2025, amplifying landed costs. A weaker AUD inflates maintenance and replacement spend, pressuring margins. Contractual FX pass‑through clauses help protect EBITDA, while USD‑linked hire and sale contracts create natural hedges that reduce net FX exposure.

Labor availability and wage inflation

Tight markets for diesel fitters and operators are increasing repair turnaround and costs; with Australia Wage Price Index at about 3.9% year to June 2024 and unemployment near 3.6%, wage pressure can compress Emeco margins if not priced through. Emeco’s in-house training pipelines and productivity tools improve technician throughput and regional labour planning reduces churn and mobilisation delays.

- WPI ~3.9% (Jun 2024)

- Unemployment ~3.6% (2024)

- Training pipelines raise internal supply

- Regional planning cuts churn and mobilisation time

Client capital discipline and procurement trends

Miners’ intensified focus on cash flow and ROIC is driving demand for value-based rental solutions that eliminate upfront capex and can cut total equipment TCO by up to 20% in industry benchmarks. Longer-term, performance‑linked contracts (3–7 year terms) are improving revenue visibility and alignment with mine life. Bundled maintenance offers win rates versus outright sale by lowering downtime and enabling predictable operating costs, while data‑backed SLAs (telemetry, uptime targets) strengthen Emeco’s negotiation position.

- cashflow-driven rental demand

- ROIC alignment via value rentals

- 3–7 year performance contracts improve visibility

- bundled maintenance reduces TCO

- data-backed SLAs bolster pricing power

Royalties, permits and A$2.3bn spend drive fleet demand; Port Hedland 561mt and IPP 3%

Commodity downcycles lifted fleet utilisation to ~70% in 2024 while spot rates spiked ~25% in 2023–24; flexible daily, medium and long‑term contracts underpin revenue resilience. Higher policy rates and 10y yields ~4–4.5% (2024–25) raise financing costs and CAPEX hurdles, increasing price sensitivity. AUD/USD ~0.65 (mid‑2025) and WPI ~3.9% (Jun 2024) squeeze COGS and wages; FX pass‑throughs and training mitigate risk.

