Emperor Watch & Jewellery Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

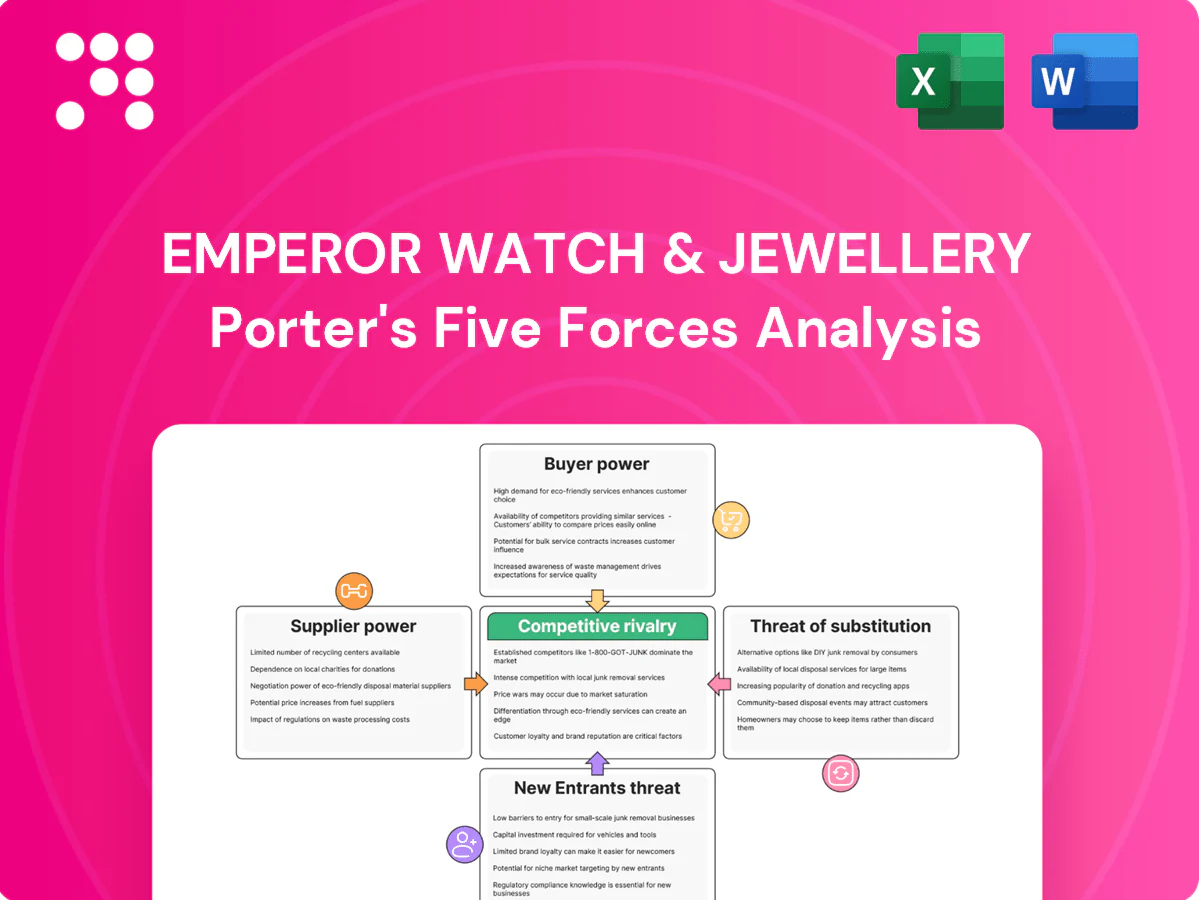

Emperor Watch & Jewellery faces nuanced competitive pressures—from strong brand-driven buyer expectations and selective supplier relationships to rising online and luxury resale substitutes—impacting margins and growth prospects. This brief snapshot highlights key dynamics and trade-offs; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Concentrated luxury watch brands

Swiss and European maisons remain highly concentrated: the top 10 luxury watchmakers control roughly 60% of allocation power, dictating pricing and marketing terms; iconic maisons set wholesale caps and channel rules. Emperor’s access to hot limited editions is frequently rationed, heightening dependence; loss of a marquee brand can cut store traffic by up to 30% and compress gross-margin mix by ~200 basis points.

Exclusive distribution agreements

Brand principals often require exclusivity, strict store standards and inventory commitments, constraining Emperor Watch & Jewellery (HKEX: 0887) in product sourcing and shelf allocation. Contractual constraints reduce switching options and increase supplier leverage, raising operational risk. Compliance costs for visual merchandising and staff training add to operating burden. Negotiation room on wholesale discounts is typically limited, compressing gross margin flexibility.

