Enaex Porter's Five Forces Analysis

Don't Miss the Bigger Picture

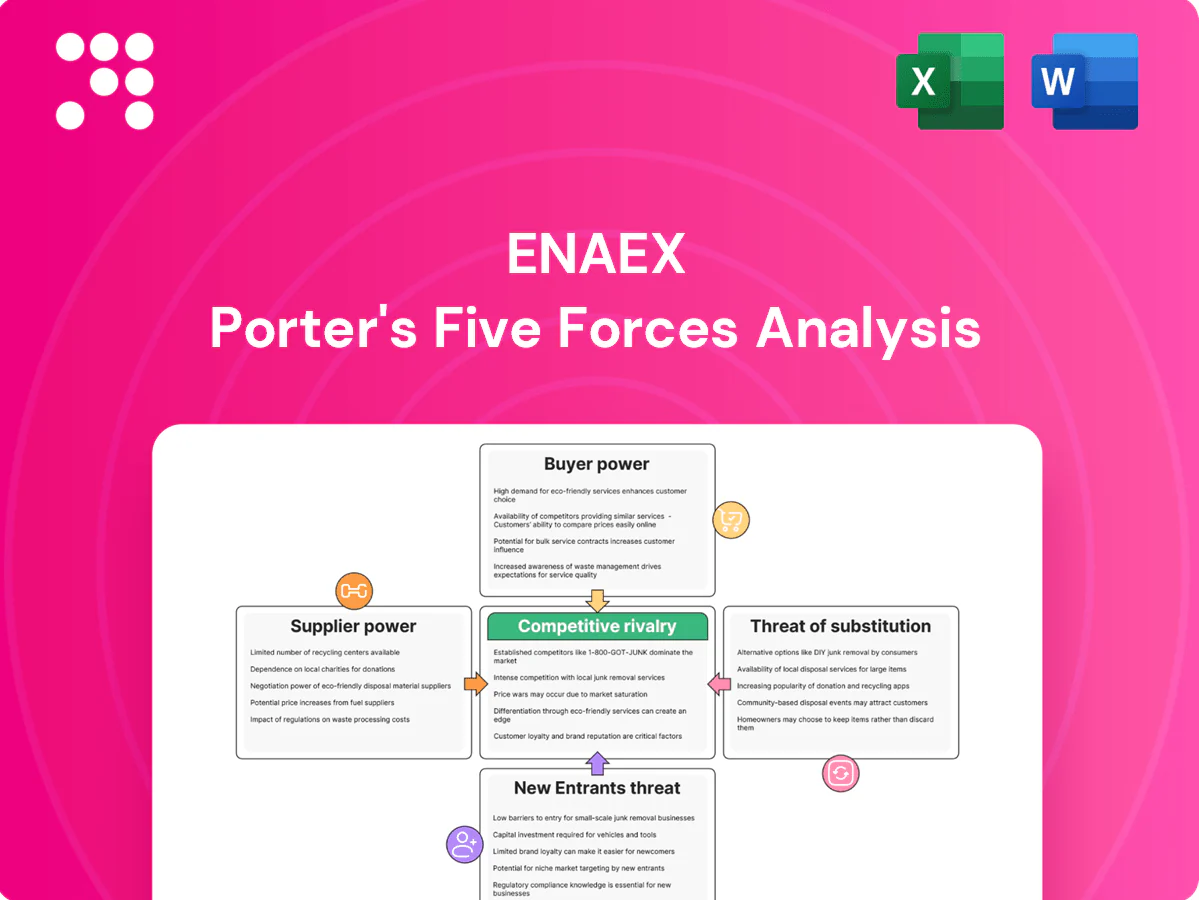

Enaex’s Porter’s Five Forces snapshot highlights concentrated supplier relationships, moderate buyer power, high barriers in explosives manufacturing, and niche substitute threats driven by innovation. Competitive rivalry is shaped by scale and regulatory compliance, impacting margins and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Enaex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical inputs: ammonium nitrate and precursors

Explosives production depends on ammonia, nitric acid, ammonium nitrate, fuels and specialty additives supplied by a small global set of producers, so any disruption or price spike flows directly into COGS. Long-term contracts and vertical integration reduce volatility but cannot fully eliminate feedstock risk. Enaex’s scale and integrated operations strengthen negotiating power, yet concentrated chemical feedstock markets sustain supplier leverage.