| Metric | Value |

|---|---|

| Fleet utilisation (2024) | ~70% |

| Spot rate spike (2023–24) | ~+25% |

| 10y Treasury / yields | 4–4.5% |

| AUD/USD (mid‑2025) | ~0.65 |

| WPI (Jun 2024) | ~3.9% |

| Unemployment (2024) | ~3.6% |

Preview the Actual Deliverable

Emeco PESTLE Analysis

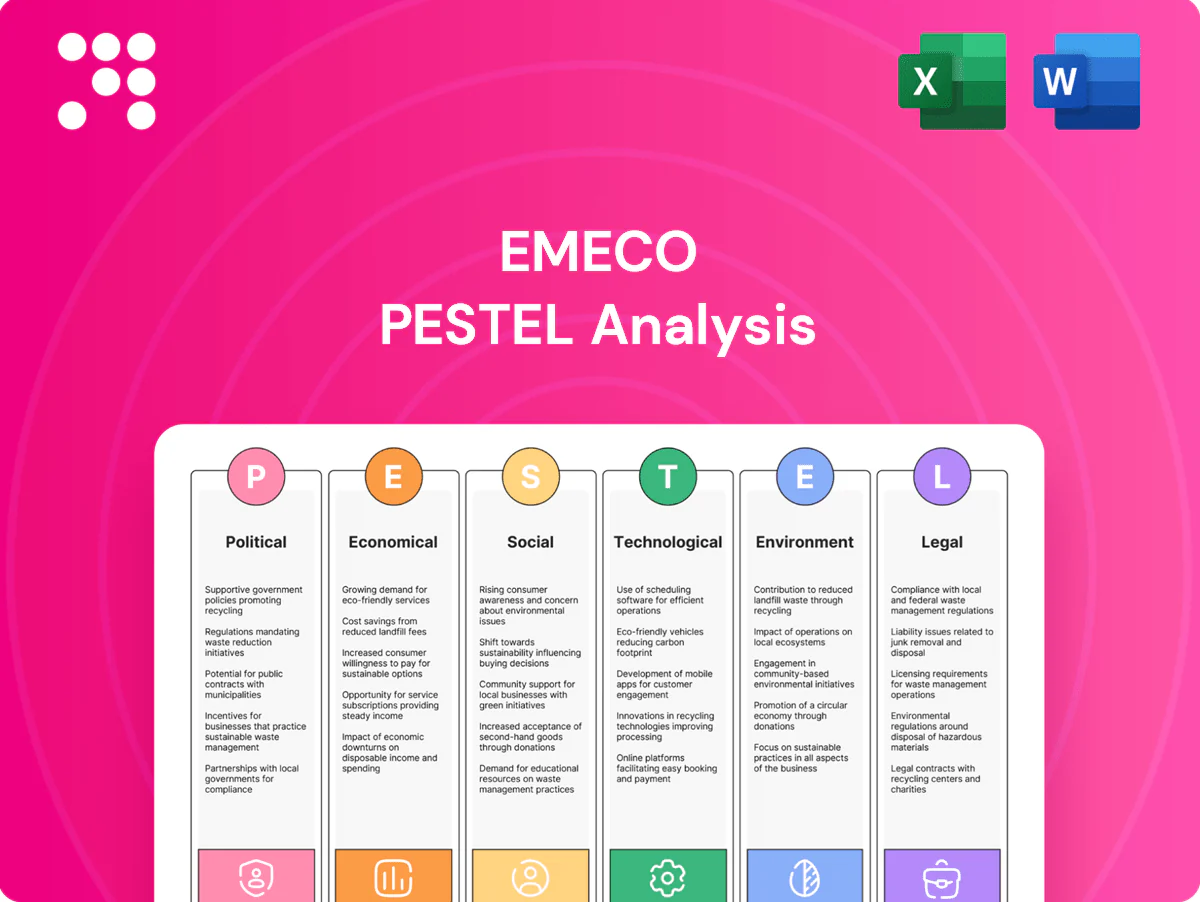

The preview shown here is the exact Emeco PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible are exactly what you’ll download immediately after buying.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are shaping Emeco’s strategic outlook in our concise PESTLE snapshot—designed for investors and strategists. This ready-to-use analysis highlights risks and opportunities you can act on immediately. Purchase the full PESTLE to access detailed, editable insights and make confident decisions.

Political factors

Resource royalties and mining policy shifts

Changes in federal and state royalty regimes can widen miners’ cost bases and shift rental appetite, reducing fleet utilization visibility for Emeco; policy moves that enable or delay new mine approvals directly affect near-term demand for heavy-equipment hire.

Infrastructure and regional development priorities

Government spend on roads, ports and energy reliability directly shapes mine uptime and equipment utilization; for example Port Hedland handled about 561 million tonnes in 2023-24, so port and road improvements materially affect fleet loading and turnarounds. Improved haul roads can reduce cycle times, shifting fleet mix and extending maintenance intervals. Delays in public works elevate downtime and logistics costs, so Emeco can co-plan deployment with regional capital programs to align asset timing and reduce idle rates.

Trade relations and equipment import tariffs

Shifts in tariffs or trade tensions raise the landed cost of heavy machinery and parts, increasing maintenance and capex per unit and pressuring margins. Variable lead-times from customs or export controls disrupt fleet availability and project scheduling. Emeco’s diversified sourcing and dealer network reduce political supply risk, while forward hedging on freight/currency and inventory buffers protect service levels and uptime.

Indigenous affairs and local stakeholder expectations

Policies on Indigenous engagement, anchored by the federal Indigenous Procurement Policy target of 3% for government contracts, guide hiring, training and procurement pathways for Emeco near mine sites. Strong compliance boosts social licence to operate and supports awarding of long-tenor service contracts; mining projects commonly set local Indigenous employment targets of 10–20%. Misalignment risks project delays, fines or contract loss.

- Compliance: aligns with IPP 3% procurement target

- Revenue impact: secures long-tenor contracts

- Risk: misalignment can cause delays or contract termination

Geopolitical commodity security and critical minerals

National critical-minerals strategies (Australia’s A$2.3bn package announced in 2023) are speeding approvals and permitting, accelerating mine and processing projects; rising demand for lithium, nickel and rare earths is reshaping fleet allocation toward battery- and magnet-metal plays. Emeco can prioritise growth basins aligned with these policy tailwinds and use scenario planning to balance commodity exposure and operational risk.