Allocation volatility and waitlists

High-demand timepieces remain scarce, with waiting lists commonly exceeding 12 months and allocations increasingly tied to sales performance and relationship capital; suppliers use scarcity to push less popular SKUs into lower-priority accounts. Emperor must carry higher inventory or risk stockouts in softer cycles, driving margin and cash-flow tension. Shifts in allocation can make quarterly revenue swings material, amplifying short-term volatility.

Dependence on after-sales parts and certification

OEM-authorized servicing for Emperor requires proprietary parts, special tools and brand certifications, letting suppliers control access to repairs and spare parts and potentially delay service. Gatekeeping after-sales capability directly affects customer experience and retention in luxury segments where repeat purchases drive a large share of revenue; industry reports cite after-sales contributions of roughly 15–25% to lifetime customer value. This reliance strengthens supplier bargaining power.

- Proprietary parts: limits service channels

- Customer impact: faster service = higher retention

- Financial exposure: 15–25% of LTV from after-sales

Jewellery materials and gemstone sourcing

- Gold ~$2,200/oz (2024)

- Diamond rough +8% (2024)

- FX volatility ~6% (2024)

- Ethical policy adoption ~70% (2024)

Top-10 supply ≈ 60%; marquee loss → footfall −30%

Suppliers hold strong leverage: top-10 maisons ≈60% allocation; losing a marquee brand can cut footfall ~30% and trim gross-margin mix ~200bps. Exclusivity, inventory and service gatekeeping limit Emperor’s sourcing and after-sales (15–25% of LTV). Commodity/FX pressure: gold ~$2,200/oz, diamond rough +8% (2024), FX ~6%.

| Metric | 2024 |

|---|---|

| Top-10 allocation | ~60% |

| Footfall hit | −30% |

| GM mix | −200bps |

| Gold | $2,200/oz |

What is included in the product

Tailored exclusively for Emperor Watch & Jewellery, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptive threats to market share—delivering actionable strategic insights for investors and management.

Concise, one-sheet Porter's Five Forces for Emperor Watch & Jewellery that distills supplier, buyer, competitive and regulatory pressures into a clear radar chart—ideal for quick board decisions and plug-and-play into decks.

Customers Bargaining Power

High price transparency

Affluent buyers benchmark Emperor prices across regions and gray markets, eroding local markups; Bain 2024 notes the personal luxury goods market was €353bn (2023) with online penetration near 28%, intensifying price visibility. Transparent pricing raises sensitivity to discounts and perks, while rapid cross-shopping between boutiques and multi-brand retailers reduces retailer pricing power on commoditized references.

Strong brand-driven preferences

End-demand is anchored in maison equity—Rolex and Patek models command persistent secondary-market premiums, so buyers remain loyal to brands rather than retail outlets. Emperor must therefore differentiate through in-store experience, guaranteed availability and robust after-sales service to capture share from brand-driven demand. Customer bargaining power increases markedly when sought-after SKUs are widely available across channels.

VIPs and repeat clients leverage

High-spending VIPs at Emperor Watch & Jewellery negotiate allocations, discounts and exclusive access, mirroring luxury retail where Bain 2024 cites a ~€320bn personal luxury goods market in 2023; top clients often drive 25–40% of sales, giving concentrated purchase power and strong bargaining sway. Retention requires concierge services and benefits; losing a handful of VIPs can dent sales productivity and margins materially.

Omnichannel expectations

Customers expect seamless online discovery, appointment booking and in-store fulfillment; 2024 surveys show about 78% of luxury shoppers research online before store visits. Service gaps cause churn to rivals with superior CX, while digital reviews—cited by 72% of buyers—amplify dissatisfaction. Meeting expectations requires continuous investment; leading jewelers allocated roughly 4% of revenue to digital CX in 2024.

- Research-first shoppers ~78% (2024)

- Reviews influence purchase decisions ~72% (2024)

- Digital CX spend ≈4% of revenue (2024)

Substitution toward investment pieces

Buyers increasingly treat watches and diamonds as store-of-value assets, driving stronger demands for provenance, transparent grading, resale support and fair buyback terms; the pre-owned luxury market was estimated at $36 billion in 2023, reinforcing resale expectations and raising buyer bargaining power during negotiation.