Transport and hazardous logistics constraints

Explosives and precursors demand specialized storage, permits and hazmat transport, narrowing carrier options and concentrating supply; the global mining explosives market was estimated at about USD 8.5bn in 2024, intensifying carrier leverage. Route, port and regulatory bottlenecks—especially in major copper producer Chile (≈5.6 Mt copper in 2024)—raise switching costs and boost logistics providers’ influence. On-site emulsion plants lower transport dependence but require significant capex and permitting, while remote mine locations further strengthen logistics suppliers’ position.

Equipment and technology vendors

Equipment and technology vendors for mobile manufacturing units, blast planning software and detonator systems are concentrated among major OEMs such as Epiroc, Sandvik, Atlas Copco, Orica and Enaex, creating concentrated supply channels in 2024. Proprietary standards for detonators and software APIs increase lock-in and vendor power. Mining service contracts drive targets of >95% equipment uptime, heightening dependence on vendors. Strategic partnerships and dual-sourcing are used to dilute vendor leverage.

Energy and utilities exposure

Gas and electricity drive up to 40% of ammonia and nitrate production costs, linking Enaex margins directly to energy markets; 2024 volatility kept cost exposure high. Pass-through to customers can lag due to contract terms, amplifying margin pressure during spikes. Regional utility monopolies in Chile and Peru constrain pricing leverage and can affect supply reliability despite company controls.

- Energy share ~40%

- 2024: elevated volatility

- Utility monopoly risk

- Hedging/diversification mitigates but not eliminates

Regulatory and compliance intermediaries

Regulatory and compliance intermediaries for licensing, security, and environmental testing are often specialized, with 2024 lead times commonly creating critical-path dependencies of 6–12 weeks for certification and site testing; limited accredited providers in some Latin American jurisdictions can be fewer than five, increasing their bargaining power. Building in-house compliance capacity reduces supplier leverage but requires capital and skilled hires.

- Certification lead time: 6–12 weeks

- Accredited providers in some regions: <5

- Trade-off: CAPEX and hiring vs supplier dependence

Concentrated feedstock markets keep supplier leverage high despite hedging

Feedstock markets are concentrated, so ammonia/nitrate price spikes feed directly into COGS despite Enaex’s scale. Energy-linked costs (~40% of ammonia production) and 2024 volatility sustain supplier leverage. Logistics, equipment OEMs and limited certifiers (lead times 6–12 weeks) raise switching costs. Vertical integration and hedging mitigate but do not remove supplier power.

| Metric | 2024 Value |

|---|---|

| Global mining explosives market | USD 8.5bn |

| Chile copper production | ≈5.6 Mt |

| Energy share (ammonia/nitrate) | ~40% |

| Certification lead time | 6–12 weeks |

| Accredited providers (some regions) | <5 |

What is included in the product

Tailored Porter’s Five Forces analysis of Enaex that uncovers key competitive drivers, supplier and buyer power, substitutes and new-entry risks, and identifies disruptive threats to its market share and pricing power.

A concise Enaex Porter's Five Forces one-sheet that pinpoints competitive pressures and removes analysis bottlenecks—ready to customize, share, and drop into investor decks for faster, clearer strategic decisions.

Customers Bargaining Power

Concentrated mining customers

Large global miners purchase explosives and blasting services at scale and secure multi-year contracts, giving them strong negotiating leverage over Enaex. Vendor performance is benchmarked rigorously on cost-per-ton and safety KPIs, with penalties and re-bids common. Consolidation among miners amplifies buyer power and pricing pressure. Enaex counters with integrated blasting, digital optimization and performance-linked pricing to retain long-term contracts.

Switching costs vs multi-sourcing

Operational integration with Enaex—through supply chains, blasting design and on-site services—raises switching frictions, yet many mining clients retain dual suppliers to ensure resilience and continuity. Tender cycles remain a key battleground, provoking tight price competition and extended technical trials that test product and service parity. When Enaex demonstrates measurable productivity gains via improved fragmentation or reduced explosives consumption, customers often lock in share despite price pressure. Service quality, logistics reliability and on-site support are decisive differentiators in final supplier selection.