- Policy tailwinds: A$2.3bn (Australia)

- Commodity shift: lithium, nickel, rare earths

- Strategy: focus on aligned basins

- Risk control: scenario planning to diversify exposure

Royalties, permits and A$2.3bn spend drive fleet demand; Port Hedland 561mt and IPP 3%

Royalty, tariff and permitting changes plus public infrastructure spend drive Emeco fleet utilisation and capex; Port Hedland handled ~561mt in 2023–24 and Australia announced A$2.3bn for critical minerals in 2023. Indigenous Procurement Policy 3% and common local hiring targets (10–20%) influence contract access and social licence.

| Factor | 2023–24 datapoint | Impact |

|---|---|---|

| Port throughput | Port Hedland ~561mt | fleet loading/turnarounds |

| Policy funding | A$2.3bn | permits, demand for equipment |

| Indigenous policy | IPP 3%; targets 10–20% | contract eligibility |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely affect Emeco, combining data-driven trends and region-specific regulatory context to identify risks and opportunities for executives, investors and strategists in concise, actionable form.

Emeco's PESTLE analysis condenses external risk insights into a clean, visually segmented summary for quick interpretation and seamless inclusion in presentations. Editable notes and shareable formatting make it ideal for team alignment and client-ready strategy packs.

Economic factors

Commodity price cycles and miners’ capex/opex mix

In commodity downcycles miners shift from capex to renting, lifting Emeco fleet utilisation to near 70% in 2024 as reflected in higher rental days; in upcycles capex returns but short-term rentals still bridge supply gaps with spot rates rising ~25% during 2023–24 spikes. Emeco’s flexible terms capture both phases and contract diversity—daily, medium and long-term—underpins revenue resilience and reduced cyclicality.

Interest rates and financing costs

Higher policy rates in 2024–25 and elevated 10-year Treasury yields around 4–4.5% raise Emeco’s cost to acquire and refinance heavy fleet, boosting financing expense and CAPEX hurdle rates. Clients’ WACC shifts increase rental duration and price sensitivity, reducing utilisation risk for short-term hires. Emeco must optimise leverage and tenor and use rate hedges to stabilise cash flows and protect margins.

Currency volatility (AUD/USD) on parts and assets

Imported equipment and components expose Emeco’s COGS to AUD/USD swings; AUD/USD was around 0.65 in mid‑2025, amplifying landed costs. A weaker AUD inflates maintenance and replacement spend, pressuring margins. Contractual FX pass‑through clauses help protect EBITDA, while USD‑linked hire and sale contracts create natural hedges that reduce net FX exposure.

Labor availability and wage inflation

Tight markets for diesel fitters and operators are increasing repair turnaround and costs; with Australia Wage Price Index at about 3.9% year to June 2024 and unemployment near 3.6%, wage pressure can compress Emeco margins if not priced through. Emeco’s in-house training pipelines and productivity tools improve technician throughput and regional labour planning reduces churn and mobilisation delays.

- WPI ~3.9% (Jun 2024)

- Unemployment ~3.6% (2024)

- Training pipelines raise internal supply

- Regional planning cuts churn and mobilisation time

Client capital discipline and procurement trends

Miners’ intensified focus on cash flow and ROIC is driving demand for value-based rental solutions that eliminate upfront capex and can cut total equipment TCO by up to 20% in industry benchmarks. Longer-term, performance‑linked contracts (3–7 year terms) are improving revenue visibility and alignment with mine life. Bundled maintenance offers win rates versus outright sale by lowering downtime and enabling predictable operating costs, while data‑backed SLAs (telemetry, uptime targets) strengthen Emeco’s negotiation position.