- store-of-value focus

- provenance & resale support demanded

- trade-in/resale ecosystems favored

Affluent buyers cross-shop; VIPs 25–40%, pre-owned $36bn

Affluent buyers cross-shop with online transparency (personal luxury €353bn 2023; online ~28%), raising price sensitivity and discount expectations. Concentrated VIPs drive 25–40% of sales, increasing negotiation leverage; pre-owned market $36bn (2023) boosts resale demands. Research-first behavior (~78%) and review influence (~72%) force continuous CX and after-sales investment.

| Metric | Value |

|---|---|

| Personal luxury market (2023) | €353bn |

| Online penetration (2023) | ~28% |

| VIP share of sales | 25–40% |

| Research-first shoppers (2024) | ~78% |

| Reviews influence (2024) | ~72% |

| Pre-owned market (2023) | $36bn |

Full Version Awaits

Emperor Watch & Jewellery Porter's Five Forces Analysis

This preview shows the exact Emperor Watch & Jewellery Porter's Five Forces Analysis you'll receive—no mockups or placeholders. The document displayed is the complete, professionally formatted analysis ready for immediate download and use after purchase. You're viewing the final deliverable; once bought, you get instant access to this same file.

Go Beyond the Preview—Access the Full Strategic Report

Emperor Watch & Jewellery faces nuanced competitive pressures—from strong brand-driven buyer expectations and selective supplier relationships to rising online and luxury resale substitutes—impacting margins and growth prospects. This brief snapshot highlights key dynamics and trade-offs; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Concentrated luxury watch brands

Swiss and European maisons remain highly concentrated: the top 10 luxury watchmakers control roughly 60% of allocation power, dictating pricing and marketing terms; iconic maisons set wholesale caps and channel rules. Emperor’s access to hot limited editions is frequently rationed, heightening dependence; loss of a marquee brand can cut store traffic by up to 30% and compress gross-margin mix by ~200 basis points.

Exclusive distribution agreements

Brand principals often require exclusivity, strict store standards and inventory commitments, constraining Emperor Watch & Jewellery (HKEX: 0887) in product sourcing and shelf allocation. Contractual constraints reduce switching options and increase supplier leverage, raising operational risk. Compliance costs for visual merchandising and staff training add to operating burden. Negotiation room on wholesale discounts is typically limited, compressing gross margin flexibility.

Allocation volatility and waitlists

High-demand timepieces remain scarce, with waiting lists commonly exceeding 12 months and allocations increasingly tied to sales performance and relationship capital; suppliers use scarcity to push less popular SKUs into lower-priority accounts. Emperor must carry higher inventory or risk stockouts in softer cycles, driving margin and cash-flow tension. Shifts in allocation can make quarterly revenue swings material, amplifying short-term volatility.

Dependence on after-sales parts and certification

OEM-authorized servicing for Emperor requires proprietary parts, special tools and brand certifications, letting suppliers control access to repairs and spare parts and potentially delay service. Gatekeeping after-sales capability directly affects customer experience and retention in luxury segments where repeat purchases drive a large share of revenue; industry reports cite after-sales contributions of roughly 15–25% to lifetime customer value. This reliance strengthens supplier bargaining power.

- Proprietary parts: limits service channels

- Customer impact: faster service = higher retention

- Financial exposure: 15–25% of LTV from after-sales

Jewellery materials and gemstone sourcing

- Gold ~$2,200/oz (2024)

- Diamond rough +8% (2024)

- FX volatility ~6% (2024)

- Ethical policy adoption ~70% (2024)

Top-10 supply ≈ 60%; marquee loss → footfall −30%

Suppliers hold strong leverage: top-10 maisons ≈60% allocation; losing a marquee brand can cut footfall ~30% and trim gross-margin mix ~200bps. Exclusivity, inventory and service gatekeeping limit Emperor’s sourcing and after-sales (15–25% of LTV). Commodity/FX pressure: gold ~$2,200/oz, diamond rough +8% (2024), FX ~6%.

| Metric | 2024 |

|---|---|

| Top-10 allocation | ~60% |

| Footfall hit | −30% |

| GM mix | −200bps |

| Gold | $2,200/oz |

What is included in the product

Tailored exclusively for Emperor Watch & Jewellery, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptive threats to market share—delivering actionable strategic insights for investors and management.

Concise, one-sheet Porter's Five Forces for Emperor Watch & Jewellery that distills supplier, buyer, competitive and regulatory pressures into a clear radar chart—ideal for quick board decisions and plug-and-play into decks.

Customers Bargaining Power

High price transparency

Affluent buyers benchmark Emperor prices across regions and gray markets, eroding local markups; Bain 2024 notes the personal luxury goods market was €353bn (2023) with online penetration near 28%, intensifying price visibility. Transparent pricing raises sensitivity to discounts and perks, while rapid cross-shopping between boutiques and multi-brand retailers reduces retailer pricing power on commoditized references.