Price sensitivity through commodity cycles

When metal prices fell in 2024 (copper peak-to-trough volatility ~12%), miners aggressively cut input costs, amplifying buyer power and pushing suppliers like Enaex to offer purchase discounts typically in the 5–10% range. In up-cycles demand tightness eases price pressure but value-for-money remains critical, with indexation and formula pricing (used in ~70% of contracts) tempering spot volatility. Buyers still request concessions; performance penalties and rebates (commonly 1–3% of contract value) are widespread.

Demand for safety and ESG compliance

Buyers demand stringent safety records, quantified emissions reductions and community standards; non-compliance can cause immediate disqualification regardless of price. This elevates certified suppliers and embeds measurable KPIs into negotiations, with CSRD expanding EU reporting to ~50,000 companies by 2024 increasing buyer scrutiny. Superior ESG performance measurably reduces price sensitivity and wins longer contracts.

- Safety & emissions KPIs mandatory

- Non-compliance = disqualification

- Certified suppliers preferred

- CSRD ~50,000 firms (2024)

Preference for end-to-end blasting services

Customers increasingly demand design-to-blast end-to-end services that raise mine productivity, embedding vendors deeper and concentrating spend, which broadens buyer negotiating scope and pressures unit pricing. Outcome-based contracts now shift procurement toward cost-per-rock-broken metrics, prioritizing measurable productivity over input prices. Enaex leverages technical support and digital blasting tools to defend margins by demonstrating measurable productivity gains and reducing variability.

- End-to-end demand increases vendor embedding

- Outcome contracts focus on cost-per-rock-broken

- Enaex technical/digital tools protect margins

Miners force 5-10% discounts; 70% indexation extends contracts

Large global miners with multi-year contracts and consolidation exert strong buyer power, forcing 5–10% average supplier discounts in 2024 and widespread 1–3% performance rebates; ~70% of contracts use indexation. Enaex defends via integrated blasting, digital optimisation and ESG-certified services, securing longer terms when productivity gains exceed 10%.

| Metric | 2024 |

|---|---|

| Avg supplier discount | 5–10% |

| Indexation in contracts | ~70% |

| Performance rebates | 1–3% |

Full Version Awaits

Enaex Porter's Five Forces Analysis

This preview shows the exact Enaex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the professionally written, fully formatted final document, ready to download and use the moment you buy. No surprises—what you see is what you get.

Don't Miss the Bigger Picture

Enaex’s Porter’s Five Forces snapshot highlights concentrated supplier relationships, moderate buyer power, high barriers in explosives manufacturing, and niche substitute threats driven by innovation. Competitive rivalry is shaped by scale and regulatory compliance, impacting margins and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Enaex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical inputs: ammonium nitrate and precursors

Explosives production depends on ammonia, nitric acid, ammonium nitrate, fuels and specialty additives supplied by a small global set of producers, so any disruption or price spike flows directly into COGS. Long-term contracts and vertical integration reduce volatility but cannot fully eliminate feedstock risk. Enaex’s scale and integrated operations strengthen negotiating power, yet concentrated chemical feedstock markets sustain supplier leverage.

Transport and hazardous logistics constraints

Explosives and precursors demand specialized storage, permits and hazmat transport, narrowing carrier options and concentrating supply; the global mining explosives market was estimated at about USD 8.5bn in 2024, intensifying carrier leverage. Route, port and regulatory bottlenecks—especially in major copper producer Chile (≈5.6 Mt copper in 2024)—raise switching costs and boost logistics providers’ influence. On-site emulsion plants lower transport dependence but require significant capex and permitting, while remote mine locations further strengthen logistics suppliers’ position.

Equipment and technology vendors

Equipment and technology vendors for mobile manufacturing units, blast planning software and detonator systems are concentrated among major OEMs such as Epiroc, Sandvik, Atlas Copco, Orica and Enaex, creating concentrated supply channels in 2024. Proprietary standards for detonators and software APIs increase lock-in and vendor power. Mining service contracts drive targets of >95% equipment uptime, heightening dependence on vendors. Strategic partnerships and dual-sourcing are used to dilute vendor leverage.