- cashflow-driven rental demand

- ROIC alignment via value rentals

- 3–7 year performance contracts improve visibility

- bundled maintenance reduces TCO

- data-backed SLAs bolster pricing power

Royalties, permits and A$2.3bn spend drive fleet demand; Port Hedland 561mt and IPP 3%

Commodity downcycles lifted fleet utilisation to ~70% in 2024 while spot rates spiked ~25% in 2023–24; flexible daily, medium and long‑term contracts underpin revenue resilience. Higher policy rates and 10y yields ~4–4.5% (2024–25) raise financing costs and CAPEX hurdles, increasing price sensitivity. AUD/USD ~0.65 (mid‑2025) and WPI ~3.9% (Jun 2024) squeeze COGS and wages; FX pass‑throughs and training mitigate risk.

| Metric | Value |

|---|---|

| Fleet utilisation (2024) | ~70% |

| Spot rate spike (2023–24) | ~+25% |

| 10y Treasury / yields | 4–4.5% |

| AUD/USD (mid‑2025) | ~0.65 |

| WPI (Jun 2024) | ~3.9% |

| Unemployment (2024) | ~3.6% |

Preview the Actual Deliverable

Emeco PESTLE Analysis

The preview shown here is the exact Emeco PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible are exactly what you’ll download immediately after buying.

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are shaping Emeco’s strategic outlook in our concise PESTLE snapshot—designed for investors and strategists. This ready-to-use analysis highlights risks and opportunities you can act on immediately. Purchase the full PESTLE to access detailed, editable insights and make confident decisions.

Political factors

Resource royalties and mining policy shifts

Changes in federal and state royalty regimes can widen miners’ cost bases and shift rental appetite, reducing fleet utilization visibility for Emeco; policy moves that enable or delay new mine approvals directly affect near-term demand for heavy-equipment hire.

Infrastructure and regional development priorities

Government spend on roads, ports and energy reliability directly shapes mine uptime and equipment utilization; for example Port Hedland handled about 561 million tonnes in 2023-24, so port and road improvements materially affect fleet loading and turnarounds. Improved haul roads can reduce cycle times, shifting fleet mix and extending maintenance intervals. Delays in public works elevate downtime and logistics costs, so Emeco can co-plan deployment with regional capital programs to align asset timing and reduce idle rates.

Trade relations and equipment import tariffs

Shifts in tariffs or trade tensions raise the landed cost of heavy machinery and parts, increasing maintenance and capex per unit and pressuring margins. Variable lead-times from customs or export controls disrupt fleet availability and project scheduling. Emeco’s diversified sourcing and dealer network reduce political supply risk, while forward hedging on freight/currency and inventory buffers protect service levels and uptime.

Indigenous affairs and local stakeholder expectations

Policies on Indigenous engagement, anchored by the federal Indigenous Procurement Policy target of 3% for government contracts, guide hiring, training and procurement pathways for Emeco near mine sites. Strong compliance boosts social licence to operate and supports awarding of long-tenor service contracts; mining projects commonly set local Indigenous employment targets of 10–20%. Misalignment risks project delays, fines or contract loss.

- Compliance: aligns with IPP 3% procurement target

- Revenue impact: secures long-tenor contracts

- Risk: misalignment can cause delays or contract termination

Geopolitical commodity security and critical minerals

National critical-minerals strategies (Australia’s A$2.3bn package announced in 2023) are speeding approvals and permitting, accelerating mine and processing projects; rising demand for lithium, nickel and rare earths is reshaping fleet allocation toward battery- and magnet-metal plays. Emeco can prioritise growth basins aligned with these policy tailwinds and use scenario planning to balance commodity exposure and operational risk.

- Policy tailwinds: A$2.3bn (Australia)

- Commodity shift: lithium, nickel, rare earths

- Strategy: focus on aligned basins

- Risk control: scenario planning to diversify exposure

Royalties, permits and A$2.3bn spend drive fleet demand; Port Hedland 561mt and IPP 3%

Royalty, tariff and permitting changes plus public infrastructure spend drive Emeco fleet utilisation and capex; Port Hedland handled ~561mt in 2023–24 and Australia announced A$2.3bn for critical minerals in 2023. Indigenous Procurement Policy 3% and common local hiring targets (10–20%) influence contract access and social licence.

| Factor | 2023–24 datapoint | Impact |

|---|---|---|

| Port throughput | Port Hedland ~561mt | fleet loading/turnarounds |

| Policy funding | A$2.3bn | permits, demand for equipment |

| Indigenous policy | IPP 3%; targets 10–20% | contract eligibility |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely affect Emeco, combining data-driven trends and region-specific regulatory context to identify risks and opportunities for executives, investors and strategists in concise, actionable form.