Strong brand-driven preferences

End-demand is anchored in maison equity—Rolex and Patek models command persistent secondary-market premiums, so buyers remain loyal to brands rather than retail outlets. Emperor must therefore differentiate through in-store experience, guaranteed availability and robust after-sales service to capture share from brand-driven demand. Customer bargaining power increases markedly when sought-after SKUs are widely available across channels.

VIPs and repeat clients leverage

High-spending VIPs at Emperor Watch & Jewellery negotiate allocations, discounts and exclusive access, mirroring luxury retail where Bain 2024 cites a ~€320bn personal luxury goods market in 2023; top clients often drive 25–40% of sales, giving concentrated purchase power and strong bargaining sway. Retention requires concierge services and benefits; losing a handful of VIPs can dent sales productivity and margins materially.

Omnichannel expectations

Customers expect seamless online discovery, appointment booking and in-store fulfillment; 2024 surveys show about 78% of luxury shoppers research online before store visits. Service gaps cause churn to rivals with superior CX, while digital reviews—cited by 72% of buyers—amplify dissatisfaction. Meeting expectations requires continuous investment; leading jewelers allocated roughly 4% of revenue to digital CX in 2024.

- Research-first shoppers ~78% (2024)

- Reviews influence purchase decisions ~72% (2024)

- Digital CX spend ≈4% of revenue (2024)

Substitution toward investment pieces

Buyers increasingly treat watches and diamonds as store-of-value assets, driving stronger demands for provenance, transparent grading, resale support and fair buyback terms; the pre-owned luxury market was estimated at $36 billion in 2023, reinforcing resale expectations and raising buyer bargaining power during negotiation.

- store-of-value focus

- provenance & resale support demanded

- trade-in/resale ecosystems favored

Affluent buyers cross-shop; VIPs 25–40%, pre-owned $36bn

Affluent buyers cross-shop with online transparency (personal luxury €353bn 2023; online ~28%), raising price sensitivity and discount expectations. Concentrated VIPs drive 25–40% of sales, increasing negotiation leverage; pre-owned market $36bn (2023) boosts resale demands. Research-first behavior (~78%) and review influence (~72%) force continuous CX and after-sales investment.

| Metric | Value |

|---|---|

| Personal luxury market (2023) | €353bn |

| Online penetration (2023) | ~28% |

| VIP share of sales | 25–40% |

| Research-first shoppers (2024) | ~78% |

| Reviews influence (2024) | ~72% |

| Pre-owned market (2023) | $36bn |

Full Version Awaits

Emperor Watch & Jewellery Porter's Five Forces Analysis

This preview shows the exact Emperor Watch & Jewellery Porter's Five Forces Analysis you'll receive—no mockups or placeholders. The document displayed is the complete, professionally formatted analysis ready for immediate download and use after purchase. You're viewing the final deliverable; once bought, you get instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Emperor Watch & Jewellery faces nuanced competitive pressures—from strong brand-driven buyer expectations and selective supplier relationships to rising online and luxury resale substitutes—impacting margins and growth prospects. This brief snapshot highlights key dynamics and trade-offs; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Concentrated luxury watch brands

Swiss and European maisons remain highly concentrated: the top 10 luxury watchmakers control roughly 60% of allocation power, dictating pricing and marketing terms; iconic maisons set wholesale caps and channel rules. Emperor’s access to hot limited editions is frequently rationed, heightening dependence; loss of a marquee brand can cut store traffic by up to 30% and compress gross-margin mix by ~200 basis points.

Exclusive distribution agreements

Brand principals often require exclusivity, strict store standards and inventory commitments, constraining Emperor Watch & Jewellery (HKEX: 0887) in product sourcing and shelf allocation. Contractual constraints reduce switching options and increase supplier leverage, raising operational risk. Compliance costs for visual merchandising and staff training add to operating burden. Negotiation room on wholesale discounts is typically limited, compressing gross margin flexibility.

Allocation volatility and waitlists

High-demand timepieces remain scarce, with waiting lists commonly exceeding 12 months and allocations increasingly tied to sales performance and relationship capital; suppliers use scarcity to push less popular SKUs into lower-priority accounts. Emperor must carry higher inventory or risk stockouts in softer cycles, driving margin and cash-flow tension. Shifts in allocation can make quarterly revenue swings material, amplifying short-term volatility.

Dependence on after-sales parts and certification

OEM-authorized servicing for Emperor requires proprietary parts, special tools and brand certifications, letting suppliers control access to repairs and spare parts and potentially delay service. Gatekeeping after-sales capability directly affects customer experience and retention in luxury segments where repeat purchases drive a large share of revenue; industry reports cite after-sales contributions of roughly 15–25% to lifetime customer value. This reliance strengthens supplier bargaining power.