Energy and utilities exposure

Gas and electricity drive up to 40% of ammonia and nitrate production costs, linking Enaex margins directly to energy markets; 2024 volatility kept cost exposure high. Pass-through to customers can lag due to contract terms, amplifying margin pressure during spikes. Regional utility monopolies in Chile and Peru constrain pricing leverage and can affect supply reliability despite company controls.

- Energy share ~40%

- 2024: elevated volatility

- Utility monopoly risk

- Hedging/diversification mitigates but not eliminates

Regulatory and compliance intermediaries

Regulatory and compliance intermediaries for licensing, security, and environmental testing are often specialized, with 2024 lead times commonly creating critical-path dependencies of 6–12 weeks for certification and site testing; limited accredited providers in some Latin American jurisdictions can be fewer than five, increasing their bargaining power. Building in-house compliance capacity reduces supplier leverage but requires capital and skilled hires.

- Certification lead time: 6–12 weeks

- Accredited providers in some regions: <5

- Trade-off: CAPEX and hiring vs supplier dependence

Concentrated feedstock markets keep supplier leverage high despite hedging

Feedstock markets are concentrated, so ammonia/nitrate price spikes feed directly into COGS despite Enaex’s scale. Energy-linked costs (~40% of ammonia production) and 2024 volatility sustain supplier leverage. Logistics, equipment OEMs and limited certifiers (lead times 6–12 weeks) raise switching costs. Vertical integration and hedging mitigate but do not remove supplier power.

| Metric | 2024 Value |

|---|---|

| Global mining explosives market | USD 8.5bn |

| Chile copper production | ≈5.6 Mt |

| Energy share (ammonia/nitrate) | ~40% |

| Certification lead time | 6–12 weeks |

| Accredited providers (some regions) | <5 |

What is included in the product

Tailored Porter’s Five Forces analysis of Enaex that uncovers key competitive drivers, supplier and buyer power, substitutes and new-entry risks, and identifies disruptive threats to its market share and pricing power.

A concise Enaex Porter's Five Forces one-sheet that pinpoints competitive pressures and removes analysis bottlenecks—ready to customize, share, and drop into investor decks for faster, clearer strategic decisions.

Customers Bargaining Power

Concentrated mining customers

Large global miners purchase explosives and blasting services at scale and secure multi-year contracts, giving them strong negotiating leverage over Enaex. Vendor performance is benchmarked rigorously on cost-per-ton and safety KPIs, with penalties and re-bids common. Consolidation among miners amplifies buyer power and pricing pressure. Enaex counters with integrated blasting, digital optimization and performance-linked pricing to retain long-term contracts.

Switching costs vs multi-sourcing

Operational integration with Enaex—through supply chains, blasting design and on-site services—raises switching frictions, yet many mining clients retain dual suppliers to ensure resilience and continuity. Tender cycles remain a key battleground, provoking tight price competition and extended technical trials that test product and service parity. When Enaex demonstrates measurable productivity gains via improved fragmentation or reduced explosives consumption, customers often lock in share despite price pressure. Service quality, logistics reliability and on-site support are decisive differentiators in final supplier selection.

Price sensitivity through commodity cycles

When metal prices fell in 2024 (copper peak-to-trough volatility ~12%), miners aggressively cut input costs, amplifying buyer power and pushing suppliers like Enaex to offer purchase discounts typically in the 5–10% range. In up-cycles demand tightness eases price pressure but value-for-money remains critical, with indexation and formula pricing (used in ~70% of contracts) tempering spot volatility. Buyers still request concessions; performance penalties and rebates (commonly 1–3% of contract value) are widespread.

Demand for safety and ESG compliance

Buyers demand stringent safety records, quantified emissions reductions and community standards; non-compliance can cause immediate disqualification regardless of price. This elevates certified suppliers and embeds measurable KPIs into negotiations, with CSRD expanding EU reporting to ~50,000 companies by 2024 increasing buyer scrutiny. Superior ESG performance measurably reduces price sensitivity and wins longer contracts.