Emeco's PESTLE analysis condenses external risk insights into a clean, visually segmented summary for quick interpretation and seamless inclusion in presentations. Editable notes and shareable formatting make it ideal for team alignment and client-ready strategy packs.

Economic factors

Commodity price cycles and miners’ capex/opex mix

In commodity downcycles miners shift from capex to renting, lifting Emeco fleet utilisation to near 70% in 2024 as reflected in higher rental days; in upcycles capex returns but short-term rentals still bridge supply gaps with spot rates rising ~25% during 2023–24 spikes. Emeco’s flexible terms capture both phases and contract diversity—daily, medium and long-term—underpins revenue resilience and reduced cyclicality.

Interest rates and financing costs

Higher policy rates in 2024–25 and elevated 10-year Treasury yields around 4–4.5% raise Emeco’s cost to acquire and refinance heavy fleet, boosting financing expense and CAPEX hurdle rates. Clients’ WACC shifts increase rental duration and price sensitivity, reducing utilisation risk for short-term hires. Emeco must optimise leverage and tenor and use rate hedges to stabilise cash flows and protect margins.

Currency volatility (AUD/USD) on parts and assets

Imported equipment and components expose Emeco’s COGS to AUD/USD swings; AUD/USD was around 0.65 in mid‑2025, amplifying landed costs. A weaker AUD inflates maintenance and replacement spend, pressuring margins. Contractual FX pass‑through clauses help protect EBITDA, while USD‑linked hire and sale contracts create natural hedges that reduce net FX exposure.

Labor availability and wage inflation

Tight markets for diesel fitters and operators are increasing repair turnaround and costs; with Australia Wage Price Index at about 3.9% year to June 2024 and unemployment near 3.6%, wage pressure can compress Emeco margins if not priced through. Emeco’s in-house training pipelines and productivity tools improve technician throughput and regional labour planning reduces churn and mobilisation delays.

- WPI ~3.9% (Jun 2024)

- Unemployment ~3.6% (2024)

- Training pipelines raise internal supply

- Regional planning cuts churn and mobilisation time

Client capital discipline and procurement trends

Miners’ intensified focus on cash flow and ROIC is driving demand for value-based rental solutions that eliminate upfront capex and can cut total equipment TCO by up to 20% in industry benchmarks. Longer-term, performance‑linked contracts (3–7 year terms) are improving revenue visibility and alignment with mine life. Bundled maintenance offers win rates versus outright sale by lowering downtime and enabling predictable operating costs, while data‑backed SLAs (telemetry, uptime targets) strengthen Emeco’s negotiation position.

- cashflow-driven rental demand

- ROIC alignment via value rentals

- 3–7 year performance contracts improve visibility

- bundled maintenance reduces TCO

- data-backed SLAs bolster pricing power

Royalties, permits and A$2.3bn spend drive fleet demand; Port Hedland 561mt and IPP 3%

Commodity downcycles lifted fleet utilisation to ~70% in 2024 while spot rates spiked ~25% in 2023–24; flexible daily, medium and long‑term contracts underpin revenue resilience. Higher policy rates and 10y yields ~4–4.5% (2024–25) raise financing costs and CAPEX hurdles, increasing price sensitivity. AUD/USD ~0.65 (mid‑2025) and WPI ~3.9% (Jun 2024) squeeze COGS and wages; FX pass‑throughs and training mitigate risk.

| Metric | Value |

|---|---|

| Fleet utilisation (2024) | ~70% |

| Spot rate spike (2023–24) | ~+25% |

| 10y Treasury / yields | 4–4.5% |

| AUD/USD (mid‑2025) | ~0.65 |

| WPI (Jun 2024) | ~3.9% |

| Unemployment (2024) | ~3.6% |

Preview the Actual Deliverable

Emeco PESTLE Analysis

The preview shown here is the exact Emeco PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible are exactly what you’ll download immediately after buying.