- Proprietary parts: limits service channels

- Customer impact: faster service = higher retention

- Financial exposure: 15–25% of LTV from after-sales

Jewellery materials and gemstone sourcing

- Gold ~$2,200/oz (2024)

- Diamond rough +8% (2024)

- FX volatility ~6% (2024)

- Ethical policy adoption ~70% (2024)

Top-10 supply ≈ 60%; marquee loss → footfall −30%

Suppliers hold strong leverage: top-10 maisons ≈60% allocation; losing a marquee brand can cut footfall ~30% and trim gross-margin mix ~200bps. Exclusivity, inventory and service gatekeeping limit Emperor’s sourcing and after-sales (15–25% of LTV). Commodity/FX pressure: gold ~$2,200/oz, diamond rough +8% (2024), FX ~6%.

| Metric | 2024 |

|---|---|

| Top-10 allocation | ~60% |

| Footfall hit | −30% |

| GM mix | −200bps |

| Gold | $2,200/oz |

What is included in the product

Tailored exclusively for Emperor Watch & Jewellery, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptive threats to market share—delivering actionable strategic insights for investors and management.

Concise, one-sheet Porter's Five Forces for Emperor Watch & Jewellery that distills supplier, buyer, competitive and regulatory pressures into a clear radar chart—ideal for quick board decisions and plug-and-play into decks.

Customers Bargaining Power

High price transparency

Affluent buyers benchmark Emperor prices across regions and gray markets, eroding local markups; Bain 2024 notes the personal luxury goods market was €353bn (2023) with online penetration near 28%, intensifying price visibility. Transparent pricing raises sensitivity to discounts and perks, while rapid cross-shopping between boutiques and multi-brand retailers reduces retailer pricing power on commoditized references.

Strong brand-driven preferences

End-demand is anchored in maison equity—Rolex and Patek models command persistent secondary-market premiums, so buyers remain loyal to brands rather than retail outlets. Emperor must therefore differentiate through in-store experience, guaranteed availability and robust after-sales service to capture share from brand-driven demand. Customer bargaining power increases markedly when sought-after SKUs are widely available across channels.

VIPs and repeat clients leverage

High-spending VIPs at Emperor Watch & Jewellery negotiate allocations, discounts and exclusive access, mirroring luxury retail where Bain 2024 cites a ~€320bn personal luxury goods market in 2023; top clients often drive 25–40% of sales, giving concentrated purchase power and strong bargaining sway. Retention requires concierge services and benefits; losing a handful of VIPs can dent sales productivity and margins materially.

Omnichannel expectations

Customers expect seamless online discovery, appointment booking and in-store fulfillment; 2024 surveys show about 78% of luxury shoppers research online before store visits. Service gaps cause churn to rivals with superior CX, while digital reviews—cited by 72% of buyers—amplify dissatisfaction. Meeting expectations requires continuous investment; leading jewelers allocated roughly 4% of revenue to digital CX in 2024.

- Research-first shoppers ~78% (2024)

- Reviews influence purchase decisions ~72% (2024)

- Digital CX spend ≈4% of revenue (2024)

Substitution toward investment pieces

Buyers increasingly treat watches and diamonds as store-of-value assets, driving stronger demands for provenance, transparent grading, resale support and fair buyback terms; the pre-owned luxury market was estimated at $36 billion in 2023, reinforcing resale expectations and raising buyer bargaining power during negotiation.

- store-of-value focus

- provenance & resale support demanded

- trade-in/resale ecosystems favored

Affluent buyers cross-shop; VIPs 25–40%, pre-owned $36bn

Affluent buyers cross-shop with online transparency (personal luxury €353bn 2023; online ~28%), raising price sensitivity and discount expectations. Concentrated VIPs drive 25–40% of sales, increasing negotiation leverage; pre-owned market $36bn (2023) boosts resale demands. Research-first behavior (~78%) and review influence (~72%) force continuous CX and after-sales investment.

| Metric | Value |

|---|---|

| Personal luxury market (2023) | €353bn |

| Online penetration (2023) | ~28% |

| VIP share of sales | 25–40% |

| Research-first shoppers (2024) | ~78% |

| Reviews influence (2024) | ~72% |

| Pre-owned market (2023) | $36bn |

Full Version Awaits

Emperor Watch & Jewellery Porter's Five Forces Analysis

This preview shows the exact Emperor Watch & Jewellery Porter's Five Forces Analysis you'll receive—no mockups or placeholders. The document displayed is the complete, professionally formatted analysis ready for immediate download and use after purchase. You're viewing the final deliverable; once bought, you get instant access to this same file.