- Safety & emissions KPIs mandatory

- Non-compliance = disqualification

- Certified suppliers preferred

- CSRD ~50,000 firms (2024)

Preference for end-to-end blasting services

Customers increasingly demand design-to-blast end-to-end services that raise mine productivity, embedding vendors deeper and concentrating spend, which broadens buyer negotiating scope and pressures unit pricing. Outcome-based contracts now shift procurement toward cost-per-rock-broken metrics, prioritizing measurable productivity over input prices. Enaex leverages technical support and digital blasting tools to defend margins by demonstrating measurable productivity gains and reducing variability.

- End-to-end demand increases vendor embedding

- Outcome contracts focus on cost-per-rock-broken

- Enaex technical/digital tools protect margins

Miners force 5-10% discounts; 70% indexation extends contracts

Large global miners with multi-year contracts and consolidation exert strong buyer power, forcing 5–10% average supplier discounts in 2024 and widespread 1–3% performance rebates; ~70% of contracts use indexation. Enaex defends via integrated blasting, digital optimisation and ESG-certified services, securing longer terms when productivity gains exceed 10%.

| Metric | 2024 |

|---|---|

| Avg supplier discount | 5–10% |

| Indexation in contracts | ~70% |

| Performance rebates | 1–3% |

Full Version Awaits

Enaex Porter's Five Forces Analysis

This preview shows the exact Enaex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the professionally written, fully formatted final document, ready to download and use the moment you buy. No surprises—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Enaex’s Porter’s Five Forces snapshot highlights concentrated supplier relationships, moderate buyer power, high barriers in explosives manufacturing, and niche substitute threats driven by innovation. Competitive rivalry is shaped by scale and regulatory compliance, impacting margins and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Enaex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical inputs: ammonium nitrate and precursors

Explosives production depends on ammonia, nitric acid, ammonium nitrate, fuels and specialty additives supplied by a small global set of producers, so any disruption or price spike flows directly into COGS. Long-term contracts and vertical integration reduce volatility but cannot fully eliminate feedstock risk. Enaex’s scale and integrated operations strengthen negotiating power, yet concentrated chemical feedstock markets sustain supplier leverage.

Transport and hazardous logistics constraints

Explosives and precursors demand specialized storage, permits and hazmat transport, narrowing carrier options and concentrating supply; the global mining explosives market was estimated at about USD 8.5bn in 2024, intensifying carrier leverage. Route, port and regulatory bottlenecks—especially in major copper producer Chile (≈5.6 Mt copper in 2024)—raise switching costs and boost logistics providers’ influence. On-site emulsion plants lower transport dependence but require significant capex and permitting, while remote mine locations further strengthen logistics suppliers’ position.

Equipment and technology vendors

Equipment and technology vendors for mobile manufacturing units, blast planning software and detonator systems are concentrated among major OEMs such as Epiroc, Sandvik, Atlas Copco, Orica and Enaex, creating concentrated supply channels in 2024. Proprietary standards for detonators and software APIs increase lock-in and vendor power. Mining service contracts drive targets of >95% equipment uptime, heightening dependence on vendors. Strategic partnerships and dual-sourcing are used to dilute vendor leverage.

Energy and utilities exposure

Gas and electricity drive up to 40% of ammonia and nitrate production costs, linking Enaex margins directly to energy markets; 2024 volatility kept cost exposure high. Pass-through to customers can lag due to contract terms, amplifying margin pressure during spikes. Regional utility monopolies in Chile and Peru constrain pricing leverage and can affect supply reliability despite company controls.

- Energy share ~40%

- 2024: elevated volatility

- Utility monopoly risk

- Hedging/diversification mitigates but not eliminates

Regulatory and compliance intermediaries

Regulatory and compliance intermediaries for licensing, security, and environmental testing are often specialized, with 2024 lead times commonly creating critical-path dependencies of 6–12 weeks for certification and site testing; limited accredited providers in some Latin American jurisdictions can be fewer than five, increasing their bargaining power. Building in-house compliance capacity reduces supplier leverage but requires capital and skilled hires.

- Certification lead time: 6–12 weeks

- Accredited providers in some regions: <5

- Trade-off: CAPEX and hiring vs supplier dependence

Concentrated feedstock markets keep supplier leverage high despite hedging

Feedstock markets are concentrated, so ammonia/nitrate price spikes feed directly into COGS despite Enaex’s scale. Energy-linked costs (~40% of ammonia production) and 2024 volatility sustain supplier leverage. Logistics, equipment OEMs and limited certifiers (lead times 6–12 weeks) raise switching costs. Vertical integration and hedging mitigate but do not remove supplier power.

| Metric | 2024 Value |

|---|---|

| Global mining explosives market | USD 8.5bn |

| Chile copper production | ≈5.6 Mt |

| Energy share (ammonia/nitrate) | ~40% |

| Certification lead time | 6–12 weeks |

| Accredited providers (some regions) | <5 |

What is included in the product

Tailored Porter’s Five Forces analysis of Enaex that uncovers key competitive drivers, supplier and buyer power, substitutes and new-entry risks, and identifies disruptive threats to its market share and pricing power.

A concise Enaex Porter's Five Forces one-sheet that pinpoints competitive pressures and removes analysis bottlenecks—ready to customize, share, and drop into investor decks for faster, clearer strategic decisions.

Customers Bargaining Power

Concentrated mining customers

Large global miners purchase explosives and blasting services at scale and secure multi-year contracts, giving them strong negotiating leverage over Enaex. Vendor performance is benchmarked rigorously on cost-per-ton and safety KPIs, with penalties and re-bids common. Consolidation among miners amplifies buyer power and pricing pressure. Enaex counters with integrated blasting, digital optimization and performance-linked pricing to retain long-term contracts.

Switching costs vs multi-sourcing

Operational integration with Enaex—through supply chains, blasting design and on-site services—raises switching frictions, yet many mining clients retain dual suppliers to ensure resilience and continuity. Tender cycles remain a key battleground, provoking tight price competition and extended technical trials that test product and service parity. When Enaex demonstrates measurable productivity gains via improved fragmentation or reduced explosives consumption, customers often lock in share despite price pressure. Service quality, logistics reliability and on-site support are decisive differentiators in final supplier selection.

Price sensitivity through commodity cycles

When metal prices fell in 2024 (copper peak-to-trough volatility ~12%), miners aggressively cut input costs, amplifying buyer power and pushing suppliers like Enaex to offer purchase discounts typically in the 5–10% range. In up-cycles demand tightness eases price pressure but value-for-money remains critical, with indexation and formula pricing (used in ~70% of contracts) tempering spot volatility. Buyers still request concessions; performance penalties and rebates (commonly 1–3% of contract value) are widespread.

Demand for safety and ESG compliance

Buyers demand stringent safety records, quantified emissions reductions and community standards; non-compliance can cause immediate disqualification regardless of price. This elevates certified suppliers and embeds measurable KPIs into negotiations, with CSRD expanding EU reporting to ~50,000 companies by 2024 increasing buyer scrutiny. Superior ESG performance measurably reduces price sensitivity and wins longer contracts.

- Safety & emissions KPIs mandatory

- Non-compliance = disqualification

- Certified suppliers preferred

- CSRD ~50,000 firms (2024)

Preference for end-to-end blasting services

Customers increasingly demand design-to-blast end-to-end services that raise mine productivity, embedding vendors deeper and concentrating spend, which broadens buyer negotiating scope and pressures unit pricing. Outcome-based contracts now shift procurement toward cost-per-rock-broken metrics, prioritizing measurable productivity over input prices. Enaex leverages technical support and digital blasting tools to defend margins by demonstrating measurable productivity gains and reducing variability.

- End-to-end demand increases vendor embedding

- Outcome contracts focus on cost-per-rock-broken

- Enaex technical/digital tools protect margins

Miners force 5-10% discounts; 70% indexation extends contracts

Large global miners with multi-year contracts and consolidation exert strong buyer power, forcing 5–10% average supplier discounts in 2024 and widespread 1–3% performance rebates; ~70% of contracts use indexation. Enaex defends via integrated blasting, digital optimisation and ESG-certified services, securing longer terms when productivity gains exceed 10%.

| Metric | 2024 |

|---|---|

| Avg supplier discount | 5–10% |

| Indexation in contracts | ~70% |

| Performance rebates | 1–3% |

Full Version Awaits

Enaex Porter's Five Forces Analysis

This preview shows the exact Enaex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the professionally written, fully formatted final document, ready to download and use the moment you buy. No surprises—what you see is what you